First Quantum Minerals Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

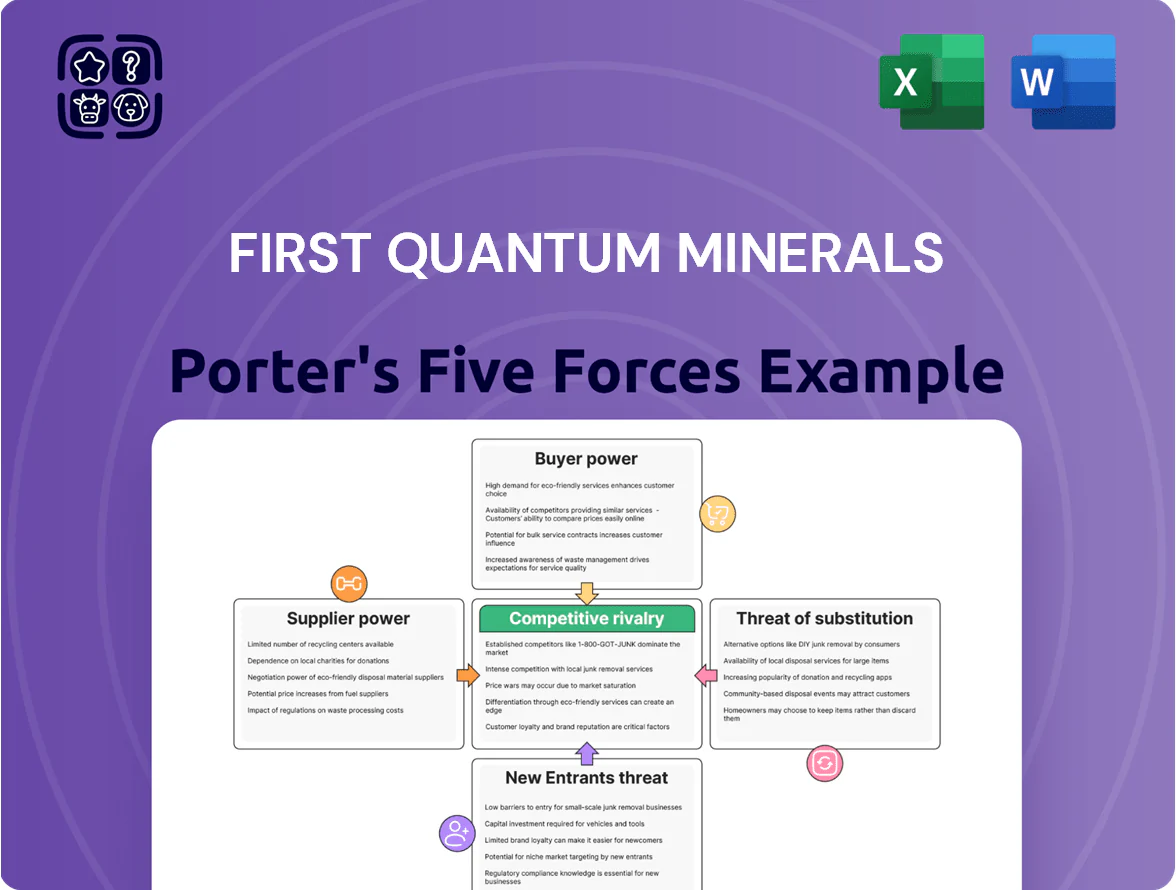

First Quantum Minerals faces strong rivalry from large diversified miners, significant supplier leverage for specialized equipment and inputs, and moderate buyer power driven by concentrate markets—while capital intensity and regulatory barriers limit new entrants and substitution risk remains low for key metals.

Suppliers Bargaining Power

Concentration of Specialized Equipment Providers

The mining sector depends on a few global makers for large earthmoving and processing kit; Caterpillar and Komatsu hold outsized power because products are specialized and replacement lead times exceed 12–18 months, raising vendor leverage.

For First Quantum Minerals, concentrated suppliers make equipment prices and maintenance contracts largely non-negotiable, pushing 2024 capex pressure—company spent US$1.2bn on sustaining and growth capex in 2024.

First Quantum’s scale helps in talks, but the technical complexity of automated fleets and long OEM support cycles keep bargaining power tilted toward manufacturers, limiting cost-flexibility.

Energy Dependency and Utility Providers

Mining is energy-heavy—First Quantum Minerals used ~4.3 TWh of electricity across operations in 2024, driving high costs for mills and haulage.

In Zambia Q4 2024, state-owned ZESCO's limited competition constrains First Quantum's rate negotiations, raising supplier leverage.

Fuel price swings (Brent averaged $88/bbl in 2024) directly raised diesel costs; short-term alternatives for heavy equipment are limited.

FQM is investing in on-site renewables (projects target ~250 MW by 2027) to cut exposure, but market price shocks still pose material risk.

Labor Unions and Skilled Workforce Availability

Labor bargaining power is high for First Quantum Minerals in jurisdictions with strong unions; collective agreements in 2024-25 raised labor costs by ~6-9% at some Canadian and Zambian sites, and strikes risk month-long output losses.

Advanced automation raises demand for specialized technicians, boosting wage premia for controls engineers and electricians by ~10-15%, shifting leverage to skilled staff.

Global shortages of experienced mining engineers and geologists—ILO estimates show a 12% supply gap in 2024—strengthen worker negotiating power and recruitment costs for First Quantum.

Consumables and Chemical Reagents

Consumables like reagents, explosives and grinding media are vital for First Quantum Minerals’ (FQM) copper and nickel processing; global ammonia and steel price spikes in 2024 raised reagent-related input costs ~8–12% for the mining sector, boosting FQM’s site operating costs in 2024 by an estimated mid-single digits percent.

More suppliers exist than for heavy equipment, but remote-site logistics create dependence on regional distributors and trucking; single-route interruptions in Zambia and Panama have previously delayed deliveries by 7–21 days, increasing outage risk.

FQM uses long-term supply contracts and annual hedges to stabilize pricing and ensure continuity, keeping supplier power at a moderate level despite essentiality of inputs and exposure to commodity-driven price shocks.

- Key inputs: ammonia, detonators, steel grinding media

- 2024 reagent cost rise: ~8–12%

- Delivery delays: 7–21 days at remote sites

- Supplier power: moderate due to contracts + logistics risk

Logistics and Infrastructure Constraints

Transporting bulky copper concentrates from remote First Quantum Minerals mines needs strong rail and road links; 2024 company reports show logistics delays cut shipments by up to 8% at times.

In several operating countries a single national rail or a few trucking firms dominate, giving carriers pricing and schedule power that raises freight cost volatility.

Logistics failures directly hit revenue recognition and cash flow, so management prioritizes supply-chain resilience and contingency spend (~$50–120m capex range for 2023–24 upgrades).

- Single-rail national routes common

- Up to 8% shipment loss from delays (2024)

- Freight cost volatility raises margins pressure

- $50–120m recent logistics capex

FQM’s scale, hedges blunt supplier pressure despite rising reagent costs and shipment losses

Supplier power is moderate: concentrated OEMs (Caterpillar, Komatsu) and energy/fuel suppliers tilt leverage up, but FQM’s scale, long-term contracts and 2024 hedges (US$1.2bn capex; ~4.3 TWh power use; Brent $88/bbl) cap pricing risk; reagent costs rose ~8–12% in 2024 and logistics delays cut shipments up to 8%.

| Metric | 2024 value |

|---|---|

| Sustaining & growth capex | US$1.2bn |

| Electricity use | ~4.3 TWh |

| Brent average | $88/bbl |

| Reagent cost rise | 8–12% |

| Shipment loss from delays | up to 8% |

What is included in the product

Tailored exclusively for First Quantum Minerals, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats shaping its profitability and strategic positioning.

A concise Porter's Five Forces one-sheet for First Quantum Minerals—quickly compare supplier power, buyer leverage, rival intensity, threat of substitutes, and new entrants to guide strategic decisions.

Customers Bargaining Power

Consolidation of Global Smelters and Refiners

A large share of First Quantum Minerals’ copper concentrate is sold to a handful of global smelters, notably Chinese firms that accounted for about 50–60% of global smelting throughput in 2024, giving buyers strong pricing leverage.

When smelter capacity tightened in 2023–24, average treatment and refining charges (TC/RC) rose by roughly 15–25%, cutting miners’ net revenue per tonne; First Quantum faces that margin squeeze directly.

This buyer concentration forces First Quantum to diversify contracts and geographies; relying on a single market risks price exposure and higher TC/RC if a major smelter chain tightens capacity.

Influence of Commodity Trading Giants

Large traders like Glencore and Trafigura handle ~25–35% of global copper trade and often take mine output en route to end users, giving them price-setting leverage over First Quantum Minerals (FQM).

Their market intelligence and balance-sheet capital let them secure favorable off-take terms in volatile 2024–25 copper markets (LME avg 2025 YTD ~US$9,200/t), squeezing FQM’s capture of spot upside.

FQM’s 2024 production scale—~711 kt copper eq. sold—lets it negotiate better margins than juniors, but reliance on traders still caps full price realization.

Standardization of Metal Pricing

Copper and nickel prices are set on exchanges like the London Metal Exchange, so First Quantum Minerals is a global price-taker; in 2024 copper averaged ~US$9,100/t and nickel ~US$23,000/t, limiting customer power over base prices.

Buyers can still press for premiums or discounts tied to grade, cathode quality, and delivery timing, so negotiation shifts to contract terms rather than spot price.

Exchange transparency reduces risk of arbitrary price suppression by large customers, forcing concessions into fees, payment terms, or logistics instead.

Demand Driven by the Energy Transition

The global shift to EVs and renewables has pushed copper demand up: IEA estimated copper demand for clean energy rose to ~22% of total demand by 2023 and is projected to reach ~30% by 2030, tightening markets and boosting producers’ leverage.

Auto makers and utilities are signing long-term deals, but when demand outstrips supply First Quantum (2024 copper output ~880 kt, nickel growing from Cobre Panama cadence) gains stronger bargaining power on off-take volumes and contract length.

Higher realized prices (LME copper average 2024 ~$8,500/t) and constrained project pipeline mean First Quantum can negotiate favorable term sheets and volume commitments.

- IEA: copper clean-energy demand ~22% (2023)

- Projected clean-energy share ~30% (2030)

- FQM ~880 kt Cu output (2024)

- LME copper avg 2024 ≈ $8,500/t

Quality and Purity Requirements

Customers now demand consistent high-purity concentrates; smelters pay penalties for Cu grades below specs, and spot premiums rose ~12% in 2024 for low-impurity feedstocks, so First Quantum faces margin risk if ore quality drops.

Buyers increasingly prefer green copper—by 2025 >20% of European offtake tenders include carbon-intensity clauses—so customers can push First Quantum to fund ESG upgrades to keep premium contracts.

- 2024 spot premium ~12% for low-impurity concentrates

- 2025: >20% EU offtakes include carbon clauses

- Ore-grade volatility → price penalties or lost buyers

- ESG investment needed to retain premium markets

Smelters, traders squeeze prices as clean-energy demand boosts producer leverage

Customers hold moderate-to-high bargaining power: concentrated smelters (China ~50–60% throughput 2024) and traders (Glencore/Trafigura ~25–35% trade) squeeze TCs/RCs, while FQM scale (~711–880 kt Cu eq. sold in 2024) mitigates but cannot eliminate price capture; demand tailwinds (IEA clean-energy 22% 2023 → ~30% 2030) improve producer leverage, yet buyers push grade, timing, and carbon clauses (>20% EU offtakes 2025).

| Metric | Value |

|---|---|

| China smelter share (2024) | 50–60% |

| Traders' trade share | 25–35% |

| FQM Cu output (2024) | 711–880 kt |

| LME Cu avg (2024) | ~$8,500/t |

| IEA clean-energy copper (2023) | 22% |

| EU offtakes w/ carbon clauses (2025) | >20% |

Preview the Actual Deliverable

First Quantum Minerals Porter's Five Forces Analysis

This preview shows the exact First Quantum Minerals Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no abridgments, fully formatted and ready for download.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

First Quantum Minerals faces strong rivalry from large diversified miners, significant supplier leverage for specialized equipment and inputs, and moderate buyer power driven by concentrate markets—while capital intensity and regulatory barriers limit new entrants and substitution risk remains low for key metals.

Suppliers Bargaining Power

Concentration of Specialized Equipment Providers

The mining sector depends on a few global makers for large earthmoving and processing kit; Caterpillar and Komatsu hold outsized power because products are specialized and replacement lead times exceed 12–18 months, raising vendor leverage.

For First Quantum Minerals, concentrated suppliers make equipment prices and maintenance contracts largely non-negotiable, pushing 2024 capex pressure—company spent US$1.2bn on sustaining and growth capex in 2024.

First Quantum’s scale helps in talks, but the technical complexity of automated fleets and long OEM support cycles keep bargaining power tilted toward manufacturers, limiting cost-flexibility.

Energy Dependency and Utility Providers

Mining is energy-heavy—First Quantum Minerals used ~4.3 TWh of electricity across operations in 2024, driving high costs for mills and haulage.

In Zambia Q4 2024, state-owned ZESCO's limited competition constrains First Quantum's rate negotiations, raising supplier leverage.

Fuel price swings (Brent averaged $88/bbl in 2024) directly raised diesel costs; short-term alternatives for heavy equipment are limited.

FQM is investing in on-site renewables (projects target ~250 MW by 2027) to cut exposure, but market price shocks still pose material risk.

Labor Unions and Skilled Workforce Availability

Labor bargaining power is high for First Quantum Minerals in jurisdictions with strong unions; collective agreements in 2024-25 raised labor costs by ~6-9% at some Canadian and Zambian sites, and strikes risk month-long output losses.

Advanced automation raises demand for specialized technicians, boosting wage premia for controls engineers and electricians by ~10-15%, shifting leverage to skilled staff.

Global shortages of experienced mining engineers and geologists—ILO estimates show a 12% supply gap in 2024—strengthen worker negotiating power and recruitment costs for First Quantum.

Consumables and Chemical Reagents

Consumables like reagents, explosives and grinding media are vital for First Quantum Minerals’ (FQM) copper and nickel processing; global ammonia and steel price spikes in 2024 raised reagent-related input costs ~8–12% for the mining sector, boosting FQM’s site operating costs in 2024 by an estimated mid-single digits percent.

More suppliers exist than for heavy equipment, but remote-site logistics create dependence on regional distributors and trucking; single-route interruptions in Zambia and Panama have previously delayed deliveries by 7–21 days, increasing outage risk.

FQM uses long-term supply contracts and annual hedges to stabilize pricing and ensure continuity, keeping supplier power at a moderate level despite essentiality of inputs and exposure to commodity-driven price shocks.

- Key inputs: ammonia, detonators, steel grinding media

- 2024 reagent cost rise: ~8–12%

- Delivery delays: 7–21 days at remote sites

- Supplier power: moderate due to contracts + logistics risk

Logistics and Infrastructure Constraints

Transporting bulky copper concentrates from remote First Quantum Minerals mines needs strong rail and road links; 2024 company reports show logistics delays cut shipments by up to 8% at times.

In several operating countries a single national rail or a few trucking firms dominate, giving carriers pricing and schedule power that raises freight cost volatility.

Logistics failures directly hit revenue recognition and cash flow, so management prioritizes supply-chain resilience and contingency spend (~$50–120m capex range for 2023–24 upgrades).

- Single-rail national routes common

- Up to 8% shipment loss from delays (2024)

- Freight cost volatility raises margins pressure

- $50–120m recent logistics capex

FQM’s scale, hedges blunt supplier pressure despite rising reagent costs and shipment losses

Supplier power is moderate: concentrated OEMs (Caterpillar, Komatsu) and energy/fuel suppliers tilt leverage up, but FQM’s scale, long-term contracts and 2024 hedges (US$1.2bn capex; ~4.3 TWh power use; Brent $88/bbl) cap pricing risk; reagent costs rose ~8–12% in 2024 and logistics delays cut shipments up to 8%.

| Metric | 2024 value |

|---|---|

| Sustaining & growth capex | US$1.2bn |

| Electricity use | ~4.3 TWh |

| Brent average | $88/bbl |

| Reagent cost rise | 8–12% |

| Shipment loss from delays | up to 8% |

What is included in the product

Tailored exclusively for First Quantum Minerals, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats shaping its profitability and strategic positioning.

A concise Porter's Five Forces one-sheet for First Quantum Minerals—quickly compare supplier power, buyer leverage, rival intensity, threat of substitutes, and new entrants to guide strategic decisions.

Customers Bargaining Power

Consolidation of Global Smelters and Refiners

A large share of First Quantum Minerals’ copper concentrate is sold to a handful of global smelters, notably Chinese firms that accounted for about 50–60% of global smelting throughput in 2024, giving buyers strong pricing leverage.

When smelter capacity tightened in 2023–24, average treatment and refining charges (TC/RC) rose by roughly 15–25%, cutting miners’ net revenue per tonne; First Quantum faces that margin squeeze directly.

This buyer concentration forces First Quantum to diversify contracts and geographies; relying on a single market risks price exposure and higher TC/RC if a major smelter chain tightens capacity.

Influence of Commodity Trading Giants

Large traders like Glencore and Trafigura handle ~25–35% of global copper trade and often take mine output en route to end users, giving them price-setting leverage over First Quantum Minerals (FQM).

Their market intelligence and balance-sheet capital let them secure favorable off-take terms in volatile 2024–25 copper markets (LME avg 2025 YTD ~US$9,200/t), squeezing FQM’s capture of spot upside.

FQM’s 2024 production scale—~711 kt copper eq. sold—lets it negotiate better margins than juniors, but reliance on traders still caps full price realization.

Standardization of Metal Pricing

Copper and nickel prices are set on exchanges like the London Metal Exchange, so First Quantum Minerals is a global price-taker; in 2024 copper averaged ~US$9,100/t and nickel ~US$23,000/t, limiting customer power over base prices.

Buyers can still press for premiums or discounts tied to grade, cathode quality, and delivery timing, so negotiation shifts to contract terms rather than spot price.

Exchange transparency reduces risk of arbitrary price suppression by large customers, forcing concessions into fees, payment terms, or logistics instead.

Demand Driven by the Energy Transition

The global shift to EVs and renewables has pushed copper demand up: IEA estimated copper demand for clean energy rose to ~22% of total demand by 2023 and is projected to reach ~30% by 2030, tightening markets and boosting producers’ leverage.

Auto makers and utilities are signing long-term deals, but when demand outstrips supply First Quantum (2024 copper output ~880 kt, nickel growing from Cobre Panama cadence) gains stronger bargaining power on off-take volumes and contract length.

Higher realized prices (LME copper average 2024 ~$8,500/t) and constrained project pipeline mean First Quantum can negotiate favorable term sheets and volume commitments.

- IEA: copper clean-energy demand ~22% (2023)

- Projected clean-energy share ~30% (2030)

- FQM ~880 kt Cu output (2024)

- LME copper avg 2024 ≈ $8,500/t

Quality and Purity Requirements

Customers now demand consistent high-purity concentrates; smelters pay penalties for Cu grades below specs, and spot premiums rose ~12% in 2024 for low-impurity feedstocks, so First Quantum faces margin risk if ore quality drops.

Buyers increasingly prefer green copper—by 2025 >20% of European offtake tenders include carbon-intensity clauses—so customers can push First Quantum to fund ESG upgrades to keep premium contracts.

- 2024 spot premium ~12% for low-impurity concentrates

- 2025: >20% EU offtakes include carbon clauses

- Ore-grade volatility → price penalties or lost buyers

- ESG investment needed to retain premium markets

Smelters, traders squeeze prices as clean-energy demand boosts producer leverage

Customers hold moderate-to-high bargaining power: concentrated smelters (China ~50–60% throughput 2024) and traders (Glencore/Trafigura ~25–35% trade) squeeze TCs/RCs, while FQM scale (~711–880 kt Cu eq. sold in 2024) mitigates but cannot eliminate price capture; demand tailwinds (IEA clean-energy 22% 2023 → ~30% 2030) improve producer leverage, yet buyers push grade, timing, and carbon clauses (>20% EU offtakes 2025).

| Metric | Value |

|---|---|

| China smelter share (2024) | 50–60% |

| Traders' trade share | 25–35% |

| FQM Cu output (2024) | 711–880 kt |

| LME Cu avg (2024) | ~$8,500/t |

| IEA clean-energy copper (2023) | 22% |

| EU offtakes w/ carbon clauses (2025) | >20% |

Preview the Actual Deliverable

First Quantum Minerals Porter's Five Forces Analysis

This preview shows the exact First Quantum Minerals Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no abridgments, fully formatted and ready for download.