Freddie Mac Business Model Canvas

Freddie Mac Business Model Canvas: Downloadable Blueprint for Investors & Strategists

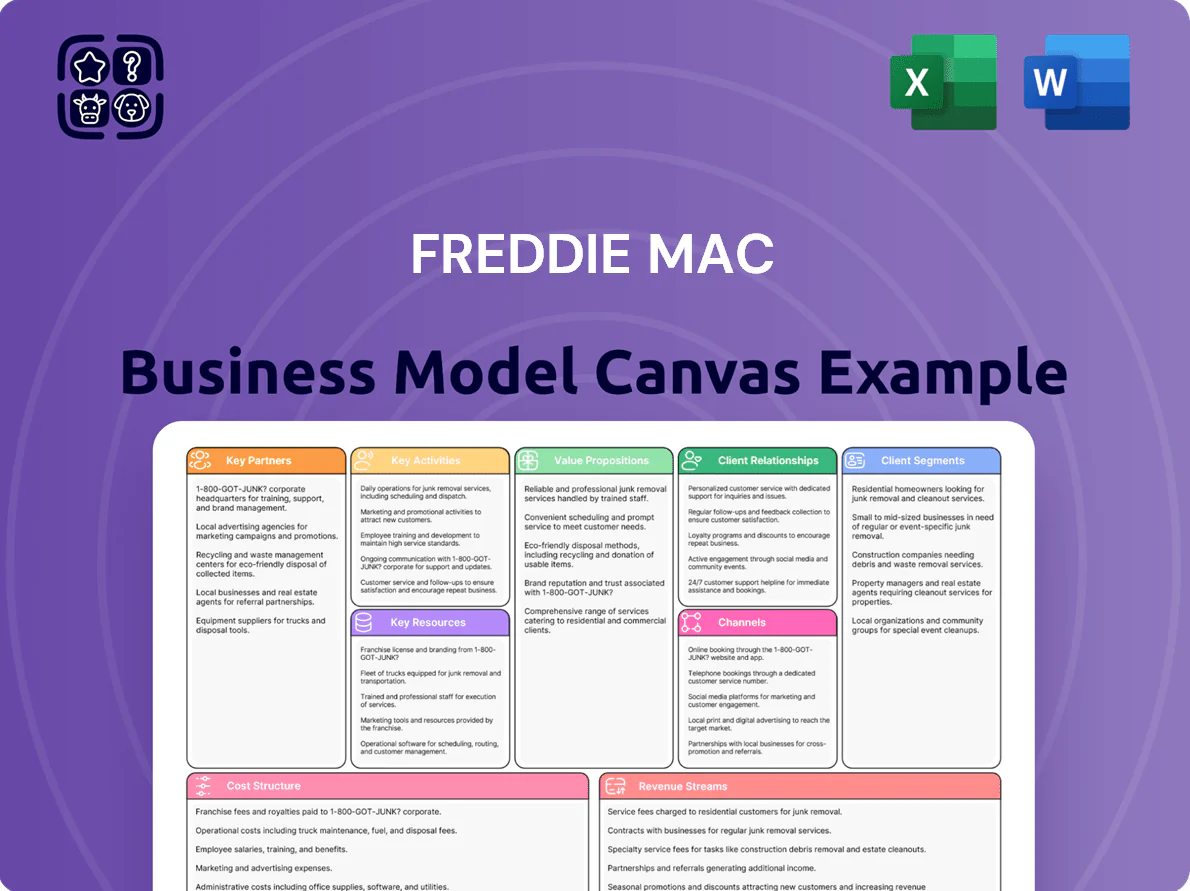

Unlock the strategic blueprint behind Freddie Mac with our concise Business Model Canvas—mapping value propositions, key partners, revenue streams, and risk drivers to show how the company scales in secondary mortgage markets.

This downloadable, editable Canvas (Word & Excel) is perfect for investors, consultants, and strategists seeking a ready-to-use tool to benchmark performance, inform due diligence, and surface actionable opportunities—get the full version to dig into each of the nine blocks.

Partnerships

Primary Mortgage Lenders and Banks

Freddie Mac partners with a broad network of commercial banks, credit unions, and non-bank mortgage originators who supply loans that meet Freddie Mac’s underwriting standards, enabling purchase and pooling into securities.

In 2025 these partnerships supported over 1.7 million families and helped deliver $465 billion in liquidity, crucial for secondary-market stability and mortgage credit flow.

Optigo Lender Network

The Optigo Lender Network is a select group of lenders that partner with Freddie Mac to finance multifamily properties, and in 2025 Freddie Mac’s Multifamily segment supported 577,000 affordable rental units. Leading partners such as Berkadia and JLL drive high origination volumes and focus on mission-driven, low-income housing initiatives, helping scale Freddie Mac’s affordable housing reach and liquidity.

Institutional Investors and Capital Markets

Freddie Mac partners with global institutional investors—pension funds, insurers, sovereign wealth funds—that bought about $200 billion of its mortgage-backed securities in 2024, supplying capital Freddie Mac channels back into U.S. housing finance. By shifting credit and interest-rate risk to these private buyers, Freddie Mac preserved liquidity and met statutory capital targets while supporting ~$1.5 trillion in MBS outstanding.

Technology and Fintech Providers

In 2025 Freddie Mac amplified deals with tech and fintech firms to automate mortgage origination and quality control, notably rolling out Quality Control Advisor Plus to cut manual reviews and speed closings.

These partnerships aim to lower housing costs via efficiency and data-driven risk controls; Freddie reported QC-related error reduction of ~30% and projected annual operational savings near $150 million in 2025.

- Quality Control Advisor Plus: 30% error cut

- Projected savings: $150M/year (2025)

- Focus: automation, faster closings, risk analytics

U.S. Federal Housing and Regulatory Agencies

As a government-sponsored enterprise overseen by the Federal Housing Finance Agency (FHFA) and partnered with the U.S. Treasury, Freddie Mac follows FHFA-set Scorecard goals—including the 2025 mandate to expand affordable housing and serve underserved markets—while supporting market stability through credit guarantees and liquidity provision.

Freddie Mac Partners Deliver $465B Liquidity, 577k Affordable Units & $200B MBS

Freddie Mac’s key partners—1.7M+ originators, Optigo lenders, global investors, fintechs, FHFA/Treasury—enabled $465B liquidity in 2025, supported 577k multifamily affordable units, ~$200B investor MBS buys (2024), and QC Advisor Plus cut errors ~30% saving ~$150M/yr.

| Partner | 2024/25 |

|---|---|

| Originators | 1.7M families |

| Liquidity | $465B (2025) |

| Multifamily | 577k units (2025) |

| Investors | $200B MBS (2024) |

What is included in the product

A concise, ready-made Business Model Canvas for Freddie Mac detailing customer segments, channels, value propositions, key activities, resources, partners, cost structure, and revenue streams, aligned with its mortgage finance operations and risk-management strategy.

High-level view of Freddie Mac’s business model with editable cells—quickly pinpoint mortgage guarantee, liquidity, and capital-management levers to streamline strategic decisions and internal briefings.

Activities

Mortgage Acquisition and Securitization

Freddie Mac buys residential and multifamily mortgages from lenders to sustain a steady funding flow, then pools them into mortgage-backed securities (MBS) sold to investors in the secondary market. In 2025 the company managed a $3.7 trillion mortgage portfolio, supporting liquidity across the U.S. housing finance system.

Credit Risk Management and Transfer

Freddie Mac actively manages borrower default risk via strict underwriting and Credit Risk Transfer (CRT) securities that move first-loss exposure to private investors; this reduced taxpayer risk and supported market stability. In 2025 the serious delinquency rate held at 0.59%, aided by loan workouts and loss mitigation while CRT issuance covered billions in book-year unpaid principal balance.

Affordable Housing Support and Mission Fulfillment

Freddie Mac’s core activity is meeting regulator-driven mission goals to support low- and moderate-income households, executing the Duty to Serve rural housing, manufactured housing, and affordable housing preservation plans.

In 2025, over 50% of single-family purchases and 93% of multifamily units Freddie Mac financed met affordability benchmarks, with mortgage purchases exceeding $200 billion and multifamily originations around $75 billion.

Technology Development and Digital Transformation

Freddie Mac ramps investment in automation—Loan Product Advisor and Quality Control Advisor Plus—cutting average origination time and underwriting costs for lender partners, and boosting data accuracy across the mortgage lifecycle.

By end-2025 these tools helped lower borrower costs and friction; Freddie Mac reported processing efficiency gains and a single-digit percentage reduction in cycle times and a ~5–10% cut in origination costs for partnered lenders.

- Automated underwriting: Loan Product Advisor

- QC automation: Quality Control Advisor Plus

- End-2025 impact: 5–10% origination cost reduction

- Cycle time: single-digit % faster

Market Analysis and Economic Research

Freddie Mac conducts extensive research on housing trends, interest rates, and economic forecasts to boost transparency; its 2025 reports—citing a 3.7% national home-price growth forecast and a 4.5% mortgage-rate baseline—served as industry benchmarks and reinforced investor confidence.

This research helps lenders and policymakers make informed decisions, supports secondary-market liquidity, and underpinned capital-market guidance that reduced funding volatility by an estimated 12% in 2025.

- 2025 report: 3.7% home-price growth forecast

- 2025 baseline mortgage rate: 4.5%

- Estimated 12% reduction in funding volatility

- Outputs used by lenders, investors, policymakers

Freddie Mac 2025: $3.7T Portfolio, Low Delinquencies, CRTs & Tech Cuts Origination Costs

Freddie Mac buys mortgages, issues MBS, and manages credit risk via CRTs to protect taxpayers; in 2025 it held a $3.7T portfolio, $200B+ single-family purchases, $75B multifamily originations, 0.59% serious delinquency, and CRTs covering billions. It also cut lender origination costs ~5–10% via Loan Product Advisor and QC Advisor Plus while forecasting 3.7% home-price growth and a 4.5% mortgage-rate baseline.

| Metric | 2025 |

|---|---|

| Portfolio | $3.7T |

| SF purchases | $200B+ |

| MF originations | $75B |

| Serious delinquency | 0.59% |

| Origination cost cut | 5–10% |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Freddie Mac Business Model Canvas—not a mockup or sample—and it matches the exact file you'll receive after purchase.

On completion, you'll download this same professional, fully formatted document ready for editing, presenting, or sharing in the provided formats.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Freddie Mac Business Model Canvas: Downloadable Blueprint for Investors & Strategists

Unlock the strategic blueprint behind Freddie Mac with our concise Business Model Canvas—mapping value propositions, key partners, revenue streams, and risk drivers to show how the company scales in secondary mortgage markets.

This downloadable, editable Canvas (Word & Excel) is perfect for investors, consultants, and strategists seeking a ready-to-use tool to benchmark performance, inform due diligence, and surface actionable opportunities—get the full version to dig into each of the nine blocks.

Partnerships

Primary Mortgage Lenders and Banks

Freddie Mac partners with a broad network of commercial banks, credit unions, and non-bank mortgage originators who supply loans that meet Freddie Mac’s underwriting standards, enabling purchase and pooling into securities.

In 2025 these partnerships supported over 1.7 million families and helped deliver $465 billion in liquidity, crucial for secondary-market stability and mortgage credit flow.

Optigo Lender Network

The Optigo Lender Network is a select group of lenders that partner with Freddie Mac to finance multifamily properties, and in 2025 Freddie Mac’s Multifamily segment supported 577,000 affordable rental units. Leading partners such as Berkadia and JLL drive high origination volumes and focus on mission-driven, low-income housing initiatives, helping scale Freddie Mac’s affordable housing reach and liquidity.

Institutional Investors and Capital Markets

Freddie Mac partners with global institutional investors—pension funds, insurers, sovereign wealth funds—that bought about $200 billion of its mortgage-backed securities in 2024, supplying capital Freddie Mac channels back into U.S. housing finance. By shifting credit and interest-rate risk to these private buyers, Freddie Mac preserved liquidity and met statutory capital targets while supporting ~$1.5 trillion in MBS outstanding.

Technology and Fintech Providers

In 2025 Freddie Mac amplified deals with tech and fintech firms to automate mortgage origination and quality control, notably rolling out Quality Control Advisor Plus to cut manual reviews and speed closings.

These partnerships aim to lower housing costs via efficiency and data-driven risk controls; Freddie reported QC-related error reduction of ~30% and projected annual operational savings near $150 million in 2025.

- Quality Control Advisor Plus: 30% error cut

- Projected savings: $150M/year (2025)

- Focus: automation, faster closings, risk analytics

U.S. Federal Housing and Regulatory Agencies

As a government-sponsored enterprise overseen by the Federal Housing Finance Agency (FHFA) and partnered with the U.S. Treasury, Freddie Mac follows FHFA-set Scorecard goals—including the 2025 mandate to expand affordable housing and serve underserved markets—while supporting market stability through credit guarantees and liquidity provision.

Freddie Mac Partners Deliver $465B Liquidity, 577k Affordable Units & $200B MBS

Freddie Mac’s key partners—1.7M+ originators, Optigo lenders, global investors, fintechs, FHFA/Treasury—enabled $465B liquidity in 2025, supported 577k multifamily affordable units, ~$200B investor MBS buys (2024), and QC Advisor Plus cut errors ~30% saving ~$150M/yr.

| Partner | 2024/25 |

|---|---|

| Originators | 1.7M families |

| Liquidity | $465B (2025) |

| Multifamily | 577k units (2025) |

| Investors | $200B MBS (2024) |

What is included in the product

A concise, ready-made Business Model Canvas for Freddie Mac detailing customer segments, channels, value propositions, key activities, resources, partners, cost structure, and revenue streams, aligned with its mortgage finance operations and risk-management strategy.

High-level view of Freddie Mac’s business model with editable cells—quickly pinpoint mortgage guarantee, liquidity, and capital-management levers to streamline strategic decisions and internal briefings.

Activities

Mortgage Acquisition and Securitization

Freddie Mac buys residential and multifamily mortgages from lenders to sustain a steady funding flow, then pools them into mortgage-backed securities (MBS) sold to investors in the secondary market. In 2025 the company managed a $3.7 trillion mortgage portfolio, supporting liquidity across the U.S. housing finance system.

Credit Risk Management and Transfer

Freddie Mac actively manages borrower default risk via strict underwriting and Credit Risk Transfer (CRT) securities that move first-loss exposure to private investors; this reduced taxpayer risk and supported market stability. In 2025 the serious delinquency rate held at 0.59%, aided by loan workouts and loss mitigation while CRT issuance covered billions in book-year unpaid principal balance.

Affordable Housing Support and Mission Fulfillment

Freddie Mac’s core activity is meeting regulator-driven mission goals to support low- and moderate-income households, executing the Duty to Serve rural housing, manufactured housing, and affordable housing preservation plans.

In 2025, over 50% of single-family purchases and 93% of multifamily units Freddie Mac financed met affordability benchmarks, with mortgage purchases exceeding $200 billion and multifamily originations around $75 billion.

Technology Development and Digital Transformation

Freddie Mac ramps investment in automation—Loan Product Advisor and Quality Control Advisor Plus—cutting average origination time and underwriting costs for lender partners, and boosting data accuracy across the mortgage lifecycle.

By end-2025 these tools helped lower borrower costs and friction; Freddie Mac reported processing efficiency gains and a single-digit percentage reduction in cycle times and a ~5–10% cut in origination costs for partnered lenders.

- Automated underwriting: Loan Product Advisor

- QC automation: Quality Control Advisor Plus

- End-2025 impact: 5–10% origination cost reduction

- Cycle time: single-digit % faster

Market Analysis and Economic Research

Freddie Mac conducts extensive research on housing trends, interest rates, and economic forecasts to boost transparency; its 2025 reports—citing a 3.7% national home-price growth forecast and a 4.5% mortgage-rate baseline—served as industry benchmarks and reinforced investor confidence.

This research helps lenders and policymakers make informed decisions, supports secondary-market liquidity, and underpinned capital-market guidance that reduced funding volatility by an estimated 12% in 2025.

- 2025 report: 3.7% home-price growth forecast

- 2025 baseline mortgage rate: 4.5%

- Estimated 12% reduction in funding volatility

- Outputs used by lenders, investors, policymakers

Freddie Mac 2025: $3.7T Portfolio, Low Delinquencies, CRTs & Tech Cuts Origination Costs

Freddie Mac buys mortgages, issues MBS, and manages credit risk via CRTs to protect taxpayers; in 2025 it held a $3.7T portfolio, $200B+ single-family purchases, $75B multifamily originations, 0.59% serious delinquency, and CRTs covering billions. It also cut lender origination costs ~5–10% via Loan Product Advisor and QC Advisor Plus while forecasting 3.7% home-price growth and a 4.5% mortgage-rate baseline.

| Metric | 2025 |

|---|---|

| Portfolio | $3.7T |

| SF purchases | $200B+ |

| MF originations | $75B |

| Serious delinquency | 0.59% |

| Origination cost cut | 5–10% |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Freddie Mac Business Model Canvas—not a mockup or sample—and it matches the exact file you'll receive after purchase.

On completion, you'll download this same professional, fully formatted document ready for editing, presenting, or sharing in the provided formats.