Firstsource Solutions Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

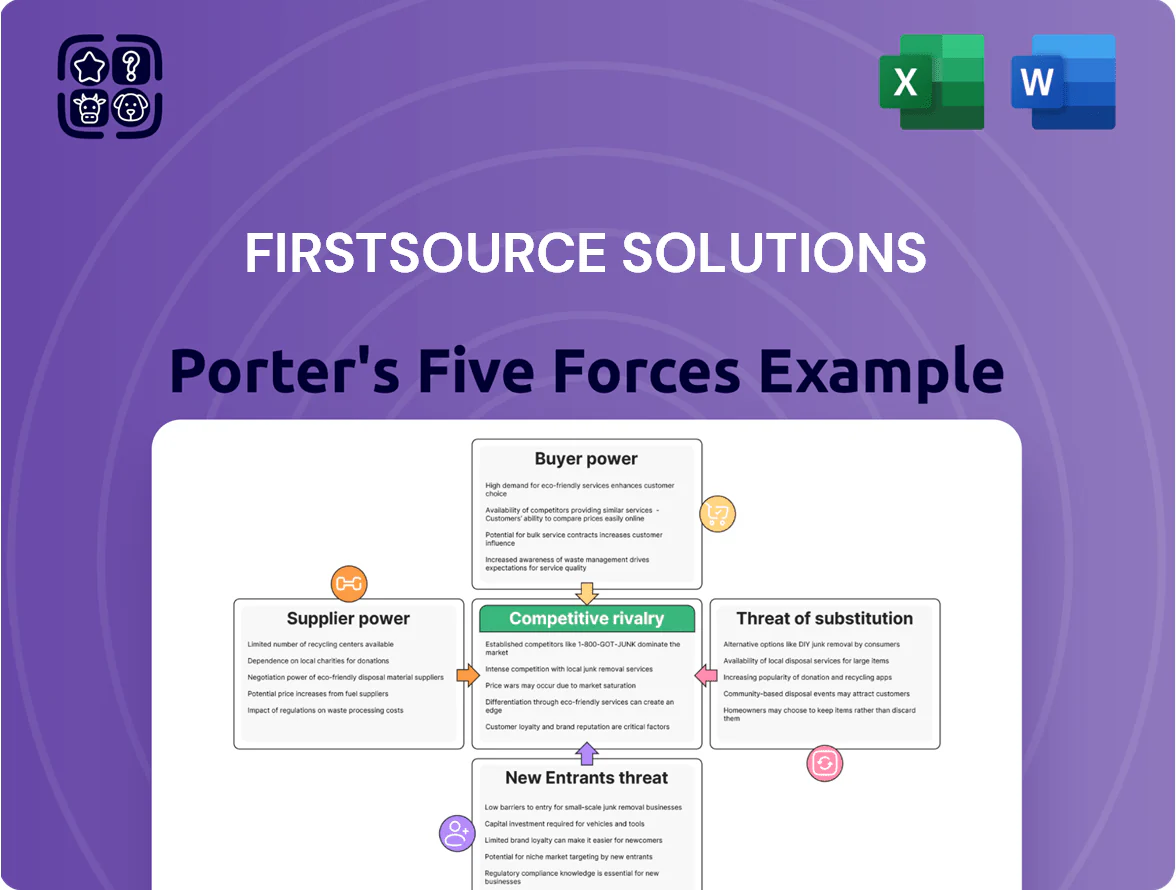

Suppliers Bargaining Power

Access to Specialized Tech Talent

Firstsource’s main suppliers are skilled professionals—especially AI and data analytics experts—whose scarcity by late 2025 raised supplier bargaining power; global demand for AI specialists grew ~35% year‑over‑year in 2024–25, pushing salaries up 20–40% in India and 25–50% in the US.

Dependence on Cloud and Infrastructure Providers

Firstsource depends on major cloud and CRM providers—Microsoft Azure, AWS, and niche CRM vendors—which gives those suppliers strong leverage because migrating large-scale ops costs millions and takes months; for example, cloud spend for comparable BPOs rose ~18% in 2024, pressuring margins.

AI and Software Licensing Costs

The rise of generative AI and automated workflows forces Firstsource to license advanced third-party models and proprietary algorithms, increasing supplier leverage via tiered pricing and IP limits.

In 2025 enterprise AI license deals often carry 20–40% premium for commercial use; Firstsource faces trade-offs between paying these fees and investing in in-house models.

Securing favorable enterprise-wide licenses—and avoiding pay-per-call models that can raise costs 30%+—is critical to sustain Firstsource’s cost leadership.

Geographic Concentration of Operations

The supply of labor and infrastructure for Firstsource Solutions is concentrated in hubs like India, the Philippines, and the US; in 2024 about 68% of global contact center seats were in India and the Philippines combined, raising supplier leverage from local utilities and real estate.

Local regulatory shifts, currency moves, or geopolitical risks can sharply raise operating costs; diversifying delivery centers across multiple regions reduces reliance on any single infrastructure supplier and lowers exposure to localized rent or power hikes.

Spreading capacity also helps manage localized cost escalations—if one hub sees a 15% rent rise, impact is diluted across the network, protecting margins.

- Diverse hubs cut single-region supplier power

- India+Philippines ≈68% of seats (2024)

- Mitigates risks from local utility/real estate hikes

- A 15% local rent shock is diluted by spread

Hardware and Telecommunications Vendors

Reliable telecom and hardware are core to Firstsource’s back-office services; global IT spending on telecom infrastructure hit $1.2 trillion in 2024, keeping demand high for high-speed, secure links.

Large telcos keep stable bargaining power due to scale and redundancy, so Firstsource uses multi-year contracts and SLAs to lock pricing and priority support.

A 10% rise in connectivity costs or 12–20 week hardware lead times would meaningfully compress margins given Firstsource’s FY2024 gross margin of ~18.5%.

- Long-term contracts: limits price volatility

- Telco dominance: stable supplier leverage

- Cost shock risk: 10%+ connectivity rise hurts margins

- Lead-time risk: 12–20 week hardware delays

Suppliers Gain Leverage: AI Pay, Cloud Costs and Telco Capex Drive Premiums

Suppliers (AI talent, cloud/CRM vendors, telcos, local infrastructure) hold moderate–high power: AI talent pay rose 20–50% (2024–25), cloud spend +18% (2024), telecom capex $1.2T (2024); supplier premiums (AI licenses) 20–40% in 2025; Firstsource uses multi‑year contracts, diversified hubs (India+PH ≈68% seats) to limit shocks.

| Supplier | Key metric | 2024–25 |

|---|---|---|

| AI talent | Salary increase | 20–50% |

| Cloud | Spend change | +18% |

| AI licenses | Premium | 20–40% |

| Telco/infra | Global capex | $1.2T |

| Delivery seats | Concentration | India+PH ≈68% |

What is included in the product

Tailored exclusively for Firstsource Solutions, this Porter's Five Forces overview uncovers key competitive drivers, supplier/buyer power, threat of substitutes and entry barriers, highlighting disruptive risks and strategic levers to protect market share.

A concise Porter's Five Forces snapshot for Firstsource Solutions—quickly assess client bargaining power, competitive rivalry, supplier dynamics, entry threats, and substitution risk to streamline strategic decisions.

Customers Bargaining Power

High Concentration of Large Enterprise Clients

Firstsource serves large healthcare, BFSI and media clients that together accounted for about 72% of revenue in FY2024, giving these buyers strong leverage to demand custom solutions and steep pricing concessions. Large accounts, some representing 5–10% of revenue each, can move margins materially if lost, as seen when a top client accounted for ~8% of FY2024 revenue. So Firstsource must deepen ties with integrated, high-value services and escalated SLAs to protect revenue.

Low Switching Costs for Commodity Services

In standardized back-office and basic support segments, clients face low switching costs and can move to rivals or in-house teams if prices rise or quality slips; Firstsource saw 2024 attrition-linked contract migrations amount to about 3% of revenue, highlighting this risk.

Firstsource counters by pushing digital transformation and proprietary platforms—its Blue Prism and AI-led workflows reduced client operational costs by up to 22% in pilot accounts in 2024—creating technical lock-in that cuts churn and price sensitivity.

Demand for Outcome-Based Pricing Models

By end-2025 clients are shifting from input-based fees to outcome-based pricing, giving buyers more bargaining power as providers absorb operational risk and must meet KPIs tied to fees.

Firstsource will need to show measurable value—eg, a 10–20% lift in collections or a 15% cut in patient churn—to justify performance-linked fees and protect margins.

This trend forces sustained operational excellence: Firstsource must hit higher accuracy and productivity targets or face fee reductions and client churn.

Availability of Global Sourcing Options

Customers can choose from global integrators, niche boutiques, and regional BPM firms, enabling strict multi-vendor bidding that compresses fees—global outsourcing market was about USD 92.5bn in 2024, raising buyer leverage.

Firstsource counters this by specializing in US healthcare and UK banking, where its 2024 vertical revenues (approx 54% of total) and domain expertise reduce price-only comparisons.

- Wide supplier set fuels price competition

- Multi-vendor RFPs lower margins

- Firstsource: vertical focus—healthcare, banking

- 2024: ~54% revenue from target verticals

Client Sophistication and Internal Capabilities

Many of Firstsource’s clients have the tech and scale to build captive centers, creating a constant backdoor threat that strengthens customer bargaining power.

Firstsource must prove external delivery beats insourcing on cost and innovation; contracts often hinge on demonstrated savings—typically 10–25% vs estimated internal run-rates in industry bids.

Offering advanced AI stacks (generative models, automation platforms) that clients haven’t mastered is a key retention lever—Firstsource reported 2024 AI-driven revenue growth of ~18%.

- Clients can insource; threat raises price pressure

- Must show 10–25% cost advantage

- AI access (18% AI revenue growth in 2024) is key differentiator

Client concentration pressures Firstsource; AI growth and vertical focus counterbalance

Large healthcare/BFSI buyers (72% of FY2024 rev) exert strong leverage, with several clients at 5–10% each and one ~8%, forcing pricing concessions and customized SLAs. Low switching costs in basic BPO drove ~3% FY2024 revenue migration, while outcome-based pricing shift (2025) raises buyer risk-transfer demands. Firstsource’s AI/automation (18% AI revenue growth in 2024) and vertical focus (≈54% rev) are key retention levers.

| Metric | Value |

|---|---|

| FY2024 rev from top verticals | ≈54% |

| Clients concentration | 72% from healthcare,BFSI,media |

| Top client | ~8% of rev |

| Attrition-linked migrations | ~3% of rev (2024) |

| AI revenue growth | ~18% (2024) |

Same Document Delivered

Firstsource Solutions Porter's Five Forces Analysis

This preview shows the exact Firstsource Solutions Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full version you'll get—fully formatted and ready for download and use the moment you buy.

You're looking at the actual, professionally written analysis; once you complete your purchase, you’ll get instant access to this same file.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Suppliers Bargaining Power

Access to Specialized Tech Talent

Firstsource’s main suppliers are skilled professionals—especially AI and data analytics experts—whose scarcity by late 2025 raised supplier bargaining power; global demand for AI specialists grew ~35% year‑over‑year in 2024–25, pushing salaries up 20–40% in India and 25–50% in the US.

Dependence on Cloud and Infrastructure Providers

Firstsource depends on major cloud and CRM providers—Microsoft Azure, AWS, and niche CRM vendors—which gives those suppliers strong leverage because migrating large-scale ops costs millions and takes months; for example, cloud spend for comparable BPOs rose ~18% in 2024, pressuring margins.

AI and Software Licensing Costs

The rise of generative AI and automated workflows forces Firstsource to license advanced third-party models and proprietary algorithms, increasing supplier leverage via tiered pricing and IP limits.

In 2025 enterprise AI license deals often carry 20–40% premium for commercial use; Firstsource faces trade-offs between paying these fees and investing in in-house models.

Securing favorable enterprise-wide licenses—and avoiding pay-per-call models that can raise costs 30%+—is critical to sustain Firstsource’s cost leadership.

Geographic Concentration of Operations

The supply of labor and infrastructure for Firstsource Solutions is concentrated in hubs like India, the Philippines, and the US; in 2024 about 68% of global contact center seats were in India and the Philippines combined, raising supplier leverage from local utilities and real estate.

Local regulatory shifts, currency moves, or geopolitical risks can sharply raise operating costs; diversifying delivery centers across multiple regions reduces reliance on any single infrastructure supplier and lowers exposure to localized rent or power hikes.

Spreading capacity also helps manage localized cost escalations—if one hub sees a 15% rent rise, impact is diluted across the network, protecting margins.

- Diverse hubs cut single-region supplier power

- India+Philippines ≈68% of seats (2024)

- Mitigates risks from local utility/real estate hikes

- A 15% local rent shock is diluted by spread

Hardware and Telecommunications Vendors

Reliable telecom and hardware are core to Firstsource’s back-office services; global IT spending on telecom infrastructure hit $1.2 trillion in 2024, keeping demand high for high-speed, secure links.

Large telcos keep stable bargaining power due to scale and redundancy, so Firstsource uses multi-year contracts and SLAs to lock pricing and priority support.

A 10% rise in connectivity costs or 12–20 week hardware lead times would meaningfully compress margins given Firstsource’s FY2024 gross margin of ~18.5%.

- Long-term contracts: limits price volatility

- Telco dominance: stable supplier leverage

- Cost shock risk: 10%+ connectivity rise hurts margins

- Lead-time risk: 12–20 week hardware delays

Suppliers Gain Leverage: AI Pay, Cloud Costs and Telco Capex Drive Premiums

Suppliers (AI talent, cloud/CRM vendors, telcos, local infrastructure) hold moderate–high power: AI talent pay rose 20–50% (2024–25), cloud spend +18% (2024), telecom capex $1.2T (2024); supplier premiums (AI licenses) 20–40% in 2025; Firstsource uses multi‑year contracts, diversified hubs (India+PH ≈68% seats) to limit shocks.

| Supplier | Key metric | 2024–25 |

|---|---|---|

| AI talent | Salary increase | 20–50% |

| Cloud | Spend change | +18% |

| AI licenses | Premium | 20–40% |

| Telco/infra | Global capex | $1.2T |

| Delivery seats | Concentration | India+PH ≈68% |

What is included in the product

Tailored exclusively for Firstsource Solutions, this Porter's Five Forces overview uncovers key competitive drivers, supplier/buyer power, threat of substitutes and entry barriers, highlighting disruptive risks and strategic levers to protect market share.

A concise Porter's Five Forces snapshot for Firstsource Solutions—quickly assess client bargaining power, competitive rivalry, supplier dynamics, entry threats, and substitution risk to streamline strategic decisions.

Customers Bargaining Power

High Concentration of Large Enterprise Clients

Firstsource serves large healthcare, BFSI and media clients that together accounted for about 72% of revenue in FY2024, giving these buyers strong leverage to demand custom solutions and steep pricing concessions. Large accounts, some representing 5–10% of revenue each, can move margins materially if lost, as seen when a top client accounted for ~8% of FY2024 revenue. So Firstsource must deepen ties with integrated, high-value services and escalated SLAs to protect revenue.

Low Switching Costs for Commodity Services

In standardized back-office and basic support segments, clients face low switching costs and can move to rivals or in-house teams if prices rise or quality slips; Firstsource saw 2024 attrition-linked contract migrations amount to about 3% of revenue, highlighting this risk.

Firstsource counters by pushing digital transformation and proprietary platforms—its Blue Prism and AI-led workflows reduced client operational costs by up to 22% in pilot accounts in 2024—creating technical lock-in that cuts churn and price sensitivity.

Demand for Outcome-Based Pricing Models

By end-2025 clients are shifting from input-based fees to outcome-based pricing, giving buyers more bargaining power as providers absorb operational risk and must meet KPIs tied to fees.

Firstsource will need to show measurable value—eg, a 10–20% lift in collections or a 15% cut in patient churn—to justify performance-linked fees and protect margins.

This trend forces sustained operational excellence: Firstsource must hit higher accuracy and productivity targets or face fee reductions and client churn.

Availability of Global Sourcing Options

Customers can choose from global integrators, niche boutiques, and regional BPM firms, enabling strict multi-vendor bidding that compresses fees—global outsourcing market was about USD 92.5bn in 2024, raising buyer leverage.

Firstsource counters this by specializing in US healthcare and UK banking, where its 2024 vertical revenues (approx 54% of total) and domain expertise reduce price-only comparisons.

- Wide supplier set fuels price competition

- Multi-vendor RFPs lower margins

- Firstsource: vertical focus—healthcare, banking

- 2024: ~54% revenue from target verticals

Client Sophistication and Internal Capabilities

Many of Firstsource’s clients have the tech and scale to build captive centers, creating a constant backdoor threat that strengthens customer bargaining power.

Firstsource must prove external delivery beats insourcing on cost and innovation; contracts often hinge on demonstrated savings—typically 10–25% vs estimated internal run-rates in industry bids.

Offering advanced AI stacks (generative models, automation platforms) that clients haven’t mastered is a key retention lever—Firstsource reported 2024 AI-driven revenue growth of ~18%.

- Clients can insource; threat raises price pressure

- Must show 10–25% cost advantage

- AI access (18% AI revenue growth in 2024) is key differentiator

Client concentration pressures Firstsource; AI growth and vertical focus counterbalance

Large healthcare/BFSI buyers (72% of FY2024 rev) exert strong leverage, with several clients at 5–10% each and one ~8%, forcing pricing concessions and customized SLAs. Low switching costs in basic BPO drove ~3% FY2024 revenue migration, while outcome-based pricing shift (2025) raises buyer risk-transfer demands. Firstsource’s AI/automation (18% AI revenue growth in 2024) and vertical focus (≈54% rev) are key retention levers.

| Metric | Value |

|---|---|

| FY2024 rev from top verticals | ≈54% |

| Clients concentration | 72% from healthcare,BFSI,media |

| Top client | ~8% of rev |

| Attrition-linked migrations | ~3% of rev (2024) |

| AI revenue growth | ~18% (2024) |

Same Document Delivered

Firstsource Solutions Porter's Five Forces Analysis

This preview shows the exact Firstsource Solutions Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full version you'll get—fully formatted and ready for download and use the moment you buy.

You're looking at the actual, professionally written analysis; once you complete your purchase, you’ll get instant access to this same file.