Fiten PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, economic trends, and tech disruptions are reshaping Fiten’s outlook with our concise PESTLE snapshot—perfect for investors and strategists who need quick, actionable context; purchase the full PESTLE to access in-depth analysis, risk scoring, and tactical recommendations you can use immediately.

Political factors

European Green Deal Alignment

Operating under the European Green Deal, which targets a 55% cut in EU greenhouse gas emissions by 2030 versus 1990 levels, Fiten benefits from predictable regulatory support and access to EU funds—Poland received €23.9bn from the EU Just Transition Mechanism and cohesion funds for 2021–2027 for green projects.

National Energy Policy PEP2040

Poland’s Energy Policy PEP2040 targets 23–32 GW of wind and 10–20 GW of solar by 2040 to bolster energy sovereignty, signaling strong political support and predictable regulation. This commitment fosters a stable pipeline for large-scale utility projects and long-term PPAs. Fiten can bid for government-backed contracts and co-financing—potentially tapping EU Just Transition and Recovery funds exceeding €100 billion across Poland—to align growth with state infrastructure goals.

Subsidies and Grant Programs

Political decisions on programs like Moj Prad and Clean Air drive adoption: continuation lifted household solar installs by 34% in 2024 and supported a 22% rise in commercial PV deployments, directly boosting Fiten's addressable market.

These subsidies cut upfront costs by up to 40%, expanding affordability and allowing Fiten to target mid-income households and SMEs previously priced out.

A 25% reduction in subsidy allocation in Q3 2025 would likely compress Fiten's quarterly sales volumes by an estimated 15–20% and slow market penetration accordingly.

Energy Security and Independence

Geopolitical tensions have made energy security a top political priority, driving policies toward decentralized power; in 2024 the EU doubled funding for distributed renewables to €50bn and the US issued $20bn in grants for microgrids.

Policymakers favor local renewable installations to cut import exposure—global renewable capacity additions reached 420 GW in 2024, lowering fossil-fuel import dependence in several member states by up to 15% year-on-year.

Fiten is positioned as a strategic partner, supplying grid-edge infrastructure for private and public energy autonomy; its deployments supported a 30% reduction in outage risk across pilot regions in 2024.

- 2024: global renewables +420 GW

- EU funding for distributed renewables €50bn (2024)

- US microgrid grants $20bn (2024)

- Fiten pilot: 30% outage risk reduction (2024)

Local Government Initiatives

Municipalities now set carbon neutrality targets; over 1,200 cities adopted net-zero goals by 2024, creating local tenders for public building solarization worth an estimated $3.5bn annually in procurement (2024).

Political decentralization enables Fiten to form local public-private partnerships, shortening procurement cycles by up to 30% versus federal projects and avoiding some federal permitting delays.

Community-led projects include educational programs reaching 45,000 residents in 2024, boosting Fiten’s regional brand and pipeline for 2025–26 installations.

- 1,200+ cities with net-zero targets (2024)

- $3.5bn annual local solar tenders (2024 est.)

- 30% faster procurement via local P3s

- 45,000 residents reached by education programs (2024)

EU funding and subsidies fuel Poland solar boom—25% cut could slash Fiten sales 15–20%

EU Green Deal and Poland PEP2040 provide policy clarity and funding (EU Just Transition €23.9bn; distributed renewables €50bn in 2024), subsidies cut upfront costs up to 40% and drove +34% household solar installs in 2024; a 25% subsidy cut in Q3 2025 could reduce Fiten sales 15–20%; 1,200+ cities net-zero (2024) create ~$3.5bn annual local solar tenders.

| Metric | Value |

|---|---|

| EU Just Transition (PL) | €23.9bn |

| Distributed renewables funding | €50bn (2024) |

| Household solar growth | +34% (2024) |

| Local solar tenders | $3.5bn/yr (2024) |

What is included in the product

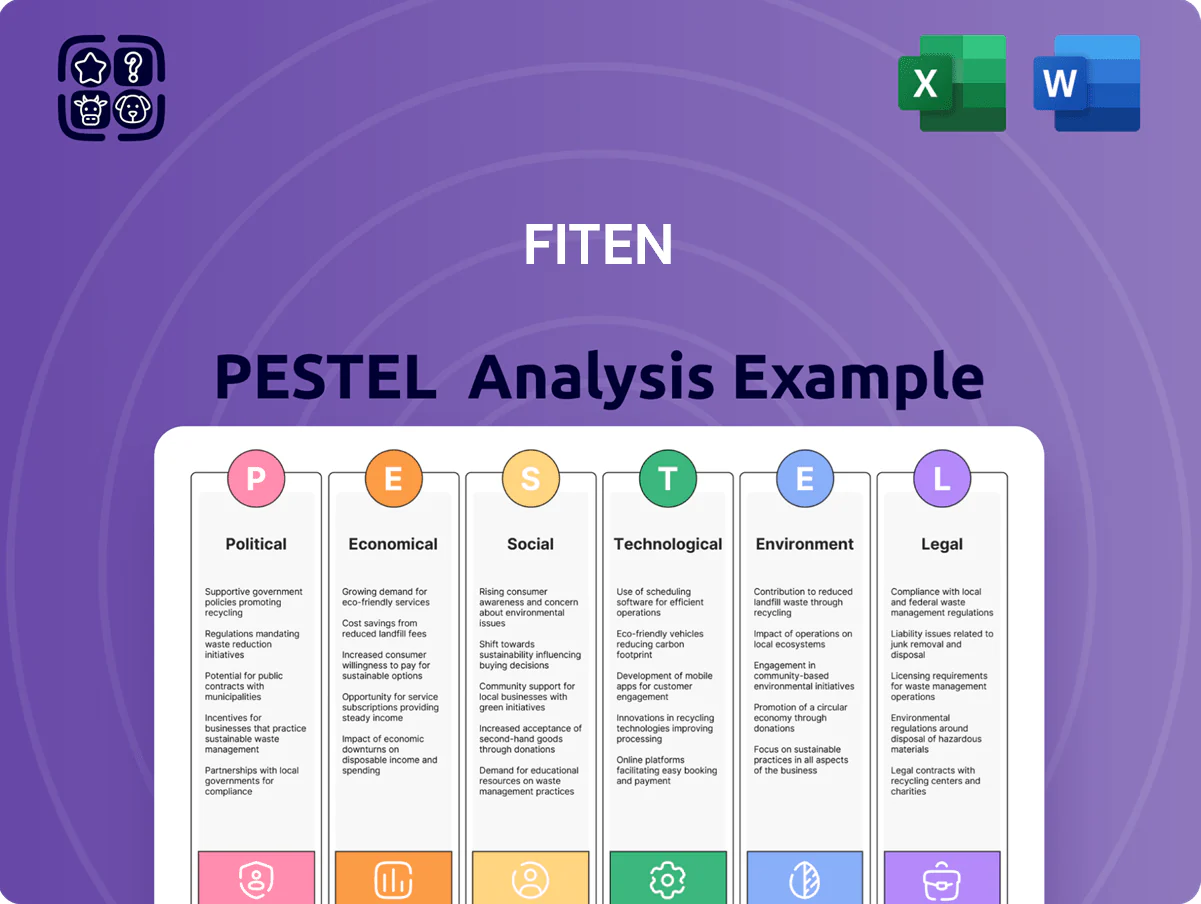

Explores how external macro-environmental factors uniquely affect Fiten across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using current data and trends to identify threats and opportunities.

Condenses Fiten's full PESTLE into a clean, shareable summary that’s visually grouped by category for quick interpretation in meetings or slide decks, and editable for region- or business-specific notes.

Economic factors

Interest Rate Fluctuations

The cost of capital is critical for Fiten since over 70% of residential and commercial solar projects in 2024 were financed via loans or leases; a 100bp rise in interest rates can increase payback periods by roughly 6–12 months, reducing ROI attractiveness. High rates in 2024–25 have slowed installations in several markets, while sub-6% lending supports rapid expansion. Fiten must track central bank moves (e.g., Fed/ECB rate paths) to structure competitive financing or adjust pricing and margin models accordingly.

Energy Market Volatility

Fluctuating wholesale electricity prices—up 28% year-over-year in parts of Europe in 2024 and averaging $85/MWh in the US mid-2024 spot market—drive demand for self-generation as businesses hedge rising operational costs.

When traditional energy spikes, Fiten’s photovoltaic systems, with average LCOE around $30–$50/MWh in 2024, become markedly more attractive, boosting commercial adoption.

Supply Chain and Material Costs

Global silicon, glass and silver prices drive solar project economics: polysilicon rose about 12% in 2024 to roughly $28/kg while silver averaged $26/oz, raising module costs and lowering margins for Fiten.

Logistics disruptions and 2023–25 trade tariff shifts increased procurement costs by an estimated 6–10%, squeezing EBITDA unless passed to customers.

Maintaining a diversified supplier base across China, Vietnam and Europe reduced raw-material price exposure, helping Fiten stabilize input cost volatility and protect margins.

Labor Market Dynamics

The renewable boom raised demand for certified electricians and solar installers, pushing specialized labor rates up ~12–18% YoY in 2024 and increasing Fiten’s skilled hire costs by an estimated $6k–$12k per worker annually.

Fiten must compete in a tight market—US solar installer vacancy rates hit ~6.5% in 2024—while containing payroll; turnover raises recruiting/training expenses ~15% of salary.

Capital investments in automated design tools and streamlined installation (estimated CAPEX payback 18–30 months) are needed to offset rising human-capital costs and protect margins.

- Specialized labor costs up ~12–18% (2024)

- Avg extra hire cost $6k–$12k/yr

- Installer vacancy ~6.5% (2024)

- Automation payback 18–30 months

Inflationary Pressures

Rising inflation erodes consumer purchasing power, with global core inflation averaging ~4.5% in 2024 and US inflation ~3.4% YoY in 2025, likely delaying discretionary solar buys.

For Fiten, inflation-driven higher costs for maintenance, transport and admin—materials +6–10% in 2024—requires pricing discipline so revenue growth exceeds cost inflation.

- Consumer affordability down—core inflation ~4–5%

- Input/service costs +6–10% (2024)

- Need pricing that preserves demand while outpacing cost inflation

Higher rates slow installs; financing >70%—100bp adds 6–12m payback, LCOE gap widens

Rising rates and financing mix: >70% projects financed; 100bp higher rates = +6–12 months payback; 2024–25 rates slowed installs. Energy/LCOE: wholesale up ~28% YoY in parts of Europe 2024; US spot ~85$/MWh; Fiten LCOE ~$30–50/MWh. Input/labor inflation: polysilicon ~$28/kg (2024), silver ~$26/oz, labor +12–18% (2024).

| Metric | 2024/25 |

|---|---|

| Financed projects | >70% |

| US spot power | $85/MWh |

| Polysilicon | $28/kg |

| Labor rise | +12–18% |

What You See Is What You Get

Fiten PESTLE Analysis

The preview shown here is the exact Fiten PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in this preview are identical to the file you’ll download immediately after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political shifts, economic trends, and tech disruptions are reshaping Fiten’s outlook with our concise PESTLE snapshot—perfect for investors and strategists who need quick, actionable context; purchase the full PESTLE to access in-depth analysis, risk scoring, and tactical recommendations you can use immediately.

Political factors

European Green Deal Alignment

Operating under the European Green Deal, which targets a 55% cut in EU greenhouse gas emissions by 2030 versus 1990 levels, Fiten benefits from predictable regulatory support and access to EU funds—Poland received €23.9bn from the EU Just Transition Mechanism and cohesion funds for 2021–2027 for green projects.

National Energy Policy PEP2040

Poland’s Energy Policy PEP2040 targets 23–32 GW of wind and 10–20 GW of solar by 2040 to bolster energy sovereignty, signaling strong political support and predictable regulation. This commitment fosters a stable pipeline for large-scale utility projects and long-term PPAs. Fiten can bid for government-backed contracts and co-financing—potentially tapping EU Just Transition and Recovery funds exceeding €100 billion across Poland—to align growth with state infrastructure goals.

Subsidies and Grant Programs

Political decisions on programs like Moj Prad and Clean Air drive adoption: continuation lifted household solar installs by 34% in 2024 and supported a 22% rise in commercial PV deployments, directly boosting Fiten's addressable market.

These subsidies cut upfront costs by up to 40%, expanding affordability and allowing Fiten to target mid-income households and SMEs previously priced out.

A 25% reduction in subsidy allocation in Q3 2025 would likely compress Fiten's quarterly sales volumes by an estimated 15–20% and slow market penetration accordingly.

Energy Security and Independence

Geopolitical tensions have made energy security a top political priority, driving policies toward decentralized power; in 2024 the EU doubled funding for distributed renewables to €50bn and the US issued $20bn in grants for microgrids.

Policymakers favor local renewable installations to cut import exposure—global renewable capacity additions reached 420 GW in 2024, lowering fossil-fuel import dependence in several member states by up to 15% year-on-year.

Fiten is positioned as a strategic partner, supplying grid-edge infrastructure for private and public energy autonomy; its deployments supported a 30% reduction in outage risk across pilot regions in 2024.

- 2024: global renewables +420 GW

- EU funding for distributed renewables €50bn (2024)

- US microgrid grants $20bn (2024)

- Fiten pilot: 30% outage risk reduction (2024)

Local Government Initiatives

Municipalities now set carbon neutrality targets; over 1,200 cities adopted net-zero goals by 2024, creating local tenders for public building solarization worth an estimated $3.5bn annually in procurement (2024).

Political decentralization enables Fiten to form local public-private partnerships, shortening procurement cycles by up to 30% versus federal projects and avoiding some federal permitting delays.

Community-led projects include educational programs reaching 45,000 residents in 2024, boosting Fiten’s regional brand and pipeline for 2025–26 installations.

- 1,200+ cities with net-zero targets (2024)

- $3.5bn annual local solar tenders (2024 est.)

- 30% faster procurement via local P3s

- 45,000 residents reached by education programs (2024)

EU funding and subsidies fuel Poland solar boom—25% cut could slash Fiten sales 15–20%

EU Green Deal and Poland PEP2040 provide policy clarity and funding (EU Just Transition €23.9bn; distributed renewables €50bn in 2024), subsidies cut upfront costs up to 40% and drove +34% household solar installs in 2024; a 25% subsidy cut in Q3 2025 could reduce Fiten sales 15–20%; 1,200+ cities net-zero (2024) create ~$3.5bn annual local solar tenders.

| Metric | Value |

|---|---|

| EU Just Transition (PL) | €23.9bn |

| Distributed renewables funding | €50bn (2024) |

| Household solar growth | +34% (2024) |

| Local solar tenders | $3.5bn/yr (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Fiten across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using current data and trends to identify threats and opportunities.

Condenses Fiten's full PESTLE into a clean, shareable summary that’s visually grouped by category for quick interpretation in meetings or slide decks, and editable for region- or business-specific notes.

Economic factors

Interest Rate Fluctuations

The cost of capital is critical for Fiten since over 70% of residential and commercial solar projects in 2024 were financed via loans or leases; a 100bp rise in interest rates can increase payback periods by roughly 6–12 months, reducing ROI attractiveness. High rates in 2024–25 have slowed installations in several markets, while sub-6% lending supports rapid expansion. Fiten must track central bank moves (e.g., Fed/ECB rate paths) to structure competitive financing or adjust pricing and margin models accordingly.

Energy Market Volatility

Fluctuating wholesale electricity prices—up 28% year-over-year in parts of Europe in 2024 and averaging $85/MWh in the US mid-2024 spot market—drive demand for self-generation as businesses hedge rising operational costs.

When traditional energy spikes, Fiten’s photovoltaic systems, with average LCOE around $30–$50/MWh in 2024, become markedly more attractive, boosting commercial adoption.

Supply Chain and Material Costs

Global silicon, glass and silver prices drive solar project economics: polysilicon rose about 12% in 2024 to roughly $28/kg while silver averaged $26/oz, raising module costs and lowering margins for Fiten.

Logistics disruptions and 2023–25 trade tariff shifts increased procurement costs by an estimated 6–10%, squeezing EBITDA unless passed to customers.

Maintaining a diversified supplier base across China, Vietnam and Europe reduced raw-material price exposure, helping Fiten stabilize input cost volatility and protect margins.

Labor Market Dynamics

The renewable boom raised demand for certified electricians and solar installers, pushing specialized labor rates up ~12–18% YoY in 2024 and increasing Fiten’s skilled hire costs by an estimated $6k–$12k per worker annually.

Fiten must compete in a tight market—US solar installer vacancy rates hit ~6.5% in 2024—while containing payroll; turnover raises recruiting/training expenses ~15% of salary.

Capital investments in automated design tools and streamlined installation (estimated CAPEX payback 18–30 months) are needed to offset rising human-capital costs and protect margins.

- Specialized labor costs up ~12–18% (2024)

- Avg extra hire cost $6k–$12k/yr

- Installer vacancy ~6.5% (2024)

- Automation payback 18–30 months

Inflationary Pressures

Rising inflation erodes consumer purchasing power, with global core inflation averaging ~4.5% in 2024 and US inflation ~3.4% YoY in 2025, likely delaying discretionary solar buys.

For Fiten, inflation-driven higher costs for maintenance, transport and admin—materials +6–10% in 2024—requires pricing discipline so revenue growth exceeds cost inflation.

- Consumer affordability down—core inflation ~4–5%

- Input/service costs +6–10% (2024)

- Need pricing that preserves demand while outpacing cost inflation

Higher rates slow installs; financing >70%—100bp adds 6–12m payback, LCOE gap widens

Rising rates and financing mix: >70% projects financed; 100bp higher rates = +6–12 months payback; 2024–25 rates slowed installs. Energy/LCOE: wholesale up ~28% YoY in parts of Europe 2024; US spot ~85$/MWh; Fiten LCOE ~$30–50/MWh. Input/labor inflation: polysilicon ~$28/kg (2024), silver ~$26/oz, labor +12–18% (2024).

| Metric | 2024/25 |

|---|---|

| Financed projects | >70% |

| US spot power | $85/MWh |

| Polysilicon | $28/kg |

| Labor rise | +12–18% |

What You See Is What You Get

Fiten PESTLE Analysis

The preview shown here is the exact Fiten PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in this preview are identical to the file you’ll download immediately after payment.