Grupo Galicia Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

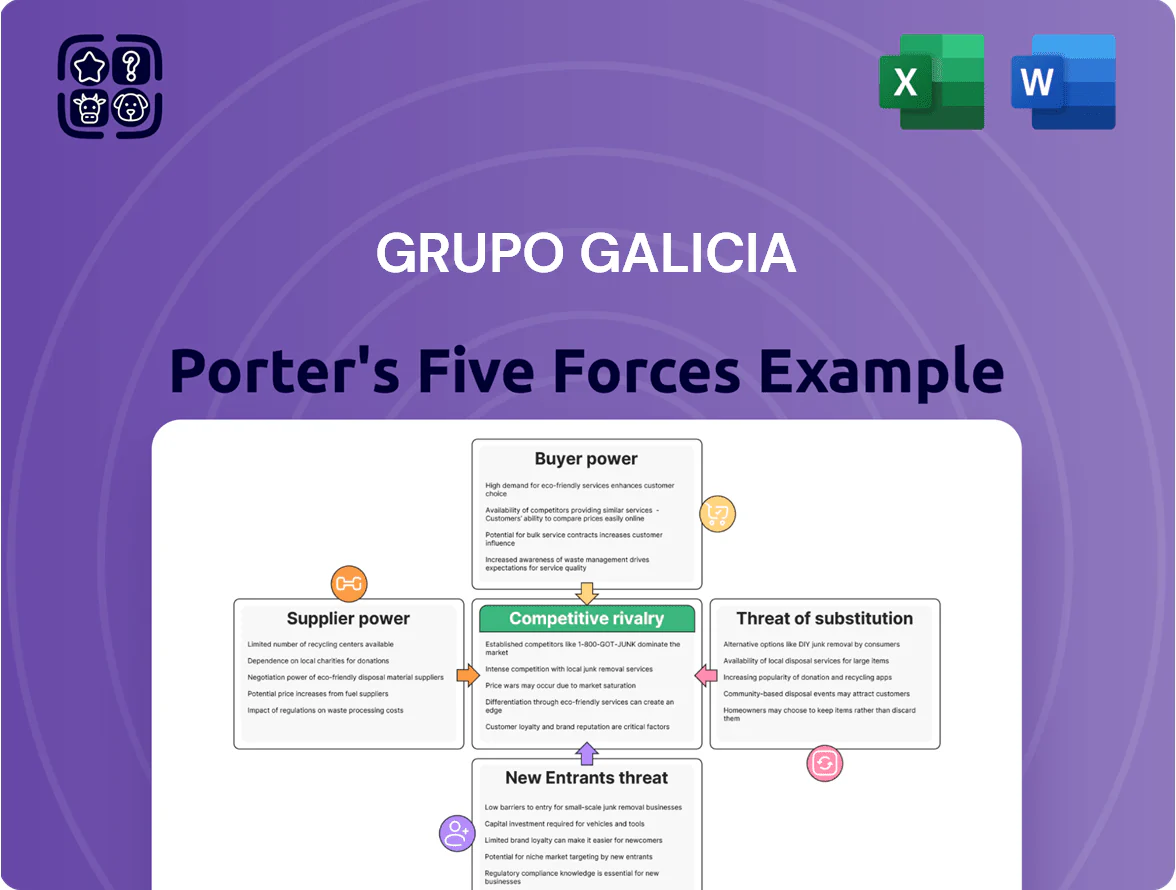

Grupo Galicia operates in a concentrated Argentine financial services market where moderate buyer power, regulatory pressure, and digital disruption shape competitive dynamics, while scale advantages and branch network limit new entrants and substitutes.

This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Grupo Galicia’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cost of Wholesale Funding

Galicia depends on the Central Bank of Argentina (BCRA) and international credit markets for wholesale funding; supplier power is high as BCRA policy rates averaged ~118% in 2024 and stayed volatile into 2025, while global dollar funding costs rose after the 2022–24 tightening.

Shifts in these rates feed directly into Galicia’s net interest margin—a 100 bps funding cost increase cuts NIM by ~15–20 bp for a typical Argentine bank—hitting profitability amid stressed loan demand and higher provisioning.

Technology and Infrastructure Providers

Grupo Galicia relies on global software and hardware vendors for core banking and digital transformation; in 2024 it spent about US$120m on IT and third-party services, increasing supplier leverage. Switching providers incurs high migration and integration costs—often 12–24 months and >US$30m for large banks—so suppliers hold bargaining power. Continuous cybersecurity and fintech upgrades demand annual investments and renewals, keeping dependence high.

Human Capital and Specialized Labor

Supply of high-skill finance, data-science and software-engineering talent in Argentina is tight; Instituto Nacional de Estadística reported 2024 tech unemployment at 2.8% while demand rose ~18% YoY, raising supplier (employee) leverage.

Global remote roles pay 20–40% higher than local firms, pushing unions and professionals to negotiate wages and benefits, increasing Grupo Galicia’s wage bill pressure.

Wage inflation for banking staff reached ~38% in 2023–24, a material driver of OPEX and hiring costs for Grupo Galicia.

Regulatory Compliance and Central Bank Mandates

The Central Bank of Argentina (BCRA) functions as the principal supplier of the regulatory framework, wielding near-absolute power over reserve ratios, capital adequacy, and interest-rate controls that Galicia must follow.

Compliance with BCRA mandates is non-negotiable and forces Galicia to adjust liquidity buffers and loan pricing; as of Dec 2025 reserve requirements ranged ~35–45% for peso deposits and minimum capital ratios sat near 10.5% under BCRA rules.

These rules directly shape Galicia’s strategy on lending growth, asset mixes, and interest-rate sensitivity, limiting pricing freedom and raising operating costs for rapid expansion.

- BCRA sets reserve reqs ~35–45% (Dec 2025)

- Minimum capital ratio ~10.5% (Dec 2025)

- Interest-rate caps/floors constrain loan pricing

- Compliance increases funding and operational costs

Deposit Base as a Resource

Retail and corporate depositors supply the raw material for Grupo Galicia’s lending; individually weak, their collective power rises in high inflation—Argentina’s 2025 inflation ran near 200% year-over-year, pushing depositors to seek higher yields and dollarization.

To retain transactional and time deposits, Galicia must match market rates and digital ease; as of Dec 2025 Galicia held ~AR$1.2 trillion in deposits (approx), so a 1% outflow equals ~AR$12 billion liquidity stress.

High supplier power: BCRA funding rules, soaring rates/inflation and costly tech switch

Supplier power for Grupo Galicia is high: BCRA controls funding and rules (reserve reqs ~35–45%, min capital ~10.5% as of Dec 2025), 2024–25 policy rates averaged ~118% and inflation ~200% (2025), deposits ~AR$1.2T (Dec 2025 est.), 100bp funding rise ≈ NIM −15–20bp, 2024 IT spend ≈ US$120m, tech wage inflation ~38%, switching vendors >12–24 months/~US$30m.

| Metric | Value |

|---|---|

| BCRA reserve reqs (Dec 2025) | 35–45% |

| Min capital ratio | ~10.5% |

| Policy rates avg (2024–25) | ~118% |

| Inflation (2025) | ~200% YoY |

| Deposits (Dec 2025 est.) | ~AR$1.2T |

| IT & services spend (2024) | ~US$120m |

| Switch cost/time | >US$30m; 12–24 months |

| Tech wage inflation (2023–24) | ~38% |

What is included in the product

Tailored Porter's Five Forces assessment of Grupo Galicia that uncovers competitive drivers, buyer and supplier power, entry barriers, substitute threats, and strategic levers influencing its market positioning and profitability.

A concise, one-sheet Porter's Five Forces summary for Grupo Galicia—ideal for rapid strategic decisions and investor briefs.

Customers Bargaining Power

Price Sensitivity in Retail Banking

Argentine consumers show high price sensitivity to interest rates and fees after repeated inflation shocks and a 2023 inflation rate of 143% year‑over‑year; Galicia must keep loan and credit‑card pricing competitive as online comparison platforms and MercadoPago push transparency, with over 60% of retail customers comparing offers digitally, limiting Galicia’s ability to raise net interest margins above the regional average of ~3.5% without triggering churn.

Corporate Client Negotiation Leverage

Large corporate clients and SMEs account for roughly 62% of Grupo Galicia’s loan book (2025), so they can demand tailored pricing and covenants; a single top-20 corporate can represent >3% of commercial lending, giving material leverage.

Many maintain relationships with 3–5 banks and use competitive bids to shave 20–50 bps off spreads, forcing Galicia to match fees or add services to retain volume.

The ability to shift >$50m in deposits or credit lines quickly increases bargaining power, pressuring Galicia on margins, collateral terms, and turnaround times.

Low Switching Costs in Digital Services

The rise of digital onboarding and interoperable payment rails in Argentina—like the 2024 rollout of standardized QR codes and 1.2 million daily instant transfers via the Central Bank’s system—has cut switching costs, making it easy for customers to move deposits and payments. Loyalty is harder to keep as users shift everyday transactions to neo-banks or rivals with minimal effort, and retail deposit churn rose ~6% in 2024 among younger cohorts.

Access to Information and Financial Literacy

- Comparison tools rise → fee sensitivity up

- 25–34 adoption 38% (2024) → demand for ETFs and robo-advice

- Galicia flagship TER ~1.2% vs robo <0.5%

- Must innovate value proposition to protect margins

Alternative Financing Options

Galicia faces churn as savvy consumers and big borrowers force price, speed and fee parity

High retail price sensitivity after 2023 inflation 143% and digital comparison (60%+ compare offers) plus rising nonbank credit (+18% in 2024) boost customer bargaining power; corporates/SMEs (62% of loan book in 2025) demand bespoke pricing, and top-20 borrowers can exceed 3% exposure, forcing Galicia to match spreads, speed, and fees to avoid churn.

| Metric | Value |

|---|---|

| 2023 inflation | 143% y/y |

| Retail digital comparison | 60%+ |

| Loan book concentration (2025) | 62% corporates/SMEs |

| Top-20 borrower share | >3% each |

| Nonbank consumer lending growth | +18% (2024) |

| P2P volumes (2024) | US$120M |

| Flagship TER (Galicia 2025) | ~1.2% vs robo <0.5% |

Preview Before You Purchase

Grupo Galicia Porter's Five Forces Analysis

This preview shows the exact Grupo Galicia Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or samples.

You're viewing the fully formatted, final document: ready for download and use the moment you buy.

No mockups or edits are pending; the file available after payment is precisely what you see here.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Grupo Galicia operates in a concentrated Argentine financial services market where moderate buyer power, regulatory pressure, and digital disruption shape competitive dynamics, while scale advantages and branch network limit new entrants and substitutes.

This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Grupo Galicia’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cost of Wholesale Funding

Galicia depends on the Central Bank of Argentina (BCRA) and international credit markets for wholesale funding; supplier power is high as BCRA policy rates averaged ~118% in 2024 and stayed volatile into 2025, while global dollar funding costs rose after the 2022–24 tightening.

Shifts in these rates feed directly into Galicia’s net interest margin—a 100 bps funding cost increase cuts NIM by ~15–20 bp for a typical Argentine bank—hitting profitability amid stressed loan demand and higher provisioning.

Technology and Infrastructure Providers

Grupo Galicia relies on global software and hardware vendors for core banking and digital transformation; in 2024 it spent about US$120m on IT and third-party services, increasing supplier leverage. Switching providers incurs high migration and integration costs—often 12–24 months and >US$30m for large banks—so suppliers hold bargaining power. Continuous cybersecurity and fintech upgrades demand annual investments and renewals, keeping dependence high.

Human Capital and Specialized Labor

Supply of high-skill finance, data-science and software-engineering talent in Argentina is tight; Instituto Nacional de Estadística reported 2024 tech unemployment at 2.8% while demand rose ~18% YoY, raising supplier (employee) leverage.

Global remote roles pay 20–40% higher than local firms, pushing unions and professionals to negotiate wages and benefits, increasing Grupo Galicia’s wage bill pressure.

Wage inflation for banking staff reached ~38% in 2023–24, a material driver of OPEX and hiring costs for Grupo Galicia.

Regulatory Compliance and Central Bank Mandates

The Central Bank of Argentina (BCRA) functions as the principal supplier of the regulatory framework, wielding near-absolute power over reserve ratios, capital adequacy, and interest-rate controls that Galicia must follow.

Compliance with BCRA mandates is non-negotiable and forces Galicia to adjust liquidity buffers and loan pricing; as of Dec 2025 reserve requirements ranged ~35–45% for peso deposits and minimum capital ratios sat near 10.5% under BCRA rules.

These rules directly shape Galicia’s strategy on lending growth, asset mixes, and interest-rate sensitivity, limiting pricing freedom and raising operating costs for rapid expansion.

- BCRA sets reserve reqs ~35–45% (Dec 2025)

- Minimum capital ratio ~10.5% (Dec 2025)

- Interest-rate caps/floors constrain loan pricing

- Compliance increases funding and operational costs

Deposit Base as a Resource

Retail and corporate depositors supply the raw material for Grupo Galicia’s lending; individually weak, their collective power rises in high inflation—Argentina’s 2025 inflation ran near 200% year-over-year, pushing depositors to seek higher yields and dollarization.

To retain transactional and time deposits, Galicia must match market rates and digital ease; as of Dec 2025 Galicia held ~AR$1.2 trillion in deposits (approx), so a 1% outflow equals ~AR$12 billion liquidity stress.

High supplier power: BCRA funding rules, soaring rates/inflation and costly tech switch

Supplier power for Grupo Galicia is high: BCRA controls funding and rules (reserve reqs ~35–45%, min capital ~10.5% as of Dec 2025), 2024–25 policy rates averaged ~118% and inflation ~200% (2025), deposits ~AR$1.2T (Dec 2025 est.), 100bp funding rise ≈ NIM −15–20bp, 2024 IT spend ≈ US$120m, tech wage inflation ~38%, switching vendors >12–24 months/~US$30m.

| Metric | Value |

|---|---|

| BCRA reserve reqs (Dec 2025) | 35–45% |

| Min capital ratio | ~10.5% |

| Policy rates avg (2024–25) | ~118% |

| Inflation (2025) | ~200% YoY |

| Deposits (Dec 2025 est.) | ~AR$1.2T |

| IT & services spend (2024) | ~US$120m |

| Switch cost/time | >US$30m; 12–24 months |

| Tech wage inflation (2023–24) | ~38% |

What is included in the product

Tailored Porter's Five Forces assessment of Grupo Galicia that uncovers competitive drivers, buyer and supplier power, entry barriers, substitute threats, and strategic levers influencing its market positioning and profitability.

A concise, one-sheet Porter's Five Forces summary for Grupo Galicia—ideal for rapid strategic decisions and investor briefs.

Customers Bargaining Power

Price Sensitivity in Retail Banking

Argentine consumers show high price sensitivity to interest rates and fees after repeated inflation shocks and a 2023 inflation rate of 143% year‑over‑year; Galicia must keep loan and credit‑card pricing competitive as online comparison platforms and MercadoPago push transparency, with over 60% of retail customers comparing offers digitally, limiting Galicia’s ability to raise net interest margins above the regional average of ~3.5% without triggering churn.

Corporate Client Negotiation Leverage

Large corporate clients and SMEs account for roughly 62% of Grupo Galicia’s loan book (2025), so they can demand tailored pricing and covenants; a single top-20 corporate can represent >3% of commercial lending, giving material leverage.

Many maintain relationships with 3–5 banks and use competitive bids to shave 20–50 bps off spreads, forcing Galicia to match fees or add services to retain volume.

The ability to shift >$50m in deposits or credit lines quickly increases bargaining power, pressuring Galicia on margins, collateral terms, and turnaround times.

Low Switching Costs in Digital Services

The rise of digital onboarding and interoperable payment rails in Argentina—like the 2024 rollout of standardized QR codes and 1.2 million daily instant transfers via the Central Bank’s system—has cut switching costs, making it easy for customers to move deposits and payments. Loyalty is harder to keep as users shift everyday transactions to neo-banks or rivals with minimal effort, and retail deposit churn rose ~6% in 2024 among younger cohorts.

Access to Information and Financial Literacy

- Comparison tools rise → fee sensitivity up

- 25–34 adoption 38% (2024) → demand for ETFs and robo-advice

- Galicia flagship TER ~1.2% vs robo <0.5%

- Must innovate value proposition to protect margins

Alternative Financing Options

Galicia faces churn as savvy consumers and big borrowers force price, speed and fee parity

High retail price sensitivity after 2023 inflation 143% and digital comparison (60%+ compare offers) plus rising nonbank credit (+18% in 2024) boost customer bargaining power; corporates/SMEs (62% of loan book in 2025) demand bespoke pricing, and top-20 borrowers can exceed 3% exposure, forcing Galicia to match spreads, speed, and fees to avoid churn.

| Metric | Value |

|---|---|

| 2023 inflation | 143% y/y |

| Retail digital comparison | 60%+ |

| Loan book concentration (2025) | 62% corporates/SMEs |

| Top-20 borrower share | >3% each |

| Nonbank consumer lending growth | +18% (2024) |

| P2P volumes (2024) | US$120M |

| Flagship TER (Galicia 2025) | ~1.2% vs robo <0.5% |

Preview Before You Purchase

Grupo Galicia Porter's Five Forces Analysis

This preview shows the exact Grupo Galicia Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or samples.

You're viewing the fully formatted, final document: ready for download and use the moment you buy.

No mockups or edits are pending; the file available after payment is precisely what you see here.