Five Below Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

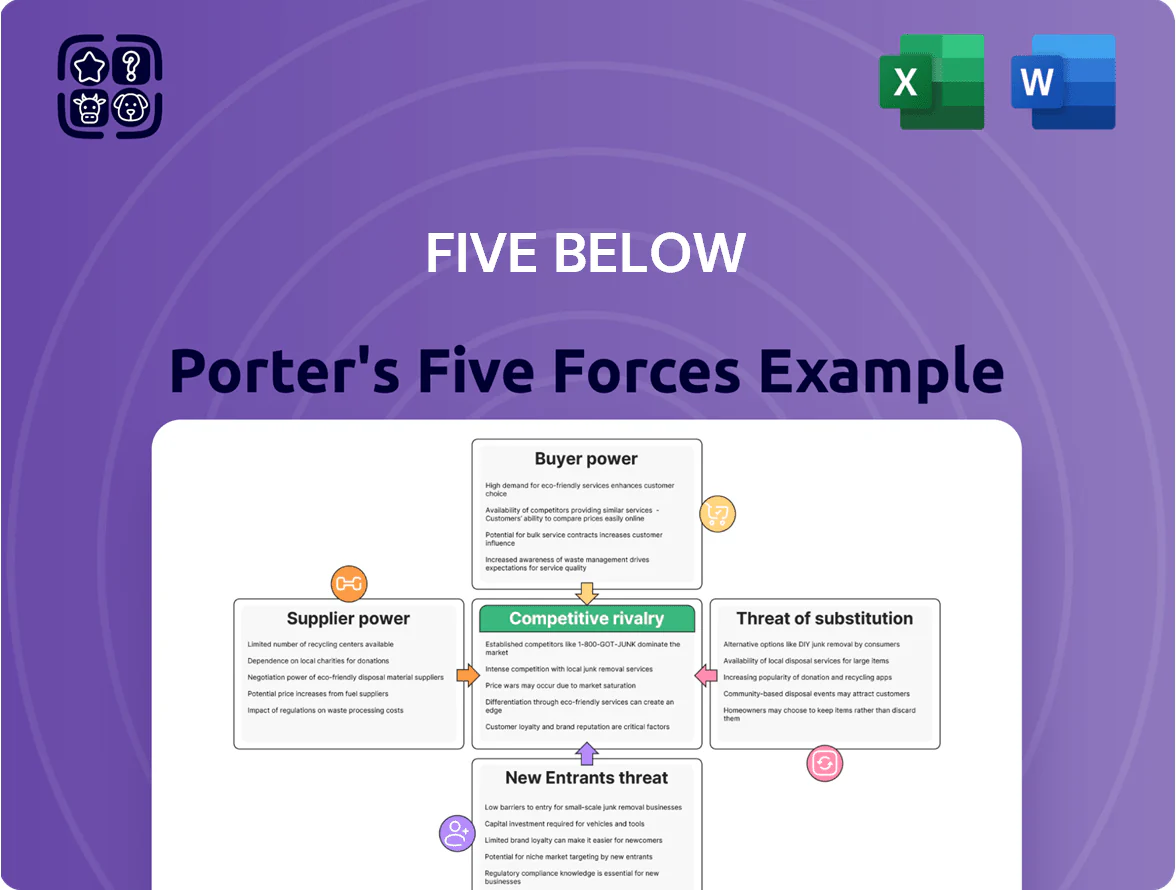

Five Below faces moderate buyer power, intense rivalry among discount retailers, low supplier leverage, moderate threat from substitutes (online value retailers), and barriers to new entrants driven by scale and real-estate expertise.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Five Below’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented Global Vendor Base

Five Below sources products from hundreds of global vendors, so no single supplier holds meaningful leverage; in 2024 the company reported over 2,500 active SKUs sourced across Asia and North America, enabling fast supplier switching if costs or quality slip. This fragmentation lets Five Below negotiate low unit costs and favorable payment terms, and in 2024 supplier concentration remained under 5% of COGS per vendor, preventing any partner from dictating terms.

Low Switching Costs for Unbranded Goods

The bulk of Five Below’s assortment is unbranded or private-label, making items easy to replicate and sourced from many manufacturers; in 2024 private-label represented over 60% of SKU breadth in value retailers. This lets Five Below shift orders to lower-cost suppliers—reducing unit cost risk—without harming brand perception or shelf consistency. Suppliers thus hold limited leverage, as products act like interchangeable commodities in the $10-and-under value segment.

Significant Purchasing Volume and Scale

With over 1,700 stores by end-2025, Five Below’s scale gives it strong buying leverage: vendors accept lower per-unit margins for predictable, high-volume orders, lowering COGS and boosting gross margin—Five Below reported a 34.9% gross margin in FY2024, reflecting such supplier concessions; this volume-driven dynamic shifts bargaining power decisively toward the retailer during contract talks, enabling favorable payment terms, slotting allowances, and promotional support.

In-House Product Development Capabilities

Five Below has shifted toward in-house design and direct factory sourcing, cutting out intermediaries and reducing supplier bargaining power; management reported private-label goods accounted for about 67% of merchandise in FY2024 (fiscal year ended Jan 29, 2024).

Controlling design and sourcing lets Five Below set costs, protect margins (gross margin 33.1% in FY2024), and reduce exposure to third-party price pressure on high-turn SKUs.

- 67% private-label goods in FY2024

- Gross margin 33.1% FY2024

- Lower supplier price leverage via vertical integration

Supply Chain Diversification and Nearshoring

By late 2025 Five Below reduced sourcing concentration from >60% in one region to under 35%, cutting average ocean transit time 12% via multiple routes and nearshoring some SKUs to Mexico and Central America.

That diversification and greater logistics control lowers supplier leverage, helping preserve the sub- $5 to $25 value pricing and cushioning gross margin swings during 2022–25 shipping-rate volatility (peak rate hikes >50%).

- Concentration fell from >60% to <35%

- Transit time down 12%

- Nearshored SKUs added in 2023–25

- Helps protect low-price model vs 50%+ peak shipping spikes

Five Below: Diversified sourcing, 67% private-label, 33–35% margins, faster nearshoring

Suppliers hold low bargaining power: Five Below sources 2,500+ SKUs from hundreds of vendors (no vendor >5% COGS in 2024), 67% private-label, scale of 1,700+ stores by end-2025, gross margin ~33–34.9% in FY2024, and sourcing concentration cut from >60% to <35% with 12% faster transit after nearshoring.

| Metric | 2024/2025 |

|---|---|

| Active SKUs | 2,500+ |

| Private-label share | 67% |

| Top-vendor COGS | <5% |

| Stores (end-2025) | 1,700+ |

| Gross margin FY2024 | 33–34.9% |

| Sourcing concentration | >60% → <35% |

| Transit time | -12% |

What is included in the product

Tailored exclusively for Five Below, this Porter's Five Forces overview uncovers key drivers of competition, buyer and supplier influence, entry barriers, substitute threats, and disruptive forces that affect pricing power and market share.

Compact, one-sheet Porter's Five Forces for Five Below—quickly gauge supplier, buyer, and competitive pressure to inform pricing, sourcing, and expansion decisions.

Customers Bargaining Power

Low Switching Costs for Value Shoppers

Customers face virtually no financial penalty switching from Five Below; average ticket was about $11.50 in FY2024, so moving to Dollar Tree, Target clearance, or online discounters costs little. Low-cost, discretionary items make brand loyalty secondary to price and stock, and Five Below’s comparable 2024 same-store sales growth of 1.1% shows pressure. This ease of switching forces Five Below to preserve its treasure-hunt experience and tight pricing.

High Price Sensitivity in the Discount Segment

The target mix of teens and value-conscious parents is highly price-sensitive; survey data from 2024 shows 62% of US shoppers in the dollar/discount cohort will switch brands after a 5% price rise, hitting discretionary items first.

Five Below’s $1–$5+ price image means even small across-the-store increases can cut foot traffic; same-store-sales growth fell from 5.8% in FY2022 to 1.9% in FY2024 when promotional intensity dropped.

This sensitivity constrains passing on rising COS (cost of sales) or rent increases—margin-preserving price hikes risk larger volume loss, as average basket size is just $6.32 (2024), limiting per-customer leeway.

Information Transparency and Price Comparison

In 2025, mobile price checks let Five Below shoppers compare aisle prices to Amazon, Walmart, and Dollar Tree in seconds; 72% of US shoppers report using smartphones to compare prices in-store (2024 NRF). This real-time transparency raises customer leverage—if a tech accessory or snack lists lower elsewhere, shoppers will find it immediately—so Five Below must keep in-store value, exclusive SKUs, or price-matching to defend margin and traffic.

Discretionary Nature of Product Assortment

Five Below sells mainly discretionary, impulse items so customers can easily walk away; in FY2024 about 70% of transactions included items under 5 dollars, underscoring want-driven demand and high buyer refusal power.

This forces Five Below to refresh SKUs frequently—company reported a 25% yearly SKU turnover in 2024—to spark repeat impulse buys and protect comps.

- Impulse/nonessential goods → high refusal power

- ~70% transactions <$5 in FY2024

- 25% annual SKU turnover (2024)

- Freshness drives traffic, sales per store

Expansion of the Five Beyond Pricing Tier

The expansion of Five Below’s higher-priced tier (items >$5) has broadened choice but raised customer scrutiny of value; in FY2024 Five Below reported average unit volume rising 3.2% while mix of >$5 items reached about 18% of SKUs, pushing shoppers to compare quality versus Target and Walmart.

As price points climb, buyers demand better materials and performance, increasing their bargaining power slightly because they now weigh cost-to-quality more and can easily substitute at big-box stores—this dynamic nudges Five Below toward clearer value messaging and tighter quality control.

- FY2024: >$5 SKUs ≈18% of assortment

- Average unit volume +3.2% in FY2024

- Comparative substitutes: Target/Walmart raise switching risk

High buyer power: price-sensitive shoppers and mobile checks squeeze Five Below margins

Customers have high bargaining power: low switching costs, price-sensitive core demo, and mobile price checks (72% use smartphones in-store, NRF 2024) pressure Five Below to keep prices, exclusive SKUs, and high SKU churn (25% in 2024). FY2024: avg ticket $11.50, basket $6.32, >$5 SKUs ~18%, comps growth 1.1%, same-store sales 1.9%; small price moves risk traffic loss.

| Metric | 2024 |

|---|---|

| Avg ticket | $11.50 |

| Avg basket | $6.32 |

| SKU turnover | 25% |

| >$5 SKUs | 18% |

| Smartphone price checks | 72% |

Preview Before You Purchase

Five Below Porter's Five Forces Analysis

This preview shows the exact Five Below Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document provides a concise assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, fully formatted and ready for download. Upon payment you’ll get instant access to this same professional file.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Five Below faces moderate buyer power, intense rivalry among discount retailers, low supplier leverage, moderate threat from substitutes (online value retailers), and barriers to new entrants driven by scale and real-estate expertise.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Five Below’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented Global Vendor Base

Five Below sources products from hundreds of global vendors, so no single supplier holds meaningful leverage; in 2024 the company reported over 2,500 active SKUs sourced across Asia and North America, enabling fast supplier switching if costs or quality slip. This fragmentation lets Five Below negotiate low unit costs and favorable payment terms, and in 2024 supplier concentration remained under 5% of COGS per vendor, preventing any partner from dictating terms.

Low Switching Costs for Unbranded Goods

The bulk of Five Below’s assortment is unbranded or private-label, making items easy to replicate and sourced from many manufacturers; in 2024 private-label represented over 60% of SKU breadth in value retailers. This lets Five Below shift orders to lower-cost suppliers—reducing unit cost risk—without harming brand perception or shelf consistency. Suppliers thus hold limited leverage, as products act like interchangeable commodities in the $10-and-under value segment.

Significant Purchasing Volume and Scale

With over 1,700 stores by end-2025, Five Below’s scale gives it strong buying leverage: vendors accept lower per-unit margins for predictable, high-volume orders, lowering COGS and boosting gross margin—Five Below reported a 34.9% gross margin in FY2024, reflecting such supplier concessions; this volume-driven dynamic shifts bargaining power decisively toward the retailer during contract talks, enabling favorable payment terms, slotting allowances, and promotional support.

In-House Product Development Capabilities

Five Below has shifted toward in-house design and direct factory sourcing, cutting out intermediaries and reducing supplier bargaining power; management reported private-label goods accounted for about 67% of merchandise in FY2024 (fiscal year ended Jan 29, 2024).

Controlling design and sourcing lets Five Below set costs, protect margins (gross margin 33.1% in FY2024), and reduce exposure to third-party price pressure on high-turn SKUs.

- 67% private-label goods in FY2024

- Gross margin 33.1% FY2024

- Lower supplier price leverage via vertical integration

Supply Chain Diversification and Nearshoring

By late 2025 Five Below reduced sourcing concentration from >60% in one region to under 35%, cutting average ocean transit time 12% via multiple routes and nearshoring some SKUs to Mexico and Central America.

That diversification and greater logistics control lowers supplier leverage, helping preserve the sub- $5 to $25 value pricing and cushioning gross margin swings during 2022–25 shipping-rate volatility (peak rate hikes >50%).

- Concentration fell from >60% to <35%

- Transit time down 12%

- Nearshored SKUs added in 2023–25

- Helps protect low-price model vs 50%+ peak shipping spikes

Five Below: Diversified sourcing, 67% private-label, 33–35% margins, faster nearshoring

Suppliers hold low bargaining power: Five Below sources 2,500+ SKUs from hundreds of vendors (no vendor >5% COGS in 2024), 67% private-label, scale of 1,700+ stores by end-2025, gross margin ~33–34.9% in FY2024, and sourcing concentration cut from >60% to <35% with 12% faster transit after nearshoring.

| Metric | 2024/2025 |

|---|---|

| Active SKUs | 2,500+ |

| Private-label share | 67% |

| Top-vendor COGS | <5% |

| Stores (end-2025) | 1,700+ |

| Gross margin FY2024 | 33–34.9% |

| Sourcing concentration | >60% → <35% |

| Transit time | -12% |

What is included in the product

Tailored exclusively for Five Below, this Porter's Five Forces overview uncovers key drivers of competition, buyer and supplier influence, entry barriers, substitute threats, and disruptive forces that affect pricing power and market share.

Compact, one-sheet Porter's Five Forces for Five Below—quickly gauge supplier, buyer, and competitive pressure to inform pricing, sourcing, and expansion decisions.

Customers Bargaining Power

Low Switching Costs for Value Shoppers

Customers face virtually no financial penalty switching from Five Below; average ticket was about $11.50 in FY2024, so moving to Dollar Tree, Target clearance, or online discounters costs little. Low-cost, discretionary items make brand loyalty secondary to price and stock, and Five Below’s comparable 2024 same-store sales growth of 1.1% shows pressure. This ease of switching forces Five Below to preserve its treasure-hunt experience and tight pricing.

High Price Sensitivity in the Discount Segment

The target mix of teens and value-conscious parents is highly price-sensitive; survey data from 2024 shows 62% of US shoppers in the dollar/discount cohort will switch brands after a 5% price rise, hitting discretionary items first.

Five Below’s $1–$5+ price image means even small across-the-store increases can cut foot traffic; same-store-sales growth fell from 5.8% in FY2022 to 1.9% in FY2024 when promotional intensity dropped.

This sensitivity constrains passing on rising COS (cost of sales) or rent increases—margin-preserving price hikes risk larger volume loss, as average basket size is just $6.32 (2024), limiting per-customer leeway.

Information Transparency and Price Comparison

In 2025, mobile price checks let Five Below shoppers compare aisle prices to Amazon, Walmart, and Dollar Tree in seconds; 72% of US shoppers report using smartphones to compare prices in-store (2024 NRF). This real-time transparency raises customer leverage—if a tech accessory or snack lists lower elsewhere, shoppers will find it immediately—so Five Below must keep in-store value, exclusive SKUs, or price-matching to defend margin and traffic.

Discretionary Nature of Product Assortment

Five Below sells mainly discretionary, impulse items so customers can easily walk away; in FY2024 about 70% of transactions included items under 5 dollars, underscoring want-driven demand and high buyer refusal power.

This forces Five Below to refresh SKUs frequently—company reported a 25% yearly SKU turnover in 2024—to spark repeat impulse buys and protect comps.

- Impulse/nonessential goods → high refusal power

- ~70% transactions <$5 in FY2024

- 25% annual SKU turnover (2024)

- Freshness drives traffic, sales per store

Expansion of the Five Beyond Pricing Tier

The expansion of Five Below’s higher-priced tier (items >$5) has broadened choice but raised customer scrutiny of value; in FY2024 Five Below reported average unit volume rising 3.2% while mix of >$5 items reached about 18% of SKUs, pushing shoppers to compare quality versus Target and Walmart.

As price points climb, buyers demand better materials and performance, increasing their bargaining power slightly because they now weigh cost-to-quality more and can easily substitute at big-box stores—this dynamic nudges Five Below toward clearer value messaging and tighter quality control.

- FY2024: >$5 SKUs ≈18% of assortment

- Average unit volume +3.2% in FY2024

- Comparative substitutes: Target/Walmart raise switching risk

High buyer power: price-sensitive shoppers and mobile checks squeeze Five Below margins

Customers have high bargaining power: low switching costs, price-sensitive core demo, and mobile price checks (72% use smartphones in-store, NRF 2024) pressure Five Below to keep prices, exclusive SKUs, and high SKU churn (25% in 2024). FY2024: avg ticket $11.50, basket $6.32, >$5 SKUs ~18%, comps growth 1.1%, same-store sales 1.9%; small price moves risk traffic loss.

| Metric | 2024 |

|---|---|

| Avg ticket | $11.50 |

| Avg basket | $6.32 |

| SKU turnover | 25% |

| >$5 SKUs | 18% |

| Smartphone price checks | 72% |

Preview Before You Purchase

Five Below Porter's Five Forces Analysis

This preview shows the exact Five Below Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document provides a concise assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, fully formatted and ready for download. Upon payment you’ll get instant access to this same professional file.