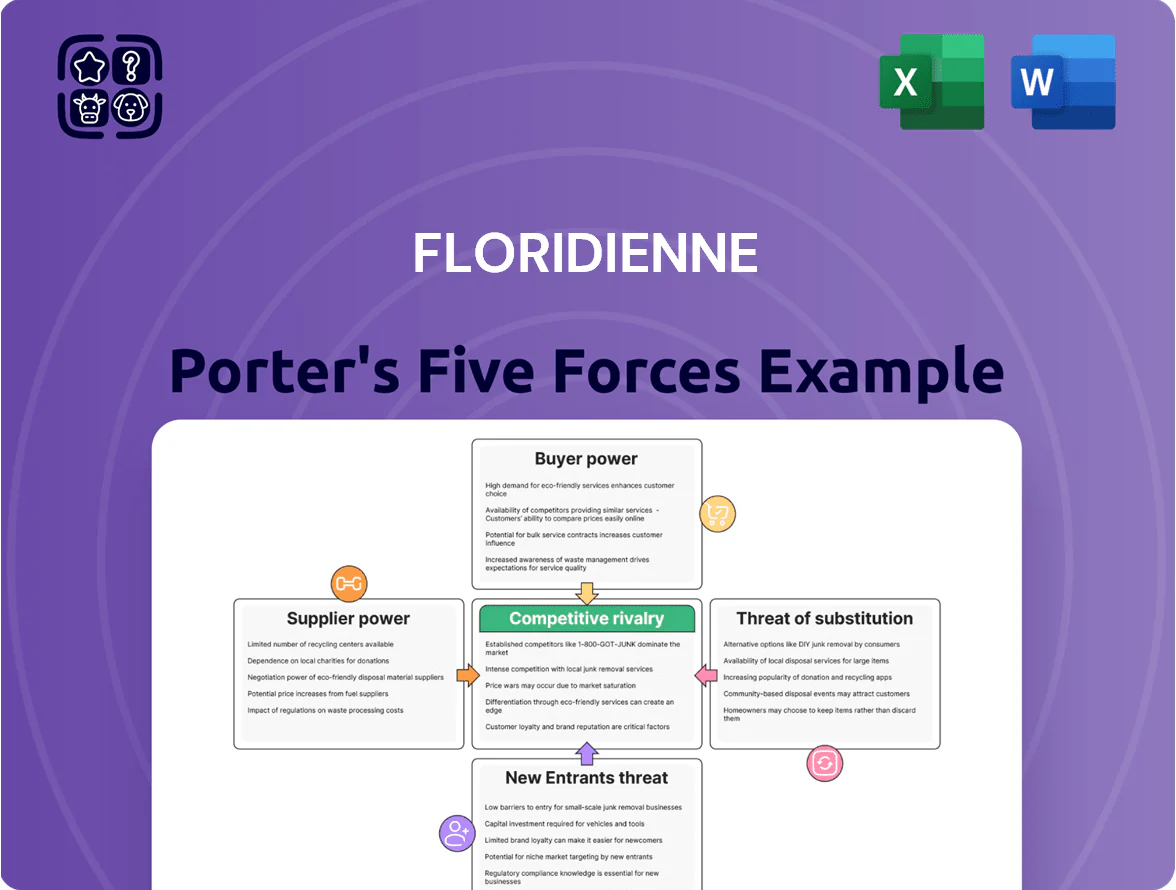

Floridienne Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Floridienne faces moderate supplier influence from specialty input providers and fragmented buyer segments, while regulatory complexity and niche substitutes shape competitive intensity—this snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Floridienne’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Volatility and Availability

Floridienne depends on specific inputs—lead for chemicals and premium seafood for gourmet foods—so raw material price swings materially affect margins; lead prices rose ~28% in 2024–25 and global fishmeal spot prices climbed 12% in 2025, increasing input cost risk. Suppliers gain leverage during scarcity, potentially passing through costs and widening EBITDA volatility. By late 2025 Floridienne reports diversifying suppliers across 6 new geographies, cutting single-vendor exposure from 42% to 18% to curb upstream pricing power.

Specialized Biotech Input Requirements

In Floridienne’s Life Sciences division, demand for highly specific natural extracts and biological components—sourced from a handful of certified vendors—gives suppliers strong leverage; industry reports show single-source suppliers account for ~30–40% of inputs in biocontrol supply chains (2024 data).

Technical certifications (ISO 9001, GMP) and regulatory quality standards raise switching costs and margin pressure, with supplier-driven price volatility of up to 8–12% annually in specialty bio-ingredients.

Maintaining multi-year contracts and joint-development partnerships is essential for Floridienne to secure steady input flows and limit disruption risk to its €120–140m Life Sciences revenue segment (2025 estimate).

Concentration of Metal Suppliers

The supplier market for non-ferrous metals and lead stabilizers is concentrated, with top miners like Glencore and Nyrstar controlling ~45% of refined zinc and lead capacity in 2024, allowing them to set delivery windows and MOQ terms that squeeze margins.

Floridienne offsets this by scaling recycling—recovered metal now supplies about 18% of Specialty Chemicals' input needs in 2025—reducing spot-buy exposure and softening supplier leverage.

Seasonal Agricultural Supply Constraints

Seasonal agricultural and marine harvests raise supplier power for Floridienne in gourmet foods and natural extracts; poor harvest years from climate variability can boost prices for snails, scallops, and niche botanicals by 15–40% (estimated 2023–2025 volatility), squeezing margins.

Floridienne offsets this by pre-buying and using logistics expertise to lock supply, but that ties up millions in working capital—inventory financing rose ~22% in 2024 to support forward contracts.

- Snail/scallop price swings: +15–40% (2023–25)

- Inventory financing increase: ~22% in 2024

- Pre-buying reduces stockouts, raises working capital needs

- Supplier leverage spikes in climate-affected years

Energy and Logistics Cost Pressure

Industrial processing across Floridienne’s three divisions is energy-intensive, so utility providers hold significant leverage over margins; EU industrial power prices averaged ~€180/MWh in 2023 and remained elevated into 2025, pushing procurement toward long-term supply contracts or on-site generation investments.

Rising energy costs prompted Floridienne to pursue PPAs and captive cogeneration to cap fuel expense, while logistics firms retain bargaining power due to specialized transport for hazardous chemicals and perishable foods, where maritime and refrigerated trucking rates rose ~12–18% between 2021–2024.

What this estimate hides: contract mix, fuel hedges, and local grid access cause large divisional variance in supplier power.

- Energy prices ~€180/MWh (EU 2023), high into 2025

- Shift to PPAs and self-generation

- Logistics rates +12–18% (2021–24)

- Specialized transport needed for chemicals, perishables

Suppliers’ rising leverage: input prices, power and volatility squeeze margins

Suppliers hold moderate-to-high power: concentrated metals and certified bio-input vendors can push prices (lead +28% 2024–25; fishmeal +12% 2025), seasonal seafood/botanicals vary +15–40% (2023–25), and EU power ~€180/MWh (2023) raises energy leverage. Floridienne cut single-vendor exposure 42%→18% and recycling supplies 18% of inputs; inventory financing +22% (2024).

| Metric | Value |

|---|---|

| Lead price change | +28% (2024–25) |

| Fishmeal | +12% (2025) |

| Seasonal volatility | +15–40% (2023–25) |

| Single-vendor exposure | 42%→18% (2025) |

| Recycled metal | 18% of inputs (2025) |

| Inventory financing | +22% (2024) |

| EU power | ~€180/MWh (2023) |

What is included in the product

Concise Porter's Five Forces analysis tailored to Floridienne, highlighting competitive rivalry, buyer and supplier power, threat of substitutes, and entry barriers to reveal strategic pressures on margins and growth.

Quick, one-sheet Floridienne Porter's Five Forces—instantly highlights competitive pressures and strategic levers to guide fast, data-driven decisions.

Customers Bargaining Power

Retail Consolidation in Gourmet Food

Large European retailers (e.g., Carrefour, Tesco, Schwarz Group) exert strong price and service pressure on Floridienne’s gourmet food arm; top 10 EU retailers controlled ~64% of grocery sales in 2024, so buyers can demand lower margins.

These chains can switch to private labels—EU private-label share hit 42% in 2024—raising churn risk if Floridienne loses niche quality.

Floridienne counters with premium branding and unique SKUs; in 2024 its gourmet segment grew ~7% vs. 2% market average, showing consumer willingness to pay for distinct products.

Industrial Client Technical Requirements

Industrial clients in chemicals and plastics set strict technical specs, especially for stabilizers and specialty packaging; failure to meet specs risks contract loss, so Floridienne earns dependency-driven pricing power. Still, top 20 global buyers—often >50% volume per account—use volume leverage to push ASPs down; in 2024 average negotiated discounts reached ~6–9% on large contracts. This mix keeps customer bargaining power balanced.

Switching Costs in Life Sciences

Switching costs in Floridienne’s life sciences are moderate: regulatory approvals and formulation ties mean switching a biocontrol can take 6–18 months and cost an estimated €50k–€200k per SKU in validation and compliance, so 62% of surveyed growers (2024 EU agri-study) keep suppliers for 2+ years.

Price Sensitivity in Commodity Chemicals

Floridienne faces high price sensitivity in commodity chemicals: some recycled-stabilizer lines compete with lower-cost virgin alternatives, and buyers will switch if price gaps exceed ~10–15% per industry studies (2024 EU chemicals pricing report).

To retain volume, Floridienne stresses higher purity and 30–50% lower lifecycle CO2 for its recycled materials (company disclosures 2025), justifying modest premiums and reducing churn.

- High price sensitivity: ~10–15% switch threshold

- Value prop: 30–50% lower lifecycle CO2

- Strategy: premium via purity and ESG claims

Demand for Sustainable Solutions

By end-2025 buyers across Floridienne’s divisions demand ESG compliance, pushing requests for product-level carbon footprints; surveys show 62% of industrial buyers cite sustainability as a purchase filter.

That buyer power forces transparency and pricing pressure; customers are willing to pay 3–7% premium for certified low-carbon inputs but switch suppliers if data is missing.

Floridienne accelerated green chemistry projects, allocating €18.5m in 2024–25 R&D to cut scope-3 emissions and retain market share.

- 62% of buyers prioritize sustainability

- 3–7% willing-to-pay premium for low-carbon

- €18.5m R&D 2024–25 for green chemistry

Buyers wield power: grocers & private-label squeeze prices; sustainability lifts 3–7% premium

Buyers hold balanced-to-strong power: grocery chains (top 10 = ~64% EU grocery sales, 2024) press prices, private-label share 42% (2024) threatens churn, while Floridienne’s gourmet grew ~7% in 2024 showing premium pull; industrial buyers push 6–9% negotiated discounts on large contracts (2024) but technical specs and 6–18 month switching (€50k–€200k) retain some pricing power; 62% of buyers prioritize sustainability, 3–7% WTP premium.

| Metric | Value |

|---|---|

| Top-10 EU grocery share (2024) | ~64% |

| EU private-label share (2024) | 42% |

| Floridienne gourmet growth (2024) | ~7% |

| Large-contract discounts (2024) | 6–9% |

| Switch time/cost | 6–18 months; €50k–€200k |

| Buyers prioritizing sustainability | 62% |

| Willing-to-pay premium | 3–7% |

Same Document Delivered

Floridienne Porter's Five Forces Analysis

This preview shows the exact Floridienne Porter’s Five Forces analysis you’ll receive immediately after purchase—fully formatted, complete, and ready for download with no placeholders or samples.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Floridienne faces moderate supplier influence from specialty input providers and fragmented buyer segments, while regulatory complexity and niche substitutes shape competitive intensity—this snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Floridienne’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Volatility and Availability

Floridienne depends on specific inputs—lead for chemicals and premium seafood for gourmet foods—so raw material price swings materially affect margins; lead prices rose ~28% in 2024–25 and global fishmeal spot prices climbed 12% in 2025, increasing input cost risk. Suppliers gain leverage during scarcity, potentially passing through costs and widening EBITDA volatility. By late 2025 Floridienne reports diversifying suppliers across 6 new geographies, cutting single-vendor exposure from 42% to 18% to curb upstream pricing power.

Specialized Biotech Input Requirements

In Floridienne’s Life Sciences division, demand for highly specific natural extracts and biological components—sourced from a handful of certified vendors—gives suppliers strong leverage; industry reports show single-source suppliers account for ~30–40% of inputs in biocontrol supply chains (2024 data).

Technical certifications (ISO 9001, GMP) and regulatory quality standards raise switching costs and margin pressure, with supplier-driven price volatility of up to 8–12% annually in specialty bio-ingredients.

Maintaining multi-year contracts and joint-development partnerships is essential for Floridienne to secure steady input flows and limit disruption risk to its €120–140m Life Sciences revenue segment (2025 estimate).

Concentration of Metal Suppliers

The supplier market for non-ferrous metals and lead stabilizers is concentrated, with top miners like Glencore and Nyrstar controlling ~45% of refined zinc and lead capacity in 2024, allowing them to set delivery windows and MOQ terms that squeeze margins.

Floridienne offsets this by scaling recycling—recovered metal now supplies about 18% of Specialty Chemicals' input needs in 2025—reducing spot-buy exposure and softening supplier leverage.

Seasonal Agricultural Supply Constraints

Seasonal agricultural and marine harvests raise supplier power for Floridienne in gourmet foods and natural extracts; poor harvest years from climate variability can boost prices for snails, scallops, and niche botanicals by 15–40% (estimated 2023–2025 volatility), squeezing margins.

Floridienne offsets this by pre-buying and using logistics expertise to lock supply, but that ties up millions in working capital—inventory financing rose ~22% in 2024 to support forward contracts.

- Snail/scallop price swings: +15–40% (2023–25)

- Inventory financing increase: ~22% in 2024

- Pre-buying reduces stockouts, raises working capital needs

- Supplier leverage spikes in climate-affected years

Energy and Logistics Cost Pressure

Industrial processing across Floridienne’s three divisions is energy-intensive, so utility providers hold significant leverage over margins; EU industrial power prices averaged ~€180/MWh in 2023 and remained elevated into 2025, pushing procurement toward long-term supply contracts or on-site generation investments.

Rising energy costs prompted Floridienne to pursue PPAs and captive cogeneration to cap fuel expense, while logistics firms retain bargaining power due to specialized transport for hazardous chemicals and perishable foods, where maritime and refrigerated trucking rates rose ~12–18% between 2021–2024.

What this estimate hides: contract mix, fuel hedges, and local grid access cause large divisional variance in supplier power.

- Energy prices ~€180/MWh (EU 2023), high into 2025

- Shift to PPAs and self-generation

- Logistics rates +12–18% (2021–24)

- Specialized transport needed for chemicals, perishables

Suppliers’ rising leverage: input prices, power and volatility squeeze margins

Suppliers hold moderate-to-high power: concentrated metals and certified bio-input vendors can push prices (lead +28% 2024–25; fishmeal +12% 2025), seasonal seafood/botanicals vary +15–40% (2023–25), and EU power ~€180/MWh (2023) raises energy leverage. Floridienne cut single-vendor exposure 42%→18% and recycling supplies 18% of inputs; inventory financing +22% (2024).

| Metric | Value |

|---|---|

| Lead price change | +28% (2024–25) |

| Fishmeal | +12% (2025) |

| Seasonal volatility | +15–40% (2023–25) |

| Single-vendor exposure | 42%→18% (2025) |

| Recycled metal | 18% of inputs (2025) |

| Inventory financing | +22% (2024) |

| EU power | ~€180/MWh (2023) |

What is included in the product

Concise Porter's Five Forces analysis tailored to Floridienne, highlighting competitive rivalry, buyer and supplier power, threat of substitutes, and entry barriers to reveal strategic pressures on margins and growth.

Quick, one-sheet Floridienne Porter's Five Forces—instantly highlights competitive pressures and strategic levers to guide fast, data-driven decisions.

Customers Bargaining Power

Retail Consolidation in Gourmet Food

Large European retailers (e.g., Carrefour, Tesco, Schwarz Group) exert strong price and service pressure on Floridienne’s gourmet food arm; top 10 EU retailers controlled ~64% of grocery sales in 2024, so buyers can demand lower margins.

These chains can switch to private labels—EU private-label share hit 42% in 2024—raising churn risk if Floridienne loses niche quality.

Floridienne counters with premium branding and unique SKUs; in 2024 its gourmet segment grew ~7% vs. 2% market average, showing consumer willingness to pay for distinct products.

Industrial Client Technical Requirements

Industrial clients in chemicals and plastics set strict technical specs, especially for stabilizers and specialty packaging; failure to meet specs risks contract loss, so Floridienne earns dependency-driven pricing power. Still, top 20 global buyers—often >50% volume per account—use volume leverage to push ASPs down; in 2024 average negotiated discounts reached ~6–9% on large contracts. This mix keeps customer bargaining power balanced.

Switching Costs in Life Sciences

Switching costs in Floridienne’s life sciences are moderate: regulatory approvals and formulation ties mean switching a biocontrol can take 6–18 months and cost an estimated €50k–€200k per SKU in validation and compliance, so 62% of surveyed growers (2024 EU agri-study) keep suppliers for 2+ years.

Price Sensitivity in Commodity Chemicals

Floridienne faces high price sensitivity in commodity chemicals: some recycled-stabilizer lines compete with lower-cost virgin alternatives, and buyers will switch if price gaps exceed ~10–15% per industry studies (2024 EU chemicals pricing report).

To retain volume, Floridienne stresses higher purity and 30–50% lower lifecycle CO2 for its recycled materials (company disclosures 2025), justifying modest premiums and reducing churn.

- High price sensitivity: ~10–15% switch threshold

- Value prop: 30–50% lower lifecycle CO2

- Strategy: premium via purity and ESG claims

Demand for Sustainable Solutions

By end-2025 buyers across Floridienne’s divisions demand ESG compliance, pushing requests for product-level carbon footprints; surveys show 62% of industrial buyers cite sustainability as a purchase filter.

That buyer power forces transparency and pricing pressure; customers are willing to pay 3–7% premium for certified low-carbon inputs but switch suppliers if data is missing.

Floridienne accelerated green chemistry projects, allocating €18.5m in 2024–25 R&D to cut scope-3 emissions and retain market share.

- 62% of buyers prioritize sustainability

- 3–7% willing-to-pay premium for low-carbon

- €18.5m R&D 2024–25 for green chemistry

Buyers wield power: grocers & private-label squeeze prices; sustainability lifts 3–7% premium

Buyers hold balanced-to-strong power: grocery chains (top 10 = ~64% EU grocery sales, 2024) press prices, private-label share 42% (2024) threatens churn, while Floridienne’s gourmet grew ~7% in 2024 showing premium pull; industrial buyers push 6–9% negotiated discounts on large contracts (2024) but technical specs and 6–18 month switching (€50k–€200k) retain some pricing power; 62% of buyers prioritize sustainability, 3–7% WTP premium.

| Metric | Value |

|---|---|

| Top-10 EU grocery share (2024) | ~64% |

| EU private-label share (2024) | 42% |

| Floridienne gourmet growth (2024) | ~7% |

| Large-contract discounts (2024) | 6–9% |

| Switch time/cost | 6–18 months; €50k–€200k |

| Buyers prioritizing sustainability | 62% |

| Willing-to-pay premium | 3–7% |

Same Document Delivered

Floridienne Porter's Five Forces Analysis

This preview shows the exact Floridienne Porter’s Five Forces analysis you’ll receive immediately after purchase—fully formatted, complete, and ready for download with no placeholders or samples.