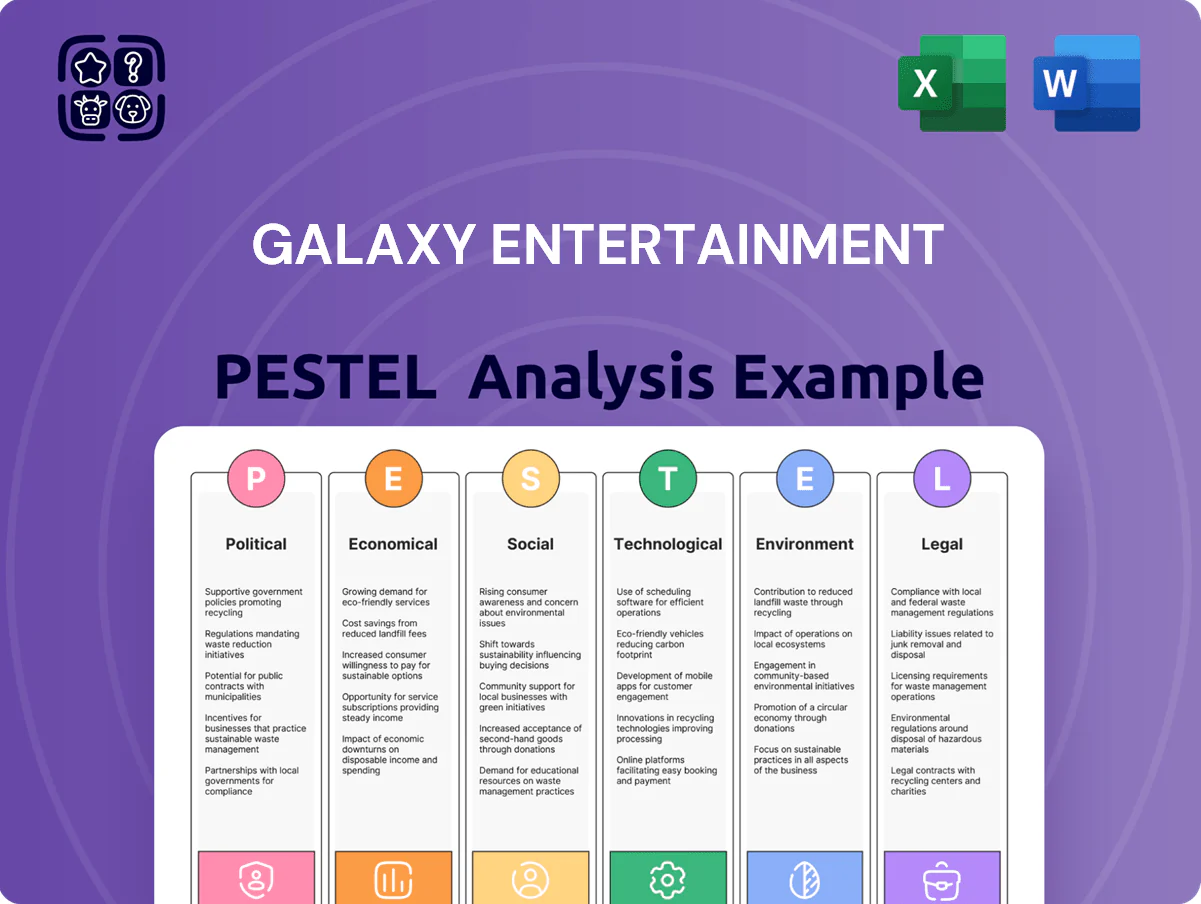

Galaxy Entertainment PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Gain a competitive edge with our PESTLE Analysis tailored for Galaxy Entertainment—uncover how political shifts, economic cycles, social trends, technological advances, legal reforms, and environmental pressures shape its strategy and valuation; ideal for investors and strategists seeking concise, actionable intelligence. Purchase the full report to access the complete, editable deep-dive and use it immediately in your decision-making.

Political factors

Macau Government Concession Compliance

Galaxy Entertainment faces strict Macau government ten-year concession conditions requiring substantial non-gaming investment; the 2024 concession update mandates progressive capital deployment into tourism, MICE, and cultural projects through 2025.

By end-2025 Galaxy is expected to show material progress on multiple committed projects totaling around MOP 20–30 billion in redevelopment and diversification spend disclosed in 2023–24 filings.

Failure to meet milestones risks regulatory friction and potential complications at next licensing review, heightening political scrutiny of Galaxy’s strategic priorities.

Mainland China Regulatory Oversight

China’s tightened cross-border gambling and capital outflow rules, including the 2020 amended criminal law curbing junkets, forced Galaxy to shift to mass-market operations; VIP table drop fell over 60% from 2019 to 2023 while mass-market revenue rose, with 2024 VIP contribution under 10% of total GGR for Macau operators.

Stable Macau–Beijing relations sustain Individual Visit Scheme flows—IVS arrivals recovered to ~70% of 2019 levels in 2023 and continued improving into 2024—supporting occupancy and F&B revenues; any abrupt policy change from Beijing could quickly reduce visitation and materially hit Galaxy’s EBITDA, which depends heavily on mainland tourist volumes.

Greater Bay Area Integration Policy

The Greater Bay Area integration drives infrastructure expansion and enlarges Galaxy Entertainment’s catchment, with the Hong Kong-Zhuhai-Macau Bridge increasing cross-border traffic—visitor arrivals to Macau reached 13.5 million in 2023, up 42% from 2022, boosting regional footfall for integrated resorts.

Government initiatives easing border formalities and funding transport links (over HKD 70 billion invested in GBA connectivity projects by 2024) lower travel friction and expand day-trip and short-stay markets for Galaxy’s properties.

Policy focus on economic synergy targets increased domestic regional tourism; Guangdong’s domestic travel expenditure grew to RMB 2.1 trillion in 2024, presenting Galaxy with higher local demand to capture through targeted marketing and capacity planning.

Galaxy’s strategic plans must align with GBA goals—adjusting room inventory, VIP and mass-market strategies, and capital allocation to leverage projected rises in regional traveler volume and connectivity-driven revenue growth.

Geopolitical Tensions and Tourism

Fluctuations in China-West relations can shift Macau visitor mix; in 2024 mainland tourists accounted for about 78% of Macau arrivals, concentrating Galaxy’s exposure to mainland policy shifts.

Geopolitical stability affects luxury retail and MICE; Macau luxury sales fell 12% YoY in 2023 during regional tensions, and convention bookings are sensitive to travel advisories.

Political friction may trigger visa changes reducing high-spend international guests; non-mainland visitation recovery to pre-COVID levels remains uneven, pressuring non-mainland revenue.

- Monitor China-West relations and visa policies

- Hedge via regional diversification and domestic-focused offers

- Track luxury retail and MICE KPIs (monthly sales, booking lead times)

National Security and Data Governance

Macau has tightened national security and data laws to mirror mainland China, forcing Galaxy to manage cross-jurisdictional guest data storage and sharing under stricter rules.

Political sensitivity over financial data and surveillance peaked in late 2025, increasing compliance costs—estimated sector-wide at 2–3% of revenue—and making adherence to state security priorities essential for Galaxy’s social license to operate.

- Aligns with mainland security/data laws

- Cross-border guest data controls required

- Late-2025 surveillance sensitivity high

- Compliance adds ~2–3% revenue cost

Galaxy shifts MOP20–30bn to non‑gaming as VIPs plunge; Macau tourism rebounds

Macau concession conditions force Galaxy to deploy MOP 20–30bn into non-gaming projects by end‑2025; VIP share fell >60% from 2019 to 2023 with VIP <10% of GGR in 2024; Macau arrivals 13.5m in 2023 (↑42% YoY), mainland 78% of arrivals; GBA connectivity investment >HKD70bn by 2024; compliance costs rose ~2–3% of revenue by late‑2025.

| Metric | Value/Year |

|---|---|

| Non‑gaming capex target | MOP20–30bn (by 2025) |

| Macau arrivals | 13.5m (2023) |

| Mainland share | 78% (2024) |

| VIP drop | >60% vs 2019 (to 2023) |

| GBA investment | HKD70bn+ (by 2024) |

| Compliance cost | ~2–3% rev (late‑2025) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Galaxy Entertainment across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends, region-specific regulatory context, and forward-looking insights to inform executives, investors, and strategists on risks, opportunities, and scenario planning.

A concise, visually segmented PESTLE snapshot of Galaxy Entertainment that can be dropped into presentations or shared across teams to quickly align on external risks, regulatory changes, and market opportunities while allowing note additions for local context.

Economic factors

Shift to Premium Mass Market Dynamics

The economic landscape at Galaxy Entertainment has shifted from VIP junket reliance to a premium mass market model, with VIP revenue falling below 25% of total gaming revenue by 2025 versus over 60% in early 2010s.

Premium mass customers deliver higher margins per segment; average spend per mass patron is ~US$1,200 annually, reducing dependency on few ultra-high rollers.

By end-2025 Galaxy’s revenue mix is weighted ~65% high-value retail and mass gaming, cutting volatility and stabilizing EBITDA margins around 22–24%.

China Disposable Income Trends

Galaxy Entertainment’s revenue is highly sensitive to China’s consumer health; mainland disposable income per capita rose 3.0% in 2024 to about CNY 38,000, but slower than pre-COVID growth, risking weaker spend on luxury travel and entertainment.

Property market strains—China home sales fell ~14% y/y in 2024—can curtail outbound tourism and VIP play, pressuring Galaxy’s mass and premium table volumes.

A rebound in mainland GDP (estimated 5.2% in 2024) supports hotel occupancy and retail spend, directly boosting Galaxy’s non-gaming segments and RevPAR.

Galaxy monitors indicators such as retail sales, urban disposable income and property sales to dynamically adjust marketing and promotional expenditures.

Interest Rate Environment and Debt Management

As Galaxy advances multi-phase Galaxy Macau expansion, global interest rate trends—with key central banks holding policy rates around 2024–25 at 4–5%—raise the cost of capital, increasing servicing expenses on its HKD and USD debt and potentially elevating weighted average cost of capital for non-gaming projects.

Galaxy reported net debt/EBITDA near pre-expansion levels in 2024, but extended high-rate periods could slow project timelines by raising financing costs and tightening investment returns.

Effective treasury actions—use of hedges, staggered maturities and liquidity buffers—remain critical to preserve cash flow for large-scale capex and to manage refinancing risk amid volatile rate cycles.

Labor Market Inflation and Supply

Macau faces rising labor costs with average wages in the hospitality sector up about 7% year-on-year in 2024, while specialized talent remains scarce, pressuring Galaxy Entertainment’s payroll.

Competition among six concessionaires increases poaching of experienced floor managers and service staff, lifting market wages and benefits.

Galaxy must balance service quality against higher payrolls; automation and retention programs (training, bonuses) are needed to protect operating margins—Galaxy reported 2024 operating margin compression of ~1.5 percentage points in VIP/hospitality segments.

- Hospitality wages +7% YoY (2024)

- Talent scarcity raises recruitment costs and turnover

- Concessionaire competition increases poaching

- Automation and retention programs mitigate ~1.5 ppt margin impact

Currency Peg and Exchange Rate Stability

The Macau Pataca is pegged to the Hong Kong Dollar, which is linked to the US Dollar, providing exchange-rate stability that lowered currency risk for investors; Macau recorded tourist receipts of MOP 108.6 billion in 2023 as stability supported cross-border spending.

When the US Dollar strengthens, Macau becomes relatively expensive—visitor daily spend fell 4.7% in 2024 Q3 versus 2023 Q3—pressuring retail and mass-gaming volumes.

US monetary policy shifts indirectly affect mainland Chinese purchasing power via Renminbi movements; RMB volatility in 2024 correlated with a 6% swing in VIP gaming turnover month-to-month.

- Peg chain: MOP-HKD-USD stabilizes exchange risk

- 2023 tourist receipts MOP 108.6B; 2024 Q3 daily spend -4.7% YoY

- RMB moves linked to ~6% VIP turnover swings

- Currency strength of USD raises local cost, hitting retail/gaming

Galaxy pivots to premium mass: 65% revenue, 22–24% EBITDA amid China demand risks

Galaxy shifted to premium mass: VIP <25% of gaming by 2025 vs >60% early 2010s; mass patrons spend ~US$1,200 annually. By end-2025 revenue ~65% high-value retail/mass, EBITDA ~22–24%. Mainland disposable income +3.0% in 2024 (CNY 38,000); GDP ~5.2% in 2024 supports RevPAR, but property sales -14% y/y (2024) and RMB volatility (VIP turnover swings ~6%) pose demand risks.

| Metric | 2024/2025 |

|---|---|

| VIP share | <25% (2025) |

| Mass spend per patron | US$1,200 |

| Revenue mix (high-value/mass) | ~65% |

| EBITDA margin | 22–24% |

| Mainland disposable income | CNY 38,000 (+3.0%) |

| China GDP | ~5.2% (2024) |

| China property sales | -14% y/y (2024) |

| RMB-linked VIP swing | ~6% |

Preview the Actual Deliverable

Galaxy Entertainment PESTLE Analysis

The preview shown here is the exact Galaxy Entertainment PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Gain a competitive edge with our PESTLE Analysis tailored for Galaxy Entertainment—uncover how political shifts, economic cycles, social trends, technological advances, legal reforms, and environmental pressures shape its strategy and valuation; ideal for investors and strategists seeking concise, actionable intelligence. Purchase the full report to access the complete, editable deep-dive and use it immediately in your decision-making.

Political factors

Macau Government Concession Compliance

Galaxy Entertainment faces strict Macau government ten-year concession conditions requiring substantial non-gaming investment; the 2024 concession update mandates progressive capital deployment into tourism, MICE, and cultural projects through 2025.

By end-2025 Galaxy is expected to show material progress on multiple committed projects totaling around MOP 20–30 billion in redevelopment and diversification spend disclosed in 2023–24 filings.

Failure to meet milestones risks regulatory friction and potential complications at next licensing review, heightening political scrutiny of Galaxy’s strategic priorities.

Mainland China Regulatory Oversight

China’s tightened cross-border gambling and capital outflow rules, including the 2020 amended criminal law curbing junkets, forced Galaxy to shift to mass-market operations; VIP table drop fell over 60% from 2019 to 2023 while mass-market revenue rose, with 2024 VIP contribution under 10% of total GGR for Macau operators.

Stable Macau–Beijing relations sustain Individual Visit Scheme flows—IVS arrivals recovered to ~70% of 2019 levels in 2023 and continued improving into 2024—supporting occupancy and F&B revenues; any abrupt policy change from Beijing could quickly reduce visitation and materially hit Galaxy’s EBITDA, which depends heavily on mainland tourist volumes.

Greater Bay Area Integration Policy

The Greater Bay Area integration drives infrastructure expansion and enlarges Galaxy Entertainment’s catchment, with the Hong Kong-Zhuhai-Macau Bridge increasing cross-border traffic—visitor arrivals to Macau reached 13.5 million in 2023, up 42% from 2022, boosting regional footfall for integrated resorts.

Government initiatives easing border formalities and funding transport links (over HKD 70 billion invested in GBA connectivity projects by 2024) lower travel friction and expand day-trip and short-stay markets for Galaxy’s properties.

Policy focus on economic synergy targets increased domestic regional tourism; Guangdong’s domestic travel expenditure grew to RMB 2.1 trillion in 2024, presenting Galaxy with higher local demand to capture through targeted marketing and capacity planning.

Galaxy’s strategic plans must align with GBA goals—adjusting room inventory, VIP and mass-market strategies, and capital allocation to leverage projected rises in regional traveler volume and connectivity-driven revenue growth.

Geopolitical Tensions and Tourism

Fluctuations in China-West relations can shift Macau visitor mix; in 2024 mainland tourists accounted for about 78% of Macau arrivals, concentrating Galaxy’s exposure to mainland policy shifts.

Geopolitical stability affects luxury retail and MICE; Macau luxury sales fell 12% YoY in 2023 during regional tensions, and convention bookings are sensitive to travel advisories.

Political friction may trigger visa changes reducing high-spend international guests; non-mainland visitation recovery to pre-COVID levels remains uneven, pressuring non-mainland revenue.

- Monitor China-West relations and visa policies

- Hedge via regional diversification and domestic-focused offers

- Track luxury retail and MICE KPIs (monthly sales, booking lead times)

National Security and Data Governance

Macau has tightened national security and data laws to mirror mainland China, forcing Galaxy to manage cross-jurisdictional guest data storage and sharing under stricter rules.

Political sensitivity over financial data and surveillance peaked in late 2025, increasing compliance costs—estimated sector-wide at 2–3% of revenue—and making adherence to state security priorities essential for Galaxy’s social license to operate.

- Aligns with mainland security/data laws

- Cross-border guest data controls required

- Late-2025 surveillance sensitivity high

- Compliance adds ~2–3% revenue cost

Galaxy shifts MOP20–30bn to non‑gaming as VIPs plunge; Macau tourism rebounds

Macau concession conditions force Galaxy to deploy MOP 20–30bn into non-gaming projects by end‑2025; VIP share fell >60% from 2019 to 2023 with VIP <10% of GGR in 2024; Macau arrivals 13.5m in 2023 (↑42% YoY), mainland 78% of arrivals; GBA connectivity investment >HKD70bn by 2024; compliance costs rose ~2–3% of revenue by late‑2025.

| Metric | Value/Year |

|---|---|

| Non‑gaming capex target | MOP20–30bn (by 2025) |

| Macau arrivals | 13.5m (2023) |

| Mainland share | 78% (2024) |

| VIP drop | >60% vs 2019 (to 2023) |

| GBA investment | HKD70bn+ (by 2024) |

| Compliance cost | ~2–3% rev (late‑2025) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Galaxy Entertainment across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends, region-specific regulatory context, and forward-looking insights to inform executives, investors, and strategists on risks, opportunities, and scenario planning.

A concise, visually segmented PESTLE snapshot of Galaxy Entertainment that can be dropped into presentations or shared across teams to quickly align on external risks, regulatory changes, and market opportunities while allowing note additions for local context.

Economic factors

Shift to Premium Mass Market Dynamics

The economic landscape at Galaxy Entertainment has shifted from VIP junket reliance to a premium mass market model, with VIP revenue falling below 25% of total gaming revenue by 2025 versus over 60% in early 2010s.

Premium mass customers deliver higher margins per segment; average spend per mass patron is ~US$1,200 annually, reducing dependency on few ultra-high rollers.

By end-2025 Galaxy’s revenue mix is weighted ~65% high-value retail and mass gaming, cutting volatility and stabilizing EBITDA margins around 22–24%.

China Disposable Income Trends

Galaxy Entertainment’s revenue is highly sensitive to China’s consumer health; mainland disposable income per capita rose 3.0% in 2024 to about CNY 38,000, but slower than pre-COVID growth, risking weaker spend on luxury travel and entertainment.

Property market strains—China home sales fell ~14% y/y in 2024—can curtail outbound tourism and VIP play, pressuring Galaxy’s mass and premium table volumes.

A rebound in mainland GDP (estimated 5.2% in 2024) supports hotel occupancy and retail spend, directly boosting Galaxy’s non-gaming segments and RevPAR.

Galaxy monitors indicators such as retail sales, urban disposable income and property sales to dynamically adjust marketing and promotional expenditures.

Interest Rate Environment and Debt Management

As Galaxy advances multi-phase Galaxy Macau expansion, global interest rate trends—with key central banks holding policy rates around 2024–25 at 4–5%—raise the cost of capital, increasing servicing expenses on its HKD and USD debt and potentially elevating weighted average cost of capital for non-gaming projects.

Galaxy reported net debt/EBITDA near pre-expansion levels in 2024, but extended high-rate periods could slow project timelines by raising financing costs and tightening investment returns.

Effective treasury actions—use of hedges, staggered maturities and liquidity buffers—remain critical to preserve cash flow for large-scale capex and to manage refinancing risk amid volatile rate cycles.

Labor Market Inflation and Supply

Macau faces rising labor costs with average wages in the hospitality sector up about 7% year-on-year in 2024, while specialized talent remains scarce, pressuring Galaxy Entertainment’s payroll.

Competition among six concessionaires increases poaching of experienced floor managers and service staff, lifting market wages and benefits.

Galaxy must balance service quality against higher payrolls; automation and retention programs (training, bonuses) are needed to protect operating margins—Galaxy reported 2024 operating margin compression of ~1.5 percentage points in VIP/hospitality segments.

- Hospitality wages +7% YoY (2024)

- Talent scarcity raises recruitment costs and turnover

- Concessionaire competition increases poaching

- Automation and retention programs mitigate ~1.5 ppt margin impact

Currency Peg and Exchange Rate Stability

The Macau Pataca is pegged to the Hong Kong Dollar, which is linked to the US Dollar, providing exchange-rate stability that lowered currency risk for investors; Macau recorded tourist receipts of MOP 108.6 billion in 2023 as stability supported cross-border spending.

When the US Dollar strengthens, Macau becomes relatively expensive—visitor daily spend fell 4.7% in 2024 Q3 versus 2023 Q3—pressuring retail and mass-gaming volumes.

US monetary policy shifts indirectly affect mainland Chinese purchasing power via Renminbi movements; RMB volatility in 2024 correlated with a 6% swing in VIP gaming turnover month-to-month.

- Peg chain: MOP-HKD-USD stabilizes exchange risk

- 2023 tourist receipts MOP 108.6B; 2024 Q3 daily spend -4.7% YoY

- RMB moves linked to ~6% VIP turnover swings

- Currency strength of USD raises local cost, hitting retail/gaming

Galaxy pivots to premium mass: 65% revenue, 22–24% EBITDA amid China demand risks

Galaxy shifted to premium mass: VIP <25% of gaming by 2025 vs >60% early 2010s; mass patrons spend ~US$1,200 annually. By end-2025 revenue ~65% high-value retail/mass, EBITDA ~22–24%. Mainland disposable income +3.0% in 2024 (CNY 38,000); GDP ~5.2% in 2024 supports RevPAR, but property sales -14% y/y (2024) and RMB volatility (VIP turnover swings ~6%) pose demand risks.

| Metric | 2024/2025 |

|---|---|

| VIP share | <25% (2025) |

| Mass spend per patron | US$1,200 |

| Revenue mix (high-value/mass) | ~65% |

| EBITDA margin | 22–24% |

| Mainland disposable income | CNY 38,000 (+3.0%) |

| China GDP | ~5.2% (2024) |

| China property sales | -14% y/y (2024) |

| RMB-linked VIP swing | ~6% |

Preview the Actual Deliverable

Galaxy Entertainment PESTLE Analysis

The preview shown here is the exact Galaxy Entertainment PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.