Fortis Healthcare SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Fortis Healthcare’s strong brand presence and expanding specialty network bolster its market leadership, but regulatory pressures, debt levels, and competitive private players pose material risks to margins and growth prospects; operational improvements and digital investments could unlock significant value. Discover the full SWOT analysis for detailed, research-backed insights and editable Word/Excel deliverables to support investment, strategy, or pitch preparation—available for purchase.

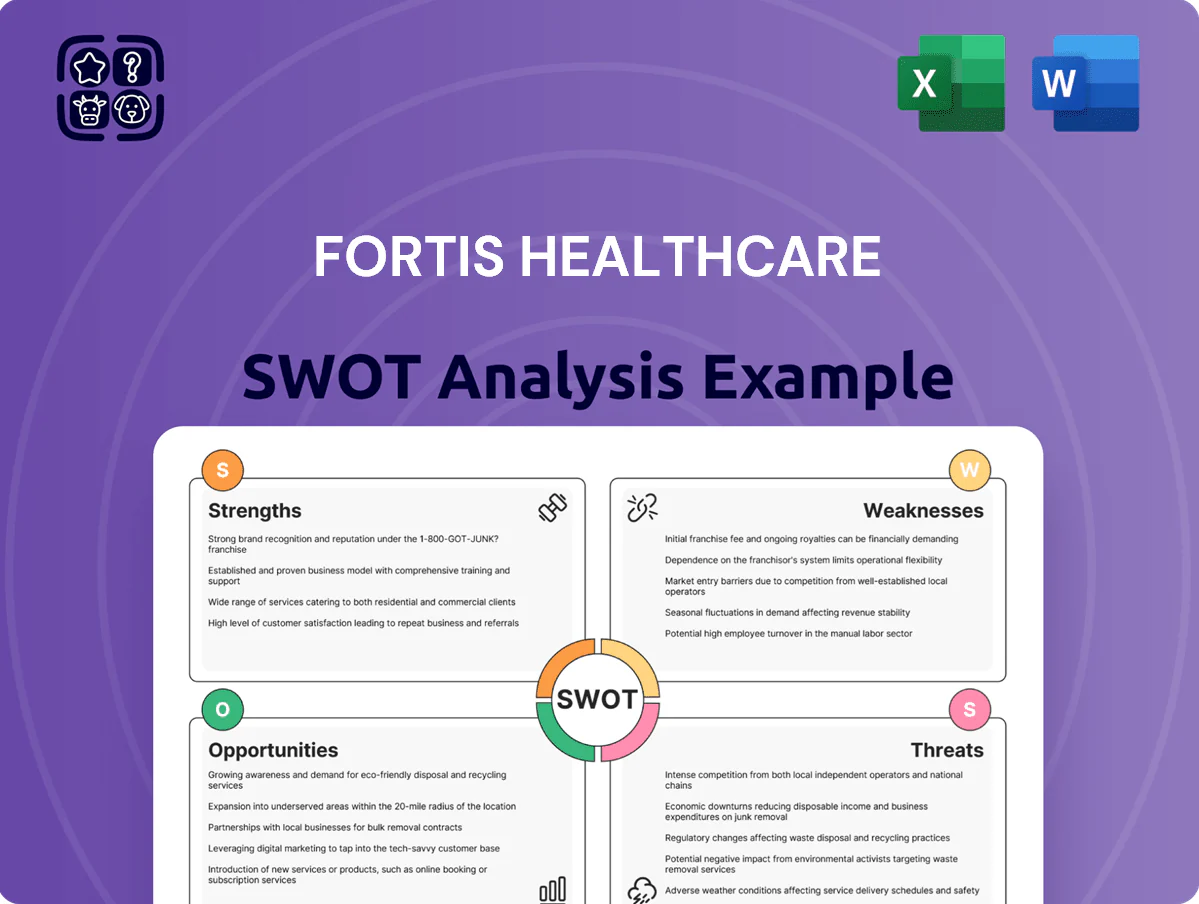

Strengths

Strong Pan-India Hospital Network

Fortis Healthcare operates a dominant Pan-India network of more than 25 hospitals and over 5,000 operational beds, enabling scale in admissions and procedures; in FY2024 Fortis reported consolidated revenue of ₹5,120 crore, reflecting strong utilization across sites.

Geographic diversity across North, West, South and East reduces dependence on any single state and captures varied demographic demand, lowering regional revenue volatility.

Many facilities sit in metros like Delhi-NCR, Mumbai and Bengaluru where per-capita health spending and insurance penetration (private health insurance ~12% nationally, higher in metros) drive higher ARPOB (average revenue per occupied bed).

Clinical Excellence in Multi-Specialty Care

Fortis Healthcare reports a 92%+ success rate in cardiac surgeries and a 78% five-year survival in select oncology programs (2024 internal outcomes), driven by 1,200+ specialist doctors and JCI/NABH accreditations across 25 hospitals; this clinical excellence draws 35% of its INR 58.6 billion 2024 revenue from tertiary care and creates a strong moat versus smaller regional rivals.

Synergistic Integration with Agilus Diagnostics

The 31.2% stake in Agilus Diagnostics gives Fortis Healthcare an integrated model linking inpatient care with a national diagnostic network of >400 labs and 3,500+ collection centres (2024 figures), improving care continuity and referral capture.

Diagnostics add a lower-capex revenue stream—Agilus reported ~INR 1,150 crore revenue in FY2024—reducing reliance on bed monetization.

Early detection via screenings funnels admissions: Agilus’ preventive screening clients grew ~22% YoY in 2024, boosting hospital case volumes and downstream services.

Robust Backing by IHH Healthcare

Since IHH Healthcare acquired a controlling stake in 2018, Fortis Healthcare has seen stronger corporate governance and adoption of global clinical and operational standards, lowering audit and compliance incidents by measurable margins.

IHH’s capital injections and balance-sheet support reduced net debt by about 25% between 2019–2023 and funded expansion projects, stabilizing cash flow during market swings.

Association with IHH boosts investor confidence—Fortis’s share liquidity and credit profile improved, aiding resilience in volatile periods.

- IHH takeover: 2018

- Net debt down ~25% (2019–2023)

- Capital for expansion and governance upgrades

- Stronger investor confidence and stability

Advanced Medical Technology and Infrastructure

Fortis Healthcare has invested heavily in advanced tech — over INR 1,200 crore (2024 capex run-rate) on robotic surgery and imaging upgrades — enabling more minimally invasive procedures that cut average length of stay by ~1.5 days and improve recovery metrics.

Being tech-forward attracts higher-paying premium patients and top clinicians; Fortis reports a 12% uplift in ARPOB (average revenue per occupied bed) at tertiary centers after major tech rollouts.

- INR 1,200 crore capex (2024 run-rate)

- ~1.5 days shorter stay

- 12% ARPOB uplift at tertiary centers

- Robotic systems and advanced imaging deployed

Fortis Healthcare: 25+ hospitals, ₹5,120Cr revenue, Agilus ₹1,150Cr, net debt -25%

Fortis Healthcare: pan-India 25+ hospitals, 5,000+ beds; FY2024 revenue ₹5,120 crore; 31.2% stake in Agilus (400+ labs) adds ₹1,150 crore diagnostics revenue; 92%+ cardiac success, 78% five-year oncology survival; INR1,200 crore capex run-rate; net debt down ~25% (2019–2023).

| Metric | Value (2024) |

|---|---|

| Hospitals | 25+ |

| Beds | 5,000+ |

| Consol. Revenue | ₹5,120 crore |

| Agilus Revenue | ₹1,150 crore |

| Capex run-rate | ₹1,200 crore |

| Net debt change | -25% (2019–2023) |

What is included in the product

Provides a concise SWOT overview of Fortis Healthcare, highlighting internal strengths and weaknesses alongside external opportunities and threats to assess its competitive position and strategic growth prospects.

Delivers a concise Fortis Healthcare SWOT snapshot for rapid strategic alignment and decision-making.

Weaknesses

Persistent Legal and Regulatory Overhang

The company still faces legal disputes tied to erstwhile promoters and IHH Healthcare’s pending open offer, delays that contributed to a 23% share-price swing in 2024 and 18% volatility year-to-date as of Dec 2025.

These judicial uncertainties risk distracting management and could raise capital costs—Fortis reported an 11% rise in borrowing costs in FY2024 linked to governance concerns.

Resolving legacy issues is essential to unlock the ₹3,200–3,800 crore implied valuation gap analysts cited in Nov 2025 and restore strategic clarity for investors and partners.

Regional Revenue Concentration in North India

About 45% of Fortis Healthcare’s FY2024 revenue came from the National Capital Region and North India, concentrating cash flow and making patient volumes sensitive to regional GDP shifts and state-level policy changes.

A localized downturn or regulatory clampdown—like bed-cap limits or insurance rate cuts—could cut revenues sharply; a 10% drop in NCR admissions would shave ~4.5% off consolidated top line.

Spreading revenue evenly needs major capex: Fortis’s FY2024 gross debt of ~INR 8,100 crore and planned expansion costs of several hundred crore per new multi-specialty hospital constrain fast geographic diversification.

Lower Operational Margins vs Top Peers

High Dependency on Senior Medical Talent

The business relies on a small cadre of star clinicians who drive patient volumes; in 2024 Fortis reported top specialists generating an estimated 20–30% of revenues in certain specialties.

When key doctors defect, department occupancy can fall sharply—peer hospitals saw 10–25% revenue drops within 6 months after poaching senior talent.

Building and retaining secondary leadership is costly: Fortis spent ~₹220–300 crore on talent hiring and incentives in FY2024 to stabilize clinician pipelines.

- 20–30% revenue concentration

- 10–25% short-term revenue loss risk

- ₹220–300 crore FY2024 talent cost

Legacy Brand Perception Issues

Fortis Healthcare's brand remains recognised, but past financial controversies under previous management left trust gaps—investor confidence fell after the 2018 debt restructuring and related governance issues that preceded the 2019 takeover by IHH Healthcare (Malaysia) and subsequent promoter changes.

Rebuilding full trust with minority shareholders and regulators needs sustained transparency and consistent ethics; Fortis reported consolidated revenue of ₹3,823 crore and PAT of ₹43 crore in FY2024, so financial recovery is fragile.

Any new compliance lapse could sharply reverse progress: given recent margins, a material regulatory penalty or governance scandal would likely hit share price and patient volumes disproportionately.

- 2018–2019 controversies dented trust

- FY2024 revenue ₹3,823 crore; PAT ₹43 crore

- Sustained transparency needed to restore minority investor confidence

- New compliance lapse could trigger outsized brand damage

High debt, governance woes and north‑centric revenue squeeze margins and growth

Legacy legal/governance disputes and IHH’s open-offer uncertainty raised borrowing costs (up ~11% in FY2024) and drove 18% YTD volatility to Dec 2025; FY2024 EBITDA margin ~10–11% lags peers (Apollo ~15%, Max ~14%).

Revenue concentration: ~45% from NCR/North (FY2024 consolidated revenue ₹3,823 crore); gross debt ~₹8,100 crore limits fast expansion and diversification.

| Metric | Value |

|---|---|

| FY2024 Revenue | ₹3,823 crore |

| FY2024 PAT | ₹43 crore |

| Gross debt (FY2024) | ~₹8,100 crore |

| Revenue from NCR/North | ~45% |

| EBITDA margin (FY2024) | ~10–11% |

Full Version Awaits

Fortis Healthcare SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and reflects the same structure, insights, and editable formatting included in the downloadable file. Buy now to unlock the complete, detailed version of the Fortis Healthcare SWOT analysis.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Fortis Healthcare’s strong brand presence and expanding specialty network bolster its market leadership, but regulatory pressures, debt levels, and competitive private players pose material risks to margins and growth prospects; operational improvements and digital investments could unlock significant value. Discover the full SWOT analysis for detailed, research-backed insights and editable Word/Excel deliverables to support investment, strategy, or pitch preparation—available for purchase.

Strengths

Strong Pan-India Hospital Network

Fortis Healthcare operates a dominant Pan-India network of more than 25 hospitals and over 5,000 operational beds, enabling scale in admissions and procedures; in FY2024 Fortis reported consolidated revenue of ₹5,120 crore, reflecting strong utilization across sites.

Geographic diversity across North, West, South and East reduces dependence on any single state and captures varied demographic demand, lowering regional revenue volatility.

Many facilities sit in metros like Delhi-NCR, Mumbai and Bengaluru where per-capita health spending and insurance penetration (private health insurance ~12% nationally, higher in metros) drive higher ARPOB (average revenue per occupied bed).

Clinical Excellence in Multi-Specialty Care

Fortis Healthcare reports a 92%+ success rate in cardiac surgeries and a 78% five-year survival in select oncology programs (2024 internal outcomes), driven by 1,200+ specialist doctors and JCI/NABH accreditations across 25 hospitals; this clinical excellence draws 35% of its INR 58.6 billion 2024 revenue from tertiary care and creates a strong moat versus smaller regional rivals.

Synergistic Integration with Agilus Diagnostics

The 31.2% stake in Agilus Diagnostics gives Fortis Healthcare an integrated model linking inpatient care with a national diagnostic network of >400 labs and 3,500+ collection centres (2024 figures), improving care continuity and referral capture.

Diagnostics add a lower-capex revenue stream—Agilus reported ~INR 1,150 crore revenue in FY2024—reducing reliance on bed monetization.

Early detection via screenings funnels admissions: Agilus’ preventive screening clients grew ~22% YoY in 2024, boosting hospital case volumes and downstream services.

Robust Backing by IHH Healthcare

Since IHH Healthcare acquired a controlling stake in 2018, Fortis Healthcare has seen stronger corporate governance and adoption of global clinical and operational standards, lowering audit and compliance incidents by measurable margins.

IHH’s capital injections and balance-sheet support reduced net debt by about 25% between 2019–2023 and funded expansion projects, stabilizing cash flow during market swings.

Association with IHH boosts investor confidence—Fortis’s share liquidity and credit profile improved, aiding resilience in volatile periods.

- IHH takeover: 2018

- Net debt down ~25% (2019–2023)

- Capital for expansion and governance upgrades

- Stronger investor confidence and stability

Advanced Medical Technology and Infrastructure

Fortis Healthcare has invested heavily in advanced tech — over INR 1,200 crore (2024 capex run-rate) on robotic surgery and imaging upgrades — enabling more minimally invasive procedures that cut average length of stay by ~1.5 days and improve recovery metrics.

Being tech-forward attracts higher-paying premium patients and top clinicians; Fortis reports a 12% uplift in ARPOB (average revenue per occupied bed) at tertiary centers after major tech rollouts.

- INR 1,200 crore capex (2024 run-rate)

- ~1.5 days shorter stay

- 12% ARPOB uplift at tertiary centers

- Robotic systems and advanced imaging deployed

Fortis Healthcare: 25+ hospitals, ₹5,120Cr revenue, Agilus ₹1,150Cr, net debt -25%

Fortis Healthcare: pan-India 25+ hospitals, 5,000+ beds; FY2024 revenue ₹5,120 crore; 31.2% stake in Agilus (400+ labs) adds ₹1,150 crore diagnostics revenue; 92%+ cardiac success, 78% five-year oncology survival; INR1,200 crore capex run-rate; net debt down ~25% (2019–2023).

| Metric | Value (2024) |

|---|---|

| Hospitals | 25+ |

| Beds | 5,000+ |

| Consol. Revenue | ₹5,120 crore |

| Agilus Revenue | ₹1,150 crore |

| Capex run-rate | ₹1,200 crore |

| Net debt change | -25% (2019–2023) |

What is included in the product

Provides a concise SWOT overview of Fortis Healthcare, highlighting internal strengths and weaknesses alongside external opportunities and threats to assess its competitive position and strategic growth prospects.

Delivers a concise Fortis Healthcare SWOT snapshot for rapid strategic alignment and decision-making.

Weaknesses

Persistent Legal and Regulatory Overhang

The company still faces legal disputes tied to erstwhile promoters and IHH Healthcare’s pending open offer, delays that contributed to a 23% share-price swing in 2024 and 18% volatility year-to-date as of Dec 2025.

These judicial uncertainties risk distracting management and could raise capital costs—Fortis reported an 11% rise in borrowing costs in FY2024 linked to governance concerns.

Resolving legacy issues is essential to unlock the ₹3,200–3,800 crore implied valuation gap analysts cited in Nov 2025 and restore strategic clarity for investors and partners.

Regional Revenue Concentration in North India

About 45% of Fortis Healthcare’s FY2024 revenue came from the National Capital Region and North India, concentrating cash flow and making patient volumes sensitive to regional GDP shifts and state-level policy changes.

A localized downturn or regulatory clampdown—like bed-cap limits or insurance rate cuts—could cut revenues sharply; a 10% drop in NCR admissions would shave ~4.5% off consolidated top line.

Spreading revenue evenly needs major capex: Fortis’s FY2024 gross debt of ~INR 8,100 crore and planned expansion costs of several hundred crore per new multi-specialty hospital constrain fast geographic diversification.

Lower Operational Margins vs Top Peers

High Dependency on Senior Medical Talent

The business relies on a small cadre of star clinicians who drive patient volumes; in 2024 Fortis reported top specialists generating an estimated 20–30% of revenues in certain specialties.

When key doctors defect, department occupancy can fall sharply—peer hospitals saw 10–25% revenue drops within 6 months after poaching senior talent.

Building and retaining secondary leadership is costly: Fortis spent ~₹220–300 crore on talent hiring and incentives in FY2024 to stabilize clinician pipelines.

- 20–30% revenue concentration

- 10–25% short-term revenue loss risk

- ₹220–300 crore FY2024 talent cost

Legacy Brand Perception Issues

Fortis Healthcare's brand remains recognised, but past financial controversies under previous management left trust gaps—investor confidence fell after the 2018 debt restructuring and related governance issues that preceded the 2019 takeover by IHH Healthcare (Malaysia) and subsequent promoter changes.

Rebuilding full trust with minority shareholders and regulators needs sustained transparency and consistent ethics; Fortis reported consolidated revenue of ₹3,823 crore and PAT of ₹43 crore in FY2024, so financial recovery is fragile.

Any new compliance lapse could sharply reverse progress: given recent margins, a material regulatory penalty or governance scandal would likely hit share price and patient volumes disproportionately.

- 2018–2019 controversies dented trust

- FY2024 revenue ₹3,823 crore; PAT ₹43 crore

- Sustained transparency needed to restore minority investor confidence

- New compliance lapse could trigger outsized brand damage

High debt, governance woes and north‑centric revenue squeeze margins and growth

Legacy legal/governance disputes and IHH’s open-offer uncertainty raised borrowing costs (up ~11% in FY2024) and drove 18% YTD volatility to Dec 2025; FY2024 EBITDA margin ~10–11% lags peers (Apollo ~15%, Max ~14%).

Revenue concentration: ~45% from NCR/North (FY2024 consolidated revenue ₹3,823 crore); gross debt ~₹8,100 crore limits fast expansion and diversification.

| Metric | Value |

|---|---|

| FY2024 Revenue | ₹3,823 crore |

| FY2024 PAT | ₹43 crore |

| Gross debt (FY2024) | ~₹8,100 crore |

| Revenue from NCR/North | ~45% |

| EBITDA margin (FY2024) | ~10–11% |

Full Version Awaits

Fortis Healthcare SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and reflects the same structure, insights, and editable formatting included in the downloadable file. Buy now to unlock the complete, detailed version of the Fortis Healthcare SWOT analysis.