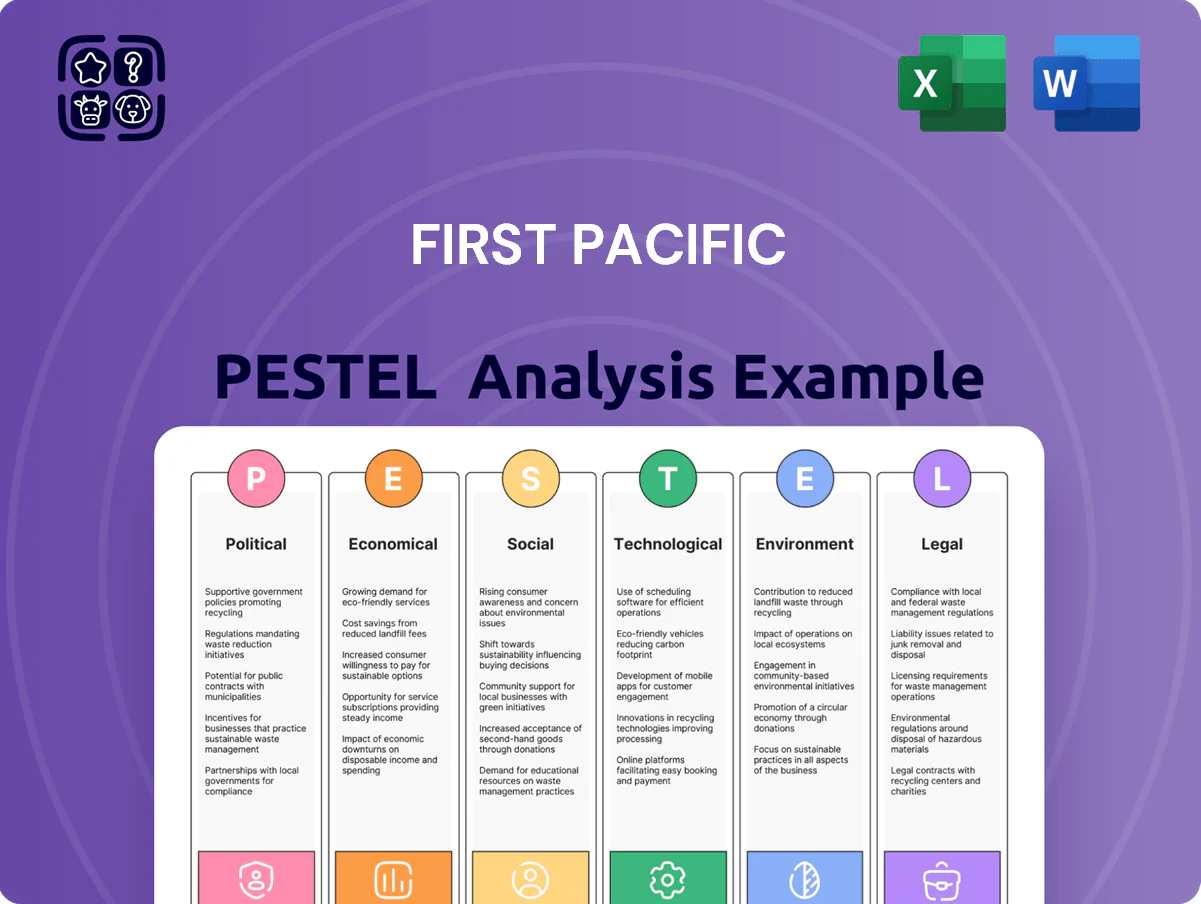

First Pacific PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Gain a strategic advantage with our targeted PESTLE Analysis of First Pacific—unpack the political, economic, social, technological, legal, and environmental forces shaping its trajectory and translate them into actionable strategy. Ideal for investors, consultants, and executives seeking concise, research-backed insights. Purchase the full report to access the complete breakdown, editable files, and practical recommendations for immediate use.

Political factors

Geopolitical Stability in Southeast Asia

Regional tensions in the South China Sea, with 2024 incidents up 12% year-on-year, continue to affect trade routes that carry about 30% of global maritime trade and influence investor sentiment across Asia-Pacific.

First Pacific must navigate complex China-ASEAN diplomatic relations where its key assets in the Philippines and Indonesia represent over 60% of its NAV, exposing it to policy and operational risk.

The company closely monitors developments to mitigate disruptions to maritime logistics and cross-border capital flows, noting that 18% of regional FDI into ASEAN in 2023 was China-linked, heightening exposure to geopolitical shifts.

Indonesian Policy Continuity

Following administrative stabilization through 2025, policy continuity in Indonesia is vital for Indofood and First Pacific; government food security programs and downstreaming mandates (e.g., 2024 palm oil downstream targets boosting domestic refining capacity by ~15%) reshape capital allocation and capex plans across holdings.

Philippine Infrastructure Priorities

The Philippine government’s push for infrastructure via PPPs—70 projects worth PHP 3.2 trillion announced under the 2024-2025 pipeline—directly benefits Metro Pacific Investments Corporation (MPIC) by expanding opportunities in transport, water and energy concessions.

Political backing for projects like the PHP 735 billion Luzon expressway expansions and Water Sector Asset Management targets a stable capital deployment and potential revenue growth for MPIC’s utilities and toll portfolios.

However, electoral shifts or reallocation of the 2025 national budget (PHP 5.5 trillion) could slow project rollouts, affecting MPIC’s concession timelines and cash flow forecasts.

Hong Kong Regulatory Environment

As a Hong Kong-listed entity, First Pacific faces an evolving SAR regulatory landscape and Greater Bay Area integration, affecting cross-border operations and capital flows; Hong Kong’s Exchanges and Clearing reporting changes in 2024 raised disclosure frequency for SNAP dealings by listed conglomerates.

Compliance with dual local and international standards is mandatory to maintain listing—HKEX’s 2023/24 listing rules and IFRS updates increased compliance costs, contributing to sectoral governance spend rises estimated at 5–8% year-on-year for major holdings.

First Pacific adjusts corporate governance and transparency frameworks to meet tightened reporting and ESG disclosure expectations; by FY2024 the group aligned its reporting cadence with HKEX’s new guidance and expanded audit committee oversight across its principal investees.

- Subject to HKEX 2023/24 rule changes and Greater Bay Area regulatory alignment

- Dual compliance: HK authorities plus IFRS/global standards—governance costs up ~5–8% YoY

- Governance adaptations: increased disclosure frequency, expanded audit oversight (implemented FY2024)

Resource Nationalism Trends

The rise in resource nationalism in Southeast Asia and the Philippines risks revisions to mining laws and ownership rules that could affect Philex Mining; in 2024 Philippine mineral royalties proposals sought increases from 2–5% to 6–10% and local processing mandates rose in 3 jurisdictions.

First Pacific models these shifts—estimating potential EBITDA reductions of 5–12% under higher royalty scenarios—and engages governments to secure fiscal stability and sustainable extraction practices.

- 2024 royalty proposals: +4–8 percentage points in target countries

- Estimated EBITDA hit to mining assets: 5–12% under worst-case

- Policy focus: higher local processing and domestic value-add requirements

South China Sea tensions imperil First Pacific NAV, PPPs and mining margins

Regional SCS tensions (incidents +12% YoY in 2024) and China-ASEAN diplomacy risk trade routes (~30% global maritime trade) impacting First Pacific’s Philippines/Indonesia NAV (>60%). Policy continuity in Indonesia and Philippine PPPs (PHP 3.2tn pipeline) shape MPIC capex; resource nationalism (royalty proposals +4–8ppt) could cut mining EBITDA 5–12%. HKEX/IFRS rule changes raised governance costs ~5–8% YoY.

| Metric | 2024/25 |

|---|---|

| SCS incidents | +12% YoY |

| Maritime trade affected | ~30% |

| NAV exposure | >60% |

| PPP pipeline | PHP 3.2tn |

| Royalty change | +4–8ppt |

| Mining EBITDA risk | −5–12% |

| Governance cost rise | +5–8% YoY |

What is included in the product

Explores how external macro-environmental factors uniquely affect First Pacific across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by relevant data and forward-looking trends to identify risks and opportunities for executives, investors, and strategists.

A concise First Pacific PESTLE summary that’s visually segmented for quick interpretation, easily dropped into presentations, annotated for local context, and shareable across teams to streamline risk discussions and strategic planning.

Economic factors

Currency Exchange Volatility

First Pacific reports in US dollars while substantial revenue streams come from Indonesian rupiah and Philippine peso; in 2024 FX swings saw the IDR fall about 3.5% vs USD and PHP weaken ~2.1% year-to-date, creating material translation risk for consolidated results.

Significant local-currency depreciation can produce translation losses—First Pacific reported FX-driven impacts in prior annual statements—and could compress reported net income and ROE.

The group uses hedging and cash management to mitigate volatility; in 2024 it disclosed using forward contracts and natural hedges to stabilize dividend remittances from PLDT, Metro Pacific and Indofood affiliates.

Interest Rate Environment

The Asia-Pacific interest rate backdrop—with central banks like the Fed and BSP lifting rates to ~5.25%-5.50% (US) and the Philippines policy rate at 6.25% in 2025—raises First Pacific’s borrowing costs for Metro Pacific and PLDT, potentially squeezing margins on capital-heavy infrastructure and telecom projects.

Inflationary Pressures on Consumers

Regional Economic Growth Trajectories

Indonesia and the Philippines, contributing over 70% of First Pacific’s EBITDA exposure, are projected to grow 4.5–5.0% (Indonesia) and 5.0–5.5% (Philippines) in 2024–2025, supporting rising demand for telecoms, power and processed foods as incomes climb.

First Pacific targets investments aligned with IMF GDP per capita gains and 3–6% annual urbanization-driven consumption growth to capture sectoral expansion.

- Indonesia GDP ~USD 1.3T (2024), Philippines ~USD 420B (2024)

- Telco subscribers and electricity demand up 3–7% y/y

- Processed food consumption rising with urbanization 2–4% annually

Capital Market Access

Access to capital in 2024–25 remains critical for First Pacific to fund expansions of PLDT, Indofood and Metro Pacific; the group tapped roughly $1.2bn in debt and equity issuances across subsidiaries in 2023–24, underscoring reliance on market funding.

Shifts in global appetite for EM assets—EM equity flows swung from +$45bn in 2023 to -$12bn YTD 2025—can depress valuations of First Pacific and its listed units, raising funding costs.

Strong investor relations, transparent reporting and diversified funding—First Pacific’s mix of bank loans, bond markets and equity placements—help sustain access to international and local capital pools.

- 2023–24 group issuances ≈ $1.2bn

- EM flows: +$45bn (2023) → -$12bn YTD 2025

- Funding mix: banks, bonds, equity placements

- IR and transparency reduce cost of capital

First Pacific: FX hits reported volatility; costs rise as growth cushions demand

First Pacific faces FX translation risk as IDR fell ~3.5% and PHP ~2.1% YTD 2024, raising reported volatility; hedging and natural offsets mitigate but do not eliminate exposure. Regional rates (Philippines policy 6.25% in 2025) and rising input costs (soy/wheat/palm +12–18% in 2024) squeeze margins, while GDP growth (ID 4.5–5%, PH 5–5.5% 2024–25) supports demand.

| Metric | 2024/25 |

|---|---|

| IDR vs USD | -3.5% YTD 2024 |

| PHP vs USD | -2.1% YTD 2024 |

| Philippines policy rate | 6.25% (2025) |

| Food input costs | +12–18% YoY 2024 |

| GDP growth | ID 4.5–5%, PH 5–5.5% |

Preview Before You Purchase

First Pacific PESTLE Analysis

The preview shown here is the exact First Pacific PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Gain a strategic advantage with our targeted PESTLE Analysis of First Pacific—unpack the political, economic, social, technological, legal, and environmental forces shaping its trajectory and translate them into actionable strategy. Ideal for investors, consultants, and executives seeking concise, research-backed insights. Purchase the full report to access the complete breakdown, editable files, and practical recommendations for immediate use.

Political factors

Geopolitical Stability in Southeast Asia

Regional tensions in the South China Sea, with 2024 incidents up 12% year-on-year, continue to affect trade routes that carry about 30% of global maritime trade and influence investor sentiment across Asia-Pacific.

First Pacific must navigate complex China-ASEAN diplomatic relations where its key assets in the Philippines and Indonesia represent over 60% of its NAV, exposing it to policy and operational risk.

The company closely monitors developments to mitigate disruptions to maritime logistics and cross-border capital flows, noting that 18% of regional FDI into ASEAN in 2023 was China-linked, heightening exposure to geopolitical shifts.

Indonesian Policy Continuity

Following administrative stabilization through 2025, policy continuity in Indonesia is vital for Indofood and First Pacific; government food security programs and downstreaming mandates (e.g., 2024 palm oil downstream targets boosting domestic refining capacity by ~15%) reshape capital allocation and capex plans across holdings.

Philippine Infrastructure Priorities

The Philippine government’s push for infrastructure via PPPs—70 projects worth PHP 3.2 trillion announced under the 2024-2025 pipeline—directly benefits Metro Pacific Investments Corporation (MPIC) by expanding opportunities in transport, water and energy concessions.

Political backing for projects like the PHP 735 billion Luzon expressway expansions and Water Sector Asset Management targets a stable capital deployment and potential revenue growth for MPIC’s utilities and toll portfolios.

However, electoral shifts or reallocation of the 2025 national budget (PHP 5.5 trillion) could slow project rollouts, affecting MPIC’s concession timelines and cash flow forecasts.

Hong Kong Regulatory Environment

As a Hong Kong-listed entity, First Pacific faces an evolving SAR regulatory landscape and Greater Bay Area integration, affecting cross-border operations and capital flows; Hong Kong’s Exchanges and Clearing reporting changes in 2024 raised disclosure frequency for SNAP dealings by listed conglomerates.

Compliance with dual local and international standards is mandatory to maintain listing—HKEX’s 2023/24 listing rules and IFRS updates increased compliance costs, contributing to sectoral governance spend rises estimated at 5–8% year-on-year for major holdings.

First Pacific adjusts corporate governance and transparency frameworks to meet tightened reporting and ESG disclosure expectations; by FY2024 the group aligned its reporting cadence with HKEX’s new guidance and expanded audit committee oversight across its principal investees.

- Subject to HKEX 2023/24 rule changes and Greater Bay Area regulatory alignment

- Dual compliance: HK authorities plus IFRS/global standards—governance costs up ~5–8% YoY

- Governance adaptations: increased disclosure frequency, expanded audit oversight (implemented FY2024)

Resource Nationalism Trends

The rise in resource nationalism in Southeast Asia and the Philippines risks revisions to mining laws and ownership rules that could affect Philex Mining; in 2024 Philippine mineral royalties proposals sought increases from 2–5% to 6–10% and local processing mandates rose in 3 jurisdictions.

First Pacific models these shifts—estimating potential EBITDA reductions of 5–12% under higher royalty scenarios—and engages governments to secure fiscal stability and sustainable extraction practices.

- 2024 royalty proposals: +4–8 percentage points in target countries

- Estimated EBITDA hit to mining assets: 5–12% under worst-case

- Policy focus: higher local processing and domestic value-add requirements

South China Sea tensions imperil First Pacific NAV, PPPs and mining margins

Regional SCS tensions (incidents +12% YoY in 2024) and China-ASEAN diplomacy risk trade routes (~30% global maritime trade) impacting First Pacific’s Philippines/Indonesia NAV (>60%). Policy continuity in Indonesia and Philippine PPPs (PHP 3.2tn pipeline) shape MPIC capex; resource nationalism (royalty proposals +4–8ppt) could cut mining EBITDA 5–12%. HKEX/IFRS rule changes raised governance costs ~5–8% YoY.

| Metric | 2024/25 |

|---|---|

| SCS incidents | +12% YoY |

| Maritime trade affected | ~30% |

| NAV exposure | >60% |

| PPP pipeline | PHP 3.2tn |

| Royalty change | +4–8ppt |

| Mining EBITDA risk | −5–12% |

| Governance cost rise | +5–8% YoY |

What is included in the product

Explores how external macro-environmental factors uniquely affect First Pacific across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by relevant data and forward-looking trends to identify risks and opportunities for executives, investors, and strategists.

A concise First Pacific PESTLE summary that’s visually segmented for quick interpretation, easily dropped into presentations, annotated for local context, and shareable across teams to streamline risk discussions and strategic planning.

Economic factors

Currency Exchange Volatility

First Pacific reports in US dollars while substantial revenue streams come from Indonesian rupiah and Philippine peso; in 2024 FX swings saw the IDR fall about 3.5% vs USD and PHP weaken ~2.1% year-to-date, creating material translation risk for consolidated results.

Significant local-currency depreciation can produce translation losses—First Pacific reported FX-driven impacts in prior annual statements—and could compress reported net income and ROE.

The group uses hedging and cash management to mitigate volatility; in 2024 it disclosed using forward contracts and natural hedges to stabilize dividend remittances from PLDT, Metro Pacific and Indofood affiliates.

Interest Rate Environment

The Asia-Pacific interest rate backdrop—with central banks like the Fed and BSP lifting rates to ~5.25%-5.50% (US) and the Philippines policy rate at 6.25% in 2025—raises First Pacific’s borrowing costs for Metro Pacific and PLDT, potentially squeezing margins on capital-heavy infrastructure and telecom projects.

Inflationary Pressures on Consumers

Regional Economic Growth Trajectories

Indonesia and the Philippines, contributing over 70% of First Pacific’s EBITDA exposure, are projected to grow 4.5–5.0% (Indonesia) and 5.0–5.5% (Philippines) in 2024–2025, supporting rising demand for telecoms, power and processed foods as incomes climb.

First Pacific targets investments aligned with IMF GDP per capita gains and 3–6% annual urbanization-driven consumption growth to capture sectoral expansion.

- Indonesia GDP ~USD 1.3T (2024), Philippines ~USD 420B (2024)

- Telco subscribers and electricity demand up 3–7% y/y

- Processed food consumption rising with urbanization 2–4% annually

Capital Market Access

Access to capital in 2024–25 remains critical for First Pacific to fund expansions of PLDT, Indofood and Metro Pacific; the group tapped roughly $1.2bn in debt and equity issuances across subsidiaries in 2023–24, underscoring reliance on market funding.

Shifts in global appetite for EM assets—EM equity flows swung from +$45bn in 2023 to -$12bn YTD 2025—can depress valuations of First Pacific and its listed units, raising funding costs.

Strong investor relations, transparent reporting and diversified funding—First Pacific’s mix of bank loans, bond markets and equity placements—help sustain access to international and local capital pools.

- 2023–24 group issuances ≈ $1.2bn

- EM flows: +$45bn (2023) → -$12bn YTD 2025

- Funding mix: banks, bonds, equity placements

- IR and transparency reduce cost of capital

First Pacific: FX hits reported volatility; costs rise as growth cushions demand

First Pacific faces FX translation risk as IDR fell ~3.5% and PHP ~2.1% YTD 2024, raising reported volatility; hedging and natural offsets mitigate but do not eliminate exposure. Regional rates (Philippines policy 6.25% in 2025) and rising input costs (soy/wheat/palm +12–18% in 2024) squeeze margins, while GDP growth (ID 4.5–5%, PH 5–5.5% 2024–25) supports demand.

| Metric | 2024/25 |

|---|---|

| IDR vs USD | -3.5% YTD 2024 |

| PHP vs USD | -2.1% YTD 2024 |

| Philippines policy rate | 6.25% (2025) |

| Food input costs | +12–18% YoY 2024 |

| GDP growth | ID 4.5–5%, PH 5–5.5% |

Preview Before You Purchase

First Pacific PESTLE Analysis

The preview shown here is the exact First Pacific PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.