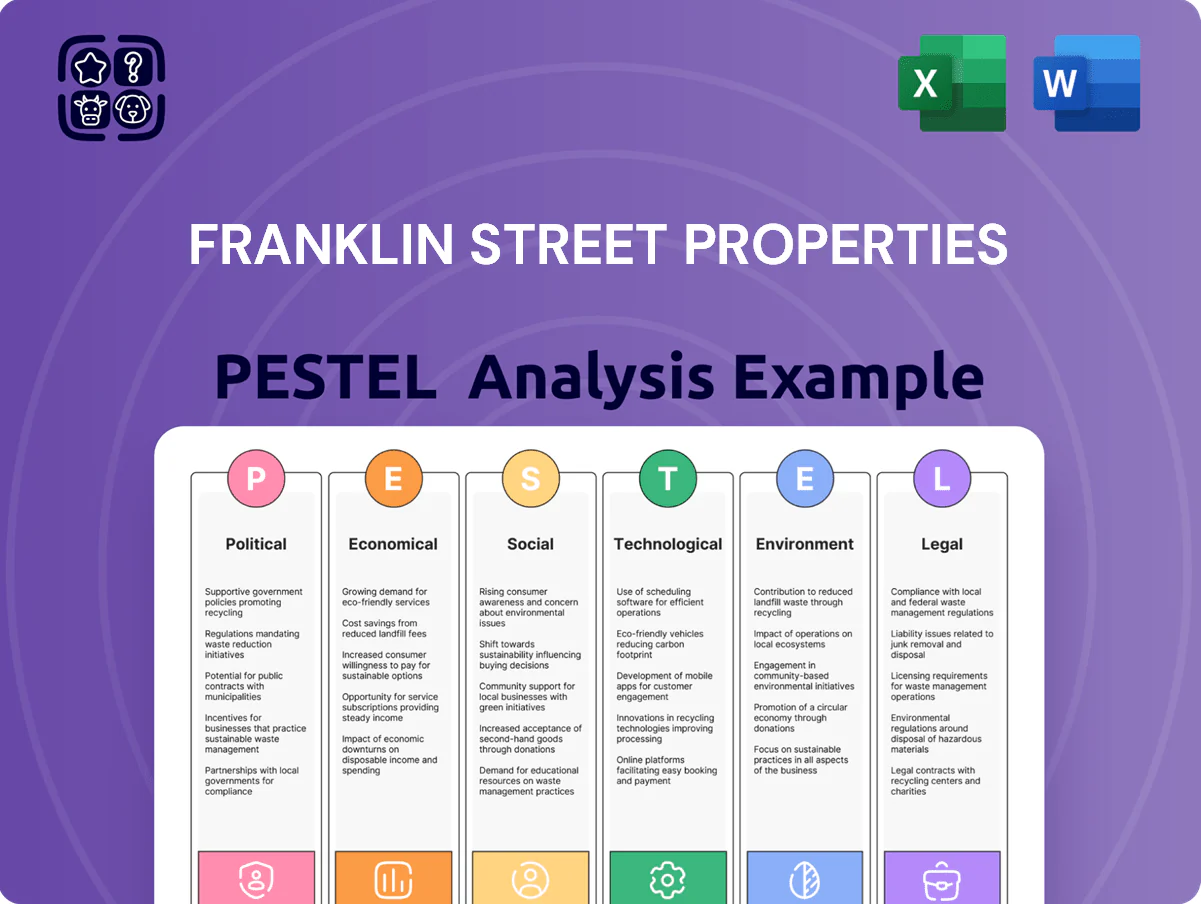

Franklin Street Properties PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and emerging tech trends are reshaping Franklin Street Properties' prospects in our concise PESTLE summary—perfect for investors and strategists seeking fast, actionable context; purchase the full analysis to access the detailed insights, risks, and opportunities that drive smarter decisions.

Political factors

Federal tax policy for REITs

The stability of the Tax Cuts and Jobs Act provisions through 2025 is material for Franklin Street Properties; the 20% pass-through deduction for REIT dividends, which boosted effective yields for many retail investors, could be curtailed by proposed congressional tax revisions that would cut after-tax dividend yields by roughly 3–5 percentage points on a 6% nominal yield. Management must monitor pending bills and model scenarios where loss of this deduction raises investor required returns and compresses NAV and share price, especially given REIT sector cap rates averaging 5.2% in 2024–25.

Local zoning and development incentives

Franklin Street’s Sunbelt/Mountain West focus benefits from local zoning and development incentives—2024 municipal tax abatements and expedited permitting averaged 10–18% cost reductions for commercial projects in target metros, bolstering mixed-use and infill yields. These incentives sustain lease-up velocity and NOI growth, but shifts in city councils or planning boards could delay approvals and raise redevelopment capex, impacting projected IRRs on expansion sites.

Government work-from-home mandates

Government work-from-home mandates, though less common than private-sector policies, set precedents that influence broader market behavior; as of 2024, 18% of major US municipalities issued formal return-to-office guidance supporting in-person work, shaping demand in FSP markets.

In regions where Franklin Street Properties operates, political pressure to revive downtown cores has led to local mandates and incentives—tax credits and transit subsidies worth up to $25–50 million cumulatively in 2023–2024—to boost office occupancy.

This political backing is critical for sustaining urban vibrancy around FSP assets, where office utilization rates recovered to an average of 68% in 2025 in cities with active government return-to-office measures.

Geopolitical stability and foreign investment

U.S. real estate's safe-haven appeal depends on federal foreign policy and trade ties; in 2024–2025 foreign capital into U.S. commercial real estate fell roughly 35% from 2019 levels, tightening liquidity for offices.

Late-2025 geopolitical tensions (e.g., U.S.-China relations) are pressuring cross-border investment, affecting cap rates—core office cap rates widened ~50–75 bps in major markets in 2024–2025.

Franklin Street must track macro-political shifts since a 1% rise in cap rates can cut asset values by ~10% for typical leveraged office holdings.

- Foreign investment down ~35% vs 2019

- Office cap rates widened ~50–75 bps (2024–2025)

- 1% cap rate rise ≈ 10% value decline

Infrastructure spending in target markets

Federal and state infrastructure bills—including the 2021 Bipartisan Infrastructure Law with $550B new spending—boost accessibility and can raise values of Franklin Street Properties office holdings by improving roads, transit and utilities in target markets.

Sunbelt infill locations stand to gain from recent state-level allocations (e.g., TX and FL projects totaling $60B+ through 2024), enhancing tenant demand and rental premiums.

Political prioritization and sustained funding flow directly correlate with long-term portfolio appreciation and cap rate compression for FSP.

- 2021 federal law: $550B new infrastructure spending

- TX/FL state projects 2022–2024: $60B+ combined

- Improved transit/utilities → higher rents, lower vacancy, cap rate compression

Policy shifts trim REIT yields but infrastructure and local abatements bolster returns

Political factors: tax-policy risk (TCJA pass-through deduction potential loss could cut after-tax REIT yields ~3–5 ppt on a 6% nominal yield), local incentives (2024 abatements cut project costs 10–18%), foreign capital drop (~35% vs 2019) widening office cap rates ~50–75 bps (2024–25), infrastructure spending (Bipartisan Infra Law $550B; TX/FL $60B+ to 2024) supporting rent and NAV.

| Factor | Key Metric | Impact |

|---|---|---|

| Tax deduction | 3–5 ppt yield loss | Higher required returns, NAV pressure |

| Local incentives | 10–18% cost reduction | Faster lease-up, higher IRR |

| Foreign capital | ↓35% vs 2019 | Liquidity squeeze, cap-rate widening 50–75 bps |

| Infrastructure | $550B federal; $60B+ TX/FL | Supports rents, lowers vacancy |

What is included in the product

Explores how external macro-environmental factors uniquely affect Franklin Street Properties across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and regional market trends to pinpoint risks and opportunities.

Concise PESTLE summary of Franklin Street Properties, visually segmented for quick interpretation and editable for local context—ideal for dropping into presentations or sharing across teams to streamline external risk discussions and strategic planning.

Economic factors

Interest rate environment and debt servicing

Employment growth in the Sunbelt and Mountain West

Franklin Street Properties' strategy is concentrated in Sunbelt and Mountain West hubs—notably Phoenix, Dallas and Denver—where 2024-25 employment expanded: Phoenix metro added ~85,000 jobs (3.4% y/y), Dallas-Fort Worth ~120,000 (2.8% y/y) and Denver ~48,000 (2.6% y/y), led by tech and financial services growth driving demand for Class A office space.

These sectors' expansion supported office market fundamentals with Q4 2025 metro office vacancy rates below national average (Phoenix 15.2%, Dallas 17.0%, Denver 14.8%), sustaining rental income for FSP.

Conversely, a regional downturn—e.g., a 2% job decline—would likely depress occupancy and rents, directly threatening FSP's cash flows given geographic concentration risk.

Inflationary pressure on operating expenses

Rising labor, materials and utilities lifted US CPI to 3.4% year-over-year in Dec 2025, squeezing office REIT NOI; Franklin Street reported same-store NOI decline of 2.1% FY2025, citing higher maintenance and energy costs. Efficient property management and expense controls plus lease structures with CPI-linked escalators are critical to protect margins. Franklin Street’s pass-through ability hinges on local market rent recovery—vacancy-weighted rents in key metros rose just 1.8% in 2025.

Office market vacancy and absorption rates

The shift to hybrid work has driven U.S. office vacancy to about 16.6% nationally in Q4 2025, with Class A vacancy near 12% versus Class B/C at ~20%, creating a bifurcated market where premier assets outperform legacy inventory.

FSP must prioritize asset quality and selective capital expenditures as market-wide vacancies remain elevated; national net absorption was negative ~45 msf in 2024 but showed pockets of positive absorption in Sun Belt markets through 2025.

Monitoring local absorption—e.g., Austin and Raleigh posted positive absorption of 1.2–1.8 msf in 2025—will guide FSP disposition and acquisition choices toward high-demand submarkets.

- National office vacancy ~16.6% (Q4 2025)

- Class A vacancy ~12%; Class B/C ~20%

- Net absorption negative ~45 msf in 2024; selective Sun Belt gains in 2025

- Focus acquisitions on submarkets with positive absorption (e.g., Austin, Raleigh)

Capital market liquidity and asset pricing

Capital availability for office real estate remained constrained at end-2025, with CRE transaction volume down about 28% year-over-year and cap rates for suburban office averaging 8.1% versus 6.4% in 2021 according to RCA data, pressuring FSP’s ability to recycle assets.

FSP’s execution of strategic dispositions hinges on private and institutional liquidity; distressed sellers and cautious LPs widened bid-ask spreads by an estimated 150–250 bps in 2025, reducing achievable valuations.

Heightened economic volatility and higher Treasury yields (10-year averaging ~4.5% in H2 2025) increased financing costs and made timely capital recycling more difficult for FSP.

- CRE transaction volume -28% YoY (2025)

- Suburban office cap rate ~8.1% (2025)

- Bid-ask spread widened 150–250 bps (2025)

- 10y Treasury ~4.5% H2 2025

Higher-for-longer rates squeeze CRE: NOI down, vacancies up, cap rates near 8%

Higher-for-longer rates (Fed 5.25–5.50% end-2025) raised WACC, widening spreads on 60–70% of FSP debt maturing through 2026; same-store NOI -2.1% FY2025 amid CPI 3.4% (Dec 2025). Sun Belt rent growth modest (vacancy: Phoenix 15.2%, Dallas 17.0%, Denver 14.8%; national 16.6%). CRE volume -28% YoY; suburban cap rate ~8.1%; 10y Treasury ~4.5% H2 2025.

| Metric | 2025 |

|---|---|

| Fed target | 5.25–5.50% |

| NoI change | -2.1% |

| National vacancy | 16.6% |

| 10y Treasury | ~4.5% |

Preview Before You Purchase

Franklin Street Properties PESTLE Analysis

The preview shown here is the exact Franklin Street Properties PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and emerging tech trends are reshaping Franklin Street Properties' prospects in our concise PESTLE summary—perfect for investors and strategists seeking fast, actionable context; purchase the full analysis to access the detailed insights, risks, and opportunities that drive smarter decisions.

Political factors

Federal tax policy for REITs

The stability of the Tax Cuts and Jobs Act provisions through 2025 is material for Franklin Street Properties; the 20% pass-through deduction for REIT dividends, which boosted effective yields for many retail investors, could be curtailed by proposed congressional tax revisions that would cut after-tax dividend yields by roughly 3–5 percentage points on a 6% nominal yield. Management must monitor pending bills and model scenarios where loss of this deduction raises investor required returns and compresses NAV and share price, especially given REIT sector cap rates averaging 5.2% in 2024–25.

Local zoning and development incentives

Franklin Street’s Sunbelt/Mountain West focus benefits from local zoning and development incentives—2024 municipal tax abatements and expedited permitting averaged 10–18% cost reductions for commercial projects in target metros, bolstering mixed-use and infill yields. These incentives sustain lease-up velocity and NOI growth, but shifts in city councils or planning boards could delay approvals and raise redevelopment capex, impacting projected IRRs on expansion sites.

Government work-from-home mandates

Government work-from-home mandates, though less common than private-sector policies, set precedents that influence broader market behavior; as of 2024, 18% of major US municipalities issued formal return-to-office guidance supporting in-person work, shaping demand in FSP markets.

In regions where Franklin Street Properties operates, political pressure to revive downtown cores has led to local mandates and incentives—tax credits and transit subsidies worth up to $25–50 million cumulatively in 2023–2024—to boost office occupancy.

This political backing is critical for sustaining urban vibrancy around FSP assets, where office utilization rates recovered to an average of 68% in 2025 in cities with active government return-to-office measures.

Geopolitical stability and foreign investment

U.S. real estate's safe-haven appeal depends on federal foreign policy and trade ties; in 2024–2025 foreign capital into U.S. commercial real estate fell roughly 35% from 2019 levels, tightening liquidity for offices.

Late-2025 geopolitical tensions (e.g., U.S.-China relations) are pressuring cross-border investment, affecting cap rates—core office cap rates widened ~50–75 bps in major markets in 2024–2025.

Franklin Street must track macro-political shifts since a 1% rise in cap rates can cut asset values by ~10% for typical leveraged office holdings.

- Foreign investment down ~35% vs 2019

- Office cap rates widened ~50–75 bps (2024–2025)

- 1% cap rate rise ≈ 10% value decline

Infrastructure spending in target markets

Federal and state infrastructure bills—including the 2021 Bipartisan Infrastructure Law with $550B new spending—boost accessibility and can raise values of Franklin Street Properties office holdings by improving roads, transit and utilities in target markets.

Sunbelt infill locations stand to gain from recent state-level allocations (e.g., TX and FL projects totaling $60B+ through 2024), enhancing tenant demand and rental premiums.

Political prioritization and sustained funding flow directly correlate with long-term portfolio appreciation and cap rate compression for FSP.

- 2021 federal law: $550B new infrastructure spending

- TX/FL state projects 2022–2024: $60B+ combined

- Improved transit/utilities → higher rents, lower vacancy, cap rate compression

Policy shifts trim REIT yields but infrastructure and local abatements bolster returns

Political factors: tax-policy risk (TCJA pass-through deduction potential loss could cut after-tax REIT yields ~3–5 ppt on a 6% nominal yield), local incentives (2024 abatements cut project costs 10–18%), foreign capital drop (~35% vs 2019) widening office cap rates ~50–75 bps (2024–25), infrastructure spending (Bipartisan Infra Law $550B; TX/FL $60B+ to 2024) supporting rent and NAV.

| Factor | Key Metric | Impact |

|---|---|---|

| Tax deduction | 3–5 ppt yield loss | Higher required returns, NAV pressure |

| Local incentives | 10–18% cost reduction | Faster lease-up, higher IRR |

| Foreign capital | ↓35% vs 2019 | Liquidity squeeze, cap-rate widening 50–75 bps |

| Infrastructure | $550B federal; $60B+ TX/FL | Supports rents, lowers vacancy |

What is included in the product

Explores how external macro-environmental factors uniquely affect Franklin Street Properties across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and regional market trends to pinpoint risks and opportunities.

Concise PESTLE summary of Franklin Street Properties, visually segmented for quick interpretation and editable for local context—ideal for dropping into presentations or sharing across teams to streamline external risk discussions and strategic planning.

Economic factors

Interest rate environment and debt servicing

Employment growth in the Sunbelt and Mountain West

Franklin Street Properties' strategy is concentrated in Sunbelt and Mountain West hubs—notably Phoenix, Dallas and Denver—where 2024-25 employment expanded: Phoenix metro added ~85,000 jobs (3.4% y/y), Dallas-Fort Worth ~120,000 (2.8% y/y) and Denver ~48,000 (2.6% y/y), led by tech and financial services growth driving demand for Class A office space.

These sectors' expansion supported office market fundamentals with Q4 2025 metro office vacancy rates below national average (Phoenix 15.2%, Dallas 17.0%, Denver 14.8%), sustaining rental income for FSP.

Conversely, a regional downturn—e.g., a 2% job decline—would likely depress occupancy and rents, directly threatening FSP's cash flows given geographic concentration risk.

Inflationary pressure on operating expenses

Rising labor, materials and utilities lifted US CPI to 3.4% year-over-year in Dec 2025, squeezing office REIT NOI; Franklin Street reported same-store NOI decline of 2.1% FY2025, citing higher maintenance and energy costs. Efficient property management and expense controls plus lease structures with CPI-linked escalators are critical to protect margins. Franklin Street’s pass-through ability hinges on local market rent recovery—vacancy-weighted rents in key metros rose just 1.8% in 2025.

Office market vacancy and absorption rates

The shift to hybrid work has driven U.S. office vacancy to about 16.6% nationally in Q4 2025, with Class A vacancy near 12% versus Class B/C at ~20%, creating a bifurcated market where premier assets outperform legacy inventory.

FSP must prioritize asset quality and selective capital expenditures as market-wide vacancies remain elevated; national net absorption was negative ~45 msf in 2024 but showed pockets of positive absorption in Sun Belt markets through 2025.

Monitoring local absorption—e.g., Austin and Raleigh posted positive absorption of 1.2–1.8 msf in 2025—will guide FSP disposition and acquisition choices toward high-demand submarkets.

- National office vacancy ~16.6% (Q4 2025)

- Class A vacancy ~12%; Class B/C ~20%

- Net absorption negative ~45 msf in 2024; selective Sun Belt gains in 2025

- Focus acquisitions on submarkets with positive absorption (e.g., Austin, Raleigh)

Capital market liquidity and asset pricing

Capital availability for office real estate remained constrained at end-2025, with CRE transaction volume down about 28% year-over-year and cap rates for suburban office averaging 8.1% versus 6.4% in 2021 according to RCA data, pressuring FSP’s ability to recycle assets.

FSP’s execution of strategic dispositions hinges on private and institutional liquidity; distressed sellers and cautious LPs widened bid-ask spreads by an estimated 150–250 bps in 2025, reducing achievable valuations.

Heightened economic volatility and higher Treasury yields (10-year averaging ~4.5% in H2 2025) increased financing costs and made timely capital recycling more difficult for FSP.

- CRE transaction volume -28% YoY (2025)

- Suburban office cap rate ~8.1% (2025)

- Bid-ask spread widened 150–250 bps (2025)

- 10y Treasury ~4.5% H2 2025

Higher-for-longer rates squeeze CRE: NOI down, vacancies up, cap rates near 8%

Higher-for-longer rates (Fed 5.25–5.50% end-2025) raised WACC, widening spreads on 60–70% of FSP debt maturing through 2026; same-store NOI -2.1% FY2025 amid CPI 3.4% (Dec 2025). Sun Belt rent growth modest (vacancy: Phoenix 15.2%, Dallas 17.0%, Denver 14.8%; national 16.6%). CRE volume -28% YoY; suburban cap rate ~8.1%; 10y Treasury ~4.5% H2 2025.

| Metric | 2025 |

|---|---|

| Fed target | 5.25–5.50% |

| NoI change | -2.1% |

| National vacancy | 16.6% |

| 10y Treasury | ~4.5% |

Preview Before You Purchase

Franklin Street Properties PESTLE Analysis

The preview shown here is the exact Franklin Street Properties PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.