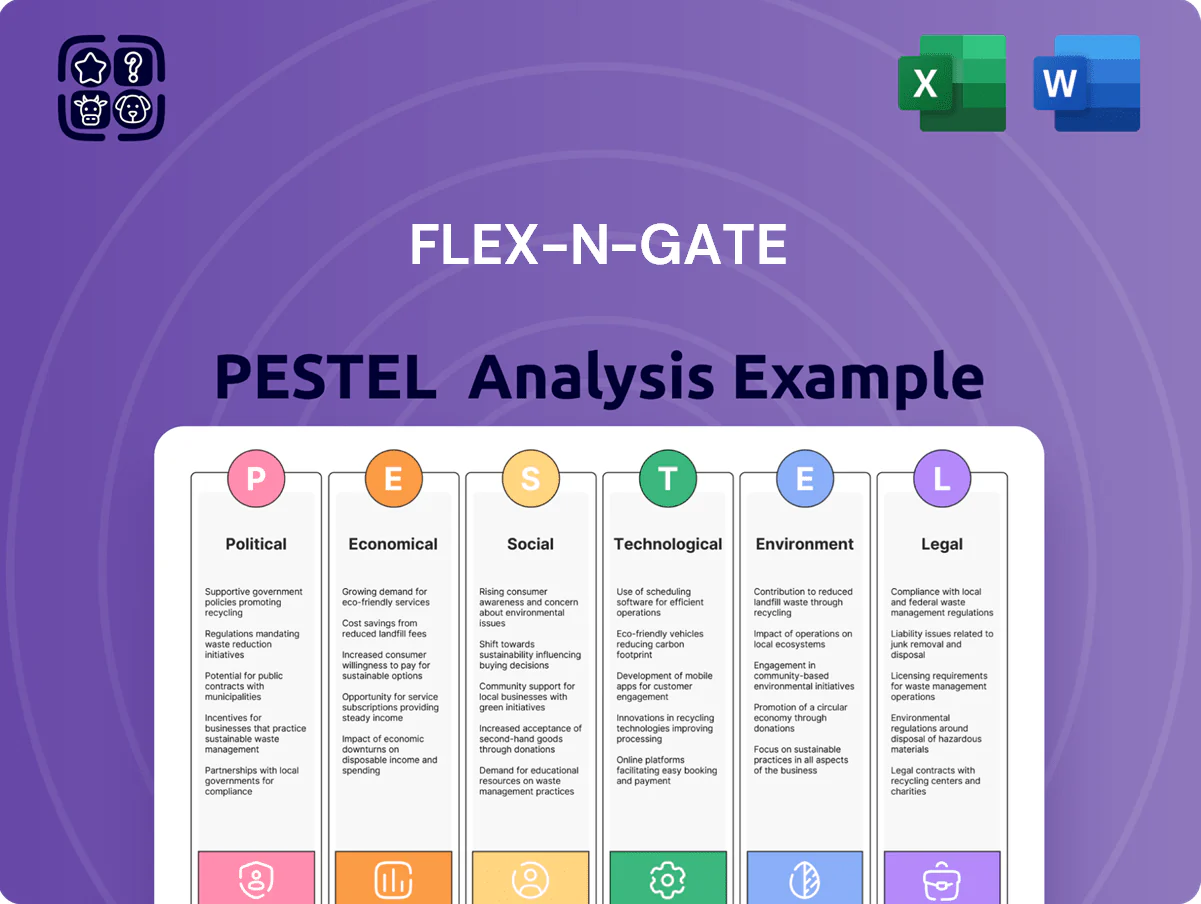

Flex-N-Gate PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, supply-chain dynamics, and rapid automotive-tech innovation are reshaping Flex‑N‑Gate’s strategy and risk profile; our concise PESTLE highlights the pressures and opportunities driving its next phase. Ideal for investors and strategists, the full analysis delivers actionable insights, forecasts, and ready-to-use slides—purchase now to get the complete, fully editable report instantly.

Political factors

Trade Policy and Tariffs

Shifts in USMCA negotiations and bilateral agreements have raised regional content thresholds to ~70% for certain vehicle classes, increasing Flex-N-Gate sourcing from North America and raising production input costs by an estimated 3–5% in 2025.

Revised rules pushed 18% more steel and 22% more resin procurement to US/Mexico suppliers YTD 2025, altering plant utilization and logistics spend.

Tariff variability on Asian components—ranging 0–10% in 2024–25—continues to drive nearshoring and supplier diversification across Flex-N-Gate’s global footprint.

Government EV Incentives

Federal and state EV manufacturing subsidies—including up to $40,000 EV tax credits and $7.5B from DOE’s 2023 battery materials/EV component programs—directly affect demand for Flex-N-Gate’s specialized EV exterior trim and lighting; higher incentives correlate with increased OEM orders and production volumes. Flex-N-Gate must phase ~$200M–$500M capex over 2024–26 to meet government-mandated transition timelines and keep products relevant for EV platforms. The persistence of incentives through 2026 is critical for locking multi-year contracts with major OEMs and underwriting ROI assumptions in bids.

Labor Union Relations

The political influence of labor unions in North America shapes Flex-N-Gate’s wage structures and operational flexibility, with UAW and USW actions contributing to a 6–8% upward pressure on labor costs industrywide in 2025. Collective bargaining trends through 2025, including several high-profile auto supplier agreements, raised strike-avoidance premiums and highlighted the need for positive labor relations to prevent stoppages that can cost suppliers tens of millions per week. Political pressure to retain manufacturing jobs domestically, reinforced by US Inflation Reduction Act incentives and federal/state job retention pledges, factors into plant expansion and closure decisions, with potential subsidies covering up to 20–30% of capital costs in targeted regions.

Geopolitical Stability

Flex-N-Gate's global footprint exposes it to geopolitical tensions that can disrupt logistics and asset security; for example, 2024 supply-chain delays linked to Black Sea and South China Sea tensions raised shipping premiums by ~18% on affected routes.

Political unrest in supplier regions can spike energy and component costs—energy price shocks in 2024 pushed regional manufacturing input costs up to 12%.

Management must monitor diplomatic shifts and maintain contingency inventories and diversified supplier contracts to mitigate cross-border operational and asset risks.

- Global operations sensitive to regional tensions

- 2024 shipping premiums on contested routes rose ~18%

- Regional input cost spikes up to 12% during unrest

- Requires diplomatic monitoring, diversified suppliers, contingency stock

Regulatory Industrial Policy

Nearshoring surge lifts costs, capex $200–500M; EV incentives drive multi‑year OEM orders

USMCA/content rules and tariffs shifted ~18–22% more procurement to US/Mexico in 2024–25, raising input costs ~3–5% and nearshoring capex needs ($200M–$500M through 2026). EV subsidies and DOE programs (>$7.5B) boosted OEM EV orders, tying incentives persistence to multi-year contracts. Labor actions (UAW/USW) lifted labor costs ~6–8% in 2025; geopolitical tensions raised shipping premiums ~18% and input shocks up to 12%.

| Metric | 2024–25 Impact |

|---|---|

| Revenue (2024) | $3.3B |

| Shifted procurement | +18–22% to US/Mexico |

| Input cost rise | 3–5% |

| Labor cost pressure | 6–8% |

| Shipping premiums (contested routes) | +18% |

| Energy/input shocks | up to 12% |

| Required capex | $200M–$500M (2024–26) |

What is included in the product

Explores how macro-environmental factors uniquely affect Flex-N-Gate across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to surface risks and opportunities for executives and investors.

A concise Flex‑N‑Gate PESTLE summary that’s visually segmented by category, easy to drop into presentations or strategy packs, and editable for regional or business‑line notes to speed team alignment and risk discussions.

Economic factors

Interest Rate Environment

High interest rates through 2025—US Fed funds peak near 5.25%–5.50% in 2023–24 and remaining elevated—have compressed consumer purchasing power, contributing to a roughly 8% YoY decline in US light-vehicle sales in 2024 and lower new-vehicle volumes for suppliers like Flex‑N‑Gate.

For Flex‑N‑Gate, higher borrowing costs raise capital expenditure financing costs; a $100m equipment upgrade at a 6% effective borrowing rate versus 3% raises annual interest expense by about $3m.

The company must balance debt-to-equity to preserve liquidity—benchmarking suppliers with net debt/EBITDA ~2.0–3.0—while funding next‑gen tooling and plant expansions amid tighter credit conditions.

Raw Material Price Volatility

Raw material price volatility—notably plastics, aluminum, and steel—remains a primary determinant of Flex-N-Gate profit margins, with steel spot prices averaging roughly $800/ton in 2024 and aluminum near $2,300/ton, pushing input costs materially higher. Global commodity swings in 2024–2025 increased EBITDA sensitivity, prompting sophisticated hedging and long-term offtake contracts to mitigate sudden price spikes that previously lifted COGS by up to 6–8%. The shift to high-performance polymers for lightweighting, adding 5–12% higher per-unit material cost by end-2025, further complicates procurement and requires blended sourcing and strategic supplier partnerships to preserve margins.

Global Inflationary Pressures

Persistent global inflation raised input and transport costs for the auto sector—freight rates rose ~15% and steel prices averaged up ~12% in 2024—pressuring Flex-N-Gate’s margins as utilities and logistics weigh more on plants; OEMs seeking price concessions complicate passing costs through, so Flex-N-Gate must rely on lean manufacturing and productivity gains (targeting 5–8% cost reduction) to protect EBITDA.

Labor Market Dynamics

A tightening market for skilled manufacturing labor has pushed average hourly wages in U.S. auto manufacturing up about 6.5% year-over-year in 2024, increasing Flex-N-Gate’s engineering and tooling payroll and fixed overhead.

Competition for specialized talent raises recruitment and retention costs; reported median salary for tooling engineers reached roughly $95,000 in 2024, pressuring margins.

Rising labor costs and a 12% CAGR in robotics adoption (2022–2025 estimates) drive Flex-N-Gate toward automation to offset scarce technical labor and long-term wage inflation.

- Wages +6.5% YoY (2024)

- Tooling engineer median ~$95,000 (2024)

- Robotics adoption ~12% CAGR (2022–2025)

Currency Exchange Fluctuations

As a global supplier, Flex-N-Gate faces USD volatility versus MXN and EUR; a 10% USD strengthening vs MXN in 2024 would reduce Mexican plant revenue in dollar terms and could erode price competitiveness in North America.

The company reports a significant share of sales from Mexico and Europe, so FX swings affect reported international earnings and margins; in 2024 FX translation impacted comparable EPS across peers by mid-single digits.

Flex-N-Gate uses strategic hedging and localized sourcing—including MXN procurement and Euro-denominated contracts—to mitigate exposure and stabilize cash flows.

- USD vs MXN: 10% move materially affects dollar revenues

- Translation risk: mid-single-digit EPS impact noted in 2024 peers

- Mitigants: currency hedging, localized sourcing, Euro contracts

Higher rates, squeezed margins: automation & hedging stabilize Flex‑N‑Gate EBITDA

Elevated rates and tighter credit (Fed funds ~5.25%–5.50% through 2025) cut US light‑vehicle volumes ~8% YoY in 2024, raising Flex‑N‑Gate financing costs; raw material and freight inflation (steel ~$800/ton, aluminum ~$2,300/ton, freight +15% in 2024) and wage inflation (+6.5% YoY) compress margins, driving automation (robotics CAGR ~12%) and hedging/local sourcing to stabilize EBITDA.

| Metric | 2024/2025 |

|---|---|

| Fed funds | 5.25%–5.50% |

| US LV sales | -8% YoY (2024) |

| Steel | $800/ton (2024) |

| Wage growth | +6.5% YoY (2024) |

What You See Is What You Get

Flex-N-Gate PESTLE Analysis

The preview shown here is the exact Flex-N-Gate PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, supply-chain dynamics, and rapid automotive-tech innovation are reshaping Flex‑N‑Gate’s strategy and risk profile; our concise PESTLE highlights the pressures and opportunities driving its next phase. Ideal for investors and strategists, the full analysis delivers actionable insights, forecasts, and ready-to-use slides—purchase now to get the complete, fully editable report instantly.

Political factors

Trade Policy and Tariffs

Shifts in USMCA negotiations and bilateral agreements have raised regional content thresholds to ~70% for certain vehicle classes, increasing Flex-N-Gate sourcing from North America and raising production input costs by an estimated 3–5% in 2025.

Revised rules pushed 18% more steel and 22% more resin procurement to US/Mexico suppliers YTD 2025, altering plant utilization and logistics spend.

Tariff variability on Asian components—ranging 0–10% in 2024–25—continues to drive nearshoring and supplier diversification across Flex-N-Gate’s global footprint.

Government EV Incentives

Federal and state EV manufacturing subsidies—including up to $40,000 EV tax credits and $7.5B from DOE’s 2023 battery materials/EV component programs—directly affect demand for Flex-N-Gate’s specialized EV exterior trim and lighting; higher incentives correlate with increased OEM orders and production volumes. Flex-N-Gate must phase ~$200M–$500M capex over 2024–26 to meet government-mandated transition timelines and keep products relevant for EV platforms. The persistence of incentives through 2026 is critical for locking multi-year contracts with major OEMs and underwriting ROI assumptions in bids.

Labor Union Relations

The political influence of labor unions in North America shapes Flex-N-Gate’s wage structures and operational flexibility, with UAW and USW actions contributing to a 6–8% upward pressure on labor costs industrywide in 2025. Collective bargaining trends through 2025, including several high-profile auto supplier agreements, raised strike-avoidance premiums and highlighted the need for positive labor relations to prevent stoppages that can cost suppliers tens of millions per week. Political pressure to retain manufacturing jobs domestically, reinforced by US Inflation Reduction Act incentives and federal/state job retention pledges, factors into plant expansion and closure decisions, with potential subsidies covering up to 20–30% of capital costs in targeted regions.

Geopolitical Stability

Flex-N-Gate's global footprint exposes it to geopolitical tensions that can disrupt logistics and asset security; for example, 2024 supply-chain delays linked to Black Sea and South China Sea tensions raised shipping premiums by ~18% on affected routes.

Political unrest in supplier regions can spike energy and component costs—energy price shocks in 2024 pushed regional manufacturing input costs up to 12%.

Management must monitor diplomatic shifts and maintain contingency inventories and diversified supplier contracts to mitigate cross-border operational and asset risks.

- Global operations sensitive to regional tensions

- 2024 shipping premiums on contested routes rose ~18%

- Regional input cost spikes up to 12% during unrest

- Requires diplomatic monitoring, diversified suppliers, contingency stock

Regulatory Industrial Policy

Nearshoring surge lifts costs, capex $200–500M; EV incentives drive multi‑year OEM orders

USMCA/content rules and tariffs shifted ~18–22% more procurement to US/Mexico in 2024–25, raising input costs ~3–5% and nearshoring capex needs ($200M–$500M through 2026). EV subsidies and DOE programs (>$7.5B) boosted OEM EV orders, tying incentives persistence to multi-year contracts. Labor actions (UAW/USW) lifted labor costs ~6–8% in 2025; geopolitical tensions raised shipping premiums ~18% and input shocks up to 12%.

| Metric | 2024–25 Impact |

|---|---|

| Revenue (2024) | $3.3B |

| Shifted procurement | +18–22% to US/Mexico |

| Input cost rise | 3–5% |

| Labor cost pressure | 6–8% |

| Shipping premiums (contested routes) | +18% |

| Energy/input shocks | up to 12% |

| Required capex | $200M–$500M (2024–26) |

What is included in the product

Explores how macro-environmental factors uniquely affect Flex-N-Gate across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to surface risks and opportunities for executives and investors.

A concise Flex‑N‑Gate PESTLE summary that’s visually segmented by category, easy to drop into presentations or strategy packs, and editable for regional or business‑line notes to speed team alignment and risk discussions.

Economic factors

Interest Rate Environment

High interest rates through 2025—US Fed funds peak near 5.25%–5.50% in 2023–24 and remaining elevated—have compressed consumer purchasing power, contributing to a roughly 8% YoY decline in US light-vehicle sales in 2024 and lower new-vehicle volumes for suppliers like Flex‑N‑Gate.

For Flex‑N‑Gate, higher borrowing costs raise capital expenditure financing costs; a $100m equipment upgrade at a 6% effective borrowing rate versus 3% raises annual interest expense by about $3m.

The company must balance debt-to-equity to preserve liquidity—benchmarking suppliers with net debt/EBITDA ~2.0–3.0—while funding next‑gen tooling and plant expansions amid tighter credit conditions.

Raw Material Price Volatility

Raw material price volatility—notably plastics, aluminum, and steel—remains a primary determinant of Flex-N-Gate profit margins, with steel spot prices averaging roughly $800/ton in 2024 and aluminum near $2,300/ton, pushing input costs materially higher. Global commodity swings in 2024–2025 increased EBITDA sensitivity, prompting sophisticated hedging and long-term offtake contracts to mitigate sudden price spikes that previously lifted COGS by up to 6–8%. The shift to high-performance polymers for lightweighting, adding 5–12% higher per-unit material cost by end-2025, further complicates procurement and requires blended sourcing and strategic supplier partnerships to preserve margins.

Global Inflationary Pressures

Persistent global inflation raised input and transport costs for the auto sector—freight rates rose ~15% and steel prices averaged up ~12% in 2024—pressuring Flex-N-Gate’s margins as utilities and logistics weigh more on plants; OEMs seeking price concessions complicate passing costs through, so Flex-N-Gate must rely on lean manufacturing and productivity gains (targeting 5–8% cost reduction) to protect EBITDA.

Labor Market Dynamics

A tightening market for skilled manufacturing labor has pushed average hourly wages in U.S. auto manufacturing up about 6.5% year-over-year in 2024, increasing Flex-N-Gate’s engineering and tooling payroll and fixed overhead.

Competition for specialized talent raises recruitment and retention costs; reported median salary for tooling engineers reached roughly $95,000 in 2024, pressuring margins.

Rising labor costs and a 12% CAGR in robotics adoption (2022–2025 estimates) drive Flex-N-Gate toward automation to offset scarce technical labor and long-term wage inflation.

- Wages +6.5% YoY (2024)

- Tooling engineer median ~$95,000 (2024)

- Robotics adoption ~12% CAGR (2022–2025)

Currency Exchange Fluctuations

As a global supplier, Flex-N-Gate faces USD volatility versus MXN and EUR; a 10% USD strengthening vs MXN in 2024 would reduce Mexican plant revenue in dollar terms and could erode price competitiveness in North America.

The company reports a significant share of sales from Mexico and Europe, so FX swings affect reported international earnings and margins; in 2024 FX translation impacted comparable EPS across peers by mid-single digits.

Flex-N-Gate uses strategic hedging and localized sourcing—including MXN procurement and Euro-denominated contracts—to mitigate exposure and stabilize cash flows.

- USD vs MXN: 10% move materially affects dollar revenues

- Translation risk: mid-single-digit EPS impact noted in 2024 peers

- Mitigants: currency hedging, localized sourcing, Euro contracts

Higher rates, squeezed margins: automation & hedging stabilize Flex‑N‑Gate EBITDA

Elevated rates and tighter credit (Fed funds ~5.25%–5.50% through 2025) cut US light‑vehicle volumes ~8% YoY in 2024, raising Flex‑N‑Gate financing costs; raw material and freight inflation (steel ~$800/ton, aluminum ~$2,300/ton, freight +15% in 2024) and wage inflation (+6.5% YoY) compress margins, driving automation (robotics CAGR ~12%) and hedging/local sourcing to stabilize EBITDA.

| Metric | 2024/2025 |

|---|---|

| Fed funds | 5.25%–5.50% |

| US LV sales | -8% YoY (2024) |

| Steel | $800/ton (2024) |

| Wage growth | +6.5% YoY (2024) |

What You See Is What You Get

Flex-N-Gate PESTLE Analysis

The preview shown here is the exact Flex-N-Gate PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.