Focus Media Information Technology Porter's Five Forces Analysis

From Overview to Strategy Blueprint

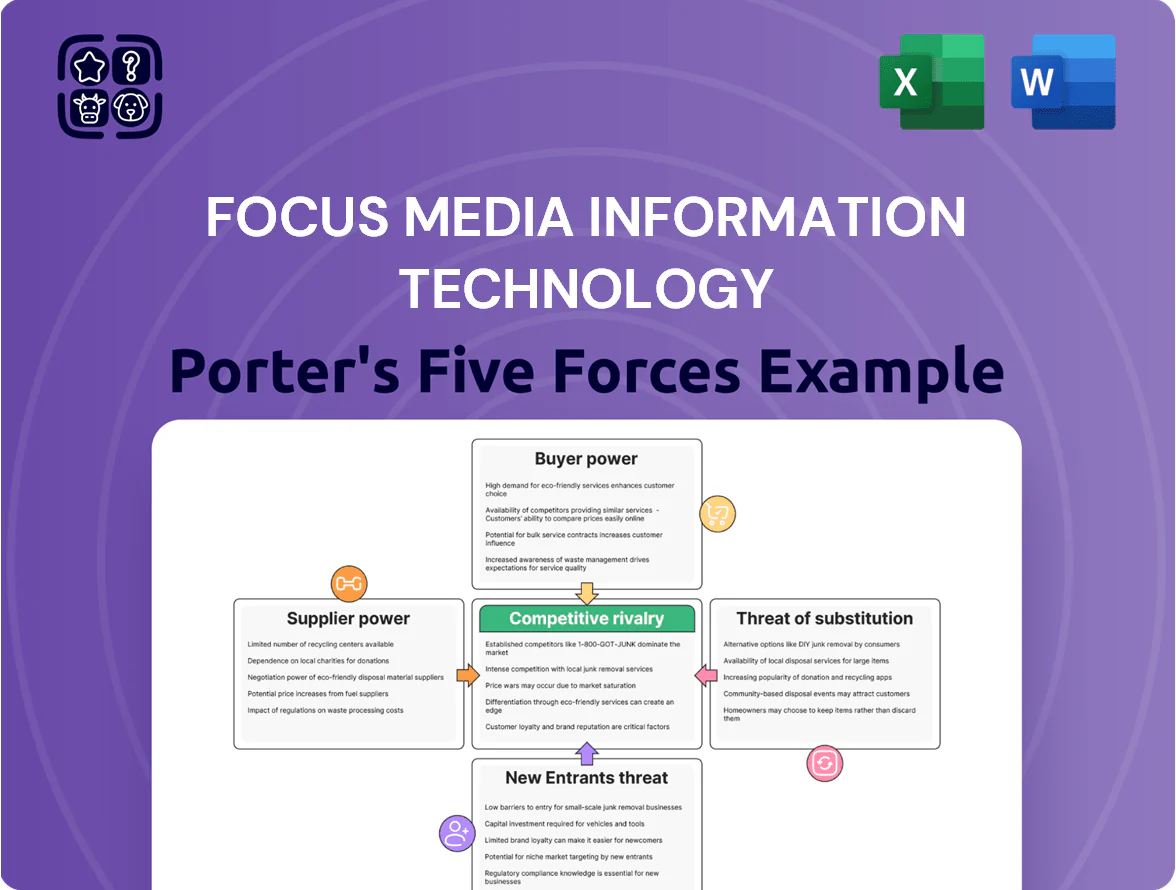

Focus Media Information Technology faces intense competitive rivalry and evolving buyer preferences that pressure margins, while supplier leverage and regulatory shifts create uneven cost dynamics across its digital advertising and tech services.

Emerging entrants and substitutes—driven by programmatic ad tech, OTT platforms, and in-house marketing teams—pose growing threats to market share and pricing power.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Focus Media Information Technology’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Property Management Dominance

Focus Media depends on premium real estate controlled by property management firms and residential committees, which gate access to elevator and lobby screens; in 2024 Beijing and Shanghai saw vacancy-adjusted retail rents fall 2–4% but elevator advertising site rents rose ~8% year-on-year, reflecting landlord leverage.

These managers can demand higher rents or stricter contract terms because they control the physical installation points; with urban elevator penetration exceeding 70% in China’s top 30 cities, high-traffic spots are limited.

As saturation grows, landlords’ bargaining power stays high—estimated site scarcity pushes price premiums of 15–30% for top-tier elevator panels versus secondary locations, squeezing Focus Media’s margins unless it secures long-term leases or revenue-sharing deals.

Hardware and Tech Providers

Focus Media sources digital displays and IoT hardware from multiple electronic manufacturers, and because these components are commoditized it can swap suppliers to preserve margins; supplier-switching lowered component spend volatility by an estimated 8% in 2024 for comparable signage firms. Global semiconductor supply cycles still matter: the 2021–23 chip shortage pushed panel prices up ~15%, and similar disruptions could raise procurement costs quickly. This supplier fragmentation weakens any single vendor’s leverage, though concentrated chip supply (top 3 fabs >70% capacity in 2025) remains a systemic risk.

Cinema Circuit Partnerships

For its movie-theater advertising segment, Focus Media Information Technology must negotiate with major cinema chains that hold moderate supplier power by controlling the captive pre-show audience; in China the top five chains (e.g., Wanda, Dadi) accounted for ~55% of box office in 2024, concentrating access.

Still, Focus Media’s scale—reported 2024 revenue of RMB 11.2 billion—lets it secure multi-year exclusive contracts covering 60–75% of screened locations, which limits sudden price hikes.

Those long-term deals shift bargaining leverage toward Focus Media, though chains can extract premium rates for blockbuster windows and high-traffic urban multiplexes.

Energy and Connectivity Costs

Operational continuity for Focus Media depends on regulated electricity and telco providers for digital signage and remote content management, limiting negotiation power as these are local monopolies/oligopolies.

Energy and connectivity costs are under 5% of operating expenses—Focus Media reported network operation costs of ~RMB 280 million in 2024—yet remain fixed dependencies that scale with rollout.

- Regulated providers → low bargaining power

- Costs ≈ <5% OpEx; RMB 280M network cost in 2024

- Fixed dependency affects scalability and margin

Labor and Maintenance Services

Maintaining 1.2m+ screens nationwide forces Focus Media to rely on local technicians or third-party vendors; in 2024 average hourly maintenance wages in Shanghai rose ~8% YoY to CNY 85, squeezing margins.

Scale lets Focus standardize SOPs and negotiate volume discounts, cutting per-screen service cost by an estimated 12% vs. smaller operators.

Still, specialized skills for AV calibration and network troubleshooting give certified technicians bargaining power, especially in tier-one cities where vacancy rates for skilled maintenance reached ~6% in 2024.

- Network size: 1.2m+ screens (2024)

- Shanghai maintenance wage: CNY 85/hr (2024, +8% YoY)

- Standardization cut service cost ~12%

- Skilled technician vacancy ~6% (2024)

Mixed supplier power squeezes margins — RMB11.2B revenue, 1.2M+ screens, top-5 55%

Suppliers hold mixed power: property managers and top cinema chains exert high leverage on site rents and premium windows, pressuring margins, while commoditized hardware suppliers and Focus Media’s scale reduce vendor leverage; regulated utilities and scarce skilled technicians remain fixed cost risks. Key 2024 figures: RMB 11.2B revenue, 1.2m+ screens, RMB 280M network cost, Shanghai maintenance CNY85/hr, top-5 chains ~55% box office.

| Metric | 2024 value |

|---|---|

| Revenue | RMB 11.2B |

| Screens | 1.2m+ |

| Network cost | RMB 280M |

| Shanghai maintenance wage | CNY 85/hr |

| Top-5 chains box office | ~55% |

What is included in the product

Tailored Porter's Five Forces analysis for Focus Media Information Technology uncovering competitive drivers, buyer and supplier power, barriers to entry, substitute threats, and strategic recommendations to protect market share and inform investor or internal strategy materials.

A concise, one-sheet Porter's Five Forces snapshot tailored to Focus Media Information Technology—perfect for quick strategic decisions and slide-ready sharing.

Customers Bargaining Power

Concentration of Large Advertisers

Low Switching Costs

Advertisers can reallocate budgets from out-of-home (OOH) to social or search within one campaign cycle, raising customer bargaining power as switching costs are low; digital ad spend in China rose 8.6% to RMB 1.2 trillion in 2024, making reallocation easy. This forces Focus Media to prove ROI and reach—its 2024 revenue fell 3.2% in some segments—so it leans into multi-month brand narratives that drive higher attention and are harder to copy on fragmented mobile screens.

Demand for Data Transparency

Modern buyers demand third-party verification and real-time analytics for ad spend; 68% of advertisers in a 2024 IAB survey said transparency influenced buying decisions, pressuring Focus Media to match online granularity. If Focus Media cannot deliver metrics comparable to programmatic platforms, buyers may cut OOH allocations—Global OOH digital share rose to 49% in 2024, signaling shifting spend. The company invested roughly RMB 1.2 billion in 2023–24 on tracking and attribution systems to retain clients and prove ROI.

Macroeconomic Sensitivity

The purchasing power of advertisers is highly cyclical and tracks China's GDP growth; in 2023 ad spend fell 1.4% as consumer spending slowed, making buyers more price-sensitive and selective about media mix.

During slow periods Focus Media must offer flexible packages and add-ons—in 2024 programmatic and bundled solutions grew 12% in revenue for OOH peers—so value-added services help retain clients.

- 2023 China ad market -1.4% decline

- Buyers shift to price-sensitive media mixes

- Flexible packages, programmatic +12% peer revenue

- Value-adds reduce churn in downturns

Direct-to-Consumer Brand Growth

The rise of niche direct-to-consumer brands created a new segment valuing targeted, localized exposure; by 2024 DTC ad spend in China grew ~18% to ~$22B, pushing demand for granular inventory.

Individually these small advertisers have limited bargaining power, but collectively their shift to performance-based buying forced Focus Media to offer CPC/CPA packages and programmatic placements.

Focus Media must adapt its sales model—smaller minimums, automated reporting, and dynamic pricing—to retain these agile advertisers and protect CPMs.

- 2024 China DTC ad spend ~ $22B, +18%

- Shift to performance pricing: CPC/CPA demand up ~30%

- Recommended: lower minimums, programmatic+reporting

Focus Media: Top clients drive 42% revenue as tracking spend lifts margins to ~39.5%

| Metric | 2024 |

|---|---|

| Top-client revenue share | ~42% |

| Gross margin | ~39.5% |

| China digital ad spend | RMB 1.2T (+8.6%) |

| Focus Media tracking spend (2023–24) | ~RMB 1.2B |

| China DTC ad spend | ~$22B (+18%) |

What You See Is What You Get

Focus Media Information Technology Porter's Five Forces Analysis

This preview shows the exact Focus Media Information Technology Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders; the document is fully formatted, professionally written, and ready for use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Focus Media Information Technology faces intense competitive rivalry and evolving buyer preferences that pressure margins, while supplier leverage and regulatory shifts create uneven cost dynamics across its digital advertising and tech services.

Emerging entrants and substitutes—driven by programmatic ad tech, OTT platforms, and in-house marketing teams—pose growing threats to market share and pricing power.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Focus Media Information Technology’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Property Management Dominance

Focus Media depends on premium real estate controlled by property management firms and residential committees, which gate access to elevator and lobby screens; in 2024 Beijing and Shanghai saw vacancy-adjusted retail rents fall 2–4% but elevator advertising site rents rose ~8% year-on-year, reflecting landlord leverage.

These managers can demand higher rents or stricter contract terms because they control the physical installation points; with urban elevator penetration exceeding 70% in China’s top 30 cities, high-traffic spots are limited.

As saturation grows, landlords’ bargaining power stays high—estimated site scarcity pushes price premiums of 15–30% for top-tier elevator panels versus secondary locations, squeezing Focus Media’s margins unless it secures long-term leases or revenue-sharing deals.

Hardware and Tech Providers

Focus Media sources digital displays and IoT hardware from multiple electronic manufacturers, and because these components are commoditized it can swap suppliers to preserve margins; supplier-switching lowered component spend volatility by an estimated 8% in 2024 for comparable signage firms. Global semiconductor supply cycles still matter: the 2021–23 chip shortage pushed panel prices up ~15%, and similar disruptions could raise procurement costs quickly. This supplier fragmentation weakens any single vendor’s leverage, though concentrated chip supply (top 3 fabs >70% capacity in 2025) remains a systemic risk.

Cinema Circuit Partnerships

For its movie-theater advertising segment, Focus Media Information Technology must negotiate with major cinema chains that hold moderate supplier power by controlling the captive pre-show audience; in China the top five chains (e.g., Wanda, Dadi) accounted for ~55% of box office in 2024, concentrating access.

Still, Focus Media’s scale—reported 2024 revenue of RMB 11.2 billion—lets it secure multi-year exclusive contracts covering 60–75% of screened locations, which limits sudden price hikes.

Those long-term deals shift bargaining leverage toward Focus Media, though chains can extract premium rates for blockbuster windows and high-traffic urban multiplexes.

Energy and Connectivity Costs

Operational continuity for Focus Media depends on regulated electricity and telco providers for digital signage and remote content management, limiting negotiation power as these are local monopolies/oligopolies.

Energy and connectivity costs are under 5% of operating expenses—Focus Media reported network operation costs of ~RMB 280 million in 2024—yet remain fixed dependencies that scale with rollout.

- Regulated providers → low bargaining power

- Costs ≈ <5% OpEx; RMB 280M network cost in 2024

- Fixed dependency affects scalability and margin

Labor and Maintenance Services

Maintaining 1.2m+ screens nationwide forces Focus Media to rely on local technicians or third-party vendors; in 2024 average hourly maintenance wages in Shanghai rose ~8% YoY to CNY 85, squeezing margins.

Scale lets Focus standardize SOPs and negotiate volume discounts, cutting per-screen service cost by an estimated 12% vs. smaller operators.

Still, specialized skills for AV calibration and network troubleshooting give certified technicians bargaining power, especially in tier-one cities where vacancy rates for skilled maintenance reached ~6% in 2024.

- Network size: 1.2m+ screens (2024)

- Shanghai maintenance wage: CNY 85/hr (2024, +8% YoY)

- Standardization cut service cost ~12%

- Skilled technician vacancy ~6% (2024)

Mixed supplier power squeezes margins — RMB11.2B revenue, 1.2M+ screens, top-5 55%

Suppliers hold mixed power: property managers and top cinema chains exert high leverage on site rents and premium windows, pressuring margins, while commoditized hardware suppliers and Focus Media’s scale reduce vendor leverage; regulated utilities and scarce skilled technicians remain fixed cost risks. Key 2024 figures: RMB 11.2B revenue, 1.2m+ screens, RMB 280M network cost, Shanghai maintenance CNY85/hr, top-5 chains ~55% box office.

| Metric | 2024 value |

|---|---|

| Revenue | RMB 11.2B |

| Screens | 1.2m+ |

| Network cost | RMB 280M |

| Shanghai maintenance wage | CNY 85/hr |

| Top-5 chains box office | ~55% |

What is included in the product

Tailored Porter's Five Forces analysis for Focus Media Information Technology uncovering competitive drivers, buyer and supplier power, barriers to entry, substitute threats, and strategic recommendations to protect market share and inform investor or internal strategy materials.

A concise, one-sheet Porter's Five Forces snapshot tailored to Focus Media Information Technology—perfect for quick strategic decisions and slide-ready sharing.

Customers Bargaining Power

Concentration of Large Advertisers

Low Switching Costs

Advertisers can reallocate budgets from out-of-home (OOH) to social or search within one campaign cycle, raising customer bargaining power as switching costs are low; digital ad spend in China rose 8.6% to RMB 1.2 trillion in 2024, making reallocation easy. This forces Focus Media to prove ROI and reach—its 2024 revenue fell 3.2% in some segments—so it leans into multi-month brand narratives that drive higher attention and are harder to copy on fragmented mobile screens.

Demand for Data Transparency

Modern buyers demand third-party verification and real-time analytics for ad spend; 68% of advertisers in a 2024 IAB survey said transparency influenced buying decisions, pressuring Focus Media to match online granularity. If Focus Media cannot deliver metrics comparable to programmatic platforms, buyers may cut OOH allocations—Global OOH digital share rose to 49% in 2024, signaling shifting spend. The company invested roughly RMB 1.2 billion in 2023–24 on tracking and attribution systems to retain clients and prove ROI.

Macroeconomic Sensitivity

The purchasing power of advertisers is highly cyclical and tracks China's GDP growth; in 2023 ad spend fell 1.4% as consumer spending slowed, making buyers more price-sensitive and selective about media mix.

During slow periods Focus Media must offer flexible packages and add-ons—in 2024 programmatic and bundled solutions grew 12% in revenue for OOH peers—so value-added services help retain clients.

- 2023 China ad market -1.4% decline

- Buyers shift to price-sensitive media mixes

- Flexible packages, programmatic +12% peer revenue

- Value-adds reduce churn in downturns

Direct-to-Consumer Brand Growth

The rise of niche direct-to-consumer brands created a new segment valuing targeted, localized exposure; by 2024 DTC ad spend in China grew ~18% to ~$22B, pushing demand for granular inventory.

Individually these small advertisers have limited bargaining power, but collectively their shift to performance-based buying forced Focus Media to offer CPC/CPA packages and programmatic placements.

Focus Media must adapt its sales model—smaller minimums, automated reporting, and dynamic pricing—to retain these agile advertisers and protect CPMs.

- 2024 China DTC ad spend ~ $22B, +18%

- Shift to performance pricing: CPC/CPA demand up ~30%

- Recommended: lower minimums, programmatic+reporting

Focus Media: Top clients drive 42% revenue as tracking spend lifts margins to ~39.5%

| Metric | 2024 |

|---|---|

| Top-client revenue share | ~42% |

| Gross margin | ~39.5% |

| China digital ad spend | RMB 1.2T (+8.6%) |

| Focus Media tracking spend (2023–24) | ~RMB 1.2B |

| China DTC ad spend | ~$22B (+18%) |

What You See Is What You Get

Focus Media Information Technology Porter's Five Forces Analysis

This preview shows the exact Focus Media Information Technology Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders; the document is fully formatted, professionally written, and ready for use.