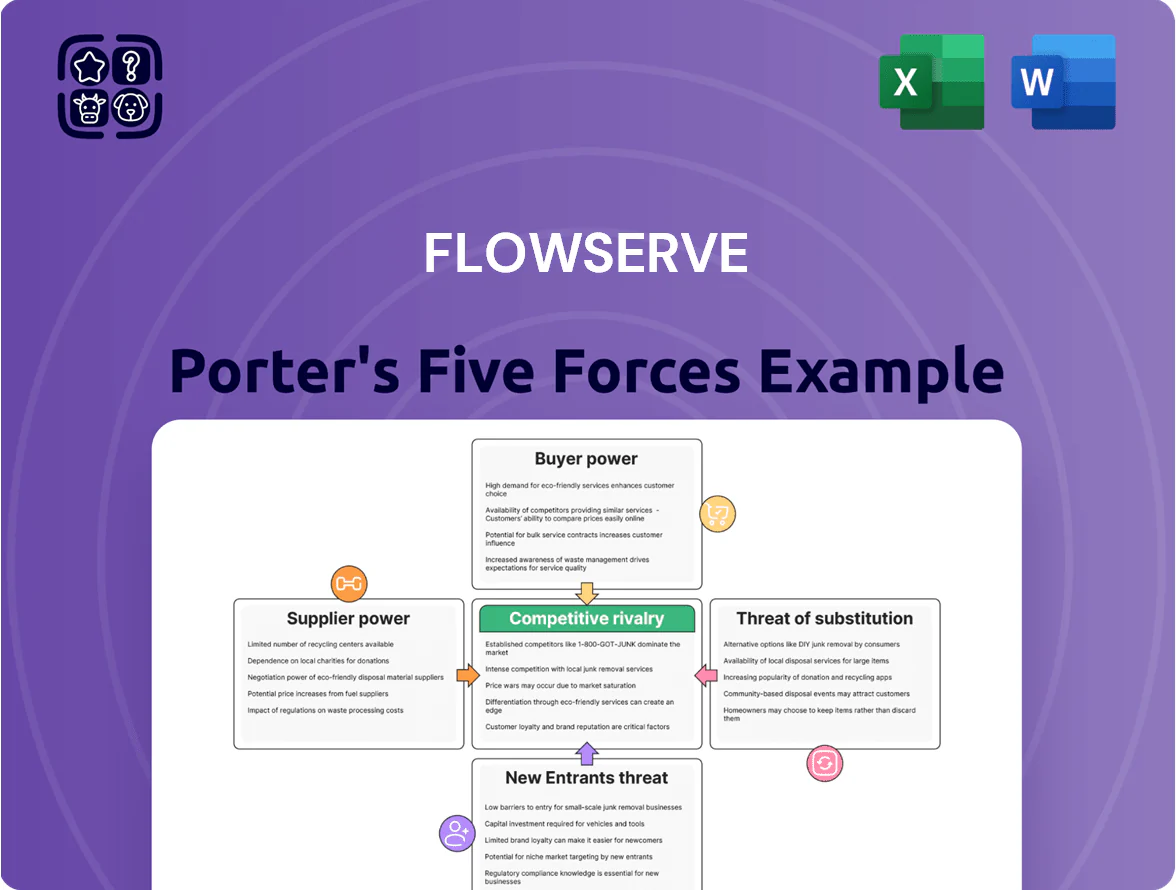

Flowserve Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Flowserve operates in a capital-intensive, technology-driven market where supplier leverage and aftermarket services shape margins, while moderate buyer power and high barriers curb new entrants; competitive rivalry hinges on innovation and scale.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Flowserve’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Price Volatility

Flowserve depends on specialized alloys—stainless steel and nickel—for high-performance pumps and valves; supplier leverage rose in late 2025 as nickel spot prices averaged about $28,000 per tonne (+22% YoY) and stainless premiums climbed 15%, boosting input costs.

The company uses long-term sourcing contracts and customer price escalation clauses; these measures cut raw-material cost volatility exposure by an estimated 40% vs. spot purchases, but moderate supplier power remains.

Specialized Component Dependency

The production of advanced flow-control systems needs specialized electronic components and seals often supplied by a handful of high-tech firms; in 2024, suppliers of precision seals accounted for an estimated 60% of critical-part shipments to top OEMs, raising supplier bargaining power. Flowserve mitigates this by diversifying suppliers across regions—Europe, North America, and APAC—cutting single-source exposure to under 25% of global assembly inputs.

Energy and Logistics Costs

Suppliers of logistics and energy have tightened leverage as global energy policy shifts raised fuel and power costs; Brent crude rose ~15% in 2024 and US industrial electricity prices jumped 6% year-on-year, squeezing margins if carriers pass costs to Flowserve.

Flowserve’s $3.7bn 2024 revenue scale gives negotiation leverage—bulk freight contracts and regional hubs lowered transport per-unit by an estimated 4%—but volatile fuel and electricity prices remain a recurring supplier pressure.

Supplier Consolidation Trends

Supplier consolidation has cut global foundry and forging suppliers by roughly 25% from 2015–2024, concentrating capacity in firms with >$500m revenue and boosting their pricing leverage.

These large suppliers now extract better payment terms and longer lead times, increasing supplier bargaining power versus buyers like Flowserve.

Flowserve needs strategic, often multi-year contracts and NPI (new product introduction) collaboration to secure quality inputs and mitigate single-supplier risk.

Labor Market Constraints

Suppliers of skilled engineering and technical services face a tight labor market in 2025, with US engineering wage growth around 4.2% year-over-year, pushing up outsourced technical labor costs for Flowserve.

Because Flowserve needs precision-engineered components, wage inflation at its specialized tier-one and tier-two suppliers increases procurement costs, forcing margin pressure.

That indirect labor pressure compels Flowserve to chase internal manufacturing efficiencies—automation, yield improvements, and vertical integration—to offset rising supplier wages.

- 2025 engineering wage growth ~4.2% YoY

- Tier supplier wage pass-through raises COGS

- Company focuses on automation, yield, vertical integration

Flowserve Navigates Supplier Power: Scale & Contracts Mitigate Nickel, Wage Pressures

Suppliers hold moderate-to-high power: specialty metals (nickel ~$28,000/t in 2025) and precision seals concentrate supply; Flowserve’s $3.7bn 2024 scale, multi-year contracts and 40% reduced spot exposure cut volatility, but supplier consolidation (-25% suppliers 2015–2024) and 4.2% engineering wage growth keep pressure on margins.

| Metric | Value |

|---|---|

| 2024 Revenue | $3.7bn |

| Ni price (2025 avg) | $28,000/t |

| Supplier count change (2015–24) | -25% |

| Engineering wage growth (2025) | 4.2% YoY |

| Estimated spot exposure cut | 40% |

What is included in the product

Tailored exclusively for Flowserve, this Porter's Five Forces overview uncovers key competitive drivers, supplier and buyer power, entry barriers, substitute threats, and strategic pressures shaping the company’s pricing and profitability.

A concise Porter's Five Forces snapshot for Flowserve—instantly flags supplier, buyer, and competitive pressures so you can prioritize strategic moves and reduce decision friction.

Customers Bargaining Power

Concentration of Major Industrial Clients

Flowserve serves massive oil & gas, chemical, and power clients—ExxonMobil, Shell, and Aramco-scale buyers—whose combined capex orders can exceed $1bn per project, giving them strong purchase leverage. These sophisticated buyers use competitive bidding and supplier rationalization; industry data show procurement-led price reductions of 5–15% on major EPC contracts. Flowserve counters by selling integrated pump-valve-actuator systems and aftermarket services, which in 2024 made up ~45% of revenue and raise switching costs. This solution focus shifts competition from price to total lifecycle value, limiting pure price-based selection.

High Switching Costs for Installed Base

Once a Flowserve pump or valve is integrated into a refinery or power plant, switching costs—engineering requalification, downtime, commissioning—can exceed 10–20% of a project’s CAPEX, effectively locking customers in and reducing their bargaining power over time.

This installed base generated roughly 45% of Flowserve’s 2024 revenue through aftermarket parts and services, a higher-margin, recurring stream that boosts long-term operating margins.

Customers exert pressure at initial procurement, but over a 20–30 year equipment life Flowserve captures pricing leverage and service revenue, lowering customer power and stabilizing cash flow.

Demand for Sustainable and Digital Solutions

By end-2025 buyers demand lower-carbon equipment and IoT monitoring; surveys show 62% of industrial buyers prioritize emissions data and 58% require remote monitoring capabilities, shifting negotiation power to customers.

Customers now ask for specific emissions metrics as contract gates, pressuring suppliers on price and specs; Flowserve reports its 2024 D, D & D (Diversify, Decarbonize, Digitize) investments rose to $120M to meet these terms.

Price Sensitivity in Commodity Markets

In water management and basic chemical processing, Flowserve faces high customer price sensitivity as clients treat valves and seals as commodities; switching to lower-cost regional suppliers is common if Flowserve’s tech edge isn’t proven.

Flowserve stresses total cost of ownership—maintenance, downtime reduction, and 10–20% longer service life in some products—to justify a premium; in 2024 aftermarket sales were ~43% of revenue, supporting this strategy.

Access to Alternative Global Vendors

Rising high-quality manufacturers in China and India cut costs by 20–40% on standard pumps, giving buyers leverage to push prices down against Flowserve.

Flowserve defends margins by stressing a 280+ service centers global network and 24–72 hour response in key markets, which regional rivals rarely match.

- Buyers' leverage: + options, price pressure 20–40%

- Flowserve's edge: 280+ service centers, 24–72h response

- Net effect: stronger negotiation, but premium for service retention

Flowserve’s service moat cuts buyer power: 45% aftermarket, 280+ centers, IoT/emissions pull

Customers have strong initial leverage—procurement cuts 5–15% and regional rivals undercut 20–40%—but Flowserve’s 43–45% aftermarket revenue, 280+ service centers, 24–72h response, and 10–20% longer asset life raise switching costs over 20–30 years, reducing customer power. Emissions/IoT demands (62%/58% buyers) shift specs and capex to suppliers.

| Metric | Value (2024–25) |

|---|---|

| Aftermarket rev | 43–45% |

| Service centers | 280+ |

| Procurement price cuts | 5–15% |

| Regional undercut | 20–40% |

| Buyers demand: emissions | 62% |

| Buyers demand: IoT | 58% |

Full Version Awaits

Flowserve Porter's Five Forces Analysis

This preview shows the exact Flowserve Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders and fully formatted for download.

The document displayed here is the actual deliverable, ready for instant access and use the moment you complete your purchase.

No mockups or samples: what you see is the complete, professionally written analysis file, prepared for your strategic or investment needs.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Flowserve operates in a capital-intensive, technology-driven market where supplier leverage and aftermarket services shape margins, while moderate buyer power and high barriers curb new entrants; competitive rivalry hinges on innovation and scale.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Flowserve’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Price Volatility

Flowserve depends on specialized alloys—stainless steel and nickel—for high-performance pumps and valves; supplier leverage rose in late 2025 as nickel spot prices averaged about $28,000 per tonne (+22% YoY) and stainless premiums climbed 15%, boosting input costs.

The company uses long-term sourcing contracts and customer price escalation clauses; these measures cut raw-material cost volatility exposure by an estimated 40% vs. spot purchases, but moderate supplier power remains.

Specialized Component Dependency

The production of advanced flow-control systems needs specialized electronic components and seals often supplied by a handful of high-tech firms; in 2024, suppliers of precision seals accounted for an estimated 60% of critical-part shipments to top OEMs, raising supplier bargaining power. Flowserve mitigates this by diversifying suppliers across regions—Europe, North America, and APAC—cutting single-source exposure to under 25% of global assembly inputs.

Energy and Logistics Costs

Suppliers of logistics and energy have tightened leverage as global energy policy shifts raised fuel and power costs; Brent crude rose ~15% in 2024 and US industrial electricity prices jumped 6% year-on-year, squeezing margins if carriers pass costs to Flowserve.

Flowserve’s $3.7bn 2024 revenue scale gives negotiation leverage—bulk freight contracts and regional hubs lowered transport per-unit by an estimated 4%—but volatile fuel and electricity prices remain a recurring supplier pressure.

Supplier Consolidation Trends

Supplier consolidation has cut global foundry and forging suppliers by roughly 25% from 2015–2024, concentrating capacity in firms with >$500m revenue and boosting their pricing leverage.

These large suppliers now extract better payment terms and longer lead times, increasing supplier bargaining power versus buyers like Flowserve.

Flowserve needs strategic, often multi-year contracts and NPI (new product introduction) collaboration to secure quality inputs and mitigate single-supplier risk.

Labor Market Constraints

Suppliers of skilled engineering and technical services face a tight labor market in 2025, with US engineering wage growth around 4.2% year-over-year, pushing up outsourced technical labor costs for Flowserve.

Because Flowserve needs precision-engineered components, wage inflation at its specialized tier-one and tier-two suppliers increases procurement costs, forcing margin pressure.

That indirect labor pressure compels Flowserve to chase internal manufacturing efficiencies—automation, yield improvements, and vertical integration—to offset rising supplier wages.

- 2025 engineering wage growth ~4.2% YoY

- Tier supplier wage pass-through raises COGS

- Company focuses on automation, yield, vertical integration

Flowserve Navigates Supplier Power: Scale & Contracts Mitigate Nickel, Wage Pressures

Suppliers hold moderate-to-high power: specialty metals (nickel ~$28,000/t in 2025) and precision seals concentrate supply; Flowserve’s $3.7bn 2024 scale, multi-year contracts and 40% reduced spot exposure cut volatility, but supplier consolidation (-25% suppliers 2015–2024) and 4.2% engineering wage growth keep pressure on margins.

| Metric | Value |

|---|---|

| 2024 Revenue | $3.7bn |

| Ni price (2025 avg) | $28,000/t |

| Supplier count change (2015–24) | -25% |

| Engineering wage growth (2025) | 4.2% YoY |

| Estimated spot exposure cut | 40% |

What is included in the product

Tailored exclusively for Flowserve, this Porter's Five Forces overview uncovers key competitive drivers, supplier and buyer power, entry barriers, substitute threats, and strategic pressures shaping the company’s pricing and profitability.

A concise Porter's Five Forces snapshot for Flowserve—instantly flags supplier, buyer, and competitive pressures so you can prioritize strategic moves and reduce decision friction.

Customers Bargaining Power

Concentration of Major Industrial Clients

Flowserve serves massive oil & gas, chemical, and power clients—ExxonMobil, Shell, and Aramco-scale buyers—whose combined capex orders can exceed $1bn per project, giving them strong purchase leverage. These sophisticated buyers use competitive bidding and supplier rationalization; industry data show procurement-led price reductions of 5–15% on major EPC contracts. Flowserve counters by selling integrated pump-valve-actuator systems and aftermarket services, which in 2024 made up ~45% of revenue and raise switching costs. This solution focus shifts competition from price to total lifecycle value, limiting pure price-based selection.

High Switching Costs for Installed Base

Once a Flowserve pump or valve is integrated into a refinery or power plant, switching costs—engineering requalification, downtime, commissioning—can exceed 10–20% of a project’s CAPEX, effectively locking customers in and reducing their bargaining power over time.

This installed base generated roughly 45% of Flowserve’s 2024 revenue through aftermarket parts and services, a higher-margin, recurring stream that boosts long-term operating margins.

Customers exert pressure at initial procurement, but over a 20–30 year equipment life Flowserve captures pricing leverage and service revenue, lowering customer power and stabilizing cash flow.

Demand for Sustainable and Digital Solutions

By end-2025 buyers demand lower-carbon equipment and IoT monitoring; surveys show 62% of industrial buyers prioritize emissions data and 58% require remote monitoring capabilities, shifting negotiation power to customers.

Customers now ask for specific emissions metrics as contract gates, pressuring suppliers on price and specs; Flowserve reports its 2024 D, D & D (Diversify, Decarbonize, Digitize) investments rose to $120M to meet these terms.

Price Sensitivity in Commodity Markets

In water management and basic chemical processing, Flowserve faces high customer price sensitivity as clients treat valves and seals as commodities; switching to lower-cost regional suppliers is common if Flowserve’s tech edge isn’t proven.

Flowserve stresses total cost of ownership—maintenance, downtime reduction, and 10–20% longer service life in some products—to justify a premium; in 2024 aftermarket sales were ~43% of revenue, supporting this strategy.

Access to Alternative Global Vendors

Rising high-quality manufacturers in China and India cut costs by 20–40% on standard pumps, giving buyers leverage to push prices down against Flowserve.

Flowserve defends margins by stressing a 280+ service centers global network and 24–72 hour response in key markets, which regional rivals rarely match.

- Buyers' leverage: + options, price pressure 20–40%

- Flowserve's edge: 280+ service centers, 24–72h response

- Net effect: stronger negotiation, but premium for service retention

Flowserve’s service moat cuts buyer power: 45% aftermarket, 280+ centers, IoT/emissions pull

Customers have strong initial leverage—procurement cuts 5–15% and regional rivals undercut 20–40%—but Flowserve’s 43–45% aftermarket revenue, 280+ service centers, 24–72h response, and 10–20% longer asset life raise switching costs over 20–30 years, reducing customer power. Emissions/IoT demands (62%/58% buyers) shift specs and capex to suppliers.

| Metric | Value (2024–25) |

|---|---|

| Aftermarket rev | 43–45% |

| Service centers | 280+ |

| Procurement price cuts | 5–15% |

| Regional undercut | 20–40% |

| Buyers demand: emissions | 62% |

| Buyers demand: IoT | 58% |

Full Version Awaits

Flowserve Porter's Five Forces Analysis

This preview shows the exact Flowserve Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders and fully formatted for download.

The document displayed here is the actual deliverable, ready for instant access and use the moment you complete your purchase.

No mockups or samples: what you see is the complete, professionally written analysis file, prepared for your strategic or investment needs.