Fortis (Canada) Boston Consulting Group Matrix

Download Your Competitive Advantage

Fortis (Canada) sits at an intriguing crossroads—regulated utility stability meets selective growth opportunities, with legacy assets behaving like Cash Cows while emerging renewable projects look and feel like potential Stars. Our preview hints at where capital is earning steady returns versus where strategic investment could accelerate market share. Purchase the full BCG Matrix for quadrant-by-quadrant placement, actionable recommendations, and downloadable Word + Excel files to guide confident investment and portfolio decisions.

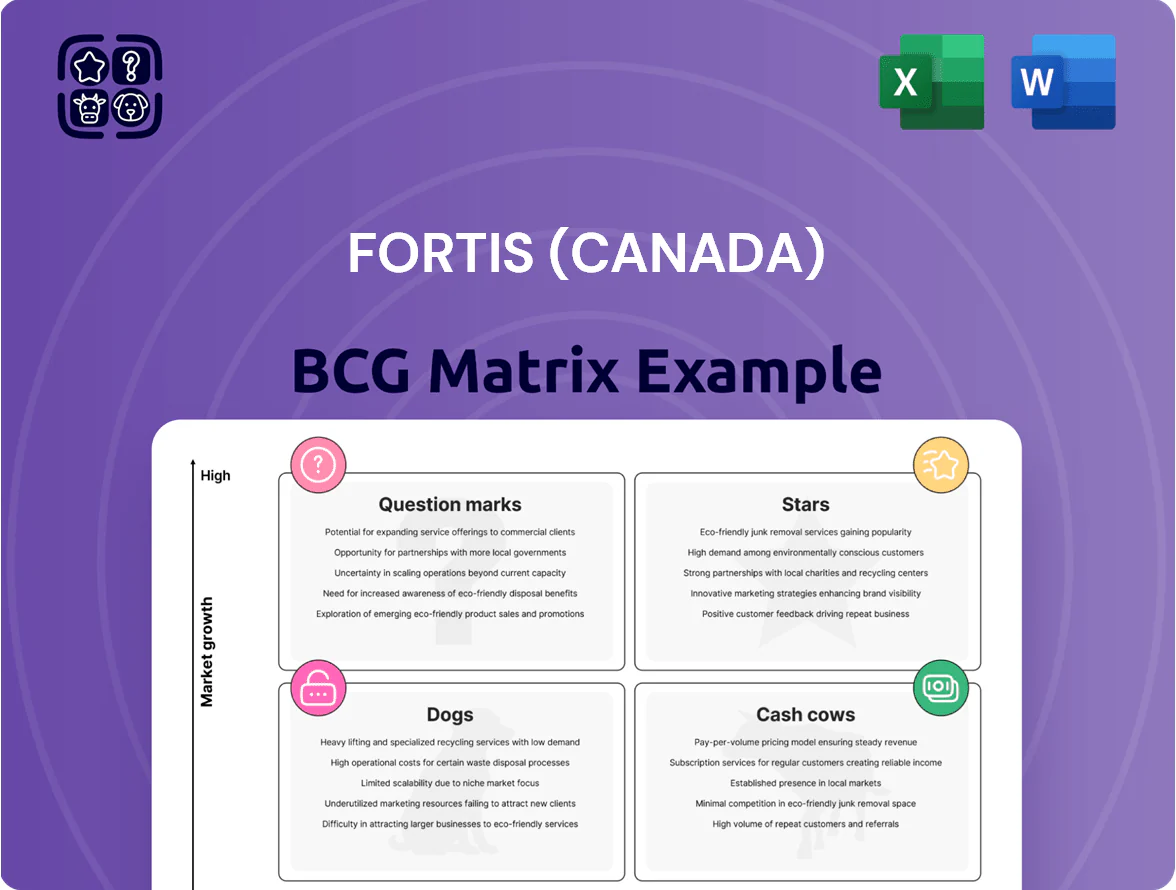

Stars

ITC Holdings Transmission Expansion

ITC Holdings, the largest independent U.S. transmission owner, sits in Fortis’s BCG matrix as a star: high market share in a high-growth market driven by grid modernization; U.S. transmission investments reached about $3.5 billion in 2024, with ITC contributing materially.

The U.S. needs roughly $120–200 billion in new long-distance lines by 2035 to link wind and solar hubs to cities; Fortis has committed multi-billion-dollar capital allocations to ITC expansion through 2025–2027 to capture this demand.

Multi-Value Project (MVP) Pipelines

Multi-Value Project (MVP) Pipelines are large regional transmission builds across the MISO footprint that boost grid reliability and cut emissions; MISO estimates these projects enable ~30% more renewable integration by 2030.

Fortis, via regulated subsidiaries, holds a dominant position in these mandated build-outs, driving high growth: projected capex tied to MVPs is ~US$1.1–1.3bn annually through 2027, fueling future rate base expansion.

Electric Vehicle (EV) Infrastructure

Fortis is scaling EV charging and grid-readiness across its Canadian and Caribbean territories, targeting 4,000+ public chargers and ~C$150M in related capital through 2026 to capture rising demand.

Arizona Clean Energy Transition

Arizona Clean Energy Transition via Tucson Electric Power (Fortis) is shifting from coal to >1 GW solar plus 500 MWh storage, addressing Arizona’s 1.2% annual population growth and rising cooling demand; regulatory mandates (Arizona’s 2030 RPS-lean targets) create a high-growth market where Fortis holds ~60% regional utility share.

High capital expenditure (projects ~USD 800–1,000M through 2027) drives near-term cash outflow but, as assets reach commercial operation (2025–2028), expected regulated returns and declining O&M put this segment on track to become a stable cash generator by 2029.

- ~1 GW solar + 500 MWh storage

- ~60% regional market share

- Population growth ~1.2% annually

- Capex USD 800–1,000M (2023–2027)

- Stable cash generation target by 2029

Renewable Energy Storage Integration

Fortis’ battery storage projects, deployed across regulated utilities in Canada and the US, balance intermittent wind and solar and now represent ~15% of new capacity additions; Fortis reported C$220m invested in non-regulated renewables and storage in 2024, positioning these assets as Stars in the BCG matrix during a high-investment growth phase.

- High market share: leading regulated storage contracts in Ontario and BC

- High growth: grid-scale storage market CAGR ~20% (2024–30)

- Capex: C$220m in 2024; multi-year pipeline >C$1bn

- Goal: secure long-term dominance of dispatch services

Fortis growth surge: $4.5–5.5bn capex to 2027 fuels leading transmission, storage, renewables

Fortis’s Stars: ITC transmission, MVP-related capex, TEP clean transition and battery/storage show high market share in fast-growth grids; combined 2024–27 capex ~US$4.5–5.5bn (ITC+MVP+TEP+storage), 2024 invested C$220m in renewables/storage, projected regulated returns from 2025–2029 with stable cash generation by 2029.

| Asset | 2024–27 Capex | 2024 Invested | Market Share | Key metric |

|---|---|---|---|---|

| ITC/transmission | US$2.5–3.0bn | — | Leading | MVP enable ~30% more renewables by 2030 |

| TEP (AZ) | US$0.8–1.0bn | — | ~60% regional | ~1 GW solar +500 MWh storage |

| Storage/renewables | US$1.2–1.5bn pipeline | C$220m | Leading in ON/BC | Market CAGR ~20% (2024–30) |

What is included in the product

Comprehensive BCG Matrix review of Fortis Canada’s units with strategic actions for Stars, Cash Cows, Question Marks, and Dogs.

One-page Fortis BCG Matrix mapping units to quadrants for swift portfolio decisions, export-ready for PowerPoint.

Cash Cows

FortisBC Natural Gas Distribution

FortisBC Natural Gas Distribution holds ~85% household market share in British Columbia and serves ~1.1 million customers, in a low-growth market (~1% CAGR 2020–2025).

Regulated rates produce stable EBITDA margins (~45% in 2024) and predictable cash flow; capital expenditures are recovery-backed, keeping marketing spend minimal.

It generates ~C$400–450M annual free cash flow (2024), funding Fortis Inc.’s higher-growth utility investments and acquisitions.

FortisAlberta Electricity Distribution

FortisAlberta, operating in Alberta’s mature, highly regulated distribution market, holds roughly 60%+ service territory market share and delivers steady regulated returns; its network serves about 550,000 customers as of Dec 31, 2025.

Capital needs are maintenance-focused—annual sustaining capex ~CAD 120–140m in 2024–25—so free cash flow is stable and funds Fortis’s track record of 48 consecutive annual dividend increases through 2025.

Newfoundland Power Operations

Newfoundland Power, Fortis Inc.'s primary utility in Newfoundland and Labrador, is a textbook cash cow: ~95% residential market penetration and serving ~250,000 customers in a near-zero growth province.

Regulatory allowed return on equity averaged 9.5% (2019–2024), generating predictable EBITDA margins ~40% and annual dividends to Fortis of roughly CAD 150–200M in recent years.

Low customer churn and regulated rates mean minimal marketing spend; keeping infrastructure reliability (~SAIDI ~2.5 hours/year) preserves its leadership with little promotion.

Maritime Electric (PEI)

Maritime Electric (PEI) is Fortis’s captive monopoly on Prince Edward Island, serving ~78,000 customers and generating roughly CAD 150–160 million in annual revenue (2024), giving predictable cash flows for debt service and dividends.

With negligible geographic growth, management prioritizes cost efficiency, grid reliability, and modest rate-base investments to sustain ~8–10% regulated ROE and steady free cash extraction to Fortis.

- Customers: ~78,000 (2024)

- Revenue: CAD 150–160M (2024)

- Regulated ROE: ~8–10%

- Role: funds corporate debt service and supports Fortis portfolio

Caribbean Regulated Utilities

Fortis holds majority stakes in regulated utilities across the Caribbean (e.g., 90% in Caribbean Utilities Ltd. on Grand Cayman), often the primary provider, delivering stable, high-margin cash flows despite limited geographic expansion.

These mature island markets yield strong EBITDA margins (typically 25–35% reported in 2024 filings), providing roughly US$150–220m annual free cash flow to Fortis and bolstering dividend coverage and resilience to North American cyclicality.

- High market share: monopoly/primary provider on several islands

- Mature markets: limited growth but 25–35% EBITDA margins (2024)

- Cash contribution: ~US$150–220m FCF to Fortis (2024)

- Diversification: non-continental cash flows support dividend safety

Fortis’s regulated utilities: C$900–1,100M FCF in 2024 — stable dividends, steady ROE

Fortis’s cash cows are regulated utilities (FortisBC Gas, FortisAlberta, Newfoundland Power, Maritime Electric, Caribbean holdings) delivering stable cash flow: combined FCF ~C$900–1,100M (2024), regulated ROE ~8–9.5%, EBITDA margins 25–45%, customer base ~2.27M; funds dividends and higher-growth investments.

| Asset | Customers | FCF 2024 | ROE | EBITDA% |

|---|---|---|---|---|

| FortisBC Gas | 1.1M | C$400–450M | — | ~45% |

| FortisAlberta | 550k | C$120–140M | ~8–9% | ~40% |

| Newfoundland Power | 250k | C$150–200M | ~9.5% | ~40% |

| Maritime Electric | 78k | C$20–30M | ~8–10% | ~30% |

| Caribbean | various | US$150–220M | ~8–10% | 25–35% |

Delivered as Shown

Fortis (Canada) BCG Matrix

The file you're previewing on this page is the final Fortis (Canada) BCG Matrix you'll receive after purchase—no watermarks, no demo content—just a fully formatted, ready-to-use strategic report tailored to Fortis's market position.

This preview reflects the exact same analysis-ready BCG Matrix you'll download post-purchase, combining market-backed insights and clear quadrant placement for informed portfolio decisions.

What you see is the actual document that becomes yours upon payment, immediately available for editing, printing, or presenting to stakeholders.

You're previewing the real Fortis (Canada) BCG Matrix report—professionally designed for integration into business plans, investor decks, or strategic reviews without further revisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

Fortis (Canada) sits at an intriguing crossroads—regulated utility stability meets selective growth opportunities, with legacy assets behaving like Cash Cows while emerging renewable projects look and feel like potential Stars. Our preview hints at where capital is earning steady returns versus where strategic investment could accelerate market share. Purchase the full BCG Matrix for quadrant-by-quadrant placement, actionable recommendations, and downloadable Word + Excel files to guide confident investment and portfolio decisions.

Stars

ITC Holdings Transmission Expansion

ITC Holdings, the largest independent U.S. transmission owner, sits in Fortis’s BCG matrix as a star: high market share in a high-growth market driven by grid modernization; U.S. transmission investments reached about $3.5 billion in 2024, with ITC contributing materially.

The U.S. needs roughly $120–200 billion in new long-distance lines by 2035 to link wind and solar hubs to cities; Fortis has committed multi-billion-dollar capital allocations to ITC expansion through 2025–2027 to capture this demand.

Multi-Value Project (MVP) Pipelines

Multi-Value Project (MVP) Pipelines are large regional transmission builds across the MISO footprint that boost grid reliability and cut emissions; MISO estimates these projects enable ~30% more renewable integration by 2030.

Fortis, via regulated subsidiaries, holds a dominant position in these mandated build-outs, driving high growth: projected capex tied to MVPs is ~US$1.1–1.3bn annually through 2027, fueling future rate base expansion.

Electric Vehicle (EV) Infrastructure

Fortis is scaling EV charging and grid-readiness across its Canadian and Caribbean territories, targeting 4,000+ public chargers and ~C$150M in related capital through 2026 to capture rising demand.

Arizona Clean Energy Transition

Arizona Clean Energy Transition via Tucson Electric Power (Fortis) is shifting from coal to >1 GW solar plus 500 MWh storage, addressing Arizona’s 1.2% annual population growth and rising cooling demand; regulatory mandates (Arizona’s 2030 RPS-lean targets) create a high-growth market where Fortis holds ~60% regional utility share.

High capital expenditure (projects ~USD 800–1,000M through 2027) drives near-term cash outflow but, as assets reach commercial operation (2025–2028), expected regulated returns and declining O&M put this segment on track to become a stable cash generator by 2029.

- ~1 GW solar + 500 MWh storage

- ~60% regional market share

- Population growth ~1.2% annually

- Capex USD 800–1,000M (2023–2027)

- Stable cash generation target by 2029

Renewable Energy Storage Integration

Fortis’ battery storage projects, deployed across regulated utilities in Canada and the US, balance intermittent wind and solar and now represent ~15% of new capacity additions; Fortis reported C$220m invested in non-regulated renewables and storage in 2024, positioning these assets as Stars in the BCG matrix during a high-investment growth phase.

- High market share: leading regulated storage contracts in Ontario and BC

- High growth: grid-scale storage market CAGR ~20% (2024–30)

- Capex: C$220m in 2024; multi-year pipeline >C$1bn

- Goal: secure long-term dominance of dispatch services

Fortis growth surge: $4.5–5.5bn capex to 2027 fuels leading transmission, storage, renewables

Fortis’s Stars: ITC transmission, MVP-related capex, TEP clean transition and battery/storage show high market share in fast-growth grids; combined 2024–27 capex ~US$4.5–5.5bn (ITC+MVP+TEP+storage), 2024 invested C$220m in renewables/storage, projected regulated returns from 2025–2029 with stable cash generation by 2029.

| Asset | 2024–27 Capex | 2024 Invested | Market Share | Key metric |

|---|---|---|---|---|

| ITC/transmission | US$2.5–3.0bn | — | Leading | MVP enable ~30% more renewables by 2030 |

| TEP (AZ) | US$0.8–1.0bn | — | ~60% regional | ~1 GW solar +500 MWh storage |

| Storage/renewables | US$1.2–1.5bn pipeline | C$220m | Leading in ON/BC | Market CAGR ~20% (2024–30) |

What is included in the product

Comprehensive BCG Matrix review of Fortis Canada’s units with strategic actions for Stars, Cash Cows, Question Marks, and Dogs.

One-page Fortis BCG Matrix mapping units to quadrants for swift portfolio decisions, export-ready for PowerPoint.

Cash Cows

FortisBC Natural Gas Distribution

FortisBC Natural Gas Distribution holds ~85% household market share in British Columbia and serves ~1.1 million customers, in a low-growth market (~1% CAGR 2020–2025).

Regulated rates produce stable EBITDA margins (~45% in 2024) and predictable cash flow; capital expenditures are recovery-backed, keeping marketing spend minimal.

It generates ~C$400–450M annual free cash flow (2024), funding Fortis Inc.’s higher-growth utility investments and acquisitions.

FortisAlberta Electricity Distribution

FortisAlberta, operating in Alberta’s mature, highly regulated distribution market, holds roughly 60%+ service territory market share and delivers steady regulated returns; its network serves about 550,000 customers as of Dec 31, 2025.

Capital needs are maintenance-focused—annual sustaining capex ~CAD 120–140m in 2024–25—so free cash flow is stable and funds Fortis’s track record of 48 consecutive annual dividend increases through 2025.

Newfoundland Power Operations

Newfoundland Power, Fortis Inc.'s primary utility in Newfoundland and Labrador, is a textbook cash cow: ~95% residential market penetration and serving ~250,000 customers in a near-zero growth province.

Regulatory allowed return on equity averaged 9.5% (2019–2024), generating predictable EBITDA margins ~40% and annual dividends to Fortis of roughly CAD 150–200M in recent years.

Low customer churn and regulated rates mean minimal marketing spend; keeping infrastructure reliability (~SAIDI ~2.5 hours/year) preserves its leadership with little promotion.

Maritime Electric (PEI)

Maritime Electric (PEI) is Fortis’s captive monopoly on Prince Edward Island, serving ~78,000 customers and generating roughly CAD 150–160 million in annual revenue (2024), giving predictable cash flows for debt service and dividends.

With negligible geographic growth, management prioritizes cost efficiency, grid reliability, and modest rate-base investments to sustain ~8–10% regulated ROE and steady free cash extraction to Fortis.

- Customers: ~78,000 (2024)

- Revenue: CAD 150–160M (2024)

- Regulated ROE: ~8–10%

- Role: funds corporate debt service and supports Fortis portfolio

Caribbean Regulated Utilities

Fortis holds majority stakes in regulated utilities across the Caribbean (e.g., 90% in Caribbean Utilities Ltd. on Grand Cayman), often the primary provider, delivering stable, high-margin cash flows despite limited geographic expansion.

These mature island markets yield strong EBITDA margins (typically 25–35% reported in 2024 filings), providing roughly US$150–220m annual free cash flow to Fortis and bolstering dividend coverage and resilience to North American cyclicality.

- High market share: monopoly/primary provider on several islands

- Mature markets: limited growth but 25–35% EBITDA margins (2024)

- Cash contribution: ~US$150–220m FCF to Fortis (2024)

- Diversification: non-continental cash flows support dividend safety

Fortis’s regulated utilities: C$900–1,100M FCF in 2024 — stable dividends, steady ROE

Fortis’s cash cows are regulated utilities (FortisBC Gas, FortisAlberta, Newfoundland Power, Maritime Electric, Caribbean holdings) delivering stable cash flow: combined FCF ~C$900–1,100M (2024), regulated ROE ~8–9.5%, EBITDA margins 25–45%, customer base ~2.27M; funds dividends and higher-growth investments.

| Asset | Customers | FCF 2024 | ROE | EBITDA% |

|---|---|---|---|---|

| FortisBC Gas | 1.1M | C$400–450M | — | ~45% |

| FortisAlberta | 550k | C$120–140M | ~8–9% | ~40% |

| Newfoundland Power | 250k | C$150–200M | ~9.5% | ~40% |

| Maritime Electric | 78k | C$20–30M | ~8–10% | ~30% |

| Caribbean | various | US$150–220M | ~8–10% | 25–35% |

Delivered as Shown

Fortis (Canada) BCG Matrix

The file you're previewing on this page is the final Fortis (Canada) BCG Matrix you'll receive after purchase—no watermarks, no demo content—just a fully formatted, ready-to-use strategic report tailored to Fortis's market position.

This preview reflects the exact same analysis-ready BCG Matrix you'll download post-purchase, combining market-backed insights and clear quadrant placement for informed portfolio decisions.

What you see is the actual document that becomes yours upon payment, immediately available for editing, printing, or presenting to stakeholders.

You're previewing the real Fortis (Canada) BCG Matrix report—professionally designed for integration into business plans, investor decks, or strategic reviews without further revisions.