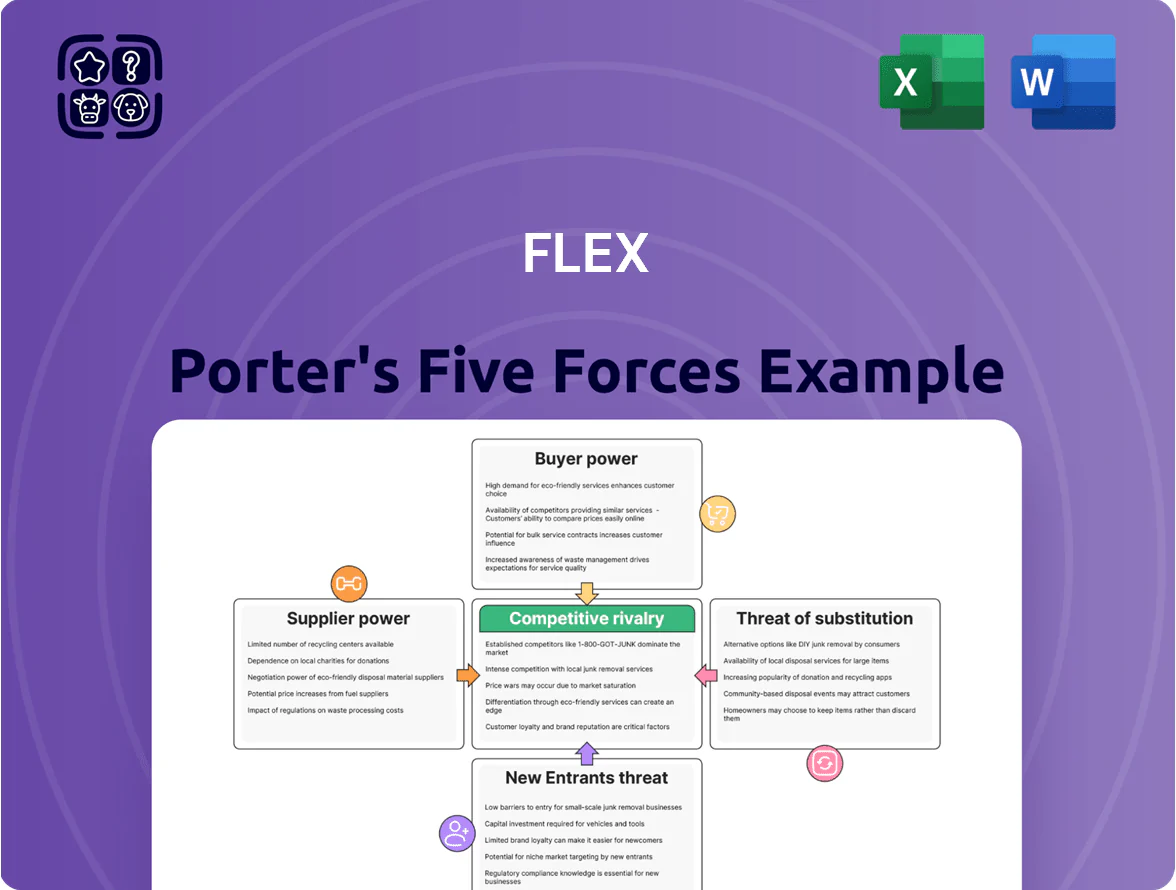

Flex Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Flex faces moderate supplier leverage, intense buyer demands, and significant rivalry from manufacturing and supply-chain specialists, with emerging tech and substitutes shaping future threats.

This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Flex’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of semiconductor and component providers

The supplier base for critical electronic components is highly consolidated: top 10 semiconductor firms (TSMC, Samsung, Intel, SK Hynix, Micron, Broadcom, Nvidia, Qualcomm, Infineon, and Texas Instruments) accounted for about 75% of global semiconductor revenue in 2024; Flex remains dependent on these vendors for specialized chips and high-value materials as of late 2025.

This concentration gives suppliers leverage: during 2021–25 demand shocks and the 2024 capacity tightness, premium pricing rose 8–15% and allocation rules tightened, increasing Flex’s procurement risk and margin pressure.

Impact of regionalized supply chain shifts

Geopolitical tensions and nearshoring have pushed suppliers to expand into regional hubs—North America, EU, and ASEAN—raising Flex’s average sourced-cost variance by about 6% and lengthening lead times by 1–3 weeks versus 2019 levels. Localized hubs empower niche vendors (e.g., semiconductor packaging in Malaysia) and give essential regional suppliers greater pricing leverage, increasing supplier bargaining power for critical components by an estimated 10–15% in 2024.

Switching costs for specialized technical inputs

High switching costs arise for suppliers of proprietary tech and custom-engineered components in healthcare and automotive, where Flex spent $1.2B on supplier qualification and compliance in 2024 to meet FDA and IATF 16949 standards. Replacing such suppliers can take 6–12 months, disrupt production lines, and raise unit costs by an estimated 8–15%. These barriers give suppliers notable bargaining power and raise operational risk.

Fluctuations in raw material and energy costs

Suppliers of copper, resin, and specialty metals hold high leverage for Flex because global copper fell 6% in 2024 but showed 18% volatility year-to-year, and resin resin prices spiked 23% in Q3 2024 on tight supply and higher feedstock costs.

Flex sees cost escalations tied to commodity swings and energy: industrial gas and power tariffs rose ~12% in 2024 in key Asian plants, raising unit manufacturing costs and giving suppliers pricing power despite pass-through contracts.

Pass-through contracts shift final billing, but initial cash-flow and margin pressure from sudden 10–30% raw-material jumps remain a supplier lever that can force order timing, minimum volumes, or longer lead times.

- High supplier leverage: copper volatility ~18% YoY (2024)

- Resin prices: +23% spike Q3 2024

- Energy costs: +12% 2024 in key Asian plants

- Pass-through protects revenue but not short-term margin/cash

Supplier forward integration threats

There is a moderate threat of supplier forward integration as large component makers—led by firms like Qualcomm and Infineon—offer reference designs and modular platforms that skip contract manufacturers; in 2024, 18% of semiconductor revenue came from integrated system solutions, up from 12% in 2020 (SIA/IDC mix estimate).

This trend lets suppliers capture higher gross margins (often 5–10 percentage points above pure-component sales) and potentially compete with Flex’s assembly and system-integration services, pressuring pricing and margins.

What this estimate hides: adoption varies by end market; automotive and industrial show higher supplier-led integration than consumer electronics.

- Moderate threat: rising supplier system revenue (18% in 2024)

- Makers offer reference designs and modular solutions

- Suppliers can gain 5–10 pp higher gross margins

- Impact concentrated in automotive and industrial segments

Supplier dominance: top semis, soaring costs & forward-integration risk squeeze OEMs

Suppliers hold high bargaining power: top 10 semis ~75% revenue (2024); specialty supplier switching costs 6–12 months and $1.2B supplier qualification spend (2024); commodity shocks: copper volatility ~18% YoY, resin +23% Q3 2024, energy +12% (Asian plants 2024); supplier system revenue rose to 18% (2024), raising forward-integration threat ~10–15%.

| Metric | 2024 |

|---|---|

| Top-10 semis rev share | ~75% |

| Supplier qual spend | $1.2B |

| Copper volatility | ~18% YoY |

| Resin spike | +23% Q3 |

| Energy rise (Asia) | +12% |

| Supplier system rev | 18% |

What is included in the product

Comprehensive Five Forces analysis for Flex that uncovers competitive pressures, buyer and supplier leverage, entry and substitute threats, and industry rivalry—supported by data-driven insights and strategic implications for pricing, profitability, and defensive positioning.

One-sheet Five Forces summary with customizable pressure levels and a radar chart for instant strategic clarity—copy-ready for decks, integrable with Excel dashboards, and simple enough for non-finance users.

Customers Bargaining Power

High concentration of revenue among key clients

Flex relies heavily on a handful of tier‑one clients in consumer electronics, automotive, and cloud infrastructure that drive large volumes; in 2024 the top 10 customers accounted for roughly 50% of revenue, giving them strong leverage.

Those clients push hard on pricing and service terms—large orders enable single-digit percentage price concessions and strict SLAs—squeezing Flex’s margins.

Losing one tier‑one account could cut annual sales by mid‑single digits to low‑teens percent and leave factories underutilized, raising fixed‑cost per unit.

Low switching costs for standardized assembly

For high-volume, simple consumer assemblies, switching costs are low—buyers can shift production between EMS providers in weeks, so price dominates; in 2024 EMS spot bids for commodity PCBs fell ~6% YoY, strengthening buyer leverage.

Customer demand for end-to-end lifecycle services

Sophisticated buyers now demand end-to-end lifecycle services—design, circular-economy takeback, and complex logistics—raising Flex’s per‑customer value but giving clients leverage to push integrated, margin‑squeezing pricing across services; in 2024 Flex reported services revenue growth of ~9% but services gross margin lagged product margin by ~6pp. Customers with in‑house R&D dictate manufacturing specs and cost targets, forcing Flex to absorb process changes and compress margins further.

Impact of vertical integration by OEMs

Some large OEMs, including examples like Apple and Tesla, are moving select high-value processes in-house to protect IP; in 2024, 12–15% of semiconductor and precision assembly volume shifted to captive production among top 50 OEMs.

This threat of backward integration strengthens customers’ bargaining power, so Flex must prove cost-efficiency and tech edge—Flex reported a 2024 gross margin of ~13% versus peers 10–18%.

What this hides: if onboarding or quality gaps appear, a 5–10% unit-cost gap makes OEMs switch to internal builds.

- OEMs bringing 12–15% volume in-house (2024)

- Flex 2024 gross margin ~13%

- 5–10% cost gap triggers OEM insourcing

Price transparency and competitive bidding

The EMS industry’s open-book accounting and multi-round RFPs give buyers clear visibility into Flex Ltd.’s cost base, enabling large customers to push unit prices down; in 2024 EMS gross margins averaged about 7–9%, pressuring suppliers to cut costs.

Customers routinely run competitive bidding across several manufacturers, with top 10 OEMs commanding >50% of volumes, so Flex must keep innovating in automation and supply-chain optimization to stay price-competitive.

Here’s the quick math: trimming operations costs by 100 basis points on $8.0B revenue (FY2024) raises operating profit ~ $80M, so efficiency investments directly protect margins.

- Open-book RFPs give buyers cost visibility

- Multi-round bids drive down unit prices

- Top OEMs concentrate volume, raising buyer leverage

- 1% cost cut ≈ $80M operating benefit on $8B revenue

Flex’s OEM concentration fuels margin edge but faces insourcing and pricing pressure

Major OEMs drive ~50% of Flex’s revenue (top 10, 2024), giving buyers strong price and SLA leverage; losing one tier‑one client cuts sales mid‑single to low‑teens %. Large buyers push single‑digit price concessions and use open‑book RFPs, and 12–15% of volume shifted in‑house (2024), raising insourcing threat—Flex’s FY2024 gross margin ~13% vs EMS avg 7–9%.

| Metric | 2024 |

|---|---|

| Top‑10 customer share | ~50% |

| Revenue (FY2024) | $8.0B |

| Flex gross margin | ~13% |

| EMS avg gross margin | 7–9% |

| OEM insourcing shift | 12–15% |

Same Document Delivered

Flex Porter's Five Forces Analysis

This preview displays the exact Flex Porter Five Forces Analysis you'll receive after purchase—no placeholders or mockups, fully formatted and ready for immediate download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Flex faces moderate supplier leverage, intense buyer demands, and significant rivalry from manufacturing and supply-chain specialists, with emerging tech and substitutes shaping future threats.

This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Flex’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of semiconductor and component providers

The supplier base for critical electronic components is highly consolidated: top 10 semiconductor firms (TSMC, Samsung, Intel, SK Hynix, Micron, Broadcom, Nvidia, Qualcomm, Infineon, and Texas Instruments) accounted for about 75% of global semiconductor revenue in 2024; Flex remains dependent on these vendors for specialized chips and high-value materials as of late 2025.

This concentration gives suppliers leverage: during 2021–25 demand shocks and the 2024 capacity tightness, premium pricing rose 8–15% and allocation rules tightened, increasing Flex’s procurement risk and margin pressure.

Impact of regionalized supply chain shifts

Geopolitical tensions and nearshoring have pushed suppliers to expand into regional hubs—North America, EU, and ASEAN—raising Flex’s average sourced-cost variance by about 6% and lengthening lead times by 1–3 weeks versus 2019 levels. Localized hubs empower niche vendors (e.g., semiconductor packaging in Malaysia) and give essential regional suppliers greater pricing leverage, increasing supplier bargaining power for critical components by an estimated 10–15% in 2024.

Switching costs for specialized technical inputs

High switching costs arise for suppliers of proprietary tech and custom-engineered components in healthcare and automotive, where Flex spent $1.2B on supplier qualification and compliance in 2024 to meet FDA and IATF 16949 standards. Replacing such suppliers can take 6–12 months, disrupt production lines, and raise unit costs by an estimated 8–15%. These barriers give suppliers notable bargaining power and raise operational risk.

Fluctuations in raw material and energy costs

Suppliers of copper, resin, and specialty metals hold high leverage for Flex because global copper fell 6% in 2024 but showed 18% volatility year-to-year, and resin resin prices spiked 23% in Q3 2024 on tight supply and higher feedstock costs.

Flex sees cost escalations tied to commodity swings and energy: industrial gas and power tariffs rose ~12% in 2024 in key Asian plants, raising unit manufacturing costs and giving suppliers pricing power despite pass-through contracts.

Pass-through contracts shift final billing, but initial cash-flow and margin pressure from sudden 10–30% raw-material jumps remain a supplier lever that can force order timing, minimum volumes, or longer lead times.

- High supplier leverage: copper volatility ~18% YoY (2024)

- Resin prices: +23% spike Q3 2024

- Energy costs: +12% 2024 in key Asian plants

- Pass-through protects revenue but not short-term margin/cash

Supplier forward integration threats

There is a moderate threat of supplier forward integration as large component makers—led by firms like Qualcomm and Infineon—offer reference designs and modular platforms that skip contract manufacturers; in 2024, 18% of semiconductor revenue came from integrated system solutions, up from 12% in 2020 (SIA/IDC mix estimate).

This trend lets suppliers capture higher gross margins (often 5–10 percentage points above pure-component sales) and potentially compete with Flex’s assembly and system-integration services, pressuring pricing and margins.

What this estimate hides: adoption varies by end market; automotive and industrial show higher supplier-led integration than consumer electronics.

- Moderate threat: rising supplier system revenue (18% in 2024)

- Makers offer reference designs and modular solutions

- Suppliers can gain 5–10 pp higher gross margins

- Impact concentrated in automotive and industrial segments

Supplier dominance: top semis, soaring costs & forward-integration risk squeeze OEMs

Suppliers hold high bargaining power: top 10 semis ~75% revenue (2024); specialty supplier switching costs 6–12 months and $1.2B supplier qualification spend (2024); commodity shocks: copper volatility ~18% YoY, resin +23% Q3 2024, energy +12% (Asian plants 2024); supplier system revenue rose to 18% (2024), raising forward-integration threat ~10–15%.

| Metric | 2024 |

|---|---|

| Top-10 semis rev share | ~75% |

| Supplier qual spend | $1.2B |

| Copper volatility | ~18% YoY |

| Resin spike | +23% Q3 |

| Energy rise (Asia) | +12% |

| Supplier system rev | 18% |

What is included in the product

Comprehensive Five Forces analysis for Flex that uncovers competitive pressures, buyer and supplier leverage, entry and substitute threats, and industry rivalry—supported by data-driven insights and strategic implications for pricing, profitability, and defensive positioning.

One-sheet Five Forces summary with customizable pressure levels and a radar chart for instant strategic clarity—copy-ready for decks, integrable with Excel dashboards, and simple enough for non-finance users.

Customers Bargaining Power

High concentration of revenue among key clients

Flex relies heavily on a handful of tier‑one clients in consumer electronics, automotive, and cloud infrastructure that drive large volumes; in 2024 the top 10 customers accounted for roughly 50% of revenue, giving them strong leverage.

Those clients push hard on pricing and service terms—large orders enable single-digit percentage price concessions and strict SLAs—squeezing Flex’s margins.

Losing one tier‑one account could cut annual sales by mid‑single digits to low‑teens percent and leave factories underutilized, raising fixed‑cost per unit.

Low switching costs for standardized assembly

For high-volume, simple consumer assemblies, switching costs are low—buyers can shift production between EMS providers in weeks, so price dominates; in 2024 EMS spot bids for commodity PCBs fell ~6% YoY, strengthening buyer leverage.

Customer demand for end-to-end lifecycle services

Sophisticated buyers now demand end-to-end lifecycle services—design, circular-economy takeback, and complex logistics—raising Flex’s per‑customer value but giving clients leverage to push integrated, margin‑squeezing pricing across services; in 2024 Flex reported services revenue growth of ~9% but services gross margin lagged product margin by ~6pp. Customers with in‑house R&D dictate manufacturing specs and cost targets, forcing Flex to absorb process changes and compress margins further.

Impact of vertical integration by OEMs

Some large OEMs, including examples like Apple and Tesla, are moving select high-value processes in-house to protect IP; in 2024, 12–15% of semiconductor and precision assembly volume shifted to captive production among top 50 OEMs.

This threat of backward integration strengthens customers’ bargaining power, so Flex must prove cost-efficiency and tech edge—Flex reported a 2024 gross margin of ~13% versus peers 10–18%.

What this hides: if onboarding or quality gaps appear, a 5–10% unit-cost gap makes OEMs switch to internal builds.

- OEMs bringing 12–15% volume in-house (2024)

- Flex 2024 gross margin ~13%

- 5–10% cost gap triggers OEM insourcing

Price transparency and competitive bidding

The EMS industry’s open-book accounting and multi-round RFPs give buyers clear visibility into Flex Ltd.’s cost base, enabling large customers to push unit prices down; in 2024 EMS gross margins averaged about 7–9%, pressuring suppliers to cut costs.

Customers routinely run competitive bidding across several manufacturers, with top 10 OEMs commanding >50% of volumes, so Flex must keep innovating in automation and supply-chain optimization to stay price-competitive.

Here’s the quick math: trimming operations costs by 100 basis points on $8.0B revenue (FY2024) raises operating profit ~ $80M, so efficiency investments directly protect margins.

- Open-book RFPs give buyers cost visibility

- Multi-round bids drive down unit prices

- Top OEMs concentrate volume, raising buyer leverage

- 1% cost cut ≈ $80M operating benefit on $8B revenue

Flex’s OEM concentration fuels margin edge but faces insourcing and pricing pressure

Major OEMs drive ~50% of Flex’s revenue (top 10, 2024), giving buyers strong price and SLA leverage; losing one tier‑one client cuts sales mid‑single to low‑teens %. Large buyers push single‑digit price concessions and use open‑book RFPs, and 12–15% of volume shifted in‑house (2024), raising insourcing threat—Flex’s FY2024 gross margin ~13% vs EMS avg 7–9%.

| Metric | 2024 |

|---|---|

| Top‑10 customer share | ~50% |

| Revenue (FY2024) | $8.0B |

| Flex gross margin | ~13% |

| EMS avg gross margin | 7–9% |

| OEM insourcing shift | 12–15% |

Same Document Delivered

Flex Porter's Five Forces Analysis

This preview displays the exact Flex Porter Five Forces Analysis you'll receive after purchase—no placeholders or mockups, fully formatted and ready for immediate download and use the moment you buy.