Freddie Mac Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

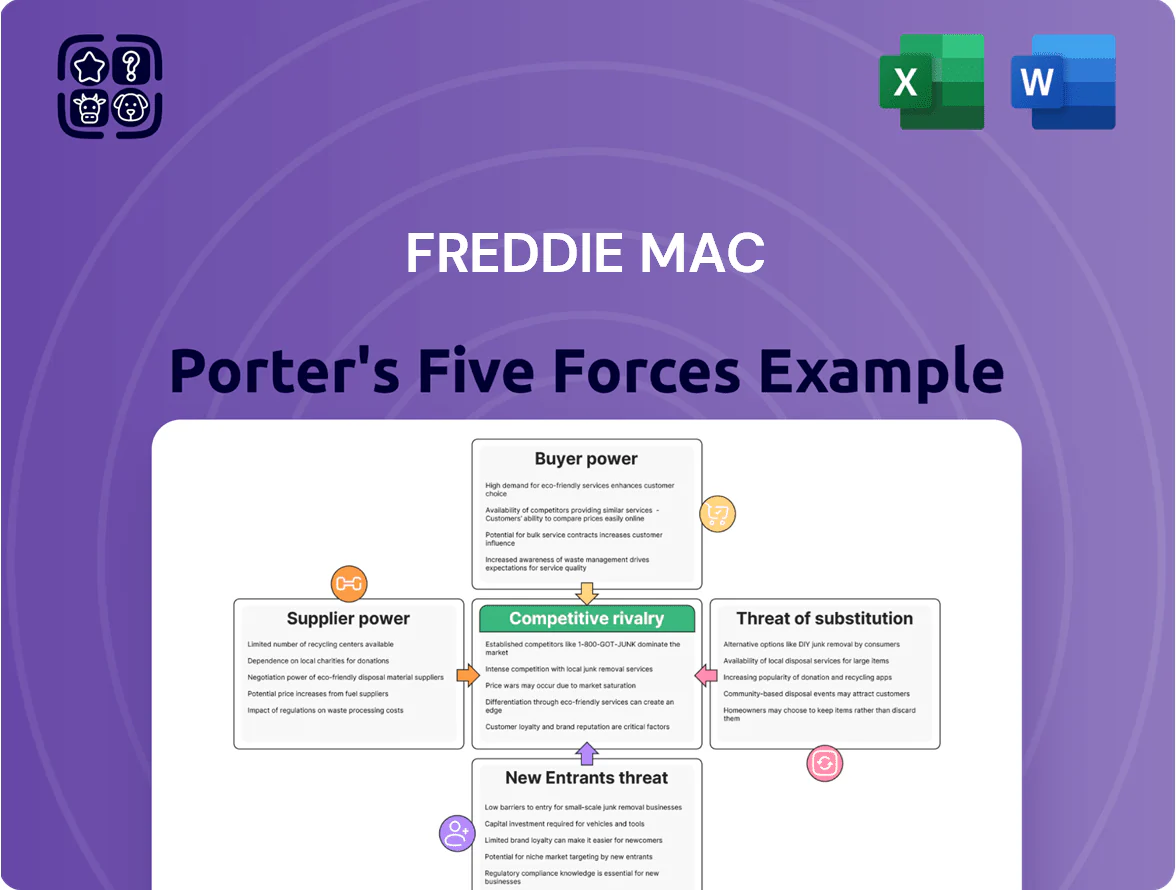

Freddie Mac faces intense regulatory oversight, concentrated buyer power from mortgage investors, and moderate supplier leverage from capital markets, while threat of substitutes and new entrants remains low due to scale and government ties.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Freddie Mac’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Primary Mortgage Lenders

Dependence on US Treasury Financial Backstop

The US Treasury, via the Preferred Stock Purchase Agreements established 2008 and extended through 2022 reforms, functions as Freddie Mac’s primary capital supplier, providing up to unlimited liquidity support; in 2025 Treasury’s remaining commitment and prior draws (cumulative Treasury injections reached about $187 billion by 2022) mean fiscal policy changes can rapidly tighten Freddie’s lending capacity.

Influence of Credit Rating Agencies

Rating agencies evaluate Freddie Mac’s debt and MBS creditworthiness, directly shaping investor confidence and funding costs; Moody’s, S&P, and Fitch together rated over 90% of US securitizations in 2024. Their outlooks can move spreads: a one-notch downgrade historically raised funding costs by ~20–40 bps for large issuers, adding roughly $200–400 million annually at Freddie Mac’s ~$200 billion debt level. With few major agencies, their bargaining power stays high.

Data and Technology Infrastructure Providers

Freddie Mac depends on specialized cloud, risk-modeling, and cybersecurity vendors whose services grew 30–40% in mortgage sector spend by 2024–25, giving suppliers leverage as digitization increases through late 2025.

Integrated platforms create high switching costs—migration can exceed tens of millions and 12–24 months—so tech suppliers hold sustained bargaining power over pricing and SLAs.

- 2024–25 vendor spend up 30–40%

- Migration cost: tens of millions

- Migration time: 12–24 months

- High dependency on cloud, modeling, cyber vendors

Supply of Mortgage Originations

- Origination volume ~ $2.1T in 2025 (‑18% YoY)

- Higher rates cut production, increasing supplier leverage

- Originators push for fee concessions and price premiums

- Freddie's G-fee spreads rose in 2024–25 under stress

Concentrated originators, rising vendor costs, and Treasury backstop amplify sector risk

| Metric | Value |

|---|---|

| Top‑10 share (2024) | ≈55% |

| Origination (2025) | ≈$2.1T (‑18% YoY) |

| Treasury draws (by 2022) | ≈$187B |

| Vendor spend change (2024–25) | +30–40% |

| Migration cost/time | Tens of $M; 12–24m |

What is included in the product

Concise Porter’s Five Forces assessment of Freddie Mac highlighting competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and regulatory barriers shaping its market position and profitability.

A concise Freddie Mac Porter’s Five Forces snapshot—translate complex mortgage market dynamics into actionable insights for lenders, investors, and policymakers.

Customers Bargaining Power

Institutional Investor Demand for MBS

Institutional investors—pension funds, central banks, insurers—are Freddie Mac’s main MBS buyers; in 2024 these groups held ~45% of agency MBS market flows, setting required yields and acceptable credit/term profiles.

Their demand drives MBS liquidity and mortgage rates; a 1% drop in global risk appetite can widen agency yield spreads by ~20–30 bps, forcing Freddie to raise coupons to attract capital.

Federal Reserve Monetary Policy Actions

The Federal Reserve acts as a massive customer and holder of agency mortgage-backed securities (MBS), owning about 20% of outstanding agency MBS as of December 2025; its buy/sell decisions move spreads and yields and thus borrower demand for Freddie Mac products.

Fed balance-sheet actions through 2025—reductions of roughly $800 billion in MBS holdings in 2023–24 followed by selective reinvestments—have tightened liquidity and lifted MBS yields, squeezing margins.

Freddie Mac is highly sensitive to the Fed as a market whale: a single quarter of net Fed purchases or sales can change agency MBS prices by 20–40 basis points, overshadowing other investor demand and shifting customer bargaining power.

Lender Choice and Switching Costs

Mortgage lenders choosing between Freddie Mac and Fannie Mae face near-identical securitization products, so small guarantee fee (g-fee) spreads matter: Freddie’s 2024 average g-fee differential vs Fannie was about 2–5 basis points on single-family loans, enough to shift volume.

Low switching costs and comparable tech offerings (Freddie’s 2024 Loan Prospector/Loan Product Advisor adoption ~48%) force Freddie to lower fees, improve pipelines, and offer faster executions to keep lender share.

Global Capital Market Volatility

International investors bought $58.4 billion of agency debt in 2024, treating Freddie Mac securities as safe-haven during geopolitical stress; their flight-to-quality lowers yields and cuts Freddie Mac’s funding costs.

When global stability returns, demand shifts to riskier assets, reducing these investors’ leverage and widening spreads, which can raise Freddie Mac borrowing costs.

- 2024 agency inflows: $58.4B

- Flight-to-quality compresses yields ~10–30 bps

- Stability shifts demand, can widen spreads

Secondary Market Liquidity Requirements

- 2024 TBA avg volume ~$1.3T/month

- Institutional buyers favor standardized coupons and pools

- Freddie must meet TBA specs to maintain large-account allocations

Institutional + Fed dominance, g‑fee tweaks and TBA liquidity steer agency MBS spreads

Institutional buyers (45% of 2024 agency MBS flows) and the Fed (≈20% of outstanding agency MBS by Dec 2025) drive yields; a 1% drop in risk appetite widens spreads ~20–30 bps, forcing higher coupons. Low switching costs and ~48% lender adoption of Freddie’s tools mean 2–5 bps g-fee gaps shift volumes. TBA liquidity (~$1.3T/month in 2024) forces standardized issuance to retain large managers.

| Metric | Value |

|---|---|

| Institutional share (2024) | ~45% |

| Fed share (Dec 2025) | ~20% |

| TBA volume (2024) | $1.3T/month |

| G-fee diff vs Fannie (2024) | 2–5 bps |

Preview the Actual Deliverable

Freddie Mac Porter's Five Forces Analysis

This preview shows the exact Freddie Mac Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups; the complete, professionally formatted document is ready for download and use the moment you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Freddie Mac faces intense regulatory oversight, concentrated buyer power from mortgage investors, and moderate supplier leverage from capital markets, while threat of substitutes and new entrants remains low due to scale and government ties.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Freddie Mac’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Primary Mortgage Lenders

Dependence on US Treasury Financial Backstop

The US Treasury, via the Preferred Stock Purchase Agreements established 2008 and extended through 2022 reforms, functions as Freddie Mac’s primary capital supplier, providing up to unlimited liquidity support; in 2025 Treasury’s remaining commitment and prior draws (cumulative Treasury injections reached about $187 billion by 2022) mean fiscal policy changes can rapidly tighten Freddie’s lending capacity.

Influence of Credit Rating Agencies

Rating agencies evaluate Freddie Mac’s debt and MBS creditworthiness, directly shaping investor confidence and funding costs; Moody’s, S&P, and Fitch together rated over 90% of US securitizations in 2024. Their outlooks can move spreads: a one-notch downgrade historically raised funding costs by ~20–40 bps for large issuers, adding roughly $200–400 million annually at Freddie Mac’s ~$200 billion debt level. With few major agencies, their bargaining power stays high.

Data and Technology Infrastructure Providers

Freddie Mac depends on specialized cloud, risk-modeling, and cybersecurity vendors whose services grew 30–40% in mortgage sector spend by 2024–25, giving suppliers leverage as digitization increases through late 2025.

Integrated platforms create high switching costs—migration can exceed tens of millions and 12–24 months—so tech suppliers hold sustained bargaining power over pricing and SLAs.

- 2024–25 vendor spend up 30–40%

- Migration cost: tens of millions

- Migration time: 12–24 months

- High dependency on cloud, modeling, cyber vendors

Supply of Mortgage Originations

- Origination volume ~ $2.1T in 2025 (‑18% YoY)

- Higher rates cut production, increasing supplier leverage

- Originators push for fee concessions and price premiums

- Freddie's G-fee spreads rose in 2024–25 under stress

Concentrated originators, rising vendor costs, and Treasury backstop amplify sector risk

| Metric | Value |

|---|---|

| Top‑10 share (2024) | ≈55% |

| Origination (2025) | ≈$2.1T (‑18% YoY) |

| Treasury draws (by 2022) | ≈$187B |

| Vendor spend change (2024–25) | +30–40% |

| Migration cost/time | Tens of $M; 12–24m |

What is included in the product

Concise Porter’s Five Forces assessment of Freddie Mac highlighting competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and regulatory barriers shaping its market position and profitability.

A concise Freddie Mac Porter’s Five Forces snapshot—translate complex mortgage market dynamics into actionable insights for lenders, investors, and policymakers.

Customers Bargaining Power

Institutional Investor Demand for MBS

Institutional investors—pension funds, central banks, insurers—are Freddie Mac’s main MBS buyers; in 2024 these groups held ~45% of agency MBS market flows, setting required yields and acceptable credit/term profiles.

Their demand drives MBS liquidity and mortgage rates; a 1% drop in global risk appetite can widen agency yield spreads by ~20–30 bps, forcing Freddie to raise coupons to attract capital.

Federal Reserve Monetary Policy Actions

The Federal Reserve acts as a massive customer and holder of agency mortgage-backed securities (MBS), owning about 20% of outstanding agency MBS as of December 2025; its buy/sell decisions move spreads and yields and thus borrower demand for Freddie Mac products.

Fed balance-sheet actions through 2025—reductions of roughly $800 billion in MBS holdings in 2023–24 followed by selective reinvestments—have tightened liquidity and lifted MBS yields, squeezing margins.

Freddie Mac is highly sensitive to the Fed as a market whale: a single quarter of net Fed purchases or sales can change agency MBS prices by 20–40 basis points, overshadowing other investor demand and shifting customer bargaining power.

Lender Choice and Switching Costs

Mortgage lenders choosing between Freddie Mac and Fannie Mae face near-identical securitization products, so small guarantee fee (g-fee) spreads matter: Freddie’s 2024 average g-fee differential vs Fannie was about 2–5 basis points on single-family loans, enough to shift volume.

Low switching costs and comparable tech offerings (Freddie’s 2024 Loan Prospector/Loan Product Advisor adoption ~48%) force Freddie to lower fees, improve pipelines, and offer faster executions to keep lender share.

Global Capital Market Volatility

International investors bought $58.4 billion of agency debt in 2024, treating Freddie Mac securities as safe-haven during geopolitical stress; their flight-to-quality lowers yields and cuts Freddie Mac’s funding costs.

When global stability returns, demand shifts to riskier assets, reducing these investors’ leverage and widening spreads, which can raise Freddie Mac borrowing costs.

- 2024 agency inflows: $58.4B

- Flight-to-quality compresses yields ~10–30 bps

- Stability shifts demand, can widen spreads

Secondary Market Liquidity Requirements

- 2024 TBA avg volume ~$1.3T/month

- Institutional buyers favor standardized coupons and pools

- Freddie must meet TBA specs to maintain large-account allocations

Institutional + Fed dominance, g‑fee tweaks and TBA liquidity steer agency MBS spreads

Institutional buyers (45% of 2024 agency MBS flows) and the Fed (≈20% of outstanding agency MBS by Dec 2025) drive yields; a 1% drop in risk appetite widens spreads ~20–30 bps, forcing higher coupons. Low switching costs and ~48% lender adoption of Freddie’s tools mean 2–5 bps g-fee gaps shift volumes. TBA liquidity (~$1.3T/month in 2024) forces standardized issuance to retain large managers.

| Metric | Value |

|---|---|

| Institutional share (2024) | ~45% |

| Fed share (Dec 2025) | ~20% |

| TBA volume (2024) | $1.3T/month |

| G-fee diff vs Fannie (2024) | 2–5 bps |

Preview the Actual Deliverable

Freddie Mac Porter's Five Forces Analysis

This preview shows the exact Freddie Mac Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups; the complete, professionally formatted document is ready for download and use the moment you buy.