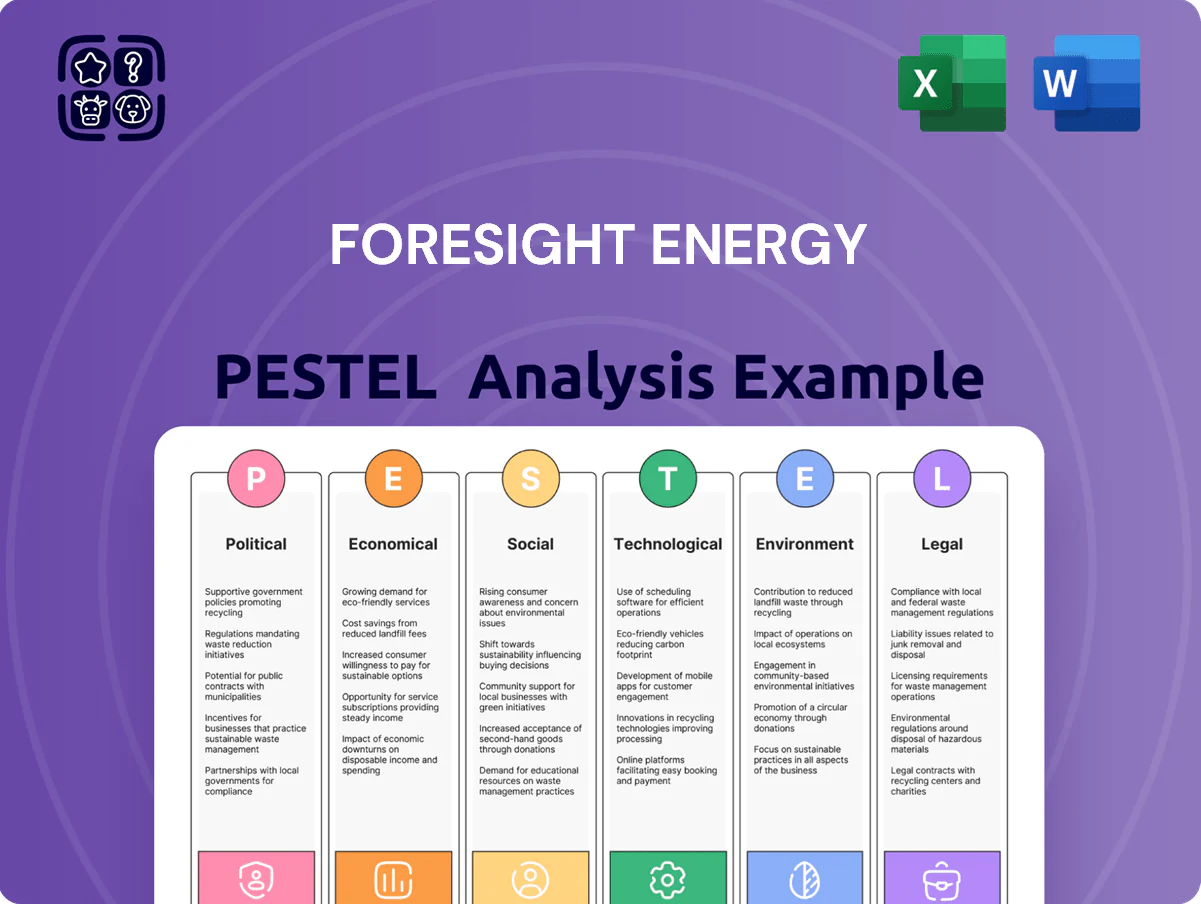

Foresight Energy PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political, economic, and environmental forces are shaping Foresight Energy’s outlook with our concise PESTLE snapshot—perfect for investors and strategists seeking fast, actionable context; purchase the full PESTLE for a comprehensive, editable report with deep-dive insights and practical recommendations.

Political factors

Federal energy policy shifts

As of late 2025 federal policy debates balance energy security and decarbonization, with the Inflation Reduction Act and follow-on measures allocating roughly $120 billion to clean energy incentives while proposed riders could restore limited support for baseload plants; this mix directly affects Illinois Basin coal demand, which fell 18% 2019–2024. Shifts in subsidies versus coal support alter Foresight Energy’s revenue visibility and asset valuation. Changes in the executive branch or Congress can trigger rapid policy pivots that affect coal-fired generation prioritization and regional dispatch economics.

Geopolitical export demand

Political instability in Europe and Asia sustains volatile but steady demand for high-Btu thermal coal, with seaborne coal imports in 2025 at about 900 Mt, keeping export markets critical for Foresight Energy’s ~6.5 Mt annual production capacity.

Foresight depends on stable trade relations and port access—tariffs or diplomatic tensions can delay shipments and compress realized prices, already pressured by a 12% year-on-year decline in coal freight rates in 2024.

Export permits and 2025-updated international climate agreements, which tightened emissions reporting and limited finance for coal projects, materially affect overseas shipment viability and risk-adjusted returns for Foresight’s export strategy.

State-level utility regulation

The Illinois Basin is shaped by state renewable portfolio standards and coal retirement mandates; Illinois targets 100% clean energy by 2050 and accelerated coal retirements cut regional coal generation 28% from 2018–2023.

Infrastructure and permitting politics

Expansion of Foresight Energy's mines and upkeep of rail and Ohio River terminals depend on federal and state permits; in 2024 US Army Corps of Engineers backlog increased permit timelines by 30% in some districts, raising project CAPEX by an estimated 10–20%.

Political opposition to coal permits in key states can delay projects by 12–36 months on average, increasing carrying costs and pushing returns below hurdle rates for marginal mines.

Maintaining inland waterways is critical to Foresight's ~60% rail-and-barge low-cost transport mix; loss of federal dredging funding (a $200–300m annual program in 2024) would raise logistics unit costs materially.

- Permit delays +30% → CAPEX +10–20%

- Opposition can add 12–36 months delay

- Inland waterways support ~60% of transport mix

- Federal dredging funding ~$200–300m/yr (2024)

National security and grid reliability

Political debate now stresses grid reliability amid extreme weather, with 2023 ERCOT and 2021 Texas outages cited; 2024 surveys show 48% of US voters prioritize reliability over emissions, boosting pro-coal policy rhetoric.

Policymakers warn against over-reliance on intermittent renewables—US wind and solar curtailment reached 4.7% in 2023—creating a policy window for thermal coal suppliers.

Foresight Energy presents its high-Btu coal (typically 12,500–13,500 Btu/lb) as essential for base-load stability; coal plants provided ~19% of US generation in 2023, underscoring resilience claims.

- 48% voters prioritize reliability (2024 polls)

- Coal ~19% of US generation (2023)

- Foresight high-Btu coal 12,500–13,500 Btu/lb

- Renewable curtailment 4.7% (2023)

Policy shifts, permit delays & transport strains squeeze Foresight’s 6.5Mt/yr outlook

Federal clean-energy funding (~$120B IRA-era) vs. potential coal supports, trade tensions, and tightened export finance reshape demand for Foresight’s ~6.5 Mt/yr capacity; permit backlogs (+30%) raise CAPEX 10–20% and political opposition can delay projects 12–36 months; inland waterways (supporting ~60% of transport) rely on ~$200–300M/yr dredging; coal ~19% US generation (2023), voters 48% favor reliability (2024).

| Metric | Value |

|---|---|

| Capacity | ~6.5 Mt/yr |

| Permit delays | +30% time → CAPEX +10–20% |

| Transport mix | ~60% rail/barge |

| Dredging fund (2024) | $200–300M/yr |

What is included in the product

Explores how macro-environmental forces uniquely impact Foresight Energy across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify threats and opportunities for executives and investors.

A concise, visually segmented PESTLE summary for Foresight Energy that relieves meeting prep by clearly highlighting political, economic, social, technological, legal, and environmental risks and opportunities, ready to drop into presentations, share across teams, or annotate for region-specific planning.

Economic factors

Global thermal coal price volatility

Foresight Energy is highly sensitive to thermal coal price swings; Newcastle thermal coal fell from about $150/ton in March 2022 to ~$105/ton by end-2023 and averaged near $95/ton in 2024, directly compressing margins for Illinois Basin producers.

Economic slowdowns in China or India could add to global oversupply—China's 2024 coal demand grew just 1.2% vs. 2023—risking further price pressure and margin erosion.

Conversely, supply shocks (e.g., Indonesian export curbs in 2022–23) have previously pushed spot prices up by 20–40%, creating windows for Illinois Basin mines like Foresight to capture higher realized prices.

Operational cost inflation

Rising labor, equipment and consumable costs—steel up ~15% and industrial electricity tariffs up 6–8% through 2025—compress margins for underground operators like Foresight, where labour accounts for ~30% of operating cost. Even as a low‑cost producer (cash cost ~A$35–40/t in 2024–25), Foresight must manage persistent inflation to protect cash flow. Efficient longwall mining, driving unit productivity gains of 5–10%, is critical to offset input inflation and sustain the company’s attractive free cash flow metrics.

Interest rates and debt servicing

The capital-intensive nature of mining means Foresight Energy is sensitive to interest rates for refinancing and expansion capital; US corporate BAA yield rose to about 6.1% in Jan 2025, raising borrowing costs versus 3.5% in 2021. High rates increase debt service, potentially constraining investment in new reserves or clean-tech upgrades. Investors monitor leverage—Foresight reported net debt/EBITDA ~3.8x in FY2024—and free cash flow generation amid tighter margins.

Natural gas price competition

Thermal coal directly competes with natural gas in power generation; US Henry Hub gas averaged about 2.96 USD/MMBtu in 2024, keeping gas-fired dispatch competitive and pressuring coal-fired demand.

When gas prices fall, utilities substitute toward gas, lowering Foresight Energy's domestic sales volume—US coal generation fell ~18% in 2024 vs 2021 as gas share rose.

The economics of Foresight's high-sulfur coal hinge on gas cost relativity and emissions compliance expenses; tighter SO2/CSAPR costs and potential carbon pricing raise coal’s breakeven versus gas.

- 2024 Henry Hub avg ~2.96 USD/MMBtu

- US coal generation down ~18% (2021–2024)

- High-sulfur coal sensitive to emissions control and carbon cost

Freight and logistics costs

The economic efficiency of moving coal from the Illinois Basin to customers is pivotal for Foresight; in 2024 average Class I rail rates rose about 6% year-over-year and inland barge rates spiked 12% during peak season, compressing mine-gate margins.

Rail fuel surcharges and diesel averaging roughly $3.60–$4.20/gal in 2024 can add $5–$12/ton to delivered costs, materially reducing netback pricing.

- 2024 rail rate +6% YoY; barge peak +12%

- Diesel $3.60–$4.20/gal → $5–$12/ton impact

- Transport volatility directly lowers mine-gate netbacks

Foresight margins squeezed as costs, rail hikes and weak coal demand tighten breakeven

Foresight faces margin pressure from 2024 Newcastle ~$95/t coal, US Henry Hub ~$2.96/MMBtu, rising input costs (steel +15%, diesel $3.60–4.20/gal), 2024 rail +6%/barge peak +12%, net debt/EBITDA ~3.8x (FY2024); demand shifts (US coal gen -18% 2021–24) and emissions/carbon costs further tighten breakeven for high‑sulfur coal.

| Metric | 2024/2025 |

|---|---|

| Newcastle | ~$95/t (2024) |

| Henry Hub | $2.96/MMBtu (2024) |

| Rail/barge | +6% / +12% (2024) |

| Net debt/EBITDA | ~3.8x (FY2024) |

Same Document Delivered

Foresight Energy PESTLE Analysis

The preview shown here is the exact Foresight Energy PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political, economic, and environmental forces are shaping Foresight Energy’s outlook with our concise PESTLE snapshot—perfect for investors and strategists seeking fast, actionable context; purchase the full PESTLE for a comprehensive, editable report with deep-dive insights and practical recommendations.

Political factors

Federal energy policy shifts

As of late 2025 federal policy debates balance energy security and decarbonization, with the Inflation Reduction Act and follow-on measures allocating roughly $120 billion to clean energy incentives while proposed riders could restore limited support for baseload plants; this mix directly affects Illinois Basin coal demand, which fell 18% 2019–2024. Shifts in subsidies versus coal support alter Foresight Energy’s revenue visibility and asset valuation. Changes in the executive branch or Congress can trigger rapid policy pivots that affect coal-fired generation prioritization and regional dispatch economics.

Geopolitical export demand

Political instability in Europe and Asia sustains volatile but steady demand for high-Btu thermal coal, with seaborne coal imports in 2025 at about 900 Mt, keeping export markets critical for Foresight Energy’s ~6.5 Mt annual production capacity.

Foresight depends on stable trade relations and port access—tariffs or diplomatic tensions can delay shipments and compress realized prices, already pressured by a 12% year-on-year decline in coal freight rates in 2024.

Export permits and 2025-updated international climate agreements, which tightened emissions reporting and limited finance for coal projects, materially affect overseas shipment viability and risk-adjusted returns for Foresight’s export strategy.

State-level utility regulation

The Illinois Basin is shaped by state renewable portfolio standards and coal retirement mandates; Illinois targets 100% clean energy by 2050 and accelerated coal retirements cut regional coal generation 28% from 2018–2023.

Infrastructure and permitting politics

Expansion of Foresight Energy's mines and upkeep of rail and Ohio River terminals depend on federal and state permits; in 2024 US Army Corps of Engineers backlog increased permit timelines by 30% in some districts, raising project CAPEX by an estimated 10–20%.

Political opposition to coal permits in key states can delay projects by 12–36 months on average, increasing carrying costs and pushing returns below hurdle rates for marginal mines.

Maintaining inland waterways is critical to Foresight's ~60% rail-and-barge low-cost transport mix; loss of federal dredging funding (a $200–300m annual program in 2024) would raise logistics unit costs materially.

- Permit delays +30% → CAPEX +10–20%

- Opposition can add 12–36 months delay

- Inland waterways support ~60% of transport mix

- Federal dredging funding ~$200–300m/yr (2024)

National security and grid reliability

Political debate now stresses grid reliability amid extreme weather, with 2023 ERCOT and 2021 Texas outages cited; 2024 surveys show 48% of US voters prioritize reliability over emissions, boosting pro-coal policy rhetoric.

Policymakers warn against over-reliance on intermittent renewables—US wind and solar curtailment reached 4.7% in 2023—creating a policy window for thermal coal suppliers.

Foresight Energy presents its high-Btu coal (typically 12,500–13,500 Btu/lb) as essential for base-load stability; coal plants provided ~19% of US generation in 2023, underscoring resilience claims.

- 48% voters prioritize reliability (2024 polls)

- Coal ~19% of US generation (2023)

- Foresight high-Btu coal 12,500–13,500 Btu/lb

- Renewable curtailment 4.7% (2023)

Policy shifts, permit delays & transport strains squeeze Foresight’s 6.5Mt/yr outlook

Federal clean-energy funding (~$120B IRA-era) vs. potential coal supports, trade tensions, and tightened export finance reshape demand for Foresight’s ~6.5 Mt/yr capacity; permit backlogs (+30%) raise CAPEX 10–20% and political opposition can delay projects 12–36 months; inland waterways (supporting ~60% of transport) rely on ~$200–300M/yr dredging; coal ~19% US generation (2023), voters 48% favor reliability (2024).

| Metric | Value |

|---|---|

| Capacity | ~6.5 Mt/yr |

| Permit delays | +30% time → CAPEX +10–20% |

| Transport mix | ~60% rail/barge |

| Dredging fund (2024) | $200–300M/yr |

What is included in the product

Explores how macro-environmental forces uniquely impact Foresight Energy across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify threats and opportunities for executives and investors.

A concise, visually segmented PESTLE summary for Foresight Energy that relieves meeting prep by clearly highlighting political, economic, social, technological, legal, and environmental risks and opportunities, ready to drop into presentations, share across teams, or annotate for region-specific planning.

Economic factors

Global thermal coal price volatility

Foresight Energy is highly sensitive to thermal coal price swings; Newcastle thermal coal fell from about $150/ton in March 2022 to ~$105/ton by end-2023 and averaged near $95/ton in 2024, directly compressing margins for Illinois Basin producers.

Economic slowdowns in China or India could add to global oversupply—China's 2024 coal demand grew just 1.2% vs. 2023—risking further price pressure and margin erosion.

Conversely, supply shocks (e.g., Indonesian export curbs in 2022–23) have previously pushed spot prices up by 20–40%, creating windows for Illinois Basin mines like Foresight to capture higher realized prices.

Operational cost inflation

Rising labor, equipment and consumable costs—steel up ~15% and industrial electricity tariffs up 6–8% through 2025—compress margins for underground operators like Foresight, where labour accounts for ~30% of operating cost. Even as a low‑cost producer (cash cost ~A$35–40/t in 2024–25), Foresight must manage persistent inflation to protect cash flow. Efficient longwall mining, driving unit productivity gains of 5–10%, is critical to offset input inflation and sustain the company’s attractive free cash flow metrics.

Interest rates and debt servicing

The capital-intensive nature of mining means Foresight Energy is sensitive to interest rates for refinancing and expansion capital; US corporate BAA yield rose to about 6.1% in Jan 2025, raising borrowing costs versus 3.5% in 2021. High rates increase debt service, potentially constraining investment in new reserves or clean-tech upgrades. Investors monitor leverage—Foresight reported net debt/EBITDA ~3.8x in FY2024—and free cash flow generation amid tighter margins.

Natural gas price competition

Thermal coal directly competes with natural gas in power generation; US Henry Hub gas averaged about 2.96 USD/MMBtu in 2024, keeping gas-fired dispatch competitive and pressuring coal-fired demand.

When gas prices fall, utilities substitute toward gas, lowering Foresight Energy's domestic sales volume—US coal generation fell ~18% in 2024 vs 2021 as gas share rose.

The economics of Foresight's high-sulfur coal hinge on gas cost relativity and emissions compliance expenses; tighter SO2/CSAPR costs and potential carbon pricing raise coal’s breakeven versus gas.

- 2024 Henry Hub avg ~2.96 USD/MMBtu

- US coal generation down ~18% (2021–2024)

- High-sulfur coal sensitive to emissions control and carbon cost

Freight and logistics costs

The economic efficiency of moving coal from the Illinois Basin to customers is pivotal for Foresight; in 2024 average Class I rail rates rose about 6% year-over-year and inland barge rates spiked 12% during peak season, compressing mine-gate margins.

Rail fuel surcharges and diesel averaging roughly $3.60–$4.20/gal in 2024 can add $5–$12/ton to delivered costs, materially reducing netback pricing.

- 2024 rail rate +6% YoY; barge peak +12%

- Diesel $3.60–$4.20/gal → $5–$12/ton impact

- Transport volatility directly lowers mine-gate netbacks

Foresight margins squeezed as costs, rail hikes and weak coal demand tighten breakeven

Foresight faces margin pressure from 2024 Newcastle ~$95/t coal, US Henry Hub ~$2.96/MMBtu, rising input costs (steel +15%, diesel $3.60–4.20/gal), 2024 rail +6%/barge peak +12%, net debt/EBITDA ~3.8x (FY2024); demand shifts (US coal gen -18% 2021–24) and emissions/carbon costs further tighten breakeven for high‑sulfur coal.

| Metric | 2024/2025 |

|---|---|

| Newcastle | ~$95/t (2024) |

| Henry Hub | $2.96/MMBtu (2024) |

| Rail/barge | +6% / +12% (2024) |

| Net debt/EBITDA | ~3.8x (FY2024) |

Same Document Delivered

Foresight Energy PESTLE Analysis

The preview shown here is the exact Foresight Energy PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.