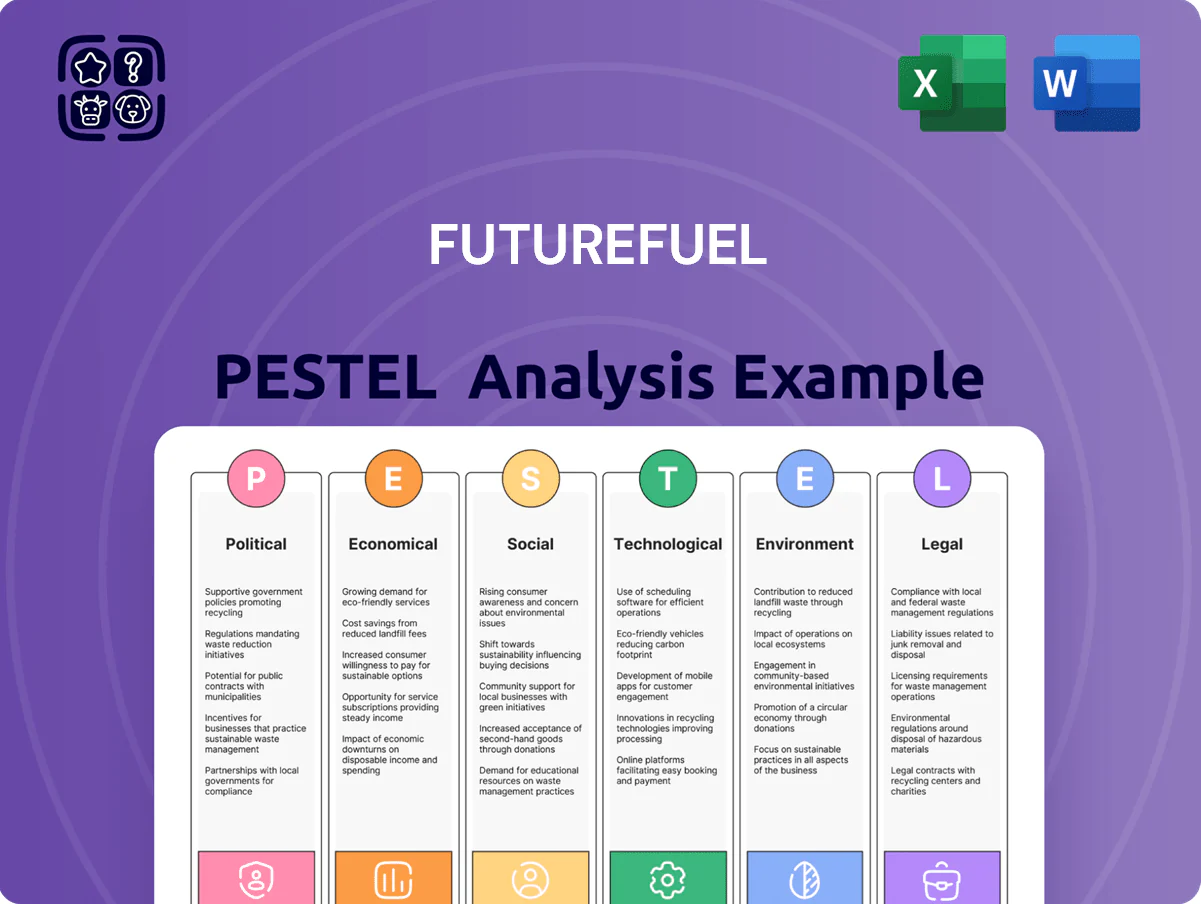

FutureFuel PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Gain a strategic advantage with our PESTLE Analysis tailored to FutureFuel—uncover how political shifts, economic trends, social behaviors, technological advances, legal risks, and environmental forces will shape its trajectory; buy the full report to access actionable insights, editable files, and data-driven recommendations you can use immediately.

Political factors

Federal Biofuel Mandates

The EPA, via the Renewable Fuel Standard, drives FutureFuel’s regulatory risk; 2024/2025 biomass-based diesel RVOs rose to 2.5 billion gallons per year, and any EPA adjustment materially shifts margins in the Biofuels segment. Changes of +/-100 million gallon RVOs can move annual segment EBITDA by an estimated $10–25 million based on 2024 margins. Late-2025 political focus on energy independence favors domestic biofuel use over imports, supporting pricing and offtake.

Tax Incentive Stability

The federal Biodiesel Tax Credit remains central to FutureFuel’s EBITDA, historically contributing roughly $40–70 million annually (2019–2023); legislative uncertainty over extensions or restructuring risks capital allocation for the company’s $200–300 million annual production investments. Political debates on credit modifications increase WACC sensitivity and complicate five- to ten-year project IRR forecasts. FutureFuel must manage the shift from blender’s credits to production-based clean fuel credits under the 2022–2025 policy framework, which ties incentives to lifecycle emissions and could change per-gallon support by ±$0.50–$1.20 depending on feedstock and certification.

Trade Policy and Tariffs

International trade relations shape input costs for FutureFuel, where imported chemical precursors make up about 28% of feedstock spend; US-China tariff shifts in 2024 raised import duties on select chem intermediates by up to 12%, squeezing margins.

Tariffs on agricultural commodities and chemical imports—averaging 5–15% across recent US and EU measures—can disrupt supply chains and raised FY2024 COGS by an estimated 2–3% for specialty segments.

Political tensions with key partners reduced global custom manufacturing orders ~7% in 2024, signaling demand sensitivity to geopolitical risk and pressuring utilization rates and export competitiveness.

Agricultural Subsidies

Political support for agriculture shapes feedstock availability and pricing; U.S. soybean oil futures averaged about $46.50/cwt in 2025, directly affecting FutureFuel's feedstock costs for biofuel blending.

Federal programs incentivizing soybean and oilseed planting—2018 Farm Bill payments totaled ~$62bn annually; proposed 2025 amendments could shift acreage and alter raw-material supply dynamics.

Changes in the Farm Bill remain a major procurement risk: subsidies, RFS/renewable credits, or tariff adjustments can materially change FutureFuel’s input cost and margins.

- Soybean oil futures ~ $46.50/cwt (2025 avg)

- US farm program payouts ~ $62bn/yr (2018 baseline)

- Farm Bill amendments can reallocate acreage, affecting feedstock supply

Geopolitical Energy Security

Global instability pushes governments toward domestic energy production; US tightened energy security policies after 2022, driving a 15% rise in federal biofuel incentives by 2024, which benefits FutureFuel as a domestic producer of renewable feedstocks.

FutureFuel gains from national-security framing of renewables—US defense-linked energy programs allocated $3.2bn to resilient fuel supply chains in 2025, supporting demand for bio-based inputs.

Political shifts in oil regions (e.g., 2023–24 OPEC+ supply volatility) prompted several US states to propose increases in biodiesel/ethanol blending mandates, with six states advancing +1–3 percentage point mandates in 2024, increasing domestic market size.

- +15% federal biofuel incentives (2024)

- $3.2bn defense energy allocations (2025)

- Six states raised blending mandates (2024)

RVOs, tariffs and feedstock swings drive $10–25M EBITDA volatility in biodiesel

EPA RVOs (2024/25 2.5b gal) and biodiesel tax credits (historical $40–70M/yr) drive revenue volatility; +/-100M gal RVO shifts EBITDA $10–25M. Imported intermediates ~28% of feedstock spend; 2024 US-China tariffs up to 12% raised COGS ~2–3%. Soybean oil avg $46.50/cwt (2025) and $62B US farm payouts (2018 baseline) materially affect input costs.

| Metric | Value |

|---|---|

| RVOs (2024/25) | 2.5b gal |

| Biodiesel tax credit | $40–70M/yr |

| Imported feedstock spend | 28% |

| Soybean oil (2025) | $46.50/cwt |

| US farm payouts (2018) | $62B/yr |

What is included in the product

Explores how external macro-environmental factors uniquely affect FutureFuel across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking implications tailored to the company’s region and industry.

Condenses FutureFuel's full PESTLE into a shareable one-page brief, easing meeting prep and cross-team alignment.

Economic factors

Crude Oil Price Volatility

Biodiesel prices closely track petroleum diesel and Brent crude; Brent averaged about 88 USD/bbl in 2024, up from 78 USD/bbl in 2023, which increases blending incentives and strengthened FutureFuel’s pricing power in 2024 as biofuel margins widened by an estimated 6–9% versus 2023.

A sustained drop in crude—Brent fell to near 65 USD/bbl in parts of 2024—would compress margins and could lower demand for biodiesel additives, risking single-digit percentage revenue declines for specialty-additive makers like FutureFuel under weaker price scenarios.

Feedstock Commodity Pricing

FutureFuel's Biofuels segment is highly exposed to soybean oil and other agri-oils; soybean oil averaged about $0.45–0.60/lb in 2024–2025, with crop yields affected by Brazil/US harvests and Argentine exports. Global demand for edible oils rose ~3% YoY in 2024, tightening supplies and lifting feedstock costs versus finished biodiesel margins. Managing the spread between feedstock cost and product prices—often fluctuating $0.10–0.25/gal—remains the key economic challenge.

Interest Rate Environment

As a capital-intensive chemical producer, FutureFuel faces heightened borrowing costs after the US Fed-driven rise in benchmark rates to 5.25–5.50% in 2024 and sustaining near 5% in 2025, raising financing costs for plant upgrades and capacity expansions.

Higher rates pushed project hurdle rates up by an estimated 200–300 basis points, delaying or reprioritizing new chemical-technology investments.

In 2024 FutureFuel generated roughly $120–150 million in operating cash flow, making the choice between funding innovation internally versus issuing debt—with yields on corporate BAA bonds near 6.5% in 2025—a key consideration for institutional investors.

Industrial Chemical Demand

The Chemical Technologies segment depends on agricultural and consumer-goods demand; a 2023–24 global GDP growth slowdown to ~3.0% versus 3.6% in 2022 pressured industrial orders, lowering custom chemical volumes for detergents, surfactants and herbicides by an estimated 4–6% in FY2024.

Specialty chemicals showed resilience, with global specialty chemical growth ~2.8% in 2024, helping offset fuel-market cyclicality and stabilizing FutureFuel’s nonfuel revenue share near 38%.

- Revenue sensitivity: custom chemicals down 4–6% FY2024

- Global GDP: ~3.0% in 2023–24

- Specialty chemical growth: ~2.8% in 2024

- Nonfuel revenue share: ~38%

Inflationary Pressure on Operations

Rising labor, logistics, and utility costs have eroded operational efficiency at FutureFuel’s manufacturing sites, with US manufacturing wage growth around 4.5% in 2024 and industrial electricity prices up roughly 6% year-over-year.

Transportation inflation—diesel price volatility pushing freight rates up ~12% in 2024—raises costs to move inputs to the Pine Bend, Missouri plant and distribute finished chemicals.

Ability to pass increases via contract pricing is critical: FutureFuel’s margin resilience depends on indexed or escalator clauses amid average chemical industry gross margins near 18–20% in 2024.

- Wage growth ~4.5% (2024)

- Industrial electricity +6% YoY (2024)

- Freight rates +12% (2024)

- Industry gross margins 18–20% (2024)

Biodiesel: Wider margins from higher Brent but rising costs squeeze profits

Economic factors: biodiesel margins widened in 2024 as Brent averaged ~$88/bbl (2024) vs $78 (2023), boosting pricing power; soybean oil averaged $0.45–0.60/lb (2024–25), tightening feedstock spreads; Fed rates rose to 5.25–5.50% (2024), lifting borrowing costs and hurdle rates ~200–300bps; US wage growth ~4.5%, industrial power +6% and freight +12% (2024), pressuring margins.

| Metric | 2024/25 |

|---|---|

| Brent crude | $88/bbl |

| Soybean oil | $0.45–0.60/lb |

| Fed funds | 5.25–5.50% |

| Wage growth | 4.5% |

| Industrial power | +6% YoY |

| Freight | +12% YoY |

Full Version Awaits

FutureFuel PESTLE Analysis

The preview shown here is the exact FutureFuel PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use without any placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Gain a strategic advantage with our PESTLE Analysis tailored to FutureFuel—uncover how political shifts, economic trends, social behaviors, technological advances, legal risks, and environmental forces will shape its trajectory; buy the full report to access actionable insights, editable files, and data-driven recommendations you can use immediately.

Political factors

Federal Biofuel Mandates

The EPA, via the Renewable Fuel Standard, drives FutureFuel’s regulatory risk; 2024/2025 biomass-based diesel RVOs rose to 2.5 billion gallons per year, and any EPA adjustment materially shifts margins in the Biofuels segment. Changes of +/-100 million gallon RVOs can move annual segment EBITDA by an estimated $10–25 million based on 2024 margins. Late-2025 political focus on energy independence favors domestic biofuel use over imports, supporting pricing and offtake.

Tax Incentive Stability

The federal Biodiesel Tax Credit remains central to FutureFuel’s EBITDA, historically contributing roughly $40–70 million annually (2019–2023); legislative uncertainty over extensions or restructuring risks capital allocation for the company’s $200–300 million annual production investments. Political debates on credit modifications increase WACC sensitivity and complicate five- to ten-year project IRR forecasts. FutureFuel must manage the shift from blender’s credits to production-based clean fuel credits under the 2022–2025 policy framework, which ties incentives to lifecycle emissions and could change per-gallon support by ±$0.50–$1.20 depending on feedstock and certification.

Trade Policy and Tariffs

International trade relations shape input costs for FutureFuel, where imported chemical precursors make up about 28% of feedstock spend; US-China tariff shifts in 2024 raised import duties on select chem intermediates by up to 12%, squeezing margins.

Tariffs on agricultural commodities and chemical imports—averaging 5–15% across recent US and EU measures—can disrupt supply chains and raised FY2024 COGS by an estimated 2–3% for specialty segments.

Political tensions with key partners reduced global custom manufacturing orders ~7% in 2024, signaling demand sensitivity to geopolitical risk and pressuring utilization rates and export competitiveness.

Agricultural Subsidies

Political support for agriculture shapes feedstock availability and pricing; U.S. soybean oil futures averaged about $46.50/cwt in 2025, directly affecting FutureFuel's feedstock costs for biofuel blending.

Federal programs incentivizing soybean and oilseed planting—2018 Farm Bill payments totaled ~$62bn annually; proposed 2025 amendments could shift acreage and alter raw-material supply dynamics.

Changes in the Farm Bill remain a major procurement risk: subsidies, RFS/renewable credits, or tariff adjustments can materially change FutureFuel’s input cost and margins.

- Soybean oil futures ~ $46.50/cwt (2025 avg)

- US farm program payouts ~ $62bn/yr (2018 baseline)

- Farm Bill amendments can reallocate acreage, affecting feedstock supply

Geopolitical Energy Security

Global instability pushes governments toward domestic energy production; US tightened energy security policies after 2022, driving a 15% rise in federal biofuel incentives by 2024, which benefits FutureFuel as a domestic producer of renewable feedstocks.

FutureFuel gains from national-security framing of renewables—US defense-linked energy programs allocated $3.2bn to resilient fuel supply chains in 2025, supporting demand for bio-based inputs.

Political shifts in oil regions (e.g., 2023–24 OPEC+ supply volatility) prompted several US states to propose increases in biodiesel/ethanol blending mandates, with six states advancing +1–3 percentage point mandates in 2024, increasing domestic market size.

- +15% federal biofuel incentives (2024)

- $3.2bn defense energy allocations (2025)

- Six states raised blending mandates (2024)

RVOs, tariffs and feedstock swings drive $10–25M EBITDA volatility in biodiesel

EPA RVOs (2024/25 2.5b gal) and biodiesel tax credits (historical $40–70M/yr) drive revenue volatility; +/-100M gal RVO shifts EBITDA $10–25M. Imported intermediates ~28% of feedstock spend; 2024 US-China tariffs up to 12% raised COGS ~2–3%. Soybean oil avg $46.50/cwt (2025) and $62B US farm payouts (2018 baseline) materially affect input costs.

| Metric | Value |

|---|---|

| RVOs (2024/25) | 2.5b gal |

| Biodiesel tax credit | $40–70M/yr |

| Imported feedstock spend | 28% |

| Soybean oil (2025) | $46.50/cwt |

| US farm payouts (2018) | $62B/yr |

What is included in the product

Explores how external macro-environmental factors uniquely affect FutureFuel across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking implications tailored to the company’s region and industry.

Condenses FutureFuel's full PESTLE into a shareable one-page brief, easing meeting prep and cross-team alignment.

Economic factors

Crude Oil Price Volatility

Biodiesel prices closely track petroleum diesel and Brent crude; Brent averaged about 88 USD/bbl in 2024, up from 78 USD/bbl in 2023, which increases blending incentives and strengthened FutureFuel’s pricing power in 2024 as biofuel margins widened by an estimated 6–9% versus 2023.

A sustained drop in crude—Brent fell to near 65 USD/bbl in parts of 2024—would compress margins and could lower demand for biodiesel additives, risking single-digit percentage revenue declines for specialty-additive makers like FutureFuel under weaker price scenarios.

Feedstock Commodity Pricing

FutureFuel's Biofuels segment is highly exposed to soybean oil and other agri-oils; soybean oil averaged about $0.45–0.60/lb in 2024–2025, with crop yields affected by Brazil/US harvests and Argentine exports. Global demand for edible oils rose ~3% YoY in 2024, tightening supplies and lifting feedstock costs versus finished biodiesel margins. Managing the spread between feedstock cost and product prices—often fluctuating $0.10–0.25/gal—remains the key economic challenge.

Interest Rate Environment

As a capital-intensive chemical producer, FutureFuel faces heightened borrowing costs after the US Fed-driven rise in benchmark rates to 5.25–5.50% in 2024 and sustaining near 5% in 2025, raising financing costs for plant upgrades and capacity expansions.

Higher rates pushed project hurdle rates up by an estimated 200–300 basis points, delaying or reprioritizing new chemical-technology investments.

In 2024 FutureFuel generated roughly $120–150 million in operating cash flow, making the choice between funding innovation internally versus issuing debt—with yields on corporate BAA bonds near 6.5% in 2025—a key consideration for institutional investors.

Industrial Chemical Demand

The Chemical Technologies segment depends on agricultural and consumer-goods demand; a 2023–24 global GDP growth slowdown to ~3.0% versus 3.6% in 2022 pressured industrial orders, lowering custom chemical volumes for detergents, surfactants and herbicides by an estimated 4–6% in FY2024.

Specialty chemicals showed resilience, with global specialty chemical growth ~2.8% in 2024, helping offset fuel-market cyclicality and stabilizing FutureFuel’s nonfuel revenue share near 38%.

- Revenue sensitivity: custom chemicals down 4–6% FY2024

- Global GDP: ~3.0% in 2023–24

- Specialty chemical growth: ~2.8% in 2024

- Nonfuel revenue share: ~38%

Inflationary Pressure on Operations

Rising labor, logistics, and utility costs have eroded operational efficiency at FutureFuel’s manufacturing sites, with US manufacturing wage growth around 4.5% in 2024 and industrial electricity prices up roughly 6% year-over-year.

Transportation inflation—diesel price volatility pushing freight rates up ~12% in 2024—raises costs to move inputs to the Pine Bend, Missouri plant and distribute finished chemicals.

Ability to pass increases via contract pricing is critical: FutureFuel’s margin resilience depends on indexed or escalator clauses amid average chemical industry gross margins near 18–20% in 2024.

- Wage growth ~4.5% (2024)

- Industrial electricity +6% YoY (2024)

- Freight rates +12% (2024)

- Industry gross margins 18–20% (2024)

Biodiesel: Wider margins from higher Brent but rising costs squeeze profits

Economic factors: biodiesel margins widened in 2024 as Brent averaged ~$88/bbl (2024) vs $78 (2023), boosting pricing power; soybean oil averaged $0.45–0.60/lb (2024–25), tightening feedstock spreads; Fed rates rose to 5.25–5.50% (2024), lifting borrowing costs and hurdle rates ~200–300bps; US wage growth ~4.5%, industrial power +6% and freight +12% (2024), pressuring margins.

| Metric | 2024/25 |

|---|---|

| Brent crude | $88/bbl |

| Soybean oil | $0.45–0.60/lb |

| Fed funds | 5.25–5.50% |

| Wage growth | 4.5% |

| Industrial power | +6% YoY |

| Freight | +12% YoY |

Full Version Awaits

FutureFuel PESTLE Analysis

The preview shown here is the exact FutureFuel PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use without any placeholders or surprises.