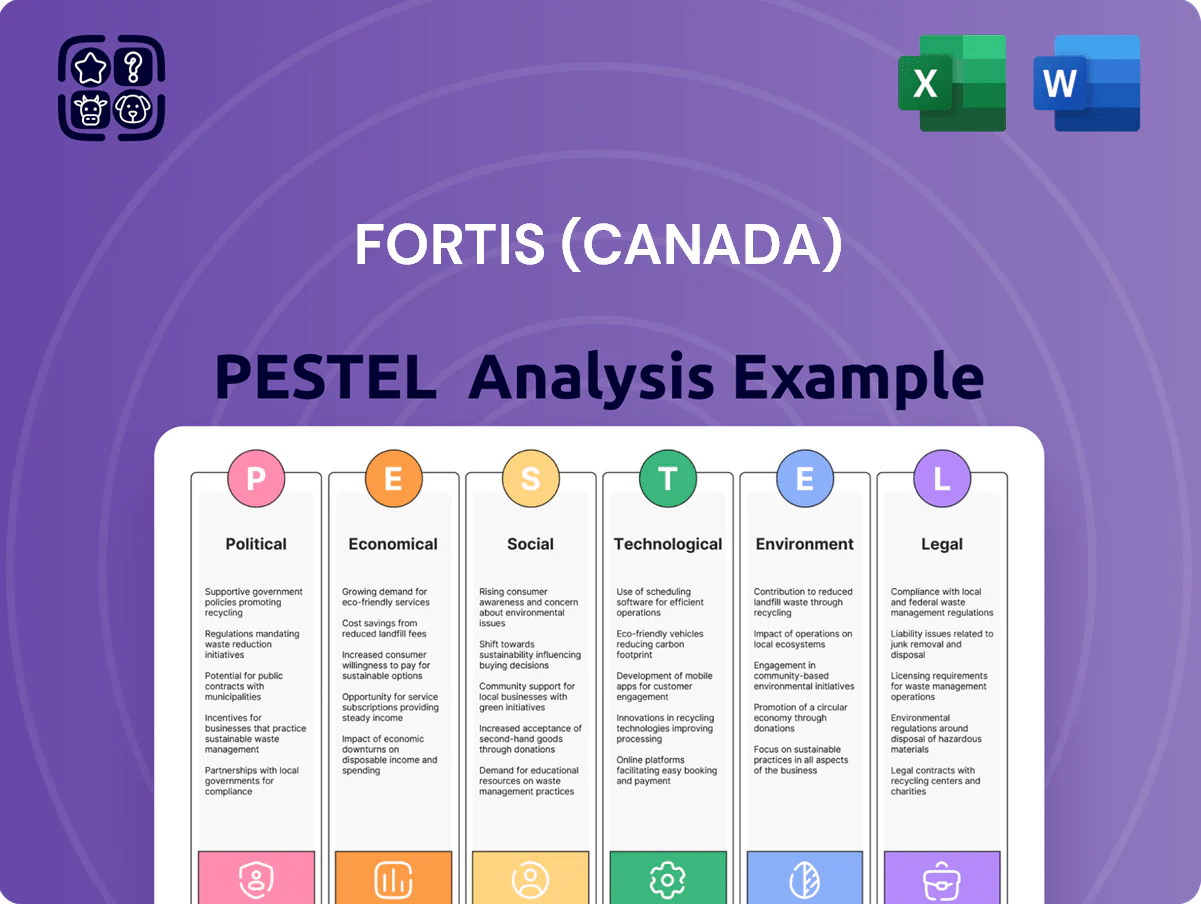

Fortis (Canada) PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Gain a strategic edge with our PESTLE Analysis of Fortis (Canada): uncover how regulatory shifts, economic trends, technological advances, social expectations, and environmental pressures shape its utilities operations—ideal for investors and strategists. Buy the full, ready-to-use report for actionable insights, downloadable Word/Excel files, and the clarity you need to make confident decisions.

Political factors

Federal Carbon Pricing Policies

The federal carbon tax rising from CAD 65/tonne in 2023 to CAD 170/tonne by 2030, with step increases through 2025 (CAD 95/tonne in 2024, CAD 115/tonne in 2025), forces Fortis to adjust natural gas tariffs to pass costs while investing in efficiency programs; this political pressure accelerates adoption of electrification and low-carbon heating, reshaping pipeline investment and long-term capex planning for the utility.

Cross-Border Energy Regulations

Fortis operates major utility assets across Canada and the U.S., exposing it to shifts in bilateral trade agreements and energy export policies that affected cross-border flows valued at roughly CAD 10–15 billion annually in 2024.

Political moves in Washington or Ottawa promoting North American energy independence could change permitting and tariff frameworks, impacting planned transmission investments of ITC Holdings, which reported US regulated assets of about $18.5 billion in 2024.

Maintaining compliance with the Federal Energy Regulatory Commission remains a priority for ITC, given FERC’s influence over regional transmission rates and recent 2023–2024 rulemakings that altered cost recovery and interconnection processes.

Indigenous Consultation and Reconciliation

In Canada, political emphasis on Indigenous rights and the Duty to Consult materially affects Fortis’ timeline for transmission and generation projects; federal and provincial decisions increasingly require documented consultation and benefit-sharing, with Indigenous equity stakes in energy projects rising—Indigenous partnerships accounted for about CAD 1.4 billion in announced clean-energy investments in 2024—failure to meet these expectations has stalled projects, risking months-to-years delays or cancellations and material capital write-offs.

Government Green Energy Subsidies

Federal and provincial grants and tax credits—including Canada’s Investment Tax Credit for CCUS and clean electricity (up to 30%) and BC/Alberta provincial incentives—directly affect Fortis Inc.'s CAD billions in planned capex through 2026, improving project NPV and IRR and enabling faster replacement of fossil assets.

Political moves to extend or sunset incentives (e.g., expiry risks post-2025 policies) materially change asset retirement timelines and stranded-asset risk, affecting shareholder returns and ratebase forecasts.

Subsidies help keep customer rates affordable while meeting provincial decarbonization targets (Net-zero by 2050 trajectories and 2035 electrification goals), lowering incremental subsidy needs per tonne CO2 avoided.

- ITC up to 30% increases project viability

- Expiry risk alters retirement schedules and stranded-asset exposure

- Supports ratepayer affordability vs. decarbonization costs

Geopolitical Energy Security

Global instability has pushed North American policy toward energy security and grid reliability; Canada’s 2024 National Cyber Security Strategy increased funding by CAD 1.6bn, signaling higher expectations for utilities like Fortis to bolster defenses.

Governments now prioritize protecting critical infrastructure from foreign interference and physical threats, with federal grants covering up to 50% of hardening projects in 2023–25 programs.

Fortis must align investments with national security priorities, implying higher capital expenditure on grid hardening and diversified generation—Fortis’s 2024 capital plan of ~CAD 2.7bn will likely tilt toward resilience projects.

- CAD 1.6bn federal cyber funding (2024)

- Up to 50% grant coverage for hardening projects

- Fortis 2024 capex ~CAD 2.7bn

Policy shifts reshape Fortis: higher carbon costs, incentives, and Indigenous risks

Political shifts — rising federal carbon price to CAD 170/t by 2030, CAD 1.6bn cyber funding (2024), up to 30% federal ITC for clean projects, and grants covering up to 50% of hardening works — materially reshape Fortis’s CAD 2.7bn 2024 capex, alter ratebase and stranded-asset risk, and increase Indigenous consultation/benefit-share requirements tied to ~CAD 1.4bn Indigenous clean-energy commitments (2024).

| Item | 2024–25 Metric |

|---|---|

| Federal carbon price | CAD 65/t (2023) → CAD 95 (2024) → CAD 115 (2025) |

| Cyber funding | CAD 1.6bn |

| Fortis capex | ~CAD 2.7bn (2024) |

| ITC / grants | Up to 30% / up to 50% coverage |

| Indigenous investments | ~CAD 1.4bn (2024) |

What is included in the product

Explores how macro-environmental forces uniquely affect Fortis (Canada) across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants and investors identify risks, opportunities and actionable strategies for regulatory, market and climate-driven transitions.

A concise Fortis (Canada) PESTLE summary that eases stakeholder briefings by distilling regulatory, economic, social, technological, environmental, and legal factors into a single slide-ready snapshot for quick decision-making.

Economic factors

Interest Rate Volatility

As a capital-intensive utility, Fortis is highly sensitive to borrowing costs; with Canadian 5-year government bond yields rising from ~1.0% in 2021 to ~3.8% by end-2024, higher rates through 2025 raise debt-servicing on Fortis’s ~CDN$25–30 billion capital program, increasing interest expense materially.

Managing this pressure requires tight balance-sheet control to preserve investment-grade ratings (S&P BBB+/A- outlooks historically) and protect dividend yields, which averaged ~3.5% in 2024, amid upward financing costs.

Inflationary Pressure on Operations

Persistent inflation in Canada (CPI 2024 ~3.4% year-over-year) is raising costs for specialized labor, copper (LME copper up ~12% in 2024) and steel, increasing Fortis’s grid maintenance expenses; the company reported 2024 operating cost pressure and sought regulatory rate applications to recover roughly CAD 200–300 million in incremental costs. If inflation exceeds approved rate hikes, Fortis’s adjusted EBITDA margin and capex funding could be temporarily compressed.

Currency Exchange Fluctuations

Regional Economic Growth Trends

The demand for electricity and gas for Fortis in Arizona, New York and British Columbia correlates with regional GDP and employment; Arizona's metro Phoenix GDP grew ~3.1% in 2024, New York State ~1.8% and British Columbia ~2.4%, driving higher residential connections and commercial usage.

Economic downturns cut industrial load and slow customer additions—US industrial consumption fell 1.2% in a 2024 contraction scenario—pressuring near-term rate base growth.

Strong local expansion boosts capital spending needs: Fortis reported capital additions of CAD 1.9bn in 2024, supporting future rate base increases as new infrastructure is required.

- Regional GDP: AZ 3.1% (2024), NY 1.8% (2024), BC 2.4% (2024)

- Industrial demand sensitivity: example -1.2% consumption in downturns (2024 scenario)

- Fortis 2024 capital additions: CAD 1.9bn supporting rate base growth

Capital Expenditure Financing

Fortis has a multiyear CAD 12–13 billion capital plan through 2028–2030 to modernize grids and shift to cleaner generation; access to equity and debt at low rates is essential to fund projects without pushing debt/EBITDA beyond credit thresholds.

Economic stability and investor confidence in utilities—reflected in Fortis’s investment-grade ratings (BBB/Baa2 as of 2025) and ~3.5%–4.0% long-term bond yields—support favorable financing conditions.

- CAD 12–13bn capex plan through 2028–30

- Maintains investment-grade ratings (BBB/Baa2 in 2025)

- Target to avoid excessive leverage (debt/EBITDA covenants)

- Reliant on ~3.5%–4.0% market yields for low-cost debt

Higher rates, FX swings and big capex strain Fortis’s credit and EPS outlook

Rising rates (CA 5y ~3.8% end-2024) and CAD-USD swings hurt Fortis’s debt servicing and reported EPS; 2024 capex CAD1.9bn within a CAD12–13bn plan through 2028–30 elevates funding needs; 2024 CPI ~3.4% and commodity inflation pushed ~CAD200–300m recovery requests; ~40% 2024 earnings from U.S. ops increases FX exposure; investment-grade ratings (BBB/Baa2 in 2025) remain key to low-cost financing.

| Metric | 2024/2025 |

|---|---|

| CA 5y yield | ~3.8% |

| CPI (Canada) | ~3.4% y/y (2024) |

| Capex (2024) | CAD1.9bn |

| Capex plan | CAD12–13bn (2028–30) |

| USD earnings share | ~40% (2024) |

| Ratings | BBB/Baa2 (2025) |

What You See Is What You Get

Fortis (Canada) PESTLE Analysis

The preview shown here is the exact Fortis (Canada) PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Gain a strategic edge with our PESTLE Analysis of Fortis (Canada): uncover how regulatory shifts, economic trends, technological advances, social expectations, and environmental pressures shape its utilities operations—ideal for investors and strategists. Buy the full, ready-to-use report for actionable insights, downloadable Word/Excel files, and the clarity you need to make confident decisions.

Political factors

Federal Carbon Pricing Policies

The federal carbon tax rising from CAD 65/tonne in 2023 to CAD 170/tonne by 2030, with step increases through 2025 (CAD 95/tonne in 2024, CAD 115/tonne in 2025), forces Fortis to adjust natural gas tariffs to pass costs while investing in efficiency programs; this political pressure accelerates adoption of electrification and low-carbon heating, reshaping pipeline investment and long-term capex planning for the utility.

Cross-Border Energy Regulations

Fortis operates major utility assets across Canada and the U.S., exposing it to shifts in bilateral trade agreements and energy export policies that affected cross-border flows valued at roughly CAD 10–15 billion annually in 2024.

Political moves in Washington or Ottawa promoting North American energy independence could change permitting and tariff frameworks, impacting planned transmission investments of ITC Holdings, which reported US regulated assets of about $18.5 billion in 2024.

Maintaining compliance with the Federal Energy Regulatory Commission remains a priority for ITC, given FERC’s influence over regional transmission rates and recent 2023–2024 rulemakings that altered cost recovery and interconnection processes.

Indigenous Consultation and Reconciliation

In Canada, political emphasis on Indigenous rights and the Duty to Consult materially affects Fortis’ timeline for transmission and generation projects; federal and provincial decisions increasingly require documented consultation and benefit-sharing, with Indigenous equity stakes in energy projects rising—Indigenous partnerships accounted for about CAD 1.4 billion in announced clean-energy investments in 2024—failure to meet these expectations has stalled projects, risking months-to-years delays or cancellations and material capital write-offs.

Government Green Energy Subsidies

Federal and provincial grants and tax credits—including Canada’s Investment Tax Credit for CCUS and clean electricity (up to 30%) and BC/Alberta provincial incentives—directly affect Fortis Inc.'s CAD billions in planned capex through 2026, improving project NPV and IRR and enabling faster replacement of fossil assets.

Political moves to extend or sunset incentives (e.g., expiry risks post-2025 policies) materially change asset retirement timelines and stranded-asset risk, affecting shareholder returns and ratebase forecasts.

Subsidies help keep customer rates affordable while meeting provincial decarbonization targets (Net-zero by 2050 trajectories and 2035 electrification goals), lowering incremental subsidy needs per tonne CO2 avoided.

- ITC up to 30% increases project viability

- Expiry risk alters retirement schedules and stranded-asset exposure

- Supports ratepayer affordability vs. decarbonization costs

Geopolitical Energy Security

Global instability has pushed North American policy toward energy security and grid reliability; Canada’s 2024 National Cyber Security Strategy increased funding by CAD 1.6bn, signaling higher expectations for utilities like Fortis to bolster defenses.

Governments now prioritize protecting critical infrastructure from foreign interference and physical threats, with federal grants covering up to 50% of hardening projects in 2023–25 programs.

Fortis must align investments with national security priorities, implying higher capital expenditure on grid hardening and diversified generation—Fortis’s 2024 capital plan of ~CAD 2.7bn will likely tilt toward resilience projects.

- CAD 1.6bn federal cyber funding (2024)

- Up to 50% grant coverage for hardening projects

- Fortis 2024 capex ~CAD 2.7bn

Policy shifts reshape Fortis: higher carbon costs, incentives, and Indigenous risks

Political shifts — rising federal carbon price to CAD 170/t by 2030, CAD 1.6bn cyber funding (2024), up to 30% federal ITC for clean projects, and grants covering up to 50% of hardening works — materially reshape Fortis’s CAD 2.7bn 2024 capex, alter ratebase and stranded-asset risk, and increase Indigenous consultation/benefit-share requirements tied to ~CAD 1.4bn Indigenous clean-energy commitments (2024).

| Item | 2024–25 Metric |

|---|---|

| Federal carbon price | CAD 65/t (2023) → CAD 95 (2024) → CAD 115 (2025) |

| Cyber funding | CAD 1.6bn |

| Fortis capex | ~CAD 2.7bn (2024) |

| ITC / grants | Up to 30% / up to 50% coverage |

| Indigenous investments | ~CAD 1.4bn (2024) |

What is included in the product

Explores how macro-environmental forces uniquely affect Fortis (Canada) across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants and investors identify risks, opportunities and actionable strategies for regulatory, market and climate-driven transitions.

A concise Fortis (Canada) PESTLE summary that eases stakeholder briefings by distilling regulatory, economic, social, technological, environmental, and legal factors into a single slide-ready snapshot for quick decision-making.

Economic factors

Interest Rate Volatility

As a capital-intensive utility, Fortis is highly sensitive to borrowing costs; with Canadian 5-year government bond yields rising from ~1.0% in 2021 to ~3.8% by end-2024, higher rates through 2025 raise debt-servicing on Fortis’s ~CDN$25–30 billion capital program, increasing interest expense materially.

Managing this pressure requires tight balance-sheet control to preserve investment-grade ratings (S&P BBB+/A- outlooks historically) and protect dividend yields, which averaged ~3.5% in 2024, amid upward financing costs.

Inflationary Pressure on Operations

Persistent inflation in Canada (CPI 2024 ~3.4% year-over-year) is raising costs for specialized labor, copper (LME copper up ~12% in 2024) and steel, increasing Fortis’s grid maintenance expenses; the company reported 2024 operating cost pressure and sought regulatory rate applications to recover roughly CAD 200–300 million in incremental costs. If inflation exceeds approved rate hikes, Fortis’s adjusted EBITDA margin and capex funding could be temporarily compressed.

Currency Exchange Fluctuations

Regional Economic Growth Trends

The demand for electricity and gas for Fortis in Arizona, New York and British Columbia correlates with regional GDP and employment; Arizona's metro Phoenix GDP grew ~3.1% in 2024, New York State ~1.8% and British Columbia ~2.4%, driving higher residential connections and commercial usage.

Economic downturns cut industrial load and slow customer additions—US industrial consumption fell 1.2% in a 2024 contraction scenario—pressuring near-term rate base growth.

Strong local expansion boosts capital spending needs: Fortis reported capital additions of CAD 1.9bn in 2024, supporting future rate base increases as new infrastructure is required.

- Regional GDP: AZ 3.1% (2024), NY 1.8% (2024), BC 2.4% (2024)

- Industrial demand sensitivity: example -1.2% consumption in downturns (2024 scenario)

- Fortis 2024 capital additions: CAD 1.9bn supporting rate base growth

Capital Expenditure Financing

Fortis has a multiyear CAD 12–13 billion capital plan through 2028–2030 to modernize grids and shift to cleaner generation; access to equity and debt at low rates is essential to fund projects without pushing debt/EBITDA beyond credit thresholds.

Economic stability and investor confidence in utilities—reflected in Fortis’s investment-grade ratings (BBB/Baa2 as of 2025) and ~3.5%–4.0% long-term bond yields—support favorable financing conditions.

- CAD 12–13bn capex plan through 2028–30

- Maintains investment-grade ratings (BBB/Baa2 in 2025)

- Target to avoid excessive leverage (debt/EBITDA covenants)

- Reliant on ~3.5%–4.0% market yields for low-cost debt

Higher rates, FX swings and big capex strain Fortis’s credit and EPS outlook

Rising rates (CA 5y ~3.8% end-2024) and CAD-USD swings hurt Fortis’s debt servicing and reported EPS; 2024 capex CAD1.9bn within a CAD12–13bn plan through 2028–30 elevates funding needs; 2024 CPI ~3.4% and commodity inflation pushed ~CAD200–300m recovery requests; ~40% 2024 earnings from U.S. ops increases FX exposure; investment-grade ratings (BBB/Baa2 in 2025) remain key to low-cost financing.

| Metric | 2024/2025 |

|---|---|

| CA 5y yield | ~3.8% |

| CPI (Canada) | ~3.4% y/y (2024) |

| Capex (2024) | CAD1.9bn |

| Capex plan | CAD12–13bn (2028–30) |

| USD earnings share | ~40% (2024) |

| Ratings | BBB/Baa2 (2025) |

What You See Is What You Get

Fortis (Canada) PESTLE Analysis

The preview shown here is the exact Fortis (Canada) PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.