First Majestic Porter's Five Forces Analysis

From Overview to Strategy Blueprint

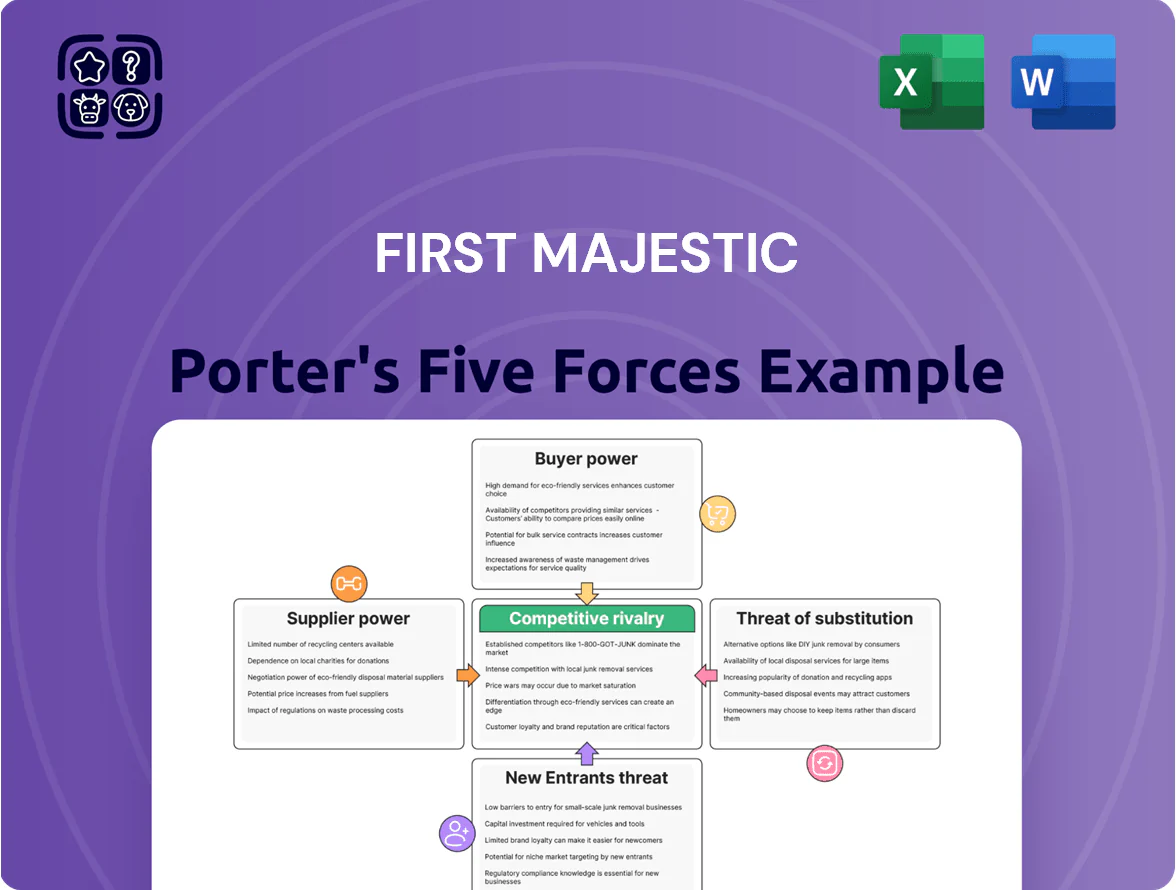

First Majestic faces moderate supplier power, commodity-price sensitivity, and regional regulatory risks that shape its competitive landscape, while barriers to entry and rivalry among mid-tier miners drive margin pressure and strategic consolidation opportunities; this snapshot highlights key dynamics but omits detailed force ratings and scenario impacts. Unlock the full Porter's Five Forces Analysis to explore First Majestic’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility of Energy and Fuel Costs

Energy makes up about 18–22% of operating costs at First Majestic Silver PLC’s Mexican mines, with diesel and grid electricity powering haulage and mills, so fuel-price moves feed directly into margins.

Dependence on imported diesel and state-run CFE electricity raises supplier leverage; a 30% diesel rally or 15% electricity tariff hike can cut EBITDA margins by ~5–7 percentage points.

By late 2025, proposed Mexican carbon pricing or energy reforms would increase utility bargaining power, as higher carbon costs translate into sustained fuel/electricity price floors and pass-through to miners.

Limited Sources for Mining Equipment

First Majestic relies on a handful of global suppliers like Sandvik and Epiroc for specialized underground mining rigs, concentrating supplier power; these vendors captured roughly 60–70% of the market for tunneling and bolt rigs by 2024.

High switching costs—equipment unit prices often exceeding US$1–3m per unit—and complex integration raise dependence, reducing bargaining leverage for First Majestic.

Long-term maintenance contracts and constrained spare-parts lead times (median 8–12 weeks in 2024) further lock the company to key suppliers across project lifecycles.

Labor Union Influence in Mexico

Labor is a critical input and Mexican unions give workforce suppliers strong leverage over First Majestic, with past disputes—like the 2022 seasonal strike at La Encantada—halting output and raising operating costs by an estimated 6–9% in affected months.

First Majestic has long negotiated with powerful local syndicates that can demand higher profit-sharing; in 2024 union wage settlements averaged a 7% increase across Sonora mines, pressuring margins.

As of 2025, demand for skilled geologists and mining engineers pushed regional wages up about 10% year-over-year, increasing bargaining power of professional labor and raising replacement costs for specialized roles.

Scarcity of Chemical Reagents

The metallurgical recovery of silver needs inputs like sodium cyanide and specialized grinding media made by few global chemical firms; in 2024 chemical suppliers concentrated the market, with top 5 producers controlling ~60% of sodium cyanide capacity, raising supplier leverage.

Supply disruptions or consolidation can push reagent prices—sodium cyanide rose ~18% in 2023–24—forcing First Majestic to absorb costs or cut output, since few viable substitutes exist for these critical agents.

Here’s the quick math: a 10% cyanide price rise can raise cash costs per ounce by roughly US$0.30–0.50, depending on ore grades and recovery rates; negotiating power is limited by lack of alternatives and switching costs.

- Top 5 producers ≈60% sodium cyanide capacity (2024)

- Sodium cyanide price +18% (2023–24)

- 10% price rise → ~US$0.30–0.50/oz cash cost impact

- Few substitutes; high switching and regulatory costs

Regulatory and Permitting Authorities

Regulatory and permitting authorities act as a supplier of legal rights in mining; Mexico issued 1,243 new mining permits in 2024, but tightened approvals for open-pit mines and water concessions through 2025, raising approval timelines from ~6 to 9+ months.

First Majestic needs top-tier ESG compliance—its 2024 corporate water use was 0.45 m3/tonne; failure to meet standards risks non-renewal of key permits and stoppage of cash-generating sites.

- Government = exclusive supplier of permits and water rights

- 2024: 1,243 permits; 2025: stricter open-pit/water rules

- Approval times rose ~50% to 9+ months

- First Majestic water use 0.45 m3/tonne (2024)

Supply shocks, energy & regulatory bottlenecks threaten mining EBITDA and costs

Suppliers hold meaningful power: energy (18–22% of costs), key equipment vendors (Sandvik/Epiroc ~60–70% market), chemicals (top‑5 cyanide ~60% capacity) and unions push costs and disruption risk; regulatory permits and water rights are exclusive levers. A 10% cyanide rise → ~US$0.30–0.50/oz; 30% diesel or 15% electricity shock cuts EBITDA ~5–7 pts; permit times rose to 9+ months (2025).

| Input | 2024–25 metric | Impact |

|---|---|---|

| Energy | 18–22% opex | Fuel/electric shocks cut EBITDA 5–7 pts |

| Equipment | Sandvik/Epiroc 60–70% share | High switching costs US$1–3m/unit |

| Sodium cyanide | Top‑5 ≈60% capacity; +18% (2023–24) | 10% price → +US$0.30–0.50/oz |

| Labor/unions | Wages +7% (2024); skilled +10% (2025) | Output stoppages ↑ costs 6–9% |

| Permits/ESG | 1,243 permits (2024); approvals 9+ months (2025) | Delays, permit risk for non‑compliance |

What is included in the product

Tailored Porter's Five Forces analysis for First Majestic that uncovers competitive intensity, supplier and buyer power, threats from substitutes and new entrants, and strategic implications for pricing and profitability.

Concise Porter's Five Forces summary for First Majestic—fast insight into competitive pressures and margin risks, ready to drop into investor decks.

Customers Bargaining Power

Global Commodity Price Takers

First Majestic sells silver and gold into global markets where prices are set by international exchanges such as the London Bullion Market Association (LBMA), so neither the company nor buyers can influence spot prices; in 2024 global silver traded ~1.05 billion oz and the LBMA average price was about $23.50/oz, forcing First Majestic to accept prevailing market rates.

Concentration of Smelting and Refining Services

The majority of First Majestic Silver Corp’s raw output must go to a small set of third‑party refineries; in 2024 about 70–80% of payable silver was sent to three major international smelters, concentrating bargaining power.

Those refiners set processing fees and settlement timing that can swing cash flow; a 2024 average treatment charge of $0.30/oz and payment lags up to 45 days raised working capital needs.

First Majestic has investigated vertical integration and tolling agreements, but continued reliance on major smelters remains a material customer‑side pressure on margins and liquidity.

Direct-to-Consumer Retail Strategy

First Majestic’s direct-to-consumer bullion store lets the miner sell silver directly to retail investors, cutting out traditional middlemen and lowering their bargaining power. By selling at an average premium of about 6.5% over spot in 2025, the channel raised gross margin on retail sales versus wholesale. By Q3 2025 retail accounted for roughly 8% of physical silver volumes and helped lift consolidated gross margin by ~120 basis points year-over-year. This retail push diversifies customers and strengthens pricing control.

Industrial Demand from Solar and Electronics

Industrial demand from photovoltaics (PV) and electronics drives about 50% of global silver consumption; PV and electronics used ~555 Moz of silver in 2024, per World Silver Survey 2025, giving large manufacturers strong leverage over pricing.

These buyers can swap to silver-thrifting tech or alternative conductors if prices spike; a 10–20% price jump historically prompts procurement shifts and reduces offtake.

Collective demand cycles set premiums First Majestic can charge for physical silver and bullion, with spot-premium spreads widening to 40–80 cents/oz during tight 2024 supply windows.

- ~50% of silver demand: PV + electronics (2024)

- PV/electronics consumed ~555 Moz silver (2024)

- 10–20% price rises trigger thrifting shifts

- Spot-premium spreads: $0.40–$0.80/oz in 2024 tight markets

Institutional Bullion Bank Influence

- Top 5 bullion banks: ~65% LBMA clearing (2024)

- LBMA/COMEX inventories changed ~18% in 2024

- First Majestic FY2024 revenue ~85% tied to silver

- Paper trading + stockpiling can widen miner price discounts

Refineries and LBMA Drive Prices; Retail Boosts Margins Despite Tight Buyer Power

Buyers have strong power: global spot prices set by LBMA force First Majestic to accept market rates (LBMA avg silver $23.50/oz in 2024), while three refineries took ~70–80% of payable silver in 2024, setting fees (~$0.30/oz) and payment lags up to 45 days; retail bullion sales (8% volumes in Q3 2025) trimmed middlemen power and raised gross margin ~120 bps YoY.

| Metric | 2024/2025 |

|---|---|

| LBMA avg price | $23.50/oz (2024) |

| Refinery share | 70–80% (2024) |

| Treatment charge | $0.30/oz (2024) |

| Retail share | 8% vols Q3 2025 |

Full Version Awaits

First Majestic Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of First Majestic you'll receive immediately after purchase—no placeholders or mockups, fully formatted and ready to use. It covers supplier power, buyer power, competitive rivalry, threat of substitution, and barriers to entry with actionable insights and concise scoring. Once you buy, you’ll get this same complete document available for instant download.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

First Majestic faces moderate supplier power, commodity-price sensitivity, and regional regulatory risks that shape its competitive landscape, while barriers to entry and rivalry among mid-tier miners drive margin pressure and strategic consolidation opportunities; this snapshot highlights key dynamics but omits detailed force ratings and scenario impacts. Unlock the full Porter's Five Forces Analysis to explore First Majestic’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility of Energy and Fuel Costs

Energy makes up about 18–22% of operating costs at First Majestic Silver PLC’s Mexican mines, with diesel and grid electricity powering haulage and mills, so fuel-price moves feed directly into margins.

Dependence on imported diesel and state-run CFE electricity raises supplier leverage; a 30% diesel rally or 15% electricity tariff hike can cut EBITDA margins by ~5–7 percentage points.

By late 2025, proposed Mexican carbon pricing or energy reforms would increase utility bargaining power, as higher carbon costs translate into sustained fuel/electricity price floors and pass-through to miners.

Limited Sources for Mining Equipment

First Majestic relies on a handful of global suppliers like Sandvik and Epiroc for specialized underground mining rigs, concentrating supplier power; these vendors captured roughly 60–70% of the market for tunneling and bolt rigs by 2024.

High switching costs—equipment unit prices often exceeding US$1–3m per unit—and complex integration raise dependence, reducing bargaining leverage for First Majestic.

Long-term maintenance contracts and constrained spare-parts lead times (median 8–12 weeks in 2024) further lock the company to key suppliers across project lifecycles.

Labor Union Influence in Mexico

Labor is a critical input and Mexican unions give workforce suppliers strong leverage over First Majestic, with past disputes—like the 2022 seasonal strike at La Encantada—halting output and raising operating costs by an estimated 6–9% in affected months.

First Majestic has long negotiated with powerful local syndicates that can demand higher profit-sharing; in 2024 union wage settlements averaged a 7% increase across Sonora mines, pressuring margins.

As of 2025, demand for skilled geologists and mining engineers pushed regional wages up about 10% year-over-year, increasing bargaining power of professional labor and raising replacement costs for specialized roles.

Scarcity of Chemical Reagents

The metallurgical recovery of silver needs inputs like sodium cyanide and specialized grinding media made by few global chemical firms; in 2024 chemical suppliers concentrated the market, with top 5 producers controlling ~60% of sodium cyanide capacity, raising supplier leverage.

Supply disruptions or consolidation can push reagent prices—sodium cyanide rose ~18% in 2023–24—forcing First Majestic to absorb costs or cut output, since few viable substitutes exist for these critical agents.

Here’s the quick math: a 10% cyanide price rise can raise cash costs per ounce by roughly US$0.30–0.50, depending on ore grades and recovery rates; negotiating power is limited by lack of alternatives and switching costs.

- Top 5 producers ≈60% sodium cyanide capacity (2024)

- Sodium cyanide price +18% (2023–24)

- 10% price rise → ~US$0.30–0.50/oz cash cost impact

- Few substitutes; high switching and regulatory costs

Regulatory and Permitting Authorities

Regulatory and permitting authorities act as a supplier of legal rights in mining; Mexico issued 1,243 new mining permits in 2024, but tightened approvals for open-pit mines and water concessions through 2025, raising approval timelines from ~6 to 9+ months.

First Majestic needs top-tier ESG compliance—its 2024 corporate water use was 0.45 m3/tonne; failure to meet standards risks non-renewal of key permits and stoppage of cash-generating sites.

- Government = exclusive supplier of permits and water rights

- 2024: 1,243 permits; 2025: stricter open-pit/water rules

- Approval times rose ~50% to 9+ months

- First Majestic water use 0.45 m3/tonne (2024)

Supply shocks, energy & regulatory bottlenecks threaten mining EBITDA and costs

Suppliers hold meaningful power: energy (18–22% of costs), key equipment vendors (Sandvik/Epiroc ~60–70% market), chemicals (top‑5 cyanide ~60% capacity) and unions push costs and disruption risk; regulatory permits and water rights are exclusive levers. A 10% cyanide rise → ~US$0.30–0.50/oz; 30% diesel or 15% electricity shock cuts EBITDA ~5–7 pts; permit times rose to 9+ months (2025).

| Input | 2024–25 metric | Impact |

|---|---|---|

| Energy | 18–22% opex | Fuel/electric shocks cut EBITDA 5–7 pts |

| Equipment | Sandvik/Epiroc 60–70% share | High switching costs US$1–3m/unit |

| Sodium cyanide | Top‑5 ≈60% capacity; +18% (2023–24) | 10% price → +US$0.30–0.50/oz |

| Labor/unions | Wages +7% (2024); skilled +10% (2025) | Output stoppages ↑ costs 6–9% |

| Permits/ESG | 1,243 permits (2024); approvals 9+ months (2025) | Delays, permit risk for non‑compliance |

What is included in the product

Tailored Porter's Five Forces analysis for First Majestic that uncovers competitive intensity, supplier and buyer power, threats from substitutes and new entrants, and strategic implications for pricing and profitability.

Concise Porter's Five Forces summary for First Majestic—fast insight into competitive pressures and margin risks, ready to drop into investor decks.

Customers Bargaining Power

Global Commodity Price Takers

First Majestic sells silver and gold into global markets where prices are set by international exchanges such as the London Bullion Market Association (LBMA), so neither the company nor buyers can influence spot prices; in 2024 global silver traded ~1.05 billion oz and the LBMA average price was about $23.50/oz, forcing First Majestic to accept prevailing market rates.

Concentration of Smelting and Refining Services

The majority of First Majestic Silver Corp’s raw output must go to a small set of third‑party refineries; in 2024 about 70–80% of payable silver was sent to three major international smelters, concentrating bargaining power.

Those refiners set processing fees and settlement timing that can swing cash flow; a 2024 average treatment charge of $0.30/oz and payment lags up to 45 days raised working capital needs.

First Majestic has investigated vertical integration and tolling agreements, but continued reliance on major smelters remains a material customer‑side pressure on margins and liquidity.

Direct-to-Consumer Retail Strategy

First Majestic’s direct-to-consumer bullion store lets the miner sell silver directly to retail investors, cutting out traditional middlemen and lowering their bargaining power. By selling at an average premium of about 6.5% over spot in 2025, the channel raised gross margin on retail sales versus wholesale. By Q3 2025 retail accounted for roughly 8% of physical silver volumes and helped lift consolidated gross margin by ~120 basis points year-over-year. This retail push diversifies customers and strengthens pricing control.

Industrial Demand from Solar and Electronics

Industrial demand from photovoltaics (PV) and electronics drives about 50% of global silver consumption; PV and electronics used ~555 Moz of silver in 2024, per World Silver Survey 2025, giving large manufacturers strong leverage over pricing.

These buyers can swap to silver-thrifting tech or alternative conductors if prices spike; a 10–20% price jump historically prompts procurement shifts and reduces offtake.

Collective demand cycles set premiums First Majestic can charge for physical silver and bullion, with spot-premium spreads widening to 40–80 cents/oz during tight 2024 supply windows.

- ~50% of silver demand: PV + electronics (2024)

- PV/electronics consumed ~555 Moz silver (2024)

- 10–20% price rises trigger thrifting shifts

- Spot-premium spreads: $0.40–$0.80/oz in 2024 tight markets

Institutional Bullion Bank Influence

- Top 5 bullion banks: ~65% LBMA clearing (2024)

- LBMA/COMEX inventories changed ~18% in 2024

- First Majestic FY2024 revenue ~85% tied to silver

- Paper trading + stockpiling can widen miner price discounts

Refineries and LBMA Drive Prices; Retail Boosts Margins Despite Tight Buyer Power

Buyers have strong power: global spot prices set by LBMA force First Majestic to accept market rates (LBMA avg silver $23.50/oz in 2024), while three refineries took ~70–80% of payable silver in 2024, setting fees (~$0.30/oz) and payment lags up to 45 days; retail bullion sales (8% volumes in Q3 2025) trimmed middlemen power and raised gross margin ~120 bps YoY.

| Metric | 2024/2025 |

|---|---|

| LBMA avg price | $23.50/oz (2024) |

| Refinery share | 70–80% (2024) |

| Treatment charge | $0.30/oz (2024) |

| Retail share | 8% vols Q3 2025 |

Full Version Awaits

First Majestic Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of First Majestic you'll receive immediately after purchase—no placeholders or mockups, fully formatted and ready to use. It covers supplier power, buyer power, competitive rivalry, threat of substitution, and barriers to entry with actionable insights and concise scoring. Once you buy, you’ll get this same complete document available for instant download.