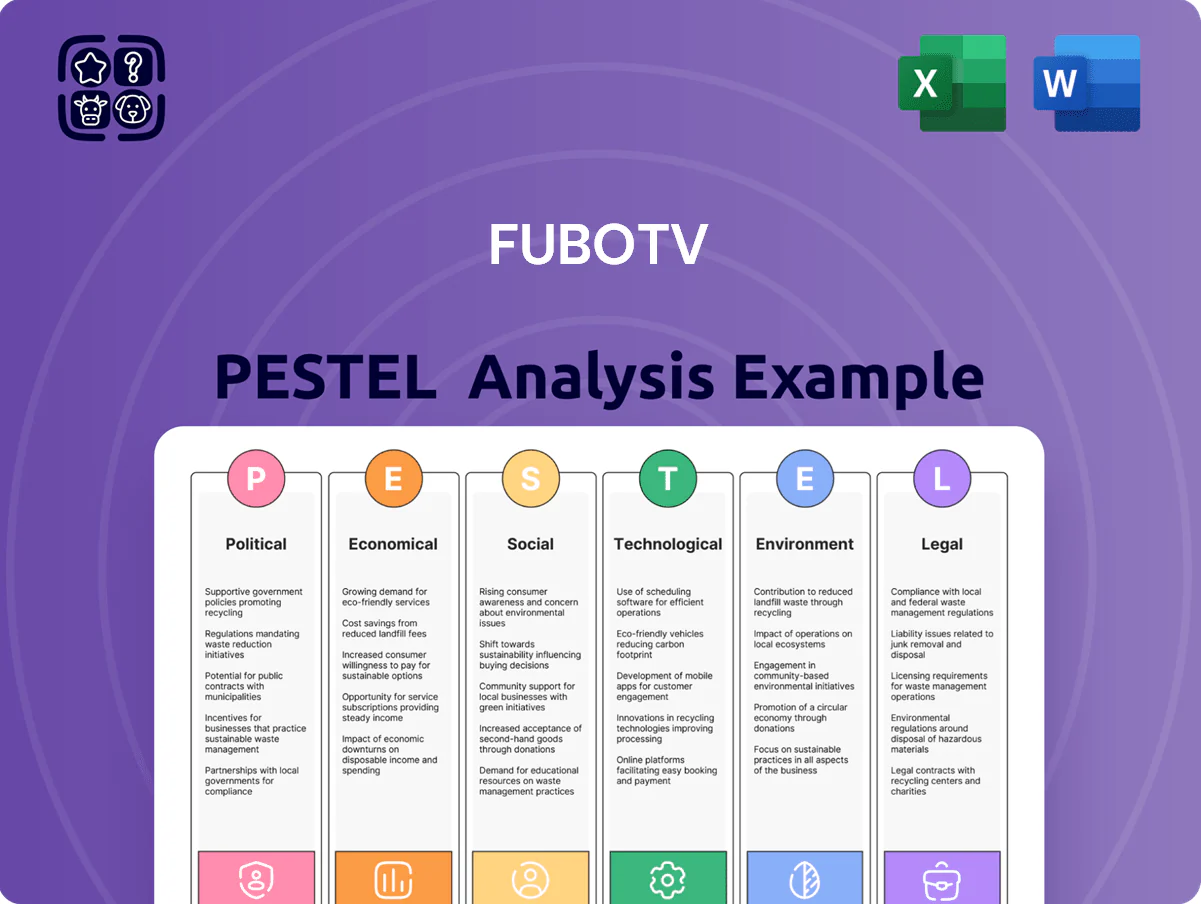

fuboTV PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Navigate the forces shaping fuboTV with our concise PESTLE snapshot—spot regulatory risks, tech disruptors, and shifting consumer trends that will affect growth and valuation; purchase the full analysis to access detailed, actionable intelligence and ready-to-use charts for investors and strategists.

Political factors

Antitrust regulatory environment

Federal scrutiny of large media mergers has risen, with DOJ and FTC actions increasing 35% from 2020–2024, targeting deals that could concentrate sports-broadcasting rights; this reduces the risk of exclusive packages that squeeze smaller platforms. For fuboTV, regulatory pressure on dominant incumbents helps level negotiations for live-sports rights amid a market where MLB/NBA rights fees topped $10B+ annually by 2024. Such interventions support competition and deter exclusionary tying or bundling by major network conglomerates, preserving fuboTV’s access to essential content.

Net neutrality protections

The political stance on net neutrality directly affects fuboTVs ability to deliver HD/4K sports streams without ISP throttling; FCC rollback in 2017 raised concerns after U.S. broadband providers served 298 million fixed broadband lines in 2024, increasing leverage for prioritization. Strong open-internet rules prevent ISPs from charging premiums for high-bandwidth streaming, protecting margins—any policy shift under new leadership could raise CDN costs or reduce average throughput, impacting ARPU and churn.

Digital services taxation

As fuboTV expands, it faces state and international digital services taxes—over 45 US jurisdictions considered DSTs or similar levies—pressuring 2025 gross margins (fubo reported -19.8% adj. gross margin in FY2024) and potentially forcing consumer price hikes or margin compression; monitoring pending US state bills and OECD/G20 digital tax talks is crucial for pricing strategy and long-term financial planning.

Government broadband initiatives

Federal and state broadband programs, including $65 billion from the BEAD program (2023-2026) and $42.5 billion from the IIJA, expand high-speed access in rural/underserved U.S. areas, enlarging fuboTVs addressable market as previously unreachable households gain streaming capability.

As digital-divide funding raises household broadband availability—BEAD aims for 100% coverage—fuboTV can penetrate new geographies, supporting long-term subscriber growth amid continued cord-cutting trends (U.S. pay-TV subscriptions fell ~22% 2019–2023).

- BEAD $65B and IIJA $42.5B boost rural broadband

- Enables access to previously unserved households

- Supports sustained cord-cutting and subscriber growth

Sports betting legislation

The political climate around state-level sports wagering shapes fuboTVs integrated gaming strategy; as of 2025, 38 US states plus DC have legalized sports betting, expanding addressable market but creating regulatory fragmentation.

Shifts in regulation can impose stricter advertising limits or increase licensing costs—average commercial sportsbook state fees range from $100k to $10m+ upfront and recurring taxes of 8–20% of GGR, impacting fuboTV monetization.

fuboTV must tailor offerings per jurisdiction to optimize interactive fan features and revenue while managing compliance and licensing expense volatility.

- 38 states + DC legalized sports betting (2025)

- Licensing fees typically $100k–$10m+; taxes 8–20% of GGR

- Regulatory variation drives localized product and ad strategies

Regulation, taxes and broadband funding reshape sports-rights and streaming margins

Rising federal antitrust enforcement (DOJ/FTC merger actions +35% 2020–2024) levels sports-rights negotiations as MLB/NBA rights surpassed $10B+ annually by 2024; net neutrality rollback risks higher CDN/ISP costs given 298M fixed broadband lines (2024); DST/state levies across 45+ jurisdictions and OECD talks threaten margins (fubo adj. gross margin -19.8% FY2024); BEAD $65B + IIJA $42.5B expand rural broadband, aiding subscriber growth; 38 states + DC legalized sports betting (2025) raising licensing/tax costs (fees $100k–$10M+, taxes 8–20% GGR).

| Factor | 2024/2025 Data |

|---|---|

| Antitrust actions | DOJ/FTC +35% (2020–2024) |

| Sports rights | MLB/NBA $10B+ annual (2024) |

| Broadband lines | 298M fixed lines (2024) |

| fubo margin | Adj. gross margin -19.8% (FY2024) |

| Digital tax scope | 45+ US jurisdictions under consideration |

| Broadband funding | BEAD $65B; IIJA $42.5B |

| Sports betting | 38 states + DC legalized (2025); fees $100k–$10M+, taxes 8–20% GGR |

What is included in the product

Explores how external macro-environmental factors uniquely affect fuboTV across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking scenarios to identify threats and opportunities for executives, investors, and strategists.

Provides a concise, visually segmented PESTLE snapshot of fuboTV that can be dropped into presentations or shared across teams to quickly align on external risks, market drivers, and strategic positioning.

Economic factors

Consumer discretionary spending trends

As of late 2025 fuboTV remains highly sensitive to household disposable income and consumer confidence; US real disposable personal income fell 1.2% YoY in Q3 2025, pressuring premium subscriptions. During economic uncertainty churn rises—streaming industry average monthly churn hit 3.1% in 2025, with price-sensitive tiers showing 20% higher cancellations. fuboTV must continually prove value to retain customers managing tighter budgets, where ARPU growth slowed to 2% YoY in 2025.

Rising costs of sports broadcasting rights

Intense competition for exclusive sports rights has pushed fees higher, with U.S. sports rights spending reaching an estimated $20–25 billion in 2024 and double-digit annual increases for major leagues; this drives up costs for fuboTV to carry national and regional sports networks.

Rising rights expenses compress fuboTVs operating margins—net loss widened to $384 million in 2024—and force frequent subscription price adjustments to protect unit economics.

Balancing bids for high-demand content against subscriber churn and cash burn is a core economic challenge as rights costs outpace revenue per user growth.

Advertising market volatility

A significant share of fuboTVs revenue comes from ad-supported tiers and live digital inventory; in 2024 advertising revenue represented about 22% of total revenue, making ad market swings material to cash flow.

During downturns brands cut marketing spend—US digital ad growth slowed to 3% in 2023 and ad CPMs fell mid-single digits—pressuring fuboTVs ad rates and revenue.

To mitigate cycles fuboTV needs broader advertiser diversification and better targeting; management reported investments in addressable TV and first-party data aiming to lift ad yield and reduce sensitivity to macro cuts.

Interest rates and capital access

The higher interest-rate environment at end-2025 (US Fed funds target 5.25–5.50%) raises fuboTVs cost of capital, making debt-financing for growth and tech investments more expensive and potentially constraining cash burn for subscriber acquisition.

Elevated borrowing costs can limit funding for aggressive marketing and infrastructure upgrades; as of FY2024 fuboTV reported $1.1B net revenue and negative free cash flow, so preserving liquidity is critical.

- Fed funds 5.25–5.50% (end-2025)

- FY2024 revenue $1.1B; negative FCF

- Strong balance sheet and clear path to profitability needed to attract capital

Currency exchange rate fluctuations

As fuboTV operates in France and Canada, currency volatility affects reported revenue and content acquisition costs; a 10% USD appreciation vs EUR or CAD could reduce translated revenue materially given 2024 international revenue of roughly $120m.

Management uses strategic hedging and local-currency pricing to mitigate FX risk; disclosed hedges covered a portion of 2024 exposures per company filings, helping stabilize margins.

- Exposure: France, Canada operations; ~15% of revenue in 2024

- Risk: USD appreciation can lower translated revenue (example: 10% move)

- Mitigation: hedging programs and local currency pricing

fuboTV pressured by weak consumer income, slowing ARPU and rising rates

Economic headwinds hurt fuboTV: Q3 2025 US real disposable income -1.2% YoY, ARPU growth slowed to 2% in 2025, FY2024 revenue $1.1B with negative FCF, net loss $384M (2024), ad revenue ~22% (2024), international revenue ~$120M (2024); Fed funds 5.25–5.50% (end-2025) raises cost of capital and increases pressure on rights bidding and subscriber acquisition.

| Metric | Value |

|---|---|

| FY2024 Revenue | $1.1B |

| Net loss 2024 | $384M |

| Ad rev 2024 | 22% |

| Intl rev 2024 | $120M |

| Fed funds | 5.25–5.50% |

Same Document Delivered

fuboTV PESTLE Analysis

The preview shown here is the exact fuboTV PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in this preview are the same file you’ll download immediately after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Navigate the forces shaping fuboTV with our concise PESTLE snapshot—spot regulatory risks, tech disruptors, and shifting consumer trends that will affect growth and valuation; purchase the full analysis to access detailed, actionable intelligence and ready-to-use charts for investors and strategists.

Political factors

Antitrust regulatory environment

Federal scrutiny of large media mergers has risen, with DOJ and FTC actions increasing 35% from 2020–2024, targeting deals that could concentrate sports-broadcasting rights; this reduces the risk of exclusive packages that squeeze smaller platforms. For fuboTV, regulatory pressure on dominant incumbents helps level negotiations for live-sports rights amid a market where MLB/NBA rights fees topped $10B+ annually by 2024. Such interventions support competition and deter exclusionary tying or bundling by major network conglomerates, preserving fuboTV’s access to essential content.

Net neutrality protections

The political stance on net neutrality directly affects fuboTVs ability to deliver HD/4K sports streams without ISP throttling; FCC rollback in 2017 raised concerns after U.S. broadband providers served 298 million fixed broadband lines in 2024, increasing leverage for prioritization. Strong open-internet rules prevent ISPs from charging premiums for high-bandwidth streaming, protecting margins—any policy shift under new leadership could raise CDN costs or reduce average throughput, impacting ARPU and churn.

Digital services taxation

As fuboTV expands, it faces state and international digital services taxes—over 45 US jurisdictions considered DSTs or similar levies—pressuring 2025 gross margins (fubo reported -19.8% adj. gross margin in FY2024) and potentially forcing consumer price hikes or margin compression; monitoring pending US state bills and OECD/G20 digital tax talks is crucial for pricing strategy and long-term financial planning.

Government broadband initiatives

Federal and state broadband programs, including $65 billion from the BEAD program (2023-2026) and $42.5 billion from the IIJA, expand high-speed access in rural/underserved U.S. areas, enlarging fuboTVs addressable market as previously unreachable households gain streaming capability.

As digital-divide funding raises household broadband availability—BEAD aims for 100% coverage—fuboTV can penetrate new geographies, supporting long-term subscriber growth amid continued cord-cutting trends (U.S. pay-TV subscriptions fell ~22% 2019–2023).

- BEAD $65B and IIJA $42.5B boost rural broadband

- Enables access to previously unserved households

- Supports sustained cord-cutting and subscriber growth

Sports betting legislation

The political climate around state-level sports wagering shapes fuboTVs integrated gaming strategy; as of 2025, 38 US states plus DC have legalized sports betting, expanding addressable market but creating regulatory fragmentation.

Shifts in regulation can impose stricter advertising limits or increase licensing costs—average commercial sportsbook state fees range from $100k to $10m+ upfront and recurring taxes of 8–20% of GGR, impacting fuboTV monetization.

fuboTV must tailor offerings per jurisdiction to optimize interactive fan features and revenue while managing compliance and licensing expense volatility.

- 38 states + DC legalized sports betting (2025)

- Licensing fees typically $100k–$10m+; taxes 8–20% of GGR

- Regulatory variation drives localized product and ad strategies

Regulation, taxes and broadband funding reshape sports-rights and streaming margins

Rising federal antitrust enforcement (DOJ/FTC merger actions +35% 2020–2024) levels sports-rights negotiations as MLB/NBA rights surpassed $10B+ annually by 2024; net neutrality rollback risks higher CDN/ISP costs given 298M fixed broadband lines (2024); DST/state levies across 45+ jurisdictions and OECD talks threaten margins (fubo adj. gross margin -19.8% FY2024); BEAD $65B + IIJA $42.5B expand rural broadband, aiding subscriber growth; 38 states + DC legalized sports betting (2025) raising licensing/tax costs (fees $100k–$10M+, taxes 8–20% GGR).

| Factor | 2024/2025 Data |

|---|---|

| Antitrust actions | DOJ/FTC +35% (2020–2024) |

| Sports rights | MLB/NBA $10B+ annual (2024) |

| Broadband lines | 298M fixed lines (2024) |

| fubo margin | Adj. gross margin -19.8% (FY2024) |

| Digital tax scope | 45+ US jurisdictions under consideration |

| Broadband funding | BEAD $65B; IIJA $42.5B |

| Sports betting | 38 states + DC legalized (2025); fees $100k–$10M+, taxes 8–20% GGR |

What is included in the product

Explores how external macro-environmental factors uniquely affect fuboTV across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking scenarios to identify threats and opportunities for executives, investors, and strategists.

Provides a concise, visually segmented PESTLE snapshot of fuboTV that can be dropped into presentations or shared across teams to quickly align on external risks, market drivers, and strategic positioning.

Economic factors

Consumer discretionary spending trends

As of late 2025 fuboTV remains highly sensitive to household disposable income and consumer confidence; US real disposable personal income fell 1.2% YoY in Q3 2025, pressuring premium subscriptions. During economic uncertainty churn rises—streaming industry average monthly churn hit 3.1% in 2025, with price-sensitive tiers showing 20% higher cancellations. fuboTV must continually prove value to retain customers managing tighter budgets, where ARPU growth slowed to 2% YoY in 2025.

Rising costs of sports broadcasting rights

Intense competition for exclusive sports rights has pushed fees higher, with U.S. sports rights spending reaching an estimated $20–25 billion in 2024 and double-digit annual increases for major leagues; this drives up costs for fuboTV to carry national and regional sports networks.

Rising rights expenses compress fuboTVs operating margins—net loss widened to $384 million in 2024—and force frequent subscription price adjustments to protect unit economics.

Balancing bids for high-demand content against subscriber churn and cash burn is a core economic challenge as rights costs outpace revenue per user growth.

Advertising market volatility

A significant share of fuboTVs revenue comes from ad-supported tiers and live digital inventory; in 2024 advertising revenue represented about 22% of total revenue, making ad market swings material to cash flow.

During downturns brands cut marketing spend—US digital ad growth slowed to 3% in 2023 and ad CPMs fell mid-single digits—pressuring fuboTVs ad rates and revenue.

To mitigate cycles fuboTV needs broader advertiser diversification and better targeting; management reported investments in addressable TV and first-party data aiming to lift ad yield and reduce sensitivity to macro cuts.

Interest rates and capital access

The higher interest-rate environment at end-2025 (US Fed funds target 5.25–5.50%) raises fuboTVs cost of capital, making debt-financing for growth and tech investments more expensive and potentially constraining cash burn for subscriber acquisition.

Elevated borrowing costs can limit funding for aggressive marketing and infrastructure upgrades; as of FY2024 fuboTV reported $1.1B net revenue and negative free cash flow, so preserving liquidity is critical.

- Fed funds 5.25–5.50% (end-2025)

- FY2024 revenue $1.1B; negative FCF

- Strong balance sheet and clear path to profitability needed to attract capital

Currency exchange rate fluctuations

As fuboTV operates in France and Canada, currency volatility affects reported revenue and content acquisition costs; a 10% USD appreciation vs EUR or CAD could reduce translated revenue materially given 2024 international revenue of roughly $120m.

Management uses strategic hedging and local-currency pricing to mitigate FX risk; disclosed hedges covered a portion of 2024 exposures per company filings, helping stabilize margins.

- Exposure: France, Canada operations; ~15% of revenue in 2024

- Risk: USD appreciation can lower translated revenue (example: 10% move)

- Mitigation: hedging programs and local currency pricing

fuboTV pressured by weak consumer income, slowing ARPU and rising rates

Economic headwinds hurt fuboTV: Q3 2025 US real disposable income -1.2% YoY, ARPU growth slowed to 2% in 2025, FY2024 revenue $1.1B with negative FCF, net loss $384M (2024), ad revenue ~22% (2024), international revenue ~$120M (2024); Fed funds 5.25–5.50% (end-2025) raises cost of capital and increases pressure on rights bidding and subscriber acquisition.

| Metric | Value |

|---|---|

| FY2024 Revenue | $1.1B |

| Net loss 2024 | $384M |

| Ad rev 2024 | 22% |

| Intl rev 2024 | $120M |

| Fed funds | 5.25–5.50% |

Same Document Delivered

fuboTV PESTLE Analysis

The preview shown here is the exact fuboTV PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in this preview are the same file you’ll download immediately after checkout.