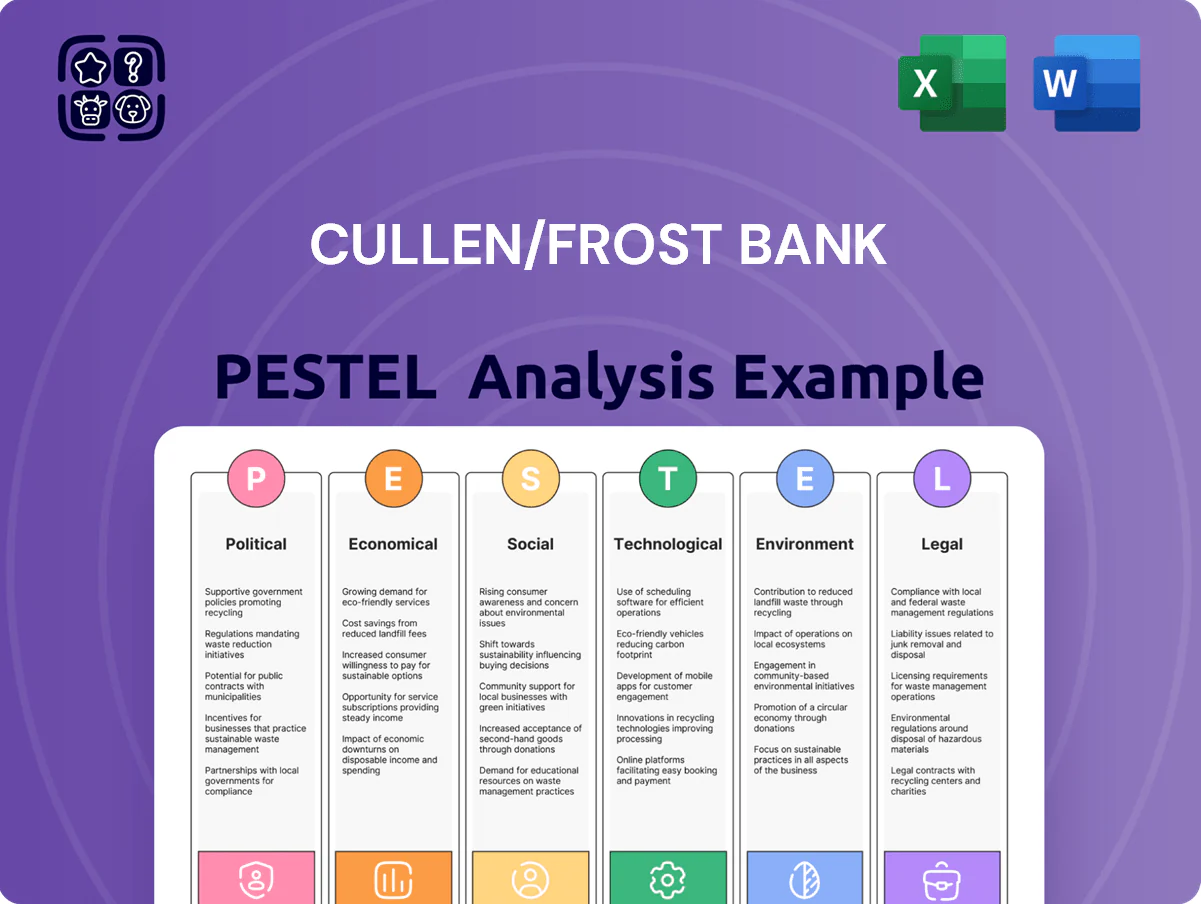

Cullen/Frost Bank PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Gain strategic clarity with our PESTLE Analysis of Cullen/Frost Bank—spot regulatory, economic, and technological forces shaping its next moves and turn those insights into actionable strategy. Purchase the full report for a complete, editable breakdown ideal for investors, advisors, and executives seeking a competitive edge.

Political factors

Texas Regulatory Environment

Frost Bank’s Texas-centric operations tie it closely to state politics; Texas reported a $33.6 billion surplus in FY2024, supporting pro-business tax and regulatory policies that benefit regional banks through lower state-level tax burdens and streamlined licensing.

Texas’ pro-growth stance and 2023 corporate tax incentives helped deposit growth for regional banks, but shifts in state leadership or moves toward tighter financial oversight could constrain Frost’s lending and expansion plans.

Federal Monetary Policy Influence

Financial Industry Lobbying and Reform

Ongoing Washington debates over Dodd-Frank revisions and targeted bank reform raise compliance costs for mid-sized banks like Cullen/Frost; estimated industry compliance spending rose to roughly $23.6 billion in 2024, pressuring regional margins. Cullen/Frost must track federal proposals that could tighten or relax capital requirements—e.g., 2025 drafts discussed raising CET1-like buffers for regional banks by 50–150 bps. Party shifts historically change regulatory intensity: Republican control (2017–2018) correlated with eased rules, Democratic control (2021–2022) with tighter enforcement, creating policy-driven volatility in compliance planning.

Geopolitical Stability and Energy Policy

Texas's energy dominance ties Cullen/Frost's commercial loan exposure to oil and gas; as of 2024 Texas accounted for about 40% of U.S. crude production, so federal or international policy shifts materially affect portfolio risk.

Political tensions in major producers and U.S. energy policy changes drove Brent/WTI volatility in 2024–25—WTI ranged roughly $60–90/bbl—raising default risk for energy clients and weakening regional GDP growth.

- ~40% of U.S. crude from Texas (2024)

- WTI swing ~$60–$90/bbl (2024–25)

- Higher energy volatility → increased loan loss provisioning

Government Infrastructure Spending

Federal and Texas state commitments to infrastructure—highlighted by the 2021 Bipartisan Infrastructure Law allocating $110B to roads and bridges and Texas' $61B 2023 transportation plan—create demand for commercial loans and municipal bond underwriting that Cullen/Frost can capture.

Large-scale public works in Texas drive need for sophisticated treasury services and local banking partnerships, aligning with Cullen/Frost’s regional footprint and relationship banking model.

The bank’s loan growth and fee income correlate with project execution; Texas public construction spending rose 8% in 2024, enhancing deal flow for regional banks.

- Opportunities: commercial lending, municipal bond underwriting, treasury services

- Tailwind: $61B Texas transport plan, $110B federal infrastructure funds

- Impact: 8% rise in Texas public construction spending in 2024

Texas surfeit fuels regional bank growth: energy, infrastructure and rising NIMs

Texas pro-business policies and a $33.6B FY2024 surplus support regional banks; Fed rate hikes to 5.25–5.50% by Dec 2023 pushed system NIM near 3.0–3.5% (2025 YTD), while 2024 compliance costs rose industry-wide to $23.6B; Texas energy (≈40% of US crude, 2024) and $61B state transport plan plus $110B federal infrastructure spending drive loan and fee opportunities.

| Metric | Value (Year) |

|---|---|

| Texas surplus | $33.6B (FY2024) |

| Fed funds | 5.25–5.50% (Dec 2023) |

| System NIM | ~3.0–3.5% (2025 YTD) |

| Industry compliance spend | $23.6B (2024) |

| Texas crude share | ~40% (2024) |

| TX transport plan | $61B (2023) |

| Federal infra | $110B (BIL 2021) |

What is included in the product

Explores how macro-environmental factors uniquely affect Cullen/Frost Bank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform strategy, risk management, and opportunity identification for executives and investors.

Condenses Cullen/Frost Bank's PESTLE into a concise, shareable brief—visually segmented for quick interpretation in meetings and easily dropped into presentations or strategy packs for cross-team alignment.

Economic factors

Interest Rate Volatility

Through 2025, interest rate cycles shifted sharply: the federal funds rate rose from near 0% in 2021 to about 5.25–5.50% by late 2024–2025, compressing Frost Bank’s loan-deposit spread and directly affecting net interest income, which represented roughly 62% of Cullen/Frost’s 2024 revenue; rate volatility alters funding costs and loan yields, so active balance-sheet and repricing management is critical to preserve margins amid persistent inflation uncertainty.

Texas Economic Diversification

Texas GDP reached about 2.1 trillion USD in 2024, with technology, healthcare, and manufacturing growing faster than energy, supporting diversified loan demand for Cullen/Frost.

Cullen/Frost’s net interest income and loan growth depend on these sectors; diversification reduces exposure to oil price shocks after energy contributed ~14% of state GDP in 2024.

The bank tracks Texas unemployment at ~4.0% (2024) and regional GDP growth ~2.5% (2024) to gauge consumer and commercial credit needs.

Inflationary Pressure on Operating Costs

Persistent US inflation, with CPI at 3.4% y/y in 2024 and Texas urban CPI running higher (Austin ~4.0% in 2024), raises Cullen/Frost Bank’s wage and benefits costs as they compete for talent in Austin and Dallas; median tech salary inflation near 6%–8% forces higher technology investment, while third-party service and branch upkeep costs—commercial rent up ~5% y/y in major Texas metros in 2024—can compress NIM and margins if not offset by efficiency gains.

Real Estate Market Trends

The Texas real estate market—driving Cullen/Frost’s loan book—shows 2025 metro home prices up ~3% YoY while statewide inventory remains tight at ~2.3 months; commercial office vacancy in Dallas-Fort Worth rose to ~22% in 2024, pressuring CRE credit risk. Rising mortgage rates to ~6.5% (2024 peak) and higher cap rates require the bank to tighten underwriting and bolster loan-loss reserves.

- Residential prices +3% YoY (2025); inventory ~2.3 months

- Mortgage rates ~6.5% peak (2024)

- DFW office vacancy ~22% (2024)

- Underwriting tightened; higher capital/reserves

Consumer Spending and Debt Levels

Texas consumer health drives demand for Cullen/Frost retail banking; with 2025 median household income ~87,000 USD and state unemployment ~3.6% (Jan 2026), consumer loan originations remain strong but sensitive to shifts.

Household debt-to-income in Texas rose to ~110% in 2024, and rising balances risk higher delinquency and slower deposit growth for Frost.

Frost monitors consumer confidence (Texas consumer sentiment fell 6% in 2024) to forecast saving/spending changes.

- Median household income ~87,000 USD (2025)

- Texas unemployment ~3.6% (Jan 2026)

- Household debt-to-income ~110% (2024)

- Consumer sentiment fell ~6% in 2024

Higher rates squeeze NII amid Texas growth, rising wages and CRE stress

Higher rates (fed funds ~5.25–5.50% late-2024/2025) compressed NII (62% of 2024 revenue); Texas GDP ~$2.1T (2024) and unemployment ~4.0% (2024)/3.6% (Jan-2026) support diversified loan demand; CPI 3.4% (2024) and Austin ~4.0% raise wage/tech costs; housing +3% YoY (2025), mortgage rates ~6.5% (2024), DFW office vacancy ~22% (2024) heighten CRE risk.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| Texas GDP (2024) | $2.1T |

| CPI (US 2024) | 3.4% |

| Mortgage peak (2024) | 6.5% |

| DFW office vac (2024) | 22% |

Preview Before You Purchase

Cullen/Frost Bank PESTLE Analysis

The preview shown here is the exact Cullen/Frost Bank PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment purposes.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Gain strategic clarity with our PESTLE Analysis of Cullen/Frost Bank—spot regulatory, economic, and technological forces shaping its next moves and turn those insights into actionable strategy. Purchase the full report for a complete, editable breakdown ideal for investors, advisors, and executives seeking a competitive edge.

Political factors

Texas Regulatory Environment

Frost Bank’s Texas-centric operations tie it closely to state politics; Texas reported a $33.6 billion surplus in FY2024, supporting pro-business tax and regulatory policies that benefit regional banks through lower state-level tax burdens and streamlined licensing.

Texas’ pro-growth stance and 2023 corporate tax incentives helped deposit growth for regional banks, but shifts in state leadership or moves toward tighter financial oversight could constrain Frost’s lending and expansion plans.

Federal Monetary Policy Influence

Financial Industry Lobbying and Reform

Ongoing Washington debates over Dodd-Frank revisions and targeted bank reform raise compliance costs for mid-sized banks like Cullen/Frost; estimated industry compliance spending rose to roughly $23.6 billion in 2024, pressuring regional margins. Cullen/Frost must track federal proposals that could tighten or relax capital requirements—e.g., 2025 drafts discussed raising CET1-like buffers for regional banks by 50–150 bps. Party shifts historically change regulatory intensity: Republican control (2017–2018) correlated with eased rules, Democratic control (2021–2022) with tighter enforcement, creating policy-driven volatility in compliance planning.

Geopolitical Stability and Energy Policy

Texas's energy dominance ties Cullen/Frost's commercial loan exposure to oil and gas; as of 2024 Texas accounted for about 40% of U.S. crude production, so federal or international policy shifts materially affect portfolio risk.

Political tensions in major producers and U.S. energy policy changes drove Brent/WTI volatility in 2024–25—WTI ranged roughly $60–90/bbl—raising default risk for energy clients and weakening regional GDP growth.

- ~40% of U.S. crude from Texas (2024)

- WTI swing ~$60–$90/bbl (2024–25)

- Higher energy volatility → increased loan loss provisioning

Government Infrastructure Spending

Federal and Texas state commitments to infrastructure—highlighted by the 2021 Bipartisan Infrastructure Law allocating $110B to roads and bridges and Texas' $61B 2023 transportation plan—create demand for commercial loans and municipal bond underwriting that Cullen/Frost can capture.

Large-scale public works in Texas drive need for sophisticated treasury services and local banking partnerships, aligning with Cullen/Frost’s regional footprint and relationship banking model.

The bank’s loan growth and fee income correlate with project execution; Texas public construction spending rose 8% in 2024, enhancing deal flow for regional banks.

- Opportunities: commercial lending, municipal bond underwriting, treasury services

- Tailwind: $61B Texas transport plan, $110B federal infrastructure funds

- Impact: 8% rise in Texas public construction spending in 2024

Texas surfeit fuels regional bank growth: energy, infrastructure and rising NIMs

Texas pro-business policies and a $33.6B FY2024 surplus support regional banks; Fed rate hikes to 5.25–5.50% by Dec 2023 pushed system NIM near 3.0–3.5% (2025 YTD), while 2024 compliance costs rose industry-wide to $23.6B; Texas energy (≈40% of US crude, 2024) and $61B state transport plan plus $110B federal infrastructure spending drive loan and fee opportunities.

| Metric | Value (Year) |

|---|---|

| Texas surplus | $33.6B (FY2024) |

| Fed funds | 5.25–5.50% (Dec 2023) |

| System NIM | ~3.0–3.5% (2025 YTD) |

| Industry compliance spend | $23.6B (2024) |

| Texas crude share | ~40% (2024) |

| TX transport plan | $61B (2023) |

| Federal infra | $110B (BIL 2021) |

What is included in the product

Explores how macro-environmental factors uniquely affect Cullen/Frost Bank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform strategy, risk management, and opportunity identification for executives and investors.

Condenses Cullen/Frost Bank's PESTLE into a concise, shareable brief—visually segmented for quick interpretation in meetings and easily dropped into presentations or strategy packs for cross-team alignment.

Economic factors

Interest Rate Volatility

Through 2025, interest rate cycles shifted sharply: the federal funds rate rose from near 0% in 2021 to about 5.25–5.50% by late 2024–2025, compressing Frost Bank’s loan-deposit spread and directly affecting net interest income, which represented roughly 62% of Cullen/Frost’s 2024 revenue; rate volatility alters funding costs and loan yields, so active balance-sheet and repricing management is critical to preserve margins amid persistent inflation uncertainty.

Texas Economic Diversification

Texas GDP reached about 2.1 trillion USD in 2024, with technology, healthcare, and manufacturing growing faster than energy, supporting diversified loan demand for Cullen/Frost.

Cullen/Frost’s net interest income and loan growth depend on these sectors; diversification reduces exposure to oil price shocks after energy contributed ~14% of state GDP in 2024.

The bank tracks Texas unemployment at ~4.0% (2024) and regional GDP growth ~2.5% (2024) to gauge consumer and commercial credit needs.

Inflationary Pressure on Operating Costs

Persistent US inflation, with CPI at 3.4% y/y in 2024 and Texas urban CPI running higher (Austin ~4.0% in 2024), raises Cullen/Frost Bank’s wage and benefits costs as they compete for talent in Austin and Dallas; median tech salary inflation near 6%–8% forces higher technology investment, while third-party service and branch upkeep costs—commercial rent up ~5% y/y in major Texas metros in 2024—can compress NIM and margins if not offset by efficiency gains.

Real Estate Market Trends

The Texas real estate market—driving Cullen/Frost’s loan book—shows 2025 metro home prices up ~3% YoY while statewide inventory remains tight at ~2.3 months; commercial office vacancy in Dallas-Fort Worth rose to ~22% in 2024, pressuring CRE credit risk. Rising mortgage rates to ~6.5% (2024 peak) and higher cap rates require the bank to tighten underwriting and bolster loan-loss reserves.

- Residential prices +3% YoY (2025); inventory ~2.3 months

- Mortgage rates ~6.5% peak (2024)

- DFW office vacancy ~22% (2024)

- Underwriting tightened; higher capital/reserves

Consumer Spending and Debt Levels

Texas consumer health drives demand for Cullen/Frost retail banking; with 2025 median household income ~87,000 USD and state unemployment ~3.6% (Jan 2026), consumer loan originations remain strong but sensitive to shifts.

Household debt-to-income in Texas rose to ~110% in 2024, and rising balances risk higher delinquency and slower deposit growth for Frost.

Frost monitors consumer confidence (Texas consumer sentiment fell 6% in 2024) to forecast saving/spending changes.

- Median household income ~87,000 USD (2025)

- Texas unemployment ~3.6% (Jan 2026)

- Household debt-to-income ~110% (2024)

- Consumer sentiment fell ~6% in 2024

Higher rates squeeze NII amid Texas growth, rising wages and CRE stress

Higher rates (fed funds ~5.25–5.50% late-2024/2025) compressed NII (62% of 2024 revenue); Texas GDP ~$2.1T (2024) and unemployment ~4.0% (2024)/3.6% (Jan-2026) support diversified loan demand; CPI 3.4% (2024) and Austin ~4.0% raise wage/tech costs; housing +3% YoY (2025), mortgage rates ~6.5% (2024), DFW office vacancy ~22% (2024) heighten CRE risk.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| Texas GDP (2024) | $2.1T |

| CPI (US 2024) | 3.4% |

| Mortgage peak (2024) | 6.5% |

| DFW office vac (2024) | 22% |

Preview Before You Purchase

Cullen/Frost Bank PESTLE Analysis

The preview shown here is the exact Cullen/Frost Bank PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment purposes.