Fidelis Insurance Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

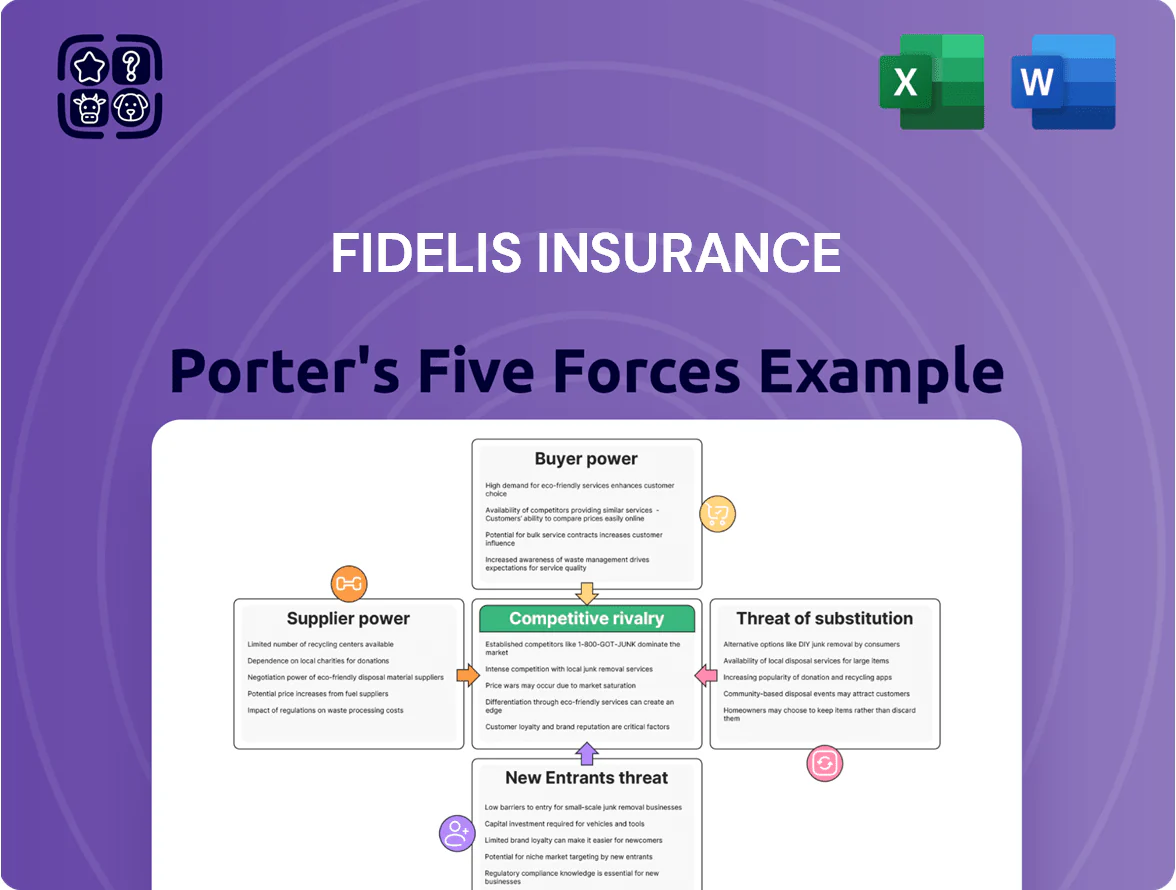

Fidelis Insurance faces moderate buyer power and rising competitive intensity from insurtechs and established carriers, while regulatory complexity and high capital requirements limit new entrants; supplier leverage and substitute threats remain manageable but warrant monitoring. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Fidelis Insurance’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Retrocessional Reinsurance Capacity

As of late 2025, global retrocessional capacity tightened after 2023-24 catastrophe losses, making retrocession a key supply constraint for Fidelis; broker reports show a ~12% reduction in available capacity among top ten retrocessionaires versus 2022.

If top-tier retrocessionaires hike rates by 20–40% (market mid-2025 pricing), Fidelis’s reinsurance spend rises materially, squeezing underwriting margins and raising combined ratios.

Fidelis’s dependency means pricing power sits with a few global players; in 2024 Fidelis ceded roughly 18% of net written premium to retrocessional cover, so cost shifts transmit directly to its P&L.

Specialist Underwriting Talent

The split between Fidelis Insurance Group and Fidelis MGU makes specialist underwriting talent a strategic bottleneck, since human capital drives underwriting authority and deal flow.

Elite underwriters in niche lines (aerospace, political risk) command high demand; Mercer found 2024 median sign-on bonuses for senior specialty underwriters rose 18% year-over-year, boosting their leverage.

To retain them, Fidelis must offer aggressive pay and carry: competitor packages reached total compensation of $400k–$1.2M in 2024 for top talent, so failure to match raises attrition risk and market-share loss.

Data and Analytics Vendors

Modern specialty insurance relies on climate and catastrophe models from a handful of vendors (e.g., RMS, AIR Worldwide, CoreLogic), giving them outsized leverage over Fidelis’s pricing and risk management; vendor model updates sway loss estimates by 10–30% per event, per industry studies through 2024.

Capital Market Investors

- Public markets set cost of capital—key growth limiter

- Typical insurer ROE targets 10–15% guide risk/dividends

- 2024–25 rate volatility raised borrowing cost ~120 bps

- Wider credit spreads (≈80 bps) constrain underwriting expansion

Financial Strength Ratings Agencies

Agencies such as A.M. Best and S&P act as essential suppliers of creditworthiness that let Fidelis underwrite global commercial and reinsurance deals; a downgrade would curtail access to large cedents and Lloyd’s syndicates.

In 2025 the median A.M. Best rating for mid-size specialty insurers was A−; a one-notch fall typically raises reinsurance costs by ~50–150 bps and can cut new treaty flows by 20–40% within 12 months.

- Ratings prerequisite for major contracts

- One-notch downgrade → +0.50–1.50% reinsurance cost

- Downgrade can reduce treaty inflows 20–40% in 12 months

Supplier squeeze drives higher reinsurance costs and talent pay, pressuring Fidelis margins

Suppliers (reinsurers, retrocessionaires, model vendors, talent, and capital providers) hold substantial leverage over Fidelis: 2024–25 capacity cuts (~12% vs 2022) and retrocession rate hikes (20–40%) raise reinsurance costs and squeeze combined ratios; Fidelis ceded ~18% of NWP in 2024. Talent pay rose ~18% sign-on; top underwriter total comp hit $400k–$1.2M. One-notch rating downgrades add ~50–150 bps reinsurance cost and can cut treaty inflows 20–40% within 12 months.

| Supplier | Key metric | Impact on Fidelis |

|---|---|---|

| Retrocessional capacity | −12% vs 2022 | Higher rates, tighter limits |

| Reinsurance pricing | +20–40% (mid‑2025) | Raises underwriting cost |

| Ceded premium | 18% of NWP (2024) | Direct P&L sensitivity |

| Talent pay | +18% sign‑on (2024) | Higher retention cost |

| Ratings | One‑notch → +50–150 bps | Less treaty flow, higher cost |

What is included in the product

Tailored Porter's Five Forces analysis for Fidelis Insurance, uncovering competitive drivers, buyer and supplier power, entry barriers, substitutes, and disruptive threats to assess pricing power and long-term profitability—fully editable for reports and presentations.

A concise, one-sheet Porter's Five Forces view for Fidelis Insurance—quickly spot competitive pressures and tailor risk-mitigation strategies for underwriting, distribution, and pricing.

Customers Bargaining Power

Global Brokerage Dominance

A small group of global brokers—Marsh, Aon, and Guy Carpenter—control roughly 60–70% of specialty submissions worldwide, channeling placement flow and driving pricing and coverage terms; they negotiate on behalf of clients with combined 2024 brokerage revenues exceeding $40bn, so their leverage is high. Fidelis must invest in distributor relationships, offer competitive commission structures, and demonstrate capacity for $50m+ single-risk limits to stay a preferred carrier for high-value risks.

Corporate Risk Manager Sophistication

Corporate clients of Fidelis are large firms with seasoned risk teams that run in-house stochastic models and scenario analyses; a 2024 Willis Towers Watson survey found 62% of global risk managers use proprietary models for placement decisions. These buyers benchmark policy wording, exclusions, and pricing across markets, often comparing offers from Lloyds, Bermuda carriers, and global reinsurers. Their analytical depth and access to market data concentrate bargaining power at annual renewals, forcing carriers to refine terms or risk a 5–12% premium reduction seen in competitive markets in 2023.

Price Sensitivity in Evolving Markets

As the insurance cycle nears 2026, rising market capital (global reinsurance capacity up 8% in 2024 to $700bn per Aon) will increase buyer price sensitivity; insureds will push harder on premiums if specialty rates soften. If specialty pricing drops—Lloyd’s specialty rate index fell 6% in 2024—customers will use multiple quotes to negotiate lower rates. Fidelis must prove superior claims payout ratios (keep combined ratio under 95%) or offer distinct coverage features to protect pricing integrity.

Switching Costs for Specialty Lines

- Standardized lines: low switching cost, high buyer power

- Bespoke lines: higher switching cost, stronger loyalty

- Financial instability: overrides switching costs, prompts exits

- 2024 reinsurance market: ~$370bn ceded premiums

Alternative Risk Retention Strategies

Many corporate clients raised self-insured retentions (SIRs) after 2020 rate spikes; by 2024 about 38% of large US firms increased SIRs or used captives, cutting commercial premium spend by an estimated $4.2bn annually.

This ability to keep risk on the balance sheet gives buyers leverage to push prices and terms; Fidelis must beat the internal cost of risk transfer, typically 8–12% annualized for captive programs.

- 38% large firms increased SIRs by 2024

- $4.2bn annual premium shift

- Internal cost of risk 8–12% pa

- Fidelis must offer net savings vs captive

Fidelis must offer $50M+ limits, beat 8–12% captive cost and hit <95% CR

Buyers hold high leverage: global brokers (Marsh, Aon, Guy Carpenter) control 60–70% of specialty flow, 2024 brokerage revenues >$40bn, and corporates use proprietary models (62% per 2024 WTW) to drive renewals; market capacity rose 8% to ~$700bn in 2024, increasing price pressure. Fidelis must offer >$50m limits, maintain combined ratio <95%, and beat captive/internal cost of risk (8–12%) to retain clients.

| Metric | 2024/2025 |

|---|---|

| Broker share (Marsh/Aon/Guy Carpenter) | 60–70% |

| Brokerage revenues | >$40bn (2024) |

| Global reinsurance capacity | $700bn (+8% YoY, 2024) |

| Clients using proprietary models | 62% (WTW 2024) |

| Required single-risk capacity | $50m+ |

| Target combined ratio | <95% |

| Internal cost of risk (captives) | 8–12% pa |

Full Version Awaits

Fidelis Insurance Porter's Five Forces Analysis

This preview shows the exact Fidelis Insurance Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full, professionally formatted file you’ll get—ready for download and use the moment you buy.

You're viewing the actual deliverable; once your purchase is complete, you’ll have instant access to this same analysis, fully ready for your needs.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Fidelis Insurance faces moderate buyer power and rising competitive intensity from insurtechs and established carriers, while regulatory complexity and high capital requirements limit new entrants; supplier leverage and substitute threats remain manageable but warrant monitoring. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Fidelis Insurance’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Retrocessional Reinsurance Capacity

As of late 2025, global retrocessional capacity tightened after 2023-24 catastrophe losses, making retrocession a key supply constraint for Fidelis; broker reports show a ~12% reduction in available capacity among top ten retrocessionaires versus 2022.

If top-tier retrocessionaires hike rates by 20–40% (market mid-2025 pricing), Fidelis’s reinsurance spend rises materially, squeezing underwriting margins and raising combined ratios.

Fidelis’s dependency means pricing power sits with a few global players; in 2024 Fidelis ceded roughly 18% of net written premium to retrocessional cover, so cost shifts transmit directly to its P&L.

Specialist Underwriting Talent

The split between Fidelis Insurance Group and Fidelis MGU makes specialist underwriting talent a strategic bottleneck, since human capital drives underwriting authority and deal flow.

Elite underwriters in niche lines (aerospace, political risk) command high demand; Mercer found 2024 median sign-on bonuses for senior specialty underwriters rose 18% year-over-year, boosting their leverage.

To retain them, Fidelis must offer aggressive pay and carry: competitor packages reached total compensation of $400k–$1.2M in 2024 for top talent, so failure to match raises attrition risk and market-share loss.

Data and Analytics Vendors

Modern specialty insurance relies on climate and catastrophe models from a handful of vendors (e.g., RMS, AIR Worldwide, CoreLogic), giving them outsized leverage over Fidelis’s pricing and risk management; vendor model updates sway loss estimates by 10–30% per event, per industry studies through 2024.

Capital Market Investors

- Public markets set cost of capital—key growth limiter

- Typical insurer ROE targets 10–15% guide risk/dividends

- 2024–25 rate volatility raised borrowing cost ~120 bps

- Wider credit spreads (≈80 bps) constrain underwriting expansion

Financial Strength Ratings Agencies

Agencies such as A.M. Best and S&P act as essential suppliers of creditworthiness that let Fidelis underwrite global commercial and reinsurance deals; a downgrade would curtail access to large cedents and Lloyd’s syndicates.

In 2025 the median A.M. Best rating for mid-size specialty insurers was A−; a one-notch fall typically raises reinsurance costs by ~50–150 bps and can cut new treaty flows by 20–40% within 12 months.

- Ratings prerequisite for major contracts

- One-notch downgrade → +0.50–1.50% reinsurance cost

- Downgrade can reduce treaty inflows 20–40% in 12 months

Supplier squeeze drives higher reinsurance costs and talent pay, pressuring Fidelis margins

Suppliers (reinsurers, retrocessionaires, model vendors, talent, and capital providers) hold substantial leverage over Fidelis: 2024–25 capacity cuts (~12% vs 2022) and retrocession rate hikes (20–40%) raise reinsurance costs and squeeze combined ratios; Fidelis ceded ~18% of NWP in 2024. Talent pay rose ~18% sign-on; top underwriter total comp hit $400k–$1.2M. One-notch rating downgrades add ~50–150 bps reinsurance cost and can cut treaty inflows 20–40% within 12 months.

| Supplier | Key metric | Impact on Fidelis |

|---|---|---|

| Retrocessional capacity | −12% vs 2022 | Higher rates, tighter limits |

| Reinsurance pricing | +20–40% (mid‑2025) | Raises underwriting cost |

| Ceded premium | 18% of NWP (2024) | Direct P&L sensitivity |

| Talent pay | +18% sign‑on (2024) | Higher retention cost |

| Ratings | One‑notch → +50–150 bps | Less treaty flow, higher cost |

What is included in the product

Tailored Porter's Five Forces analysis for Fidelis Insurance, uncovering competitive drivers, buyer and supplier power, entry barriers, substitutes, and disruptive threats to assess pricing power and long-term profitability—fully editable for reports and presentations.

A concise, one-sheet Porter's Five Forces view for Fidelis Insurance—quickly spot competitive pressures and tailor risk-mitigation strategies for underwriting, distribution, and pricing.

Customers Bargaining Power

Global Brokerage Dominance

A small group of global brokers—Marsh, Aon, and Guy Carpenter—control roughly 60–70% of specialty submissions worldwide, channeling placement flow and driving pricing and coverage terms; they negotiate on behalf of clients with combined 2024 brokerage revenues exceeding $40bn, so their leverage is high. Fidelis must invest in distributor relationships, offer competitive commission structures, and demonstrate capacity for $50m+ single-risk limits to stay a preferred carrier for high-value risks.

Corporate Risk Manager Sophistication

Corporate clients of Fidelis are large firms with seasoned risk teams that run in-house stochastic models and scenario analyses; a 2024 Willis Towers Watson survey found 62% of global risk managers use proprietary models for placement decisions. These buyers benchmark policy wording, exclusions, and pricing across markets, often comparing offers from Lloyds, Bermuda carriers, and global reinsurers. Their analytical depth and access to market data concentrate bargaining power at annual renewals, forcing carriers to refine terms or risk a 5–12% premium reduction seen in competitive markets in 2023.

Price Sensitivity in Evolving Markets

As the insurance cycle nears 2026, rising market capital (global reinsurance capacity up 8% in 2024 to $700bn per Aon) will increase buyer price sensitivity; insureds will push harder on premiums if specialty rates soften. If specialty pricing drops—Lloyd’s specialty rate index fell 6% in 2024—customers will use multiple quotes to negotiate lower rates. Fidelis must prove superior claims payout ratios (keep combined ratio under 95%) or offer distinct coverage features to protect pricing integrity.

Switching Costs for Specialty Lines

- Standardized lines: low switching cost, high buyer power

- Bespoke lines: higher switching cost, stronger loyalty

- Financial instability: overrides switching costs, prompts exits

- 2024 reinsurance market: ~$370bn ceded premiums

Alternative Risk Retention Strategies

Many corporate clients raised self-insured retentions (SIRs) after 2020 rate spikes; by 2024 about 38% of large US firms increased SIRs or used captives, cutting commercial premium spend by an estimated $4.2bn annually.

This ability to keep risk on the balance sheet gives buyers leverage to push prices and terms; Fidelis must beat the internal cost of risk transfer, typically 8–12% annualized for captive programs.

- 38% large firms increased SIRs by 2024

- $4.2bn annual premium shift

- Internal cost of risk 8–12% pa

- Fidelis must offer net savings vs captive

Fidelis must offer $50M+ limits, beat 8–12% captive cost and hit <95% CR

Buyers hold high leverage: global brokers (Marsh, Aon, Guy Carpenter) control 60–70% of specialty flow, 2024 brokerage revenues >$40bn, and corporates use proprietary models (62% per 2024 WTW) to drive renewals; market capacity rose 8% to ~$700bn in 2024, increasing price pressure. Fidelis must offer >$50m limits, maintain combined ratio <95%, and beat captive/internal cost of risk (8–12%) to retain clients.

| Metric | 2024/2025 |

|---|---|

| Broker share (Marsh/Aon/Guy Carpenter) | 60–70% |

| Brokerage revenues | >$40bn (2024) |

| Global reinsurance capacity | $700bn (+8% YoY, 2024) |

| Clients using proprietary models | 62% (WTW 2024) |

| Required single-risk capacity | $50m+ |

| Target combined ratio | <95% |

| Internal cost of risk (captives) | 8–12% pa |

Full Version Awaits

Fidelis Insurance Porter's Five Forces Analysis

This preview shows the exact Fidelis Insurance Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full, professionally formatted file you’ll get—ready for download and use the moment you buy.

You're viewing the actual deliverable; once your purchase is complete, you’ll have instant access to this same analysis, fully ready for your needs.