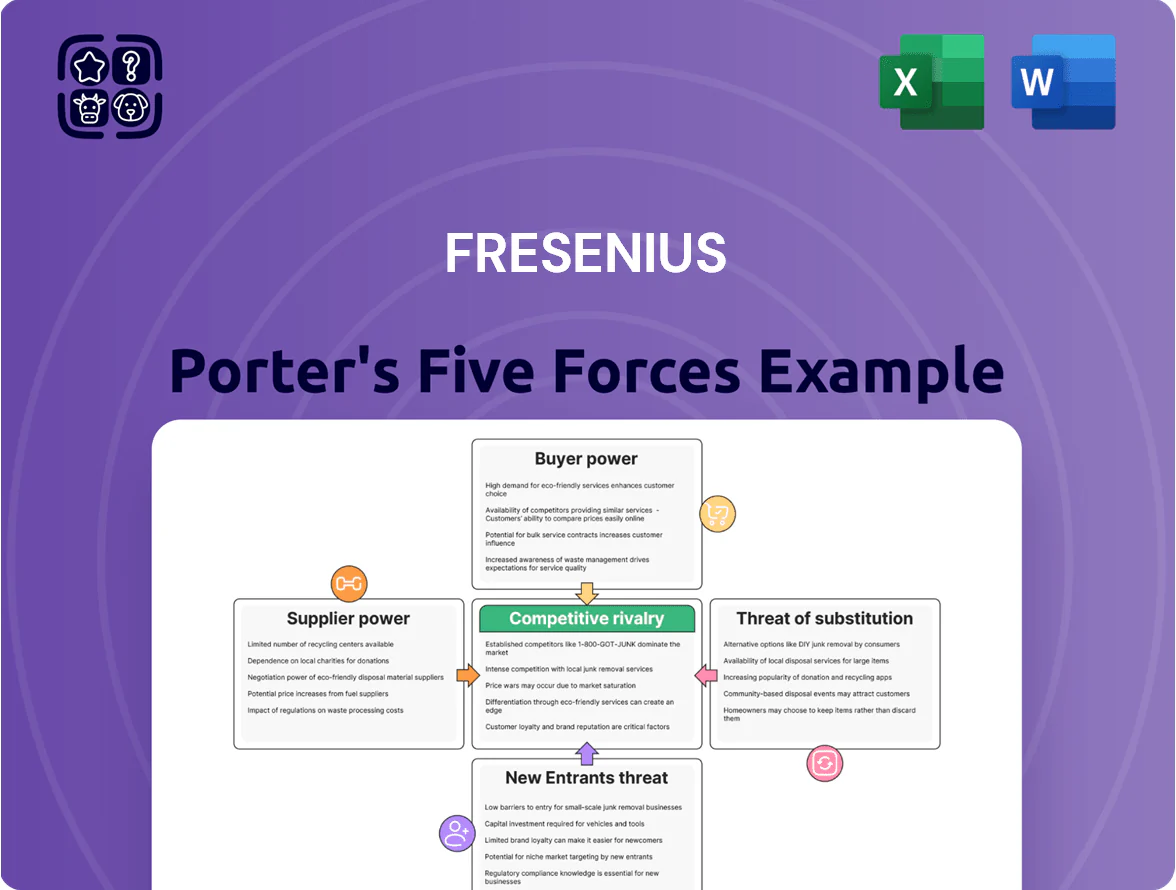

Fresenius Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Fresenius faces intense buyer power and regulatory pressure balanced by strong supplier relationships and diversified service lines, while new entrants and substitutes pose moderate threats given high capital intensity and established networks.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Fresenius’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized API Sourcing

Fresenius Kabi depends on a few certified global manufacturers for key active pharmaceutical ingredients (APIs), so supplier concentration raises bargaining power and risk of shortages; a 2024 IQVIA report noted 60–70% of certain generic injectable APIs come from under five suppliers.

Specialized Medical Labor Shortage

The global shortage of 6.6 million nurses in 2022, projected to persist into 2025, raises suppliers' power for Fresenius: Helios (hospitals) and Medical Care (dialysis) must raise pay and benefits—Fresenius Medical Care reported €1.9bn staff costs in 2024 H1—adding upward pressure on operating expenses and pushing ~€200m–€500m strategic investment needs in automated clinical workflows over 2025–27 to sustain margins.

High Tech Medical Equipment Patentees

Procurement of advanced diagnostic and therapeutic machinery faces a few dominant medtech patentees (eg, Siemens Healthineers, GE HealthCare, Philips) that command high leverage due to proprietary hardware and software lock-in; switching costs often exceed €1m per site. Fresenius offsets this by using scale—€35.7bn 2024 revenues—to secure multi-year service contracts and volume discounts, cutting unit maintenance spend by an estimated 10–15%.

Energy and Raw Material Volatility

Energy and raw-material volatility raises supplier power for Fresenius since dialysis filters and IV solutions need high energy and specialized plastics/chemicals; global oil and PVC price swings drove input cost variance of ~8–12% for med-tech in 2024.

Suppliers hold moderate leverage due to market fluctuations and stricter EU chemical rules from 2023, but Fresenius offsets risk with hedging and vertical integration—its manufacturing capex rose 6% in 2024 to boost in‑house resin and formulation capacity.

Here’s the quick math: a 10% PVC price jump can raise COGS for consumables by ~3–4%, so hedges and integration aim to cut exposure by ~60%.

- Input sensitivity: 8–12% cost variance (2024)

- Regulatory pressure: EU chemical rules tightened 2023

- Mitigation: 6% capex increase in 2024 for integration

- Hedge impact: ~60% exposure reduction vs spot

Logistics and Cold Chain Providers

Distribution of clinical nutrition and sensitive pharmaceuticals needs specialized cold-chain logistics with global reach; top providers like World Courier and Marken handle ~70% of high-value pharma shipments and charge premiums that squeeze margins.

These providers hold bargaining power via dense infrastructure and compliance with GDP (Good Distribution Practice) rules; in 2024 cold-chain capacity shortages raised spot rates by ~18% in Europe.

Fresenius offsets this by keeping in-house logistics hubs across Europe and North America and selectively outsourcing in 30+ markets to retain flexibility and control costs.

- Specialized providers: ~70% market share for high-value pharma

- Spot rates up ~18% in Europe (2024)

- Fresenius: in-house hubs + outsourcing in 30+ markets

Fresenius offsets 8–12% input swings with capex, hedges and scale on €35.7bn revenue

Suppliers exert moderate-to-high power: concentrated API and medtech markets, cold-chain specialists (~70% share), and energy/plastics volatility drove 2024 input variance of 8–12% and spot logistics rates +18%; Fresenius partly offsets with 6% higher 2024 manufacturing capex, vertical integration, hedges (~60% exposure reduction) and scale (€35.7bn 2024 revenue).

| Metric | 2024 value |

|---|---|

| Revenue | €35.7bn |

| Input variance | 8–12% |

| Logistics spot rise | +18% |

| Capex rise | +6% |

| Hedge effect | ~60% |

What is included in the product

Tailored exclusively for Fresenius, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats shaping its profitability and strategic positioning.

A concise Porter's Five Forces snapshot for Fresenius—instantly reveal supplier, buyer, entrant, substitute, and competitive pressures to speed strategic decisions.

Customers Bargaining Power

Government Reimbursement Pressures

Public health systems and national insurers fund ~70% of Fresenius Medical Care’s revenue in Europe and North America, giving governments strong bargaining power that caps price growth for dialysis and hospital services.

Since 2020, payer cost-containment pushed average annual price increases below 1.5%, forcing Fresenius to show clinical efficiency and cut per-patient costs to protect 2024 adjusted EBIT margin near 11%.

Consolidation of Private Insurers

Public Procurement Auctions

Public procurement auctions in generics and biosimilars push prices sharply down—EU hospital tenders cut average contract prices by ~25–40% in 2023, forcing manufacturers to win exclusive multi‑year deals. Fresenius Kabi needs ultra‑lean production to bid profitably for high‑volume, low‑margin contracts that can represent >30% of regional sales. Tight margins raise exit risk if capacity utilization falls below ~80%.

Patient Empowerment and Choice

Increasing transparency in quality metrics gives patients more say in where they go, boosting elective volumes at Helios; 2024 patient satisfaction scores rose 6 percentage points and online ratings grew 12% year-on-year.

Individually patients have low bargaining power, but collectively their demand for better outcomes and digital access pushed Fresenius to spend ~€350m on patient experience and IT in 2024.

Fresenius must adopt a consumer-centric delivery model to retain market share, or risk elective-case losses to higher-rated competitors.

- Patient scores +6pp in 2024

- Online ratings +12% YoY

- €350m spent on PX/IT in 2024

- Elective care sensitivity high

Group Purchasing Organizations

Large hospital networks use Group Purchasing Organizations (GPOs) to pool demand; in 2024 GPOs represented about 70% of U.S. hospital purchasing volume, squeezing vendor margins for suppliers like Fresenius Kabi.

GPOs negotiate contracts covering hundreds of facilities to drive down prices for IV fluids, generics, and oncology drugs, forcing Fresenius to compete on price and volume.

Fresenius counters by stressing supply-chain reliability—manufacturing in multiple sites—and a broad portfolio (dialysis, ICU, IV therapies) to secure preferred GPO contracts.

- GPOs ~70% U.S. hospital buying (2024)

- They aggregate hundreds of facilities per contract

- Pressure on margins for vendors like Fresenius Kabi

- Fresenius uses multi-site supply and wide product range

Payers & GPOs Squeeze Prices; Fresenius pivots to value models and IT to defend margins

Payers (governments ~70% of revenue; top 5 US insurers ~70% market) and GPOs (~70% US hospital buying) hold strong bargaining power, capping prices and forcing cost cuts; public tenders cut biosimilar prices 25–40% in 2023. Fresenius shifted >25% revenue to value-based models and spent €350m on patient experience/IT in 2024 to protect ~11% adjusted EBIT margin.

| Metric | Value |

|---|---|

| Govt/insurer revenue share | ~70% |

| Top-5 US insurers share | ~70% |

| GPO hospital buying (US) | ~70% |

| Biosimilar tender price cuts (EU 2023) | 25–40% |

| Revenue in alt payment models (2024) | >25% |

| PX/IT spend (2024) | €350m |

| Adjusted EBIT margin target (2024) | ~11% |

Same Document Delivered

Fresenius Porter's Five Forces Analysis

This preview shows the exact Fresenius Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no samples. The document is fully formatted, professionally written, and ready for download and use the moment you buy. It contains the complete assessment of industry rivalry, supplier and buyer power, threat of entrants, and substitute risks tailored to Fresenius. What you see is precisely what you’ll get.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Fresenius faces intense buyer power and regulatory pressure balanced by strong supplier relationships and diversified service lines, while new entrants and substitutes pose moderate threats given high capital intensity and established networks.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Fresenius’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized API Sourcing

Fresenius Kabi depends on a few certified global manufacturers for key active pharmaceutical ingredients (APIs), so supplier concentration raises bargaining power and risk of shortages; a 2024 IQVIA report noted 60–70% of certain generic injectable APIs come from under five suppliers.

Specialized Medical Labor Shortage

The global shortage of 6.6 million nurses in 2022, projected to persist into 2025, raises suppliers' power for Fresenius: Helios (hospitals) and Medical Care (dialysis) must raise pay and benefits—Fresenius Medical Care reported €1.9bn staff costs in 2024 H1—adding upward pressure on operating expenses and pushing ~€200m–€500m strategic investment needs in automated clinical workflows over 2025–27 to sustain margins.

High Tech Medical Equipment Patentees

Procurement of advanced diagnostic and therapeutic machinery faces a few dominant medtech patentees (eg, Siemens Healthineers, GE HealthCare, Philips) that command high leverage due to proprietary hardware and software lock-in; switching costs often exceed €1m per site. Fresenius offsets this by using scale—€35.7bn 2024 revenues—to secure multi-year service contracts and volume discounts, cutting unit maintenance spend by an estimated 10–15%.

Energy and Raw Material Volatility

Energy and raw-material volatility raises supplier power for Fresenius since dialysis filters and IV solutions need high energy and specialized plastics/chemicals; global oil and PVC price swings drove input cost variance of ~8–12% for med-tech in 2024.

Suppliers hold moderate leverage due to market fluctuations and stricter EU chemical rules from 2023, but Fresenius offsets risk with hedging and vertical integration—its manufacturing capex rose 6% in 2024 to boost in‑house resin and formulation capacity.

Here’s the quick math: a 10% PVC price jump can raise COGS for consumables by ~3–4%, so hedges and integration aim to cut exposure by ~60%.

- Input sensitivity: 8–12% cost variance (2024)

- Regulatory pressure: EU chemical rules tightened 2023

- Mitigation: 6% capex increase in 2024 for integration

- Hedge impact: ~60% exposure reduction vs spot

Logistics and Cold Chain Providers

Distribution of clinical nutrition and sensitive pharmaceuticals needs specialized cold-chain logistics with global reach; top providers like World Courier and Marken handle ~70% of high-value pharma shipments and charge premiums that squeeze margins.

These providers hold bargaining power via dense infrastructure and compliance with GDP (Good Distribution Practice) rules; in 2024 cold-chain capacity shortages raised spot rates by ~18% in Europe.

Fresenius offsets this by keeping in-house logistics hubs across Europe and North America and selectively outsourcing in 30+ markets to retain flexibility and control costs.

- Specialized providers: ~70% market share for high-value pharma

- Spot rates up ~18% in Europe (2024)

- Fresenius: in-house hubs + outsourcing in 30+ markets

Fresenius offsets 8–12% input swings with capex, hedges and scale on €35.7bn revenue

Suppliers exert moderate-to-high power: concentrated API and medtech markets, cold-chain specialists (~70% share), and energy/plastics volatility drove 2024 input variance of 8–12% and spot logistics rates +18%; Fresenius partly offsets with 6% higher 2024 manufacturing capex, vertical integration, hedges (~60% exposure reduction) and scale (€35.7bn 2024 revenue).

| Metric | 2024 value |

|---|---|

| Revenue | €35.7bn |

| Input variance | 8–12% |

| Logistics spot rise | +18% |

| Capex rise | +6% |

| Hedge effect | ~60% |

What is included in the product

Tailored exclusively for Fresenius, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats shaping its profitability and strategic positioning.

A concise Porter's Five Forces snapshot for Fresenius—instantly reveal supplier, buyer, entrant, substitute, and competitive pressures to speed strategic decisions.

Customers Bargaining Power

Government Reimbursement Pressures

Public health systems and national insurers fund ~70% of Fresenius Medical Care’s revenue in Europe and North America, giving governments strong bargaining power that caps price growth for dialysis and hospital services.

Since 2020, payer cost-containment pushed average annual price increases below 1.5%, forcing Fresenius to show clinical efficiency and cut per-patient costs to protect 2024 adjusted EBIT margin near 11%.

Consolidation of Private Insurers

Public Procurement Auctions

Public procurement auctions in generics and biosimilars push prices sharply down—EU hospital tenders cut average contract prices by ~25–40% in 2023, forcing manufacturers to win exclusive multi‑year deals. Fresenius Kabi needs ultra‑lean production to bid profitably for high‑volume, low‑margin contracts that can represent >30% of regional sales. Tight margins raise exit risk if capacity utilization falls below ~80%.

Patient Empowerment and Choice

Increasing transparency in quality metrics gives patients more say in where they go, boosting elective volumes at Helios; 2024 patient satisfaction scores rose 6 percentage points and online ratings grew 12% year-on-year.

Individually patients have low bargaining power, but collectively their demand for better outcomes and digital access pushed Fresenius to spend ~€350m on patient experience and IT in 2024.

Fresenius must adopt a consumer-centric delivery model to retain market share, or risk elective-case losses to higher-rated competitors.

- Patient scores +6pp in 2024

- Online ratings +12% YoY

- €350m spent on PX/IT in 2024

- Elective care sensitivity high

Group Purchasing Organizations

Large hospital networks use Group Purchasing Organizations (GPOs) to pool demand; in 2024 GPOs represented about 70% of U.S. hospital purchasing volume, squeezing vendor margins for suppliers like Fresenius Kabi.

GPOs negotiate contracts covering hundreds of facilities to drive down prices for IV fluids, generics, and oncology drugs, forcing Fresenius to compete on price and volume.

Fresenius counters by stressing supply-chain reliability—manufacturing in multiple sites—and a broad portfolio (dialysis, ICU, IV therapies) to secure preferred GPO contracts.

- GPOs ~70% U.S. hospital buying (2024)

- They aggregate hundreds of facilities per contract

- Pressure on margins for vendors like Fresenius Kabi

- Fresenius uses multi-site supply and wide product range

Payers & GPOs Squeeze Prices; Fresenius pivots to value models and IT to defend margins

Payers (governments ~70% of revenue; top 5 US insurers ~70% market) and GPOs (~70% US hospital buying) hold strong bargaining power, capping prices and forcing cost cuts; public tenders cut biosimilar prices 25–40% in 2023. Fresenius shifted >25% revenue to value-based models and spent €350m on patient experience/IT in 2024 to protect ~11% adjusted EBIT margin.

| Metric | Value |

|---|---|

| Govt/insurer revenue share | ~70% |

| Top-5 US insurers share | ~70% |

| GPO hospital buying (US) | ~70% |

| Biosimilar tender price cuts (EU 2023) | 25–40% |

| Revenue in alt payment models (2024) | >25% |

| PX/IT spend (2024) | €350m |

| Adjusted EBIT margin target (2024) | ~11% |

Same Document Delivered

Fresenius Porter's Five Forces Analysis

This preview shows the exact Fresenius Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no samples. The document is fully formatted, professionally written, and ready for download and use the moment you buy. It contains the complete assessment of industry rivalry, supplier and buyer power, threat of entrants, and substitute risks tailored to Fresenius. What you see is precisely what you’ll get.