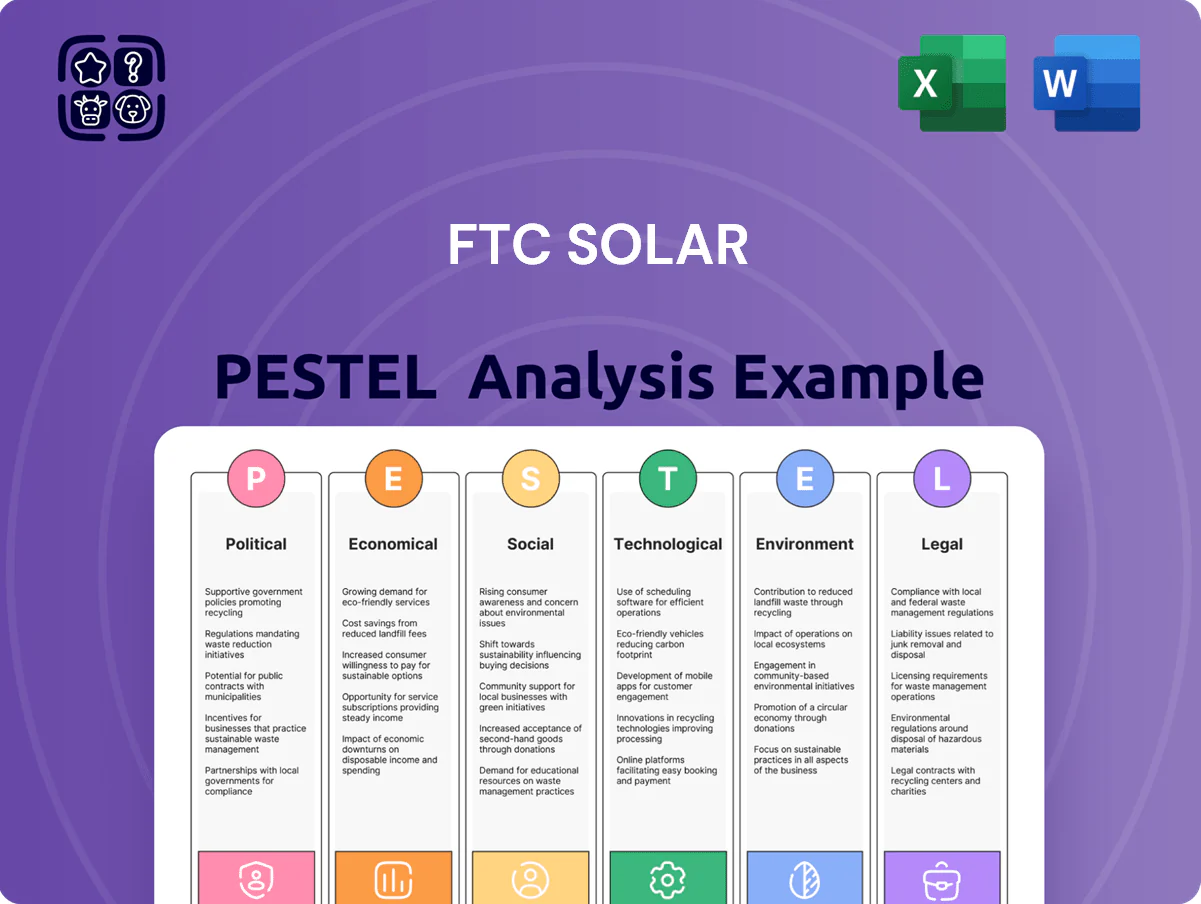

FTC Solar PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic trends, and emerging technologies are reshaping FTC Solar’s opportunities and risks—our concise PESTLE highlights the most critical external forces you need to know; purchase the full analysis for a complete, actionable breakdown to inform investing, strategy, or due diligence.

Political factors

Impact of the One Big Beautiful Bill Act

The One Big Beautiful Bill Act, enacted July 2025, accelerated phase-out of solar tax credits, cutting the ITC from 30% to 18% after 2025 and creating mid-2026 safe-harbor deadlines; this spurred a 22% surge in announced utility-scale projects in H2 2025 as developers raced to secure incentives.

Foreign Entity of Concern FEOC Regulations

Late-2025 FEOC rules cap nonqualifying foreign-sourced equipment to 60% in 2026, declining thereafter, targeting China, North Korea, Iran; projects exceeding limits lose federal tax-credit eligibility (Investment Tax Credit exposure potentially in the billions for the solar sector).

FTC Solar is accelerating US supply partnerships and onshoring steel/component sourcing; the company reported stepping up domestic purchases by an estimated 25% in 2025 to mitigate FEOC-driven revenue risk and preserve tax-credit-linked project economics.

Permitting Reform and Infrastructure Speed

Political moves in late 2025 accelerated permitting reform to unclog energy infrastructure projects, with proposed rules capping agency decisions at 150 days to cut utility-scale solar development timelines.

For FTC Solar, faster approvals could speed conversion of its multi-million-dollar backlog—about $1.2 billion reported YE 2024—into revenue, potentially shortening project cycles by 6–12 months and improving cash flow.

State-Level Policy Divergence

As federal renewables support contracted in 2025, state mandates and incentives became crucial for market stability; California, Texas and Florida still represent over 40% of US utility-scale solar capacity additions in 2024–25 combined.

Progressive states maintain aggressive RPS targets—California 60% by 2030, New York 70% by 2030—while several states cut subsidies, fragmenting the domestic market and raising deployment uncertainty.

FTC Solar should prioritize engineering and sales in states with favorable policy and pipeline concentration: CA, TX, NY, and NJ, where 2024 project pipelines exceeded 6 GW collectively.

- State policy now drives site selection and CAPEX allocation

- CA/TX/FL/NY hold 40%+ of 2024–25 additions

- Target states with robust RPS and active pipelines (CA, TX, NY, NJ)

Trade Protectionism and Tariff Risks

The 2025 political landscape saw rising protectionism; U.S. and EU tariffs on imported solar components and steel rose to average rates of 10–25%, pushing tracker bill-of-materials costs up by an estimated 8–12% industry-wide and compressing margins for suppliers.

FTC Solar’s 2024–25 acquisition of a majority stake in Alpha Steel is a strategic hedge: vertical integration reduced exposure to tariffs, lowering inbound steel cost volatility and aiming to preserve gross margins projected to improve by ~200–400 basis points versus a tariff-exposed baseline.

- Tariffs 2025: 10–25% on solar components/steel

- Estimated BOM cost rise: +8–12%

- FTC move: majority stake in Alpha Steel (2024–25)

- Projected margin benefit: +200–400 bps vs exposed peers

FTC Solar onshores supply, boosts US buys 25%—acquires Alpha Steel to protect 200–400bps

Federal tax-credit cuts (ITC 30%→18% post-2025) and FEOC foreign-content caps drove onshoring and partnerships; FTC Solar raised US purchases ~25% in 2025 and acquired Alpha Steel to hedge 10–25% tariff impacts, protecting ~200–400 bps margin; permitting reform (150-day cap) could shorten backlog conversion (~$1.2B YE2024) by 6–12 months; state RPS (CA 60%, NY 70% by 2030) concentrate pipeline risk.

| Metric | Value |

|---|---|

| FTC backlog YE2024 | $1.2B |

| US purchases ↑2025 | ~25% |

| Tariff range 2025 | 10–25% |

| Projected margin benefit | +200–400 bps |

What is included in the product

Explores how macro-environmental factors uniquely affect FTC Solar across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section tied to current market and regulatory trends.

A concise, visually segmented PESTLE summary for FTC Solar that simplifies external risk assessment and market positioning, ready to drop into presentations or share across teams for quick strategic alignment.

Economic factors

Rapid Revenue Growth and Market Rebound

FTC Solar recorded a dramatic economic turnaround in 2025, with Q3 revenue jumping more than 150% year-over-year to roughly $120 million as backlog-cleared project shipments accelerated.

Record solar installations in the US and Australia—installations up ~40% and ~35% respectively in 2025—drove much of that demand, reversing the 2024 slump.

The company’s improved gross margin, rising to about 18% in H2 2025, and stronger cash flow underpin a more optimistic financial trajectory into 2026.

Persistence of Net Losses and Margin Pressure

Despite 48% revenue growth in 2025, FTC Solar reported GAAP net losses through Q4 2025, totaling a cumulative loss of $112 million since 2023, underscoring challenges to profitability.

Non-GAAP gross margin turned positive at 6.2% in Q3 2025—the first positive reading in years—but operating expenses of $22.4 million and interest expense of $5.1 million in FY2025 kept overall margins pressured.

Investors are watching whether scale can dilute fixed costs: management targets break-even cash flow by late 2026, implying rapid revenue expansion and margin improvement are required to convert top-line gains into sustainable earnings.

Strategic Financing and Liquidity Management

The company secured a 75 million dollar strategic financing facility in July 2025 to support its operational ramp-up and liquidity needs.

By late 2025 FTC Solar reported a backlog of approximately 462 million dollars, intensifying working capital requirements funded by the facility.

However, the high cost of the debt and attached warrants increases long-term financial pressure, necessitating stronger cash flow generation to service obligations and reduce dilution risk.

Rising Electricity Rates and Solar Value Proposition

The U.S. EIA forecasted a 7 percent rise in wholesale power prices for 2025, boosting solar’s economic case as grid electricity costs climb.

Higher wholesale rates lower the comparative LCOE threshold, making solar projects with FTC Solar’s high-efficiency trackers more attractive to utilities seeking cost-effective capacity.

Developers facing rising power costs are likely to prioritize yield-maximizing tracker tech; FTC Solar benefits as demand for performance-driven solutions grows.

- 7% EIA 2025 wholesale price increase

- Improved solar LCOE competitiveness vs. grid

- Higher demand for yield-maximizing trackers

Global Supply Chain and Steel Price Volatility

FTC Solar's tracker costs are highly steel-dependent, with steel historically comprising roughly 30–40% of tracker BOM value; steel price swings of 20–30% in 2024–2025 materially change margin profiles.

By moving to full ownership of Alpha Steel, FTC aims to vertically integrate supply, secure ~50–70% of its steel needs internally and target cost reductions of 5–10% versus market purchases.

This strategy reduces exposure to 2025 steel volatility—global HRC prices ranged ~$600–$900/ton in 2024–2025—helping stabilize COGS and forecastability.

- Steel = ~30–40% of tracker BOM

- Alpha Steel integration to cover ~50–70% of steel needs

- Targeted cost savings 5–10%

- HRC price band ~$600–$900/ton (2024–2025)

FTC Solar: 2025 Revenue Surge, Margin Recovery but GAAP Losses and Steel Risk

FTC Solar’s 2025 revenue surge (~48% y/y; Q3 ≈$120M) improved gross margins (non-GAAP 6.2% Q3; H2 ~18%) but GAAP net losses persisted (cumulative ~$112M since 2023) as Opex and interest weighed.

Backlog ~$462M and a $75M financing facility support growth but increase leverage and dilution risk; management targets break-even cash flow by late 2026.

Steel (30–40% BOM) volatility (HRC ~$600–$900/ton) drives Alpha Steel integration to cover 50–70% needs and seek 5–10% cost savings.

| Metric | 2025 |

|---|---|

| Revenue growth | ~48% y/y |

| Q3 revenue | $120M |

| Backlog | $462M |

| Cumulative GAAP loss | $112M |

| Non-GAAP gross margin (Q3) | 6.2% |

| H2 gross margin | ~18% |

| Financing facility | $75M |

| Steel HRC price | $600–$900/ton |

Same Document Delivered

FTC Solar PESTLE Analysis

The preview shown here is the exact FTC Solar PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in this preview are identical to the file you’ll download immediately after payment; no placeholders, no teasers, just the final product.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic trends, and emerging technologies are reshaping FTC Solar’s opportunities and risks—our concise PESTLE highlights the most critical external forces you need to know; purchase the full analysis for a complete, actionable breakdown to inform investing, strategy, or due diligence.

Political factors

Impact of the One Big Beautiful Bill Act

The One Big Beautiful Bill Act, enacted July 2025, accelerated phase-out of solar tax credits, cutting the ITC from 30% to 18% after 2025 and creating mid-2026 safe-harbor deadlines; this spurred a 22% surge in announced utility-scale projects in H2 2025 as developers raced to secure incentives.

Foreign Entity of Concern FEOC Regulations

Late-2025 FEOC rules cap nonqualifying foreign-sourced equipment to 60% in 2026, declining thereafter, targeting China, North Korea, Iran; projects exceeding limits lose federal tax-credit eligibility (Investment Tax Credit exposure potentially in the billions for the solar sector).

FTC Solar is accelerating US supply partnerships and onshoring steel/component sourcing; the company reported stepping up domestic purchases by an estimated 25% in 2025 to mitigate FEOC-driven revenue risk and preserve tax-credit-linked project economics.

Permitting Reform and Infrastructure Speed

Political moves in late 2025 accelerated permitting reform to unclog energy infrastructure projects, with proposed rules capping agency decisions at 150 days to cut utility-scale solar development timelines.

For FTC Solar, faster approvals could speed conversion of its multi-million-dollar backlog—about $1.2 billion reported YE 2024—into revenue, potentially shortening project cycles by 6–12 months and improving cash flow.

State-Level Policy Divergence

As federal renewables support contracted in 2025, state mandates and incentives became crucial for market stability; California, Texas and Florida still represent over 40% of US utility-scale solar capacity additions in 2024–25 combined.

Progressive states maintain aggressive RPS targets—California 60% by 2030, New York 70% by 2030—while several states cut subsidies, fragmenting the domestic market and raising deployment uncertainty.

FTC Solar should prioritize engineering and sales in states with favorable policy and pipeline concentration: CA, TX, NY, and NJ, where 2024 project pipelines exceeded 6 GW collectively.

- State policy now drives site selection and CAPEX allocation

- CA/TX/FL/NY hold 40%+ of 2024–25 additions

- Target states with robust RPS and active pipelines (CA, TX, NY, NJ)

Trade Protectionism and Tariff Risks

The 2025 political landscape saw rising protectionism; U.S. and EU tariffs on imported solar components and steel rose to average rates of 10–25%, pushing tracker bill-of-materials costs up by an estimated 8–12% industry-wide and compressing margins for suppliers.

FTC Solar’s 2024–25 acquisition of a majority stake in Alpha Steel is a strategic hedge: vertical integration reduced exposure to tariffs, lowering inbound steel cost volatility and aiming to preserve gross margins projected to improve by ~200–400 basis points versus a tariff-exposed baseline.

- Tariffs 2025: 10–25% on solar components/steel

- Estimated BOM cost rise: +8–12%

- FTC move: majority stake in Alpha Steel (2024–25)

- Projected margin benefit: +200–400 bps vs exposed peers

FTC Solar onshores supply, boosts US buys 25%—acquires Alpha Steel to protect 200–400bps

Federal tax-credit cuts (ITC 30%→18% post-2025) and FEOC foreign-content caps drove onshoring and partnerships; FTC Solar raised US purchases ~25% in 2025 and acquired Alpha Steel to hedge 10–25% tariff impacts, protecting ~200–400 bps margin; permitting reform (150-day cap) could shorten backlog conversion (~$1.2B YE2024) by 6–12 months; state RPS (CA 60%, NY 70% by 2030) concentrate pipeline risk.

| Metric | Value |

|---|---|

| FTC backlog YE2024 | $1.2B |

| US purchases ↑2025 | ~25% |

| Tariff range 2025 | 10–25% |

| Projected margin benefit | +200–400 bps |

What is included in the product

Explores how macro-environmental factors uniquely affect FTC Solar across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section tied to current market and regulatory trends.

A concise, visually segmented PESTLE summary for FTC Solar that simplifies external risk assessment and market positioning, ready to drop into presentations or share across teams for quick strategic alignment.

Economic factors

Rapid Revenue Growth and Market Rebound

FTC Solar recorded a dramatic economic turnaround in 2025, with Q3 revenue jumping more than 150% year-over-year to roughly $120 million as backlog-cleared project shipments accelerated.

Record solar installations in the US and Australia—installations up ~40% and ~35% respectively in 2025—drove much of that demand, reversing the 2024 slump.

The company’s improved gross margin, rising to about 18% in H2 2025, and stronger cash flow underpin a more optimistic financial trajectory into 2026.

Persistence of Net Losses and Margin Pressure

Despite 48% revenue growth in 2025, FTC Solar reported GAAP net losses through Q4 2025, totaling a cumulative loss of $112 million since 2023, underscoring challenges to profitability.

Non-GAAP gross margin turned positive at 6.2% in Q3 2025—the first positive reading in years—but operating expenses of $22.4 million and interest expense of $5.1 million in FY2025 kept overall margins pressured.

Investors are watching whether scale can dilute fixed costs: management targets break-even cash flow by late 2026, implying rapid revenue expansion and margin improvement are required to convert top-line gains into sustainable earnings.

Strategic Financing and Liquidity Management

The company secured a 75 million dollar strategic financing facility in July 2025 to support its operational ramp-up and liquidity needs.

By late 2025 FTC Solar reported a backlog of approximately 462 million dollars, intensifying working capital requirements funded by the facility.

However, the high cost of the debt and attached warrants increases long-term financial pressure, necessitating stronger cash flow generation to service obligations and reduce dilution risk.

Rising Electricity Rates and Solar Value Proposition

The U.S. EIA forecasted a 7 percent rise in wholesale power prices for 2025, boosting solar’s economic case as grid electricity costs climb.

Higher wholesale rates lower the comparative LCOE threshold, making solar projects with FTC Solar’s high-efficiency trackers more attractive to utilities seeking cost-effective capacity.

Developers facing rising power costs are likely to prioritize yield-maximizing tracker tech; FTC Solar benefits as demand for performance-driven solutions grows.

- 7% EIA 2025 wholesale price increase

- Improved solar LCOE competitiveness vs. grid

- Higher demand for yield-maximizing trackers

Global Supply Chain and Steel Price Volatility

FTC Solar's tracker costs are highly steel-dependent, with steel historically comprising roughly 30–40% of tracker BOM value; steel price swings of 20–30% in 2024–2025 materially change margin profiles.

By moving to full ownership of Alpha Steel, FTC aims to vertically integrate supply, secure ~50–70% of its steel needs internally and target cost reductions of 5–10% versus market purchases.

This strategy reduces exposure to 2025 steel volatility—global HRC prices ranged ~$600–$900/ton in 2024–2025—helping stabilize COGS and forecastability.

- Steel = ~30–40% of tracker BOM

- Alpha Steel integration to cover ~50–70% of steel needs

- Targeted cost savings 5–10%

- HRC price band ~$600–$900/ton (2024–2025)

FTC Solar: 2025 Revenue Surge, Margin Recovery but GAAP Losses and Steel Risk

FTC Solar’s 2025 revenue surge (~48% y/y; Q3 ≈$120M) improved gross margins (non-GAAP 6.2% Q3; H2 ~18%) but GAAP net losses persisted (cumulative ~$112M since 2023) as Opex and interest weighed.

Backlog ~$462M and a $75M financing facility support growth but increase leverage and dilution risk; management targets break-even cash flow by late 2026.

Steel (30–40% BOM) volatility (HRC ~$600–$900/ton) drives Alpha Steel integration to cover 50–70% needs and seek 5–10% cost savings.

| Metric | 2025 |

|---|---|

| Revenue growth | ~48% y/y |

| Q3 revenue | $120M |

| Backlog | $462M |

| Cumulative GAAP loss | $112M |

| Non-GAAP gross margin (Q3) | 6.2% |

| H2 gross margin | ~18% |

| Financing facility | $75M |

| Steel HRC price | $600–$900/ton |

Same Document Delivered

FTC Solar PESTLE Analysis

The preview shown here is the exact FTC Solar PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in this preview are identical to the file you’ll download immediately after payment; no placeholders, no teasers, just the final product.