Flex SWOT Analysis

Your Strategic Toolkit Starts Here

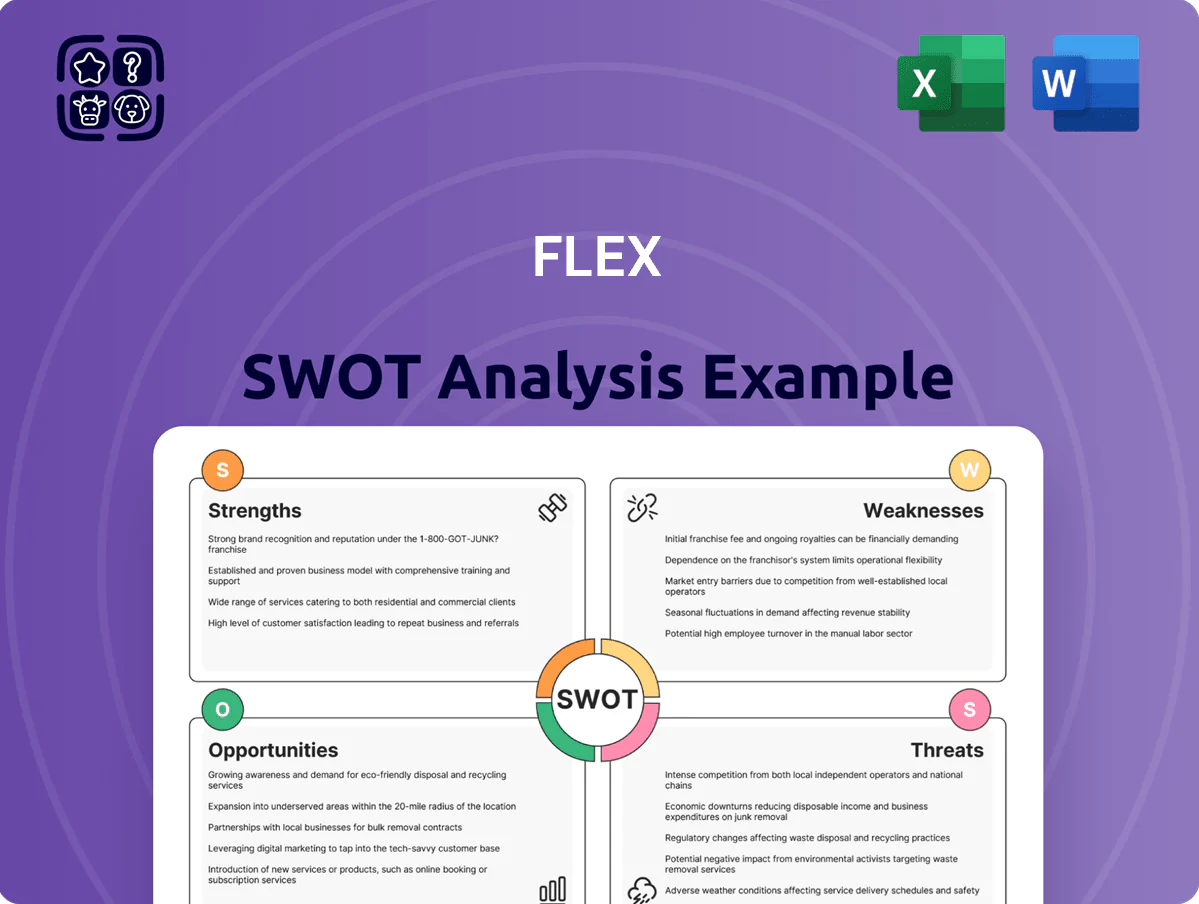

Discover how Flex leverages its diversified hardware and logistics strengths while navigating supply-chain exposure and competitive pressure; purchase the full SWOT analysis for a research-backed, editable report that equips investors and strategists with actionable insights, financial context, and ready-to-use tools to plan, pitch, and invest with confidence.

Strengths

Diversified Multi-Industry Portfolio

Flex Holdings maintains a diversified portfolio across automotive, healthcare, industrial, and cloud-infrastructure sectors, with 2025 revenue mix roughly 28% automotive, 24% healthcare, 22% industrial, and 26% cloud/consumer systems (Flex FY2025 segment report).

This spread cushions Flex from sector-specific cycles, so when consumer-electronics sales fell 14% YoY in H1 2025, overall revenue declined only 3%, preserving operating cash flow near US$1.1bn for the first nine months.

Advanced Global Manufacturing Footprint

Flex operates manufacturing in over 30 countries, with 100+ facilities and 2024 revenue of $26.2B, letting it localize production for global brands and cut landed costs by 10–20% vs purely offshore models.

Geographic reach helps Flex dodge tariffs and use nearshoring; 2023 backlog resilience showed contract wins in auto and healthcare rising 15% year-over-year.

Facilities sit near key end-markets, trimming lead times and improving on-time delivery to >95%, boosting supply-chain resilience for high-value clients.

End-to-End Lifecycle Services

Flex offers end-to-end lifecycle services from design and engineering to distribution and post-market support, driving 2024 services revenue of $5.2B and creating high switching costs for OEMs needing deep technical integration. By capturing margin across stages, Flex raised services gross margin to 11.4% in FY2024 and secured multi-year contracts with blue-chip clients like Cisco and HP, fostering long-term strategic partnerships.

Leadership in Sustainable Manufacturing

Flex’s commitment to circular economy practices and a 30% reduction in Scope 1 and 2 emissions since 2019 has made it a go-to partner for ESG-focused firms.

The company has deployed advanced resource-management and waste-reduction tech across 100+ global sites, cutting material waste by ~18% in 2024.

That sustainability reputation boosts win rates with large enterprises facing stricter environmental rules, supporting higher-margin contract bids.

- 30% cut in Scope 1/2 emissions since 2019

- 18% material-waste reduction (2024)

- 100+ sites with advanced waste/resource tech

Strong Engineering and Technical Expertise

Flex's $25B 2024 revenue supports heavy investment in design and engineering, letting it shift from contract assembly to system integration and win higher-margin projects.

Its teams hold deep skills in power electronics, connectivity, and mechanical systems—areas cited in 2024 client wins—enabling co-developed products and IP-sharing arrangements.

That technical depth drives repeat business and higher ASPs, with engineering services growing faster than COGS in 2022–24.

- 2024 revenue: $25.0B

- Engineering-led wins ↑ since 2022

- Focus: power electronics, connectivity, mechanical systems

Global diversified growth: $25–26B revenue, $5.2B services, $1.1B cash flow, 30% emissions cut

Diversified end-markets (2025 mix: auto 28%, health 24%, industrial 22%, cloud/consumer 26%) and global footprint (100+ sites, >30 countries) sustain ~US$25–26B revenue, ~US$1.1B operating cash flow YTD 2025, >95% on-time delivery, services revenue US$5.2B (2024) and 30% cut in Scope 1/2 since 2019.

| Metric | Value |

|---|---|

| Revenue (2024–25) | $25–26B |

| Services (2024) | $5.2B |

| Op. cash flow (9m 2025) | $1.1B |

| Sites | 100+ |

| Scope 1/2 cut | 30% |

What is included in the product

Provides a concise SWOT framework highlighting Flex’s core strengths, operational weaknesses, market opportunities, and external threats to inform strategic decision-making.

Delivers a compact, editable SWOT matrix that speeds strategic alignment and lets teams update priorities instantly for clear, presentation-ready insights.

Weaknesses

Thin Profit Margin Sensitivity

Operating in contract manufacturing, Flex (Flex Ltd., NASDAQ: FLEX) faces thin operating margins—2024 gross margin 11.2% and operating margin ~4.0%—so a 1% rise in labor or materials can cut operating profit by ~25% of 2024 operating income. Small cost swings hit the core electronics assembly business hard, since higher-margin services now 28% of revenue but assembly still drives volume and remains exposed to pricing pressure from large OEM customers.

High Capital Expenditure Requirements

Maintaining a competitive edge forces Flex (Flex Ltd., NASDAQ: FLEX) to spend heavily on automation, robotics and digital manufacturing—capital expenditures rose to $628 million in FY2024, pressuring free cash flow and liquidity ratios. These outlays increase leverage risk; Flex reported net debt of about $1.1 billion at end-2024, so careful debt management is needed to protect ratings. Ongoing global facility upgrades create a steady drain on cash, reducing flexibility for M&A or dividends.

Concentration of Major Customers

A large share of Flex Ltd’s revenue comes from a few multinationals; in FY2024 the top 10 customers accounted for about 60% of net sales, so losing one major contract could create immediate underutilized capacity and higher fixed-cost per unit. This customer concentration gives big clients strong pricing leverage—Flex reported gross margin pressure in 2024 after renegotiations with two top-tier customers reduced ASPs (average selling prices).

Complexity of Global Supply Chain

Managing Flex Ltd’s (Flex, ticker FLEX) 2025 supplier and logistics web—over 500 manufacturing sites and ~2000 supplier partners across 30+ countries—creates heavy operational complexity and compliance risk, raising SG&A and supply-chain software spend (Flex reported $1.1B in SG&A in FY2024).

Localized shocks—strikes, Taiwan port delays, or a Mexico rail bottleneck—can delay schedules company-wide, increasing working capital and shortening margins; inventory swings rose 12% in 2024 vs 2023.

This complexity demands costly oversight: advanced ERP and WMS systems, control towers, and dedicated teams, driving higher fixed costs and a need for continual capex in systems to avoid inventory imbalances and production downtime.

- 500+ sites, ~2000 suppliers, 30+ countries

- $1.1B SG&A (FY2024)

- Inventory volatility +12% YoY (2024)

- Higher capex for ERP/WMS and control towers

Exposure to Consumer Market Volatility

Despite diversification, about 30% of Flex Ltd’s revenue in FY2024 came from consumer electronics, leaving the firm exposed to rapid shifts in preferences and discretionary spending cuts; global smartphone shipments fell 3% in 2024, which can quickly lower factory utilization.

Short product lifecycles force frequent retooling—CapEx for tooling rose 12% year-over-year in 2024 for the industry—raising costs and reducing margins when volumes drop.

What this estimate hides: regional demand swings can amplify utilization swings inside a single quarter, increasing operating leverage risk.

- ~30% revenue tied to consumer electronics (FY2024)

- Global smartphone shipments −3% in 2024

- Industry tooling CapEx +12% YoY (2024)

Flex Ltd: Thin Margins, High Customer Concentration and Heavy CapEx Risk

Thin margins (2024 gross 11.2%, op ~4.0%) and customer concentration (top10 ≈60% sales) expose Flex Ltd. (FLEX) to pricing pressure and contract loss; heavy capex ($628M FY2024) and net debt ~$1.1B constrain cash; 500+ sites/≈2000 suppliers raise SG&A ($1.1B) and inventory volatility (+12% YoY 2024), with ~30% revenue tied to consumer electronics (smartphones −3% 2024).

| Metric | 2024 |

|---|---|

| Gross margin | 11.2% |

| Op margin | ~4.0% |

| CapEx | $628M |

| Net debt | $1.1B |

| SG&A | $1.1B |

| Inventory vol | +12% YoY |

| Top10 customers | ≈60% |

| Consumer rev | ~30% |

Preview the Actual Deliverable

Flex SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the file shown is the real, downloadable analysis included in your purchase. Once bought, you’ll receive the complete, editable version with full detail and structure. Buy now to unlock the entire report immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Strategic Toolkit Starts Here

Discover how Flex leverages its diversified hardware and logistics strengths while navigating supply-chain exposure and competitive pressure; purchase the full SWOT analysis for a research-backed, editable report that equips investors and strategists with actionable insights, financial context, and ready-to-use tools to plan, pitch, and invest with confidence.

Strengths

Diversified Multi-Industry Portfolio

Flex Holdings maintains a diversified portfolio across automotive, healthcare, industrial, and cloud-infrastructure sectors, with 2025 revenue mix roughly 28% automotive, 24% healthcare, 22% industrial, and 26% cloud/consumer systems (Flex FY2025 segment report).

This spread cushions Flex from sector-specific cycles, so when consumer-electronics sales fell 14% YoY in H1 2025, overall revenue declined only 3%, preserving operating cash flow near US$1.1bn for the first nine months.

Advanced Global Manufacturing Footprint

Flex operates manufacturing in over 30 countries, with 100+ facilities and 2024 revenue of $26.2B, letting it localize production for global brands and cut landed costs by 10–20% vs purely offshore models.

Geographic reach helps Flex dodge tariffs and use nearshoring; 2023 backlog resilience showed contract wins in auto and healthcare rising 15% year-over-year.

Facilities sit near key end-markets, trimming lead times and improving on-time delivery to >95%, boosting supply-chain resilience for high-value clients.

End-to-End Lifecycle Services

Flex offers end-to-end lifecycle services from design and engineering to distribution and post-market support, driving 2024 services revenue of $5.2B and creating high switching costs for OEMs needing deep technical integration. By capturing margin across stages, Flex raised services gross margin to 11.4% in FY2024 and secured multi-year contracts with blue-chip clients like Cisco and HP, fostering long-term strategic partnerships.

Leadership in Sustainable Manufacturing

Flex’s commitment to circular economy practices and a 30% reduction in Scope 1 and 2 emissions since 2019 has made it a go-to partner for ESG-focused firms.

The company has deployed advanced resource-management and waste-reduction tech across 100+ global sites, cutting material waste by ~18% in 2024.

That sustainability reputation boosts win rates with large enterprises facing stricter environmental rules, supporting higher-margin contract bids.

- 30% cut in Scope 1/2 emissions since 2019

- 18% material-waste reduction (2024)

- 100+ sites with advanced waste/resource tech

Strong Engineering and Technical Expertise

Flex's $25B 2024 revenue supports heavy investment in design and engineering, letting it shift from contract assembly to system integration and win higher-margin projects.

Its teams hold deep skills in power electronics, connectivity, and mechanical systems—areas cited in 2024 client wins—enabling co-developed products and IP-sharing arrangements.

That technical depth drives repeat business and higher ASPs, with engineering services growing faster than COGS in 2022–24.

- 2024 revenue: $25.0B

- Engineering-led wins ↑ since 2022

- Focus: power electronics, connectivity, mechanical systems

Global diversified growth: $25–26B revenue, $5.2B services, $1.1B cash flow, 30% emissions cut

Diversified end-markets (2025 mix: auto 28%, health 24%, industrial 22%, cloud/consumer 26%) and global footprint (100+ sites, >30 countries) sustain ~US$25–26B revenue, ~US$1.1B operating cash flow YTD 2025, >95% on-time delivery, services revenue US$5.2B (2024) and 30% cut in Scope 1/2 since 2019.

| Metric | Value |

|---|---|

| Revenue (2024–25) | $25–26B |

| Services (2024) | $5.2B |

| Op. cash flow (9m 2025) | $1.1B |

| Sites | 100+ |

| Scope 1/2 cut | 30% |

What is included in the product

Provides a concise SWOT framework highlighting Flex’s core strengths, operational weaknesses, market opportunities, and external threats to inform strategic decision-making.

Delivers a compact, editable SWOT matrix that speeds strategic alignment and lets teams update priorities instantly for clear, presentation-ready insights.

Weaknesses

Thin Profit Margin Sensitivity

Operating in contract manufacturing, Flex (Flex Ltd., NASDAQ: FLEX) faces thin operating margins—2024 gross margin 11.2% and operating margin ~4.0%—so a 1% rise in labor or materials can cut operating profit by ~25% of 2024 operating income. Small cost swings hit the core electronics assembly business hard, since higher-margin services now 28% of revenue but assembly still drives volume and remains exposed to pricing pressure from large OEM customers.

High Capital Expenditure Requirements

Maintaining a competitive edge forces Flex (Flex Ltd., NASDAQ: FLEX) to spend heavily on automation, robotics and digital manufacturing—capital expenditures rose to $628 million in FY2024, pressuring free cash flow and liquidity ratios. These outlays increase leverage risk; Flex reported net debt of about $1.1 billion at end-2024, so careful debt management is needed to protect ratings. Ongoing global facility upgrades create a steady drain on cash, reducing flexibility for M&A or dividends.

Concentration of Major Customers

A large share of Flex Ltd’s revenue comes from a few multinationals; in FY2024 the top 10 customers accounted for about 60% of net sales, so losing one major contract could create immediate underutilized capacity and higher fixed-cost per unit. This customer concentration gives big clients strong pricing leverage—Flex reported gross margin pressure in 2024 after renegotiations with two top-tier customers reduced ASPs (average selling prices).

Complexity of Global Supply Chain

Managing Flex Ltd’s (Flex, ticker FLEX) 2025 supplier and logistics web—over 500 manufacturing sites and ~2000 supplier partners across 30+ countries—creates heavy operational complexity and compliance risk, raising SG&A and supply-chain software spend (Flex reported $1.1B in SG&A in FY2024).

Localized shocks—strikes, Taiwan port delays, or a Mexico rail bottleneck—can delay schedules company-wide, increasing working capital and shortening margins; inventory swings rose 12% in 2024 vs 2023.

This complexity demands costly oversight: advanced ERP and WMS systems, control towers, and dedicated teams, driving higher fixed costs and a need for continual capex in systems to avoid inventory imbalances and production downtime.

- 500+ sites, ~2000 suppliers, 30+ countries

- $1.1B SG&A (FY2024)

- Inventory volatility +12% YoY (2024)

- Higher capex for ERP/WMS and control towers

Exposure to Consumer Market Volatility

Despite diversification, about 30% of Flex Ltd’s revenue in FY2024 came from consumer electronics, leaving the firm exposed to rapid shifts in preferences and discretionary spending cuts; global smartphone shipments fell 3% in 2024, which can quickly lower factory utilization.

Short product lifecycles force frequent retooling—CapEx for tooling rose 12% year-over-year in 2024 for the industry—raising costs and reducing margins when volumes drop.

What this estimate hides: regional demand swings can amplify utilization swings inside a single quarter, increasing operating leverage risk.

- ~30% revenue tied to consumer electronics (FY2024)

- Global smartphone shipments −3% in 2024

- Industry tooling CapEx +12% YoY (2024)

Flex Ltd: Thin Margins, High Customer Concentration and Heavy CapEx Risk

Thin margins (2024 gross 11.2%, op ~4.0%) and customer concentration (top10 ≈60% sales) expose Flex Ltd. (FLEX) to pricing pressure and contract loss; heavy capex ($628M FY2024) and net debt ~$1.1B constrain cash; 500+ sites/≈2000 suppliers raise SG&A ($1.1B) and inventory volatility (+12% YoY 2024), with ~30% revenue tied to consumer electronics (smartphones −3% 2024).

| Metric | 2024 |

|---|---|

| Gross margin | 11.2% |

| Op margin | ~4.0% |

| CapEx | $628M |

| Net debt | $1.1B |

| SG&A | $1.1B |

| Inventory vol | +12% YoY |

| Top10 customers | ≈60% |

| Consumer rev | ~30% |

Preview the Actual Deliverable

Flex SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the file shown is the real, downloadable analysis included in your purchase. Once bought, you’ll receive the complete, editable version with full detail and structure. Buy now to unlock the entire report immediately after checkout.