Foxlink Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Foxlink faces moderate supplier leverage, intense rivalry in electronics manufacturing, and evolving buyer demands that pressure margins while scale and IP offer defensive moats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Foxlink’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility in raw material pricing

The manufacturing of connectors and cable assemblies relies on copper, gold, and engineered plastics; late-2025 commodity swings—copper up ~35% year-on-year to about $10,500/ton and gold up ~8% to ~$2,100/oz—push Foxlink’s input costs and trim margins (gross margin pressure of ~2–4 percentage points in 2024–25 industry reports). Individual suppliers hold limited bargaining power due to commodity standardization, but collective market moves risk production stability and working-capital strain.

Dependence on specialized semiconductor providers

Foxlink relies on a small set of advanced semiconductor vendors for power-management ICs and SoCs, giving suppliers strong leverage; in 2024 the global fabless/foundry concentration left ~70% of high-performance nodes controlled by three players, raising switching costs. Any constraint—like the 2021–24 capacity tightness that pushed lead times beyond 20 weeks—can delay Foxlink’s high-end module shipments and squeeze margins.

Geographical concentration of component vendors

A significant share of Foxlink’s components—about 68% by volume as of 2025—originates from Taiwan and Southeast Asian hubs, so regional slowdowns or China-Taiwan tensions could quickly raise costs and delay shipments. Suppliers in these hubs show correlated pricing and face common regulatory headwinds, restricting Foxlink’s bargaining leverage and keeping average lead times near 45 days despite diversification efforts.

Energy and utility cost sensitivity

Precision manufacturing at Foxlink uses high-energy tooling and molding, making the firm highly exposed to regional utility rates and policies; industrial power/water suppliers often act as local monopolies, limiting Foxlink’s negotiation leverage.

By 2025 rising energy prices (global industrial electricity up ~18% 2021–25) pushed Foxlink to spend on efficiency—LED, variable-speed drives, CHP—to protect margins against supplier bargaining power.

- Energy intensity: high for tooling/molding

- Supplier concentration: local monopolies/oligopolies

- 2021–25 industrial electricity +18% (global)

- CapEx on efficiency risen to defend margins

Switching costs for precision machinery

High-end molding and assembly machines for Foxlink are proprietary and supplied by a few global firms, so switching vendors typically means capex of $5–20M per factory and 4–12 weeks downtime for retraining and recalibration.

That creates multi-year vendor dependency for parts, maintenance, and software updates; OEM service contracts can be 5–10% of machine value annually, raising supplier bargaining power.

- Capex $5–20M per line

- Downtime 4–12 weeks

- OEM service 5–10%/yr

Supplier squeeze: cheap commodities vs. costly semiconductors, CAPEX and utility pressure

Suppliers wield mixed power: commodity inputs (copper, gold, plastics) are low-priced and replaceable, but semiconductor ICs, high-end molding machines, and local utilities create pockets of strong leverage that can raise costs, delay shipments, and force Foxlink into multi‑million CAPEX or service contracts (capex $5–20M/line; OEM service 5–10%/yr).

| Item | 2021–25/2025 |

|---|---|

| Copper price | $10,500/ton (+35% YoY late‑2025) |

| Gold price | $2,100/oz (+8% YoY) |

| High‑end node control | ~70% by 3 firms (2024) |

| Avg lead time | ~45 days |

| Industrial electricity change | +18% (2021–25) |

What is included in the product

Tailored Porter's Five Forces analysis for Foxlink that uncovers key competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive forces and strategic defense points to inform investor presentations and internal strategy.

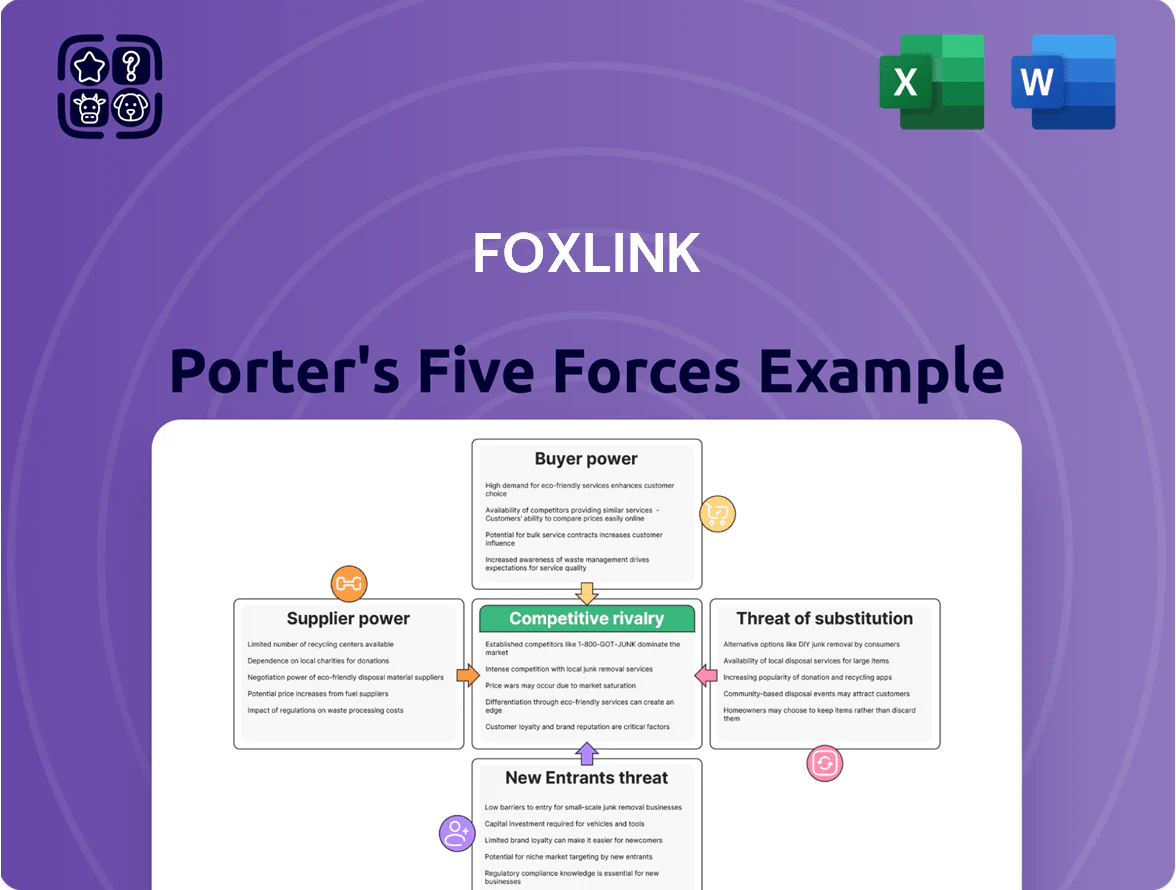

One-sheet Porter's Five Forces for Foxlink—visualize supplier, buyer, rivalry, entry, and substitute pressures at a glance to speed strategic decisions.

Customers Bargaining Power

High concentration of revenue from tech giants

Foxlink derives roughly 55–70% of revenue from a handful of tech giants, so a few OEMs wield strong leverage to push down unit prices and extract extended payment terms; in 2024 one top client accounted for about 22% of sales.

Stringent quality and sustainability requirements

Major automotive and industrial clients enforce ISO/TS 16949/ IATF 16949 quality and strict ESG rules; by 2025, 62% of Tier 1 buyers require verifiable low-carbon footprints and 48% demand supplier audits without paying premiums. These buyers leverage scale—top 5 customers account for ~41% of Foxlink revenue—so Foxlink must absorb capex for green processes to stay preferred, giving customers de facto control over production standards.

Low switching costs for standardized components

Many Foxlink connectors follow industry standards, so buyers face low switching costs and can shift to rivals like Luxshare or Foxconn—both of which reported combined 2024 connector revenues north of $10bn—during procurement rounds; this buyer leverage compresses margins. Customers routinely use multi-sourcing to force price cuts, so Foxlink must either cut costs (2024 gross margin 13.5%) or innovate to protect wallet share.

Backward integration threats from large OEMs

Large OEMs like Apple and Samsung, which accounted for roughly 35–45% of Foxlink’s revenue in 2024, have the cash and IP to insource connectors or power modules, posing a real backward-integration threat that can erode Foxlink’s volumes.

That latent risk tightens Foxlink’s margins during renewals: buyers use insourcing credibility to cap price increases, press for longer payment terms, and demand more customization at lower unit prices.

- Apple, Samsung scale: high insourcing capacity

- 2024 revenue exposure ~35–45%

- Limits price hikes and boosts negotiation leverage

- Raises need for product differentiation and sticky services

Demand for integrated solution capabilities

Modern buyers want end-to-end services—from design to final assembly—so Foxlink must expand capabilities and take on more operational risk and capex to meet demand.

This integration trend lets customers demand bundled pricing; in 2024 OEM contracts showed 5–12% lower unit margins on bundled deals versus standalone components.

Bundling pressure compresses product-line margins and forces Foxlink to weigh higher revenue against thinner EBITDA per unit.

- Higher capex and operating risk

- 5–12% lower margins on bundled deals (2024)

- Increased buyer leverage on pricing

Buyers Dominate: Top Clients Drive Price Pressure, Margin Hit & Costly ESG Capex

Buyers hold strong leverage: top 5 customers ≈41% revenue, one client ~22% in 2024, and Apple/Samsung together ~35–45% in 2024, enabling price pressure, longer payment terms, and insourcing threats that compress Foxlink’s 2024 gross margin of 13.5% and force capex for green/ESG compliance.

| Metric | Value |

|---|---|

| Top-5 customer share | ~41% |

| Largest single client (2024) | ~22% |

| Apple+Samsung exposure (2024) | 35–45% |

| Gross margin (2024) | 13.5% |

| Bundled-deal margin hit (2024) | −5–12% |

What You See Is What You Get

Foxlink Porter's Five Forces Analysis

This preview shows the exact Foxlink Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or sample excerpts—fully formatted, professionally written, and ready for download and use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Foxlink faces moderate supplier leverage, intense rivalry in electronics manufacturing, and evolving buyer demands that pressure margins while scale and IP offer defensive moats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Foxlink’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility in raw material pricing

The manufacturing of connectors and cable assemblies relies on copper, gold, and engineered plastics; late-2025 commodity swings—copper up ~35% year-on-year to about $10,500/ton and gold up ~8% to ~$2,100/oz—push Foxlink’s input costs and trim margins (gross margin pressure of ~2–4 percentage points in 2024–25 industry reports). Individual suppliers hold limited bargaining power due to commodity standardization, but collective market moves risk production stability and working-capital strain.

Dependence on specialized semiconductor providers

Foxlink relies on a small set of advanced semiconductor vendors for power-management ICs and SoCs, giving suppliers strong leverage; in 2024 the global fabless/foundry concentration left ~70% of high-performance nodes controlled by three players, raising switching costs. Any constraint—like the 2021–24 capacity tightness that pushed lead times beyond 20 weeks—can delay Foxlink’s high-end module shipments and squeeze margins.

Geographical concentration of component vendors

A significant share of Foxlink’s components—about 68% by volume as of 2025—originates from Taiwan and Southeast Asian hubs, so regional slowdowns or China-Taiwan tensions could quickly raise costs and delay shipments. Suppliers in these hubs show correlated pricing and face common regulatory headwinds, restricting Foxlink’s bargaining leverage and keeping average lead times near 45 days despite diversification efforts.

Energy and utility cost sensitivity

Precision manufacturing at Foxlink uses high-energy tooling and molding, making the firm highly exposed to regional utility rates and policies; industrial power/water suppliers often act as local monopolies, limiting Foxlink’s negotiation leverage.

By 2025 rising energy prices (global industrial electricity up ~18% 2021–25) pushed Foxlink to spend on efficiency—LED, variable-speed drives, CHP—to protect margins against supplier bargaining power.

- Energy intensity: high for tooling/molding

- Supplier concentration: local monopolies/oligopolies

- 2021–25 industrial electricity +18% (global)

- CapEx on efficiency risen to defend margins

Switching costs for precision machinery

High-end molding and assembly machines for Foxlink are proprietary and supplied by a few global firms, so switching vendors typically means capex of $5–20M per factory and 4–12 weeks downtime for retraining and recalibration.

That creates multi-year vendor dependency for parts, maintenance, and software updates; OEM service contracts can be 5–10% of machine value annually, raising supplier bargaining power.

- Capex $5–20M per line

- Downtime 4–12 weeks

- OEM service 5–10%/yr

Supplier squeeze: cheap commodities vs. costly semiconductors, CAPEX and utility pressure

Suppliers wield mixed power: commodity inputs (copper, gold, plastics) are low-priced and replaceable, but semiconductor ICs, high-end molding machines, and local utilities create pockets of strong leverage that can raise costs, delay shipments, and force Foxlink into multi‑million CAPEX or service contracts (capex $5–20M/line; OEM service 5–10%/yr).

| Item | 2021–25/2025 |

|---|---|

| Copper price | $10,500/ton (+35% YoY late‑2025) |

| Gold price | $2,100/oz (+8% YoY) |

| High‑end node control | ~70% by 3 firms (2024) |

| Avg lead time | ~45 days |

| Industrial electricity change | +18% (2021–25) |

What is included in the product

Tailored Porter's Five Forces analysis for Foxlink that uncovers key competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive forces and strategic defense points to inform investor presentations and internal strategy.

One-sheet Porter's Five Forces for Foxlink—visualize supplier, buyer, rivalry, entry, and substitute pressures at a glance to speed strategic decisions.

Customers Bargaining Power

High concentration of revenue from tech giants

Foxlink derives roughly 55–70% of revenue from a handful of tech giants, so a few OEMs wield strong leverage to push down unit prices and extract extended payment terms; in 2024 one top client accounted for about 22% of sales.

Stringent quality and sustainability requirements

Major automotive and industrial clients enforce ISO/TS 16949/ IATF 16949 quality and strict ESG rules; by 2025, 62% of Tier 1 buyers require verifiable low-carbon footprints and 48% demand supplier audits without paying premiums. These buyers leverage scale—top 5 customers account for ~41% of Foxlink revenue—so Foxlink must absorb capex for green processes to stay preferred, giving customers de facto control over production standards.

Low switching costs for standardized components

Many Foxlink connectors follow industry standards, so buyers face low switching costs and can shift to rivals like Luxshare or Foxconn—both of which reported combined 2024 connector revenues north of $10bn—during procurement rounds; this buyer leverage compresses margins. Customers routinely use multi-sourcing to force price cuts, so Foxlink must either cut costs (2024 gross margin 13.5%) or innovate to protect wallet share.

Backward integration threats from large OEMs

Large OEMs like Apple and Samsung, which accounted for roughly 35–45% of Foxlink’s revenue in 2024, have the cash and IP to insource connectors or power modules, posing a real backward-integration threat that can erode Foxlink’s volumes.

That latent risk tightens Foxlink’s margins during renewals: buyers use insourcing credibility to cap price increases, press for longer payment terms, and demand more customization at lower unit prices.

- Apple, Samsung scale: high insourcing capacity

- 2024 revenue exposure ~35–45%

- Limits price hikes and boosts negotiation leverage

- Raises need for product differentiation and sticky services

Demand for integrated solution capabilities

Modern buyers want end-to-end services—from design to final assembly—so Foxlink must expand capabilities and take on more operational risk and capex to meet demand.

This integration trend lets customers demand bundled pricing; in 2024 OEM contracts showed 5–12% lower unit margins on bundled deals versus standalone components.

Bundling pressure compresses product-line margins and forces Foxlink to weigh higher revenue against thinner EBITDA per unit.

- Higher capex and operating risk

- 5–12% lower margins on bundled deals (2024)

- Increased buyer leverage on pricing

Buyers Dominate: Top Clients Drive Price Pressure, Margin Hit & Costly ESG Capex

Buyers hold strong leverage: top 5 customers ≈41% revenue, one client ~22% in 2024, and Apple/Samsung together ~35–45% in 2024, enabling price pressure, longer payment terms, and insourcing threats that compress Foxlink’s 2024 gross margin of 13.5% and force capex for green/ESG compliance.

| Metric | Value |

|---|---|

| Top-5 customer share | ~41% |

| Largest single client (2024) | ~22% |

| Apple+Samsung exposure (2024) | 35–45% |

| Gross margin (2024) | 13.5% |

| Bundled-deal margin hit (2024) | −5–12% |

What You See Is What You Get

Foxlink Porter's Five Forces Analysis

This preview shows the exact Foxlink Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or sample excerpts—fully formatted, professionally written, and ready for download and use.