Fortinet Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

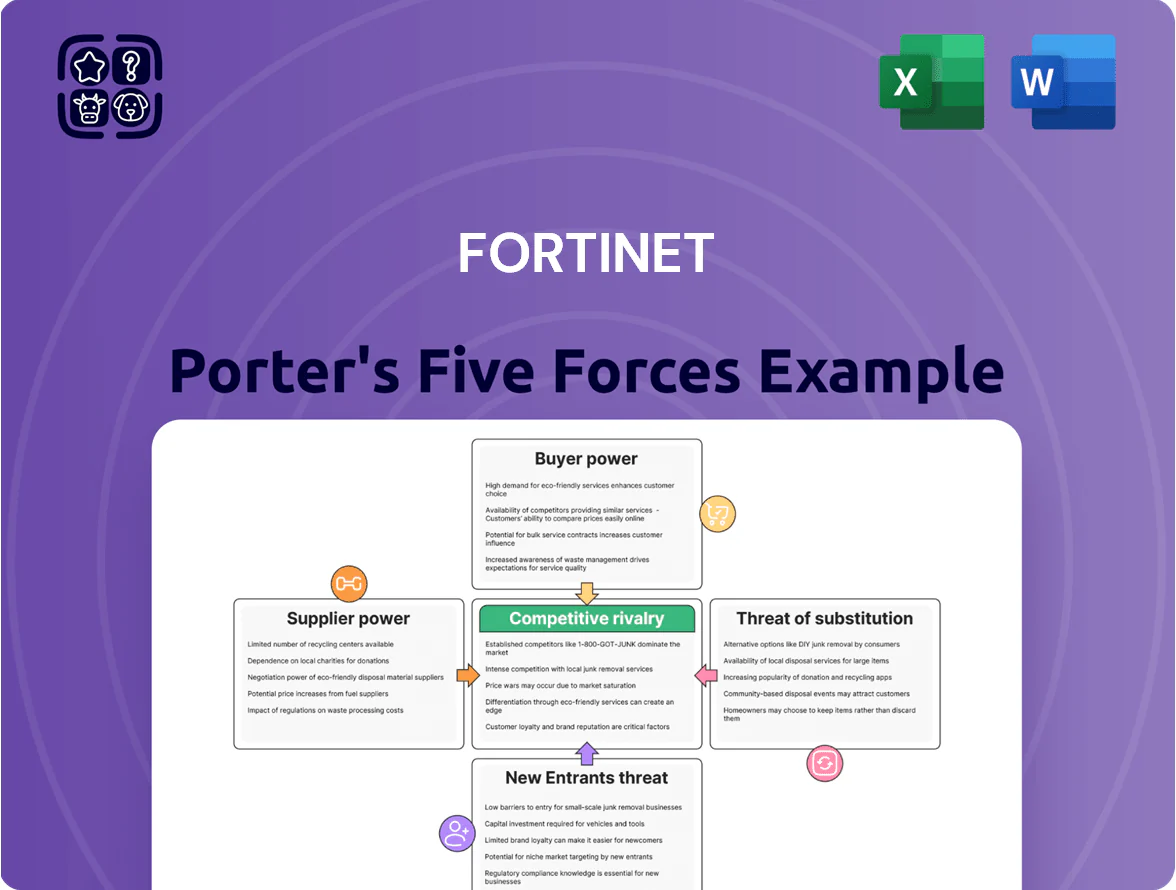

Fortinet faces intense rivalry from established cybersecurity firms, rising pressure from cloud-native competitors, and moderate buyer power as enterprise clients seek integrated, cost-effective solutions.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Fortinet’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on Semiconductor Foundries

Fortinet depends on external foundries such as TSMC for its proprietary ASICs; Fortinet designs chips but owns no fabs, creating concentration risk—TSMC held ~54% of global wafer foundry revenue in 2024, so disruptions there can bottleneck supply. In 2024 supply shortages and a 15–25% silicon price rise in parts of the industry squeezed hardware margins across networking vendors, so similar shocks would materially raise Fortinet’s COGS and delay product deliveries.

Cloud Infrastructure Provider Influence

Fortinet’s shift to cloud-native and virtualized security raises supplier risk as hyperscalers—AWS, Microsoft Azure, Google Cloud—host and list its software; in 2024 these three controlled ~62% of global cloud IaaS/PaaS spend, giving them strong leverage over integration and marketplace terms.

Access to Specialized Cybersecurity Talent

The global shortage of cybersecurity engineers—estimated at 3.5 million unfilled roles in 2025 by (ISC)²—makes talent a powerful supplier for Fortinet; it competes with Microsoft, Google, and well-funded startups for researchers vital to Fortinet’s FortiGuard threat intelligence. High demand lets specialists command salaries 20–40% above IT averages, raising Fortinet’s R&D and SG&A labor costs and pressuring margins over time.

Raw Material and Component Costs

The production of Fortinet FortiGate appliances depends on commoditized semiconductors and metals; many parts have multiple suppliers but chip shortages in 2020–22 raised component costs ~15–30% and forced higher inventories.

Geopolitical strains (eg, 2022–24 rare-earth and Taiwan tensions) can restrict minerals/parts, limiting Fortinet’s bargaining when global shortages hit and causing possible production delays.

- 2022–24 chip price rise ~15–30%

- Inventory buffers increased to cover 3–6 months

- Supplier concentration risk: key components sourced from Asia

Third-Party Software and IP Licensing

Fortinet integrates third-party protocols and tech into its Security Fabric to ensure interoperability; in FY2024 Fortinet reported 44% of software revenue tied to subscriptions and services, increasing reliance on licensed modules.

Licensing fees for patents or specialized modules can vary; a 2023 IAM survey showed 62% of vendors raised IP fees or tightened terms, a risk that can raise Fortinet’s COGS or force price hikes.

If a key provider changes licensing, Fortinet must either absorb costs—pressuring gross margin (Fortinet GAAP gross margin was 74% in FY2024)—or redesign products to substitute tech, which raises R&D spend and delays time-to-market.

- 44% of software revenue from subscriptions/services (FY2024)

- 74% GAAP gross margin (FY2024)

- 62% of vendors tightened IP terms (2023 IAM survey)

Moderate‑high supplier power: TSMC dependence, hyperscalers, talent gap squeeze

Supplier power is moderate‑high: Fortinet relies on TSMC for ASICs (TSMC ~54% wafer revenue in 2024), hyperscalers control ~62% of IaaS/PaaS (2024), cybersecurity talent gap ~3.5M vacancies (ISC2 2025) pushing salaries 20–40% above IT averages, and FY2024 metrics—44% software subscription revenue, 74% GAAP gross margin—limit buffer vs rising IP/license or component costs.

| Metric | Value |

|---|---|

| TSMC share (2024) | ~54% |

| Hyperscaler IaaS/PaaS (2024) | ~62% |

| Cybersecurity workforce gap (2025) | ~3.5M |

| Fortinet software rev (FY2024) | 44% |

| Fortinet GAAP gross margin (FY2024) | 74% |

What is included in the product

Tailored Porter's Five Forces analysis for Fortinet that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats—designed for seamless inclusion in investor decks or strategy reports.

A concise Fortinet Porter’s Five Forces one-sheet that highlights cybersecurity market dynamics—ideal for swift strategic decisions and slide-ready summaries.

Customers Bargaining Power

High Switching Costs for Fabric Integration

Customers who adopt the Fortinet Security Fabric become deeply tied to one ecosystem, raising switching costs in money and time—Gartner estimated integrated security platform migrations can cost 20–40% of initial spend and take 6–18 months (2024), so organizations with Fortinet’s interconnected firewalls, switches, and APs lose leverage post-deployment. The Fabric’s shared telemetry and single-pane management lowers operational costs but makes vendor exit complex, reducing buyer power after selection.

Availability of Tier-One Alternatives

The presence of tier-one rivals—Palo Alto Networks, Cisco, and CrowdStrike—gives large enterprise buyers strong bargaining power; Gartner reported in 2024 that 62% of enterprises run formal bake-offs for security platform purchases. Buyers use competing bids to win discounts; Morgan Stanley noted Palo Alto’s deal win rates rose after pushing aggressive pricing in 2023, compressing Fortinet’s enterprise ASPs. With feature parity across NGFW, EDR, and SASE, price and account-level SLAs drive contract decisions.

Consolidation of IT Spending

Modern enterprises consolidate security stacks to cut complexity and cost, giving large customers more leverage; Fortune 1000 accounts now account for an estimated 40% of enterprise security spend, so vendors like Fortinet (NASDAQ: FTNT) aggressively pursue and retain them. By bundling firewall, SD-WAN, and SASE services, buyers extract volume discounts—contracts often reduce per-unit pricing by 15–30%—and demand premium support SLAs rarely offered to smaller clients.

Price Sensitivity in the Mid-Market

Fortinet’s strong SMB/mid-market footing faces high price sensitivity: 2024 SMB IT spend grew ~6% but average firewall budget under $5,000, so a subscription hike risks migration to lower-cost vendors or open-source (pfSense, OPNsense) and cloud-native offerings.

To defend share, Fortinet must pair its premium features with aggressive pricing tiers; in 2024 Fortinet reported 29% of revenue from product subscriptions, so small price shifts materially affect renewal rates.

- SMB budgets tight; avg firewall spend < $5,000 (2024)

- Open-source options rising (pfSense, OPNsense)

- 29% revenue from subscriptions (Fortinet 2024)

- Need: feature-price balance to protect renewals

Information Transparency and Third-Party Testing

Independent labs like NSS Labs and Gartner publish frequent benchmark reports; in 2024 Gartner rated Fortinet in the 2024 Magic Quadrant for Network Firewalls and NSS-style AV/IPS tests showed Fortinet throughput and threat-blocking metrics comparable to Palo Alto and Check Point, forcing decisions on objective performance not brand alone.

Buyers reference these public scores—surveys show 62% of enterprise buyers cite third-party tests as decisive—so customers press for SLAs and remediation clauses, reducing Fortinet’s pricing leverage and increasing contractual accountability for security gaps.

- Third-party tests shape buying decisions

- 62% of enterprises rely on benchmarks (2024 survey)

- Forces SLAs, remediation demands

- Limits Fortinet’s brand-only pricing power

Ecosystem lock-in vs. price pressure: bake-offs, discounts & rising open-source threats

Customers gain strong leverage: ecosystem lock-in raises switching costs (migrations cost 20–40% of spend, 6–18 months, Gartner 2024) but enterprise buyers run bake-offs (62% do, 2024) and extract 15–30% volume discounts; Fortinet’s 29% subscription revenue (2024) makes price moves sensitive, while SMBs (avg firewall < $5,000) drive price pressure and open-source alternatives rise.

| Metric | Value |

|---|---|

| Migration cost | 20–40% |

| Migration time | 6–18 months |

| Enterprise bake-offs | 62% |

| Volume discounts | 15–30% |

| Fortinet subs rev | 29% |

| Avg SMB firewall | <$5,000 |

Full Version Awaits

Fortinet Porter's Five Forces Analysis

This Fortinet Porter's Five Forces analysis is the exact document you'll receive immediately after purchase—no placeholders or samples, fully formatted and ready for use.

The previewed file matches the full version in content and structure, providing immediate, actionable insights into competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry.

You're viewing the final deliverable; once purchased you’ll get instant access to this same professionally written analysis for download and application.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Fortinet faces intense rivalry from established cybersecurity firms, rising pressure from cloud-native competitors, and moderate buyer power as enterprise clients seek integrated, cost-effective solutions.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Fortinet’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on Semiconductor Foundries

Fortinet depends on external foundries such as TSMC for its proprietary ASICs; Fortinet designs chips but owns no fabs, creating concentration risk—TSMC held ~54% of global wafer foundry revenue in 2024, so disruptions there can bottleneck supply. In 2024 supply shortages and a 15–25% silicon price rise in parts of the industry squeezed hardware margins across networking vendors, so similar shocks would materially raise Fortinet’s COGS and delay product deliveries.

Cloud Infrastructure Provider Influence

Fortinet’s shift to cloud-native and virtualized security raises supplier risk as hyperscalers—AWS, Microsoft Azure, Google Cloud—host and list its software; in 2024 these three controlled ~62% of global cloud IaaS/PaaS spend, giving them strong leverage over integration and marketplace terms.

Access to Specialized Cybersecurity Talent

The global shortage of cybersecurity engineers—estimated at 3.5 million unfilled roles in 2025 by (ISC)²—makes talent a powerful supplier for Fortinet; it competes with Microsoft, Google, and well-funded startups for researchers vital to Fortinet’s FortiGuard threat intelligence. High demand lets specialists command salaries 20–40% above IT averages, raising Fortinet’s R&D and SG&A labor costs and pressuring margins over time.

Raw Material and Component Costs

The production of Fortinet FortiGate appliances depends on commoditized semiconductors and metals; many parts have multiple suppliers but chip shortages in 2020–22 raised component costs ~15–30% and forced higher inventories.

Geopolitical strains (eg, 2022–24 rare-earth and Taiwan tensions) can restrict minerals/parts, limiting Fortinet’s bargaining when global shortages hit and causing possible production delays.

- 2022–24 chip price rise ~15–30%

- Inventory buffers increased to cover 3–6 months

- Supplier concentration risk: key components sourced from Asia

Third-Party Software and IP Licensing

Fortinet integrates third-party protocols and tech into its Security Fabric to ensure interoperability; in FY2024 Fortinet reported 44% of software revenue tied to subscriptions and services, increasing reliance on licensed modules.

Licensing fees for patents or specialized modules can vary; a 2023 IAM survey showed 62% of vendors raised IP fees or tightened terms, a risk that can raise Fortinet’s COGS or force price hikes.

If a key provider changes licensing, Fortinet must either absorb costs—pressuring gross margin (Fortinet GAAP gross margin was 74% in FY2024)—or redesign products to substitute tech, which raises R&D spend and delays time-to-market.

- 44% of software revenue from subscriptions/services (FY2024)

- 74% GAAP gross margin (FY2024)

- 62% of vendors tightened IP terms (2023 IAM survey)

Moderate‑high supplier power: TSMC dependence, hyperscalers, talent gap squeeze

Supplier power is moderate‑high: Fortinet relies on TSMC for ASICs (TSMC ~54% wafer revenue in 2024), hyperscalers control ~62% of IaaS/PaaS (2024), cybersecurity talent gap ~3.5M vacancies (ISC2 2025) pushing salaries 20–40% above IT averages, and FY2024 metrics—44% software subscription revenue, 74% GAAP gross margin—limit buffer vs rising IP/license or component costs.

| Metric | Value |

|---|---|

| TSMC share (2024) | ~54% |

| Hyperscaler IaaS/PaaS (2024) | ~62% |

| Cybersecurity workforce gap (2025) | ~3.5M |

| Fortinet software rev (FY2024) | 44% |

| Fortinet GAAP gross margin (FY2024) | 74% |

What is included in the product

Tailored Porter's Five Forces analysis for Fortinet that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats—designed for seamless inclusion in investor decks or strategy reports.

A concise Fortinet Porter’s Five Forces one-sheet that highlights cybersecurity market dynamics—ideal for swift strategic decisions and slide-ready summaries.

Customers Bargaining Power

High Switching Costs for Fabric Integration

Customers who adopt the Fortinet Security Fabric become deeply tied to one ecosystem, raising switching costs in money and time—Gartner estimated integrated security platform migrations can cost 20–40% of initial spend and take 6–18 months (2024), so organizations with Fortinet’s interconnected firewalls, switches, and APs lose leverage post-deployment. The Fabric’s shared telemetry and single-pane management lowers operational costs but makes vendor exit complex, reducing buyer power after selection.

Availability of Tier-One Alternatives

The presence of tier-one rivals—Palo Alto Networks, Cisco, and CrowdStrike—gives large enterprise buyers strong bargaining power; Gartner reported in 2024 that 62% of enterprises run formal bake-offs for security platform purchases. Buyers use competing bids to win discounts; Morgan Stanley noted Palo Alto’s deal win rates rose after pushing aggressive pricing in 2023, compressing Fortinet’s enterprise ASPs. With feature parity across NGFW, EDR, and SASE, price and account-level SLAs drive contract decisions.

Consolidation of IT Spending

Modern enterprises consolidate security stacks to cut complexity and cost, giving large customers more leverage; Fortune 1000 accounts now account for an estimated 40% of enterprise security spend, so vendors like Fortinet (NASDAQ: FTNT) aggressively pursue and retain them. By bundling firewall, SD-WAN, and SASE services, buyers extract volume discounts—contracts often reduce per-unit pricing by 15–30%—and demand premium support SLAs rarely offered to smaller clients.

Price Sensitivity in the Mid-Market

Fortinet’s strong SMB/mid-market footing faces high price sensitivity: 2024 SMB IT spend grew ~6% but average firewall budget under $5,000, so a subscription hike risks migration to lower-cost vendors or open-source (pfSense, OPNsense) and cloud-native offerings.

To defend share, Fortinet must pair its premium features with aggressive pricing tiers; in 2024 Fortinet reported 29% of revenue from product subscriptions, so small price shifts materially affect renewal rates.

- SMB budgets tight; avg firewall spend < $5,000 (2024)

- Open-source options rising (pfSense, OPNsense)

- 29% revenue from subscriptions (Fortinet 2024)

- Need: feature-price balance to protect renewals

Information Transparency and Third-Party Testing

Independent labs like NSS Labs and Gartner publish frequent benchmark reports; in 2024 Gartner rated Fortinet in the 2024 Magic Quadrant for Network Firewalls and NSS-style AV/IPS tests showed Fortinet throughput and threat-blocking metrics comparable to Palo Alto and Check Point, forcing decisions on objective performance not brand alone.

Buyers reference these public scores—surveys show 62% of enterprise buyers cite third-party tests as decisive—so customers press for SLAs and remediation clauses, reducing Fortinet’s pricing leverage and increasing contractual accountability for security gaps.

- Third-party tests shape buying decisions

- 62% of enterprises rely on benchmarks (2024 survey)

- Forces SLAs, remediation demands

- Limits Fortinet’s brand-only pricing power

Ecosystem lock-in vs. price pressure: bake-offs, discounts & rising open-source threats

Customers gain strong leverage: ecosystem lock-in raises switching costs (migrations cost 20–40% of spend, 6–18 months, Gartner 2024) but enterprise buyers run bake-offs (62% do, 2024) and extract 15–30% volume discounts; Fortinet’s 29% subscription revenue (2024) makes price moves sensitive, while SMBs (avg firewall < $5,000) drive price pressure and open-source alternatives rise.

| Metric | Value |

|---|---|

| Migration cost | 20–40% |

| Migration time | 6–18 months |

| Enterprise bake-offs | 62% |

| Volume discounts | 15–30% |

| Fortinet subs rev | 29% |

| Avg SMB firewall | <$5,000 |

Full Version Awaits

Fortinet Porter's Five Forces Analysis

This Fortinet Porter's Five Forces analysis is the exact document you'll receive immediately after purchase—no placeholders or samples, fully formatted and ready for use.

The previewed file matches the full version in content and structure, providing immediate, actionable insights into competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry.

You're viewing the final deliverable; once purchased you’ll get instant access to this same professionally written analysis for download and application.