Flowserve PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and rapid tech advances are shaping Flowserve’s strategic outlook—our concise PESTLE snapshot highlights key external risks and opportunities so you can act with confidence. Purchase the full PESTLE analysis to access detailed, ready-to-use insights and forecasts tailored for investors, consultants, and strategists.

Political factors

Geopolitical instability in energy producing regions

Ongoing conflicts and diplomatic tensions in the Middle East and Eastern Europe continue to influence global energy security as of late 2025, with IEA reporting 2024–25 oil supply disruptions averaging 1.2 million bpd; Flowserve faces demand volatility for pumps and valves tied to these swings.

Shifting alliances affect delivery to major oil and gas projects—project deferrals in 2024 cut upstream capex by about 6% globally, forcing Flowserve to reallocate inventory and redirect sales channels.

Political volatility triggers sudden export license changes and sanctions—US and EU measures in 2024–25 impacted over $8 billion in energy equipment trade—requiring Flowserve agile supply chain, compliance spend increases, and contingency sourcing.

Trade protectionism and tariff policies

The resurgence of protectionism in 2024–2025, including US steel tariffs and EU safeguard measures, raised input costs for flow-control makers; US Section 232 and EU measures contributed to steel price rises of roughly 15–30% YoY, increasing Flowserve unit production costs materially. Tariffs on specialized components added effective cost uplifts estimated at 3–7% for some pump lines. Flowserve has accelerated localized manufacturing, expanding regional hubs—capex of $120m in 2024—to reduce tariff exposure and shorten supply chains.

Government subsidies for energy transition

Legislative frameworks like the US Inflation Reduction Act (up to $369bn clean energy tax credits through 2031) and the EU Green Deal (€300bn annual low-carbon investment target) materially boost demand for Flowserve pumps in carbon capture, hydrogen and CSP projects; Flowserve reported 2024 renewable orders growth of ~18% year-over-year.

Infrastructure investment programs

Large-scale government spending—US Bipartisan Infrastructure Law $1.2T (2021) with $55B for water, EU’s €300B green deal allocations—continues to drive demand for Flowserve pumps and valves as utilities modernize grids and treatment plants.

Political mandates tackling water scarcity in India, Sub-Saharan Africa and MENA (over 2B people lacking safely managed drinking water per 2022 WHO) create new markets for flow management solutions.

Flowserve tracks national budget allocations and public works procurement pipelines to prioritize sales engagement with funded projects, aligning supply chain and production capacity to capture funded contracts.

- Key drivers: $55B US water funds, €300B EU green allocations

- Opportunity: >2B people without safe water (WHO 2022)

- Strategy: align sales to national budgeted projects

Regulatory shifts in emerging markets

Political transitions in emerging economies often trigger rapid changes in industrial standards and localization rules; Flowserve faced such risks in 2023 when localization mandates in India and Brazil raised component sourcing requirements by up to 30%, impacting supply-chain costs.

Maintaining strong government relations is critical: Flowserve reported ~15% revenue exposure to high-growth emerging markets in 2024, requiring proactive compliance with made‑in‑country mandates to retain contracts.

Failure to adapt can cede market share to domestic firms—local competitors captured an estimated 10–20% share in targeted segments in recent mandate-driven procurement cycles.

- Localization mandates ↑ supply costs ~30% in some markets (2023)

- ~15% of Flowserve revenue exposed to emerging markets (2024)

- Local firms gained 10–20% share where mandates enforced

Geopolitics, tariffs drive costs; renewables lift Flowserve—18% orders, 15% EM risk

Geopolitical conflicts and sanctions (2024–25) caused ~1.2mbd oil disruptions, driving demand volatility; protectionist tariffs lifted steel costs 15–30% and added 3–7% component cost, prompting $120m regional capex (2024). Clean-energy policies (IRA, EU Green Deal) and infrastructure funds ($55B US water, €300B EU) boosted Flowserve renewable orders +18% (2024); ~15% revenue exposed to emerging markets with localization risks.

| Metric | Value |

|---|---|

| Oil supply disruption | 1.2 mbd (2024–25) |

| Steel cost rise | 15–30% YoY (2024) |

| Component tariff impact | 3–7% |

| Regional capex | $120m (2024) |

| Renewable orders growth | +18% (2024) |

| Revenue EM exposure | ~15% (2024) |

What is included in the product

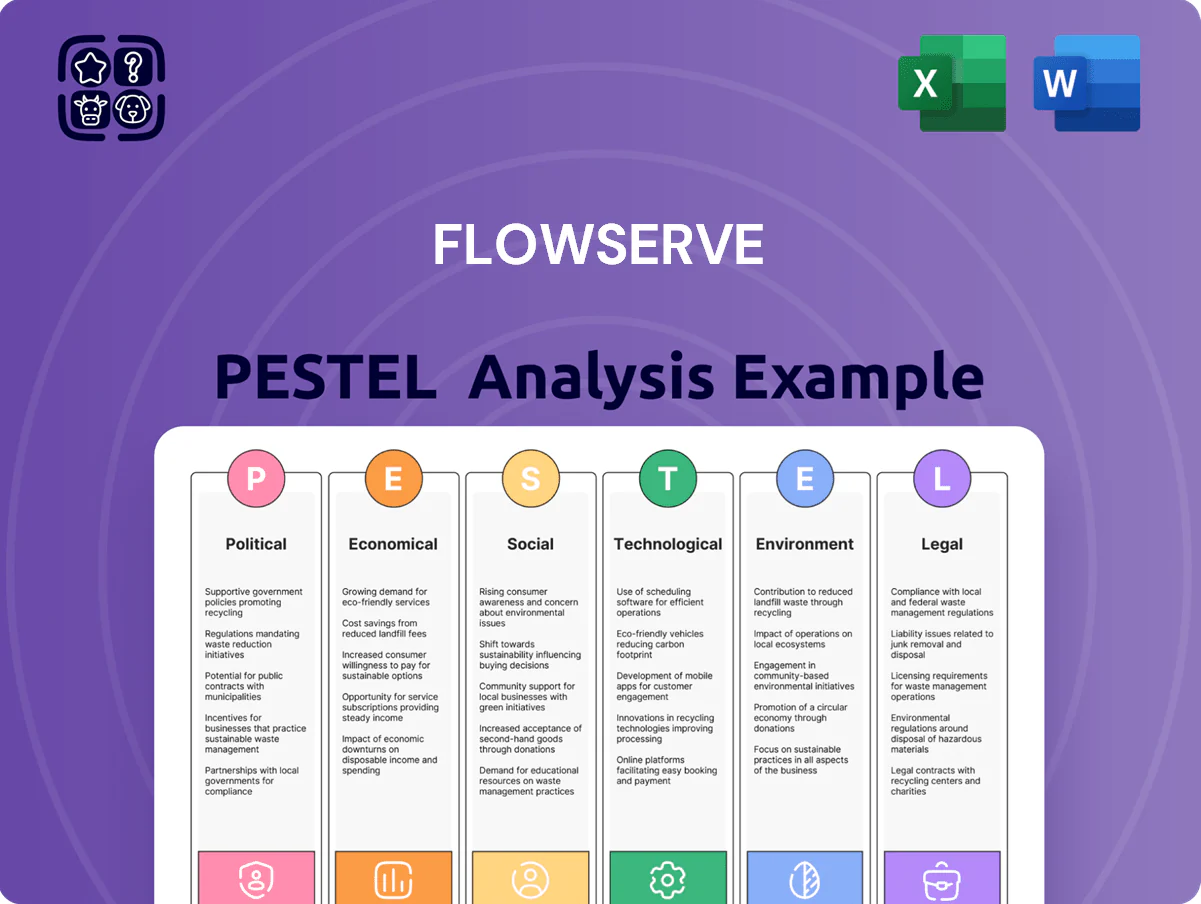

Explores how macro-environmental factors uniquely affect Flowserve across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and industry trends.

Condenses Flowserve's PESTLE into a clean, shareable brief that highlights key external risks and opportunities for quick inclusion in presentations or team planning.

Economic factors

Fluctuations in global energy prices

Fluctuations in global energy prices directly impact Flowserve through customers' capex sensitivity in oil and gas; Brent averaged about 85 USD/bbl in 2025 and WTI 81 USD/bbl by year-end, and a sudden drop could prompt project cancellations or deferred maintenance reducing pump and valve orders. High prices, as seen in 2024–2025, drive spending on efficiency upgrades and aftermarket services, lifting recurring revenue and spare-parts demand.

Interest rate impacts on capital projects

The prevailing interest rate environment raises financing costs for infrastructure and industrial plant projects; US 10-year Treasury yields averaged about 4.2% in 2024, increasing capital costs for Flowserve customers and suppliers. High rates through 2025 can reduce new construction demand, shifting revenue mix toward aftermarket and services, which accounted for roughly 45% of Flowserve’s 2024 sales. As central banks adjust rates, Flowserve must recalibrate growth forecasts to reflect rising client borrowing costs and longer project timelines.

Currency exchange rate volatility

As a global industrial pump and valve supplier, Flowserve faces sizable FX risk repatriating earnings from Europe, China and Brazil; in 2025 the USD strengthened ~4.5% vs EUR and ~3% vs CNY, compressing non‑USD revenue when converted to dollars.

USD appreciation versus BRL (down ~12% in 2024) can make Flowserve products pricier locally, hurting competitiveness in Latin America; reported net sales can swing materially quarter‑to‑quarter.

Flowserve routinely uses forward contracts and FX options; robust hedging is essential to stabilize margins given average daily FX volatility of 0.8–1.5% across major pairs in 2024–25.

Rising demand for water management

Economic growth in water-stressed regions has spurred investment—global desalination capacity rose 3.8% in 2024 to 110 million m3/day, and wastewater capex reached an estimated $90 billion in 2024–25—boosting demand for pumps and treatment equipment.

Water projects act as a countercyclical hedge, offering steadier service revenues versus energy: Flowserve reported 2024 aftermarket growth of ~7%, driven by water segment strength.

Flowserve is targeting this expansion with high-efficiency pump offerings aimed at capturing increased market share in desalination and wastewater retrofit markets.

- Desalination capacity: 110 million m3/day (2024)

- Water/wastewater capex: ~$90B (2024–25)

- Flowserve aftermarket growth: ~7% (2024)

Inflationary pressures on raw materials

Inflation has pushed prices for specialized alloys, engineering polymers and electronic components up roughly 6–12% in 2024 vs 2022, amid supply-chain constraints impacting lead times.

Flowserve mitigates by strategic sourcing, long-term supplier agreements with price-adjustment clauses and hedging, and reported a 3.5% improvement in procurement savings in FY2024.

Persistent inflation necessitates ongoing efficiency gains—Flowserve targets margin protection via productivity, automation and lean initiatives to offset input-cost inflation.

- Alloy/polymer/component inflation ~6–12% (2022–24)

- Procurement savings ~3.5% in FY2024

- Mitigants: strategic sourcing, contract price-clauses, hedging

Energy and rates reroute demand to services; desal capex offsets margin pressure

Energy price swings (Brent ~$85/bbl 2025) and higher rates (US 10-yr ~4.2% 2024) shift demand toward aftermarket/services (~45% sales 2024); USD strength (~+4.5% vs EUR 2025) and input inflation (alloys +6–12% 2022–24) pressure margins; desalination/wastewater capex (~$90B, desal capacity 110M m3/day 2024) provide stable growth opportunities.

| Metric | Value |

|---|---|

| Brent (2025) | $85/bbl |

| US 10-yr (2024) | 4.2% |

| Aftermarket share (2024) | ~45% |

| Desal capacity (2024) | 110M m3/day |

| Water capex (2024–25) | $90B |

| Alloy inflation | 6–12% |

Preview the Actual Deliverable

Flowserve PESTLE Analysis

The preview shown here is the exact Flowserve PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and rapid tech advances are shaping Flowserve’s strategic outlook—our concise PESTLE snapshot highlights key external risks and opportunities so you can act with confidence. Purchase the full PESTLE analysis to access detailed, ready-to-use insights and forecasts tailored for investors, consultants, and strategists.

Political factors

Geopolitical instability in energy producing regions

Ongoing conflicts and diplomatic tensions in the Middle East and Eastern Europe continue to influence global energy security as of late 2025, with IEA reporting 2024–25 oil supply disruptions averaging 1.2 million bpd; Flowserve faces demand volatility for pumps and valves tied to these swings.

Shifting alliances affect delivery to major oil and gas projects—project deferrals in 2024 cut upstream capex by about 6% globally, forcing Flowserve to reallocate inventory and redirect sales channels.

Political volatility triggers sudden export license changes and sanctions—US and EU measures in 2024–25 impacted over $8 billion in energy equipment trade—requiring Flowserve agile supply chain, compliance spend increases, and contingency sourcing.

Trade protectionism and tariff policies

The resurgence of protectionism in 2024–2025, including US steel tariffs and EU safeguard measures, raised input costs for flow-control makers; US Section 232 and EU measures contributed to steel price rises of roughly 15–30% YoY, increasing Flowserve unit production costs materially. Tariffs on specialized components added effective cost uplifts estimated at 3–7% for some pump lines. Flowserve has accelerated localized manufacturing, expanding regional hubs—capex of $120m in 2024—to reduce tariff exposure and shorten supply chains.

Government subsidies for energy transition

Legislative frameworks like the US Inflation Reduction Act (up to $369bn clean energy tax credits through 2031) and the EU Green Deal (€300bn annual low-carbon investment target) materially boost demand for Flowserve pumps in carbon capture, hydrogen and CSP projects; Flowserve reported 2024 renewable orders growth of ~18% year-over-year.

Infrastructure investment programs

Large-scale government spending—US Bipartisan Infrastructure Law $1.2T (2021) with $55B for water, EU’s €300B green deal allocations—continues to drive demand for Flowserve pumps and valves as utilities modernize grids and treatment plants.

Political mandates tackling water scarcity in India, Sub-Saharan Africa and MENA (over 2B people lacking safely managed drinking water per 2022 WHO) create new markets for flow management solutions.

Flowserve tracks national budget allocations and public works procurement pipelines to prioritize sales engagement with funded projects, aligning supply chain and production capacity to capture funded contracts.

- Key drivers: $55B US water funds, €300B EU green allocations

- Opportunity: >2B people without safe water (WHO 2022)

- Strategy: align sales to national budgeted projects

Regulatory shifts in emerging markets

Political transitions in emerging economies often trigger rapid changes in industrial standards and localization rules; Flowserve faced such risks in 2023 when localization mandates in India and Brazil raised component sourcing requirements by up to 30%, impacting supply-chain costs.

Maintaining strong government relations is critical: Flowserve reported ~15% revenue exposure to high-growth emerging markets in 2024, requiring proactive compliance with made‑in‑country mandates to retain contracts.

Failure to adapt can cede market share to domestic firms—local competitors captured an estimated 10–20% share in targeted segments in recent mandate-driven procurement cycles.

- Localization mandates ↑ supply costs ~30% in some markets (2023)

- ~15% of Flowserve revenue exposed to emerging markets (2024)

- Local firms gained 10–20% share where mandates enforced

Geopolitics, tariffs drive costs; renewables lift Flowserve—18% orders, 15% EM risk

Geopolitical conflicts and sanctions (2024–25) caused ~1.2mbd oil disruptions, driving demand volatility; protectionist tariffs lifted steel costs 15–30% and added 3–7% component cost, prompting $120m regional capex (2024). Clean-energy policies (IRA, EU Green Deal) and infrastructure funds ($55B US water, €300B EU) boosted Flowserve renewable orders +18% (2024); ~15% revenue exposed to emerging markets with localization risks.

| Metric | Value |

|---|---|

| Oil supply disruption | 1.2 mbd (2024–25) |

| Steel cost rise | 15–30% YoY (2024) |

| Component tariff impact | 3–7% |

| Regional capex | $120m (2024) |

| Renewable orders growth | +18% (2024) |

| Revenue EM exposure | ~15% (2024) |

What is included in the product

Explores how macro-environmental factors uniquely affect Flowserve across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and industry trends.

Condenses Flowserve's PESTLE into a clean, shareable brief that highlights key external risks and opportunities for quick inclusion in presentations or team planning.

Economic factors

Fluctuations in global energy prices

Fluctuations in global energy prices directly impact Flowserve through customers' capex sensitivity in oil and gas; Brent averaged about 85 USD/bbl in 2025 and WTI 81 USD/bbl by year-end, and a sudden drop could prompt project cancellations or deferred maintenance reducing pump and valve orders. High prices, as seen in 2024–2025, drive spending on efficiency upgrades and aftermarket services, lifting recurring revenue and spare-parts demand.

Interest rate impacts on capital projects

The prevailing interest rate environment raises financing costs for infrastructure and industrial plant projects; US 10-year Treasury yields averaged about 4.2% in 2024, increasing capital costs for Flowserve customers and suppliers. High rates through 2025 can reduce new construction demand, shifting revenue mix toward aftermarket and services, which accounted for roughly 45% of Flowserve’s 2024 sales. As central banks adjust rates, Flowserve must recalibrate growth forecasts to reflect rising client borrowing costs and longer project timelines.

Currency exchange rate volatility

As a global industrial pump and valve supplier, Flowserve faces sizable FX risk repatriating earnings from Europe, China and Brazil; in 2025 the USD strengthened ~4.5% vs EUR and ~3% vs CNY, compressing non‑USD revenue when converted to dollars.

USD appreciation versus BRL (down ~12% in 2024) can make Flowserve products pricier locally, hurting competitiveness in Latin America; reported net sales can swing materially quarter‑to‑quarter.

Flowserve routinely uses forward contracts and FX options; robust hedging is essential to stabilize margins given average daily FX volatility of 0.8–1.5% across major pairs in 2024–25.

Rising demand for water management

Economic growth in water-stressed regions has spurred investment—global desalination capacity rose 3.8% in 2024 to 110 million m3/day, and wastewater capex reached an estimated $90 billion in 2024–25—boosting demand for pumps and treatment equipment.

Water projects act as a countercyclical hedge, offering steadier service revenues versus energy: Flowserve reported 2024 aftermarket growth of ~7%, driven by water segment strength.

Flowserve is targeting this expansion with high-efficiency pump offerings aimed at capturing increased market share in desalination and wastewater retrofit markets.

- Desalination capacity: 110 million m3/day (2024)

- Water/wastewater capex: ~$90B (2024–25)

- Flowserve aftermarket growth: ~7% (2024)

Inflationary pressures on raw materials

Inflation has pushed prices for specialized alloys, engineering polymers and electronic components up roughly 6–12% in 2024 vs 2022, amid supply-chain constraints impacting lead times.

Flowserve mitigates by strategic sourcing, long-term supplier agreements with price-adjustment clauses and hedging, and reported a 3.5% improvement in procurement savings in FY2024.

Persistent inflation necessitates ongoing efficiency gains—Flowserve targets margin protection via productivity, automation and lean initiatives to offset input-cost inflation.

- Alloy/polymer/component inflation ~6–12% (2022–24)

- Procurement savings ~3.5% in FY2024

- Mitigants: strategic sourcing, contract price-clauses, hedging

Energy and rates reroute demand to services; desal capex offsets margin pressure

Energy price swings (Brent ~$85/bbl 2025) and higher rates (US 10-yr ~4.2% 2024) shift demand toward aftermarket/services (~45% sales 2024); USD strength (~+4.5% vs EUR 2025) and input inflation (alloys +6–12% 2022–24) pressure margins; desalination/wastewater capex (~$90B, desal capacity 110M m3/day 2024) provide stable growth opportunities.

| Metric | Value |

|---|---|

| Brent (2025) | $85/bbl |

| US 10-yr (2024) | 4.2% |

| Aftermarket share (2024) | ~45% |

| Desal capacity (2024) | 110M m3/day |

| Water capex (2024–25) | $90B |

| Alloy inflation | 6–12% |

Preview the Actual Deliverable

Flowserve PESTLE Analysis

The preview shown here is the exact Flowserve PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.