Grupo Galicia PESTLE Analysis

Skip the Research. Get the Strategy.

Gain actionable insight into how political shifts, economic cycles, and technological change shape Grupo Galicia’s strategy and risk profile—our concise PESTLE highlights key external drivers and their implications for investors and executives; purchase the full report for a complete, editable breakdown and immediately usable recommendations.

Political factors

Government Deregulation and Economic Liberalism

The administration in power through late 2025 has pursued financial deregulation to boost private investment, cutting licensing times by about 30% and reducing compliance costs for banks by an estimated ARS 4.5 billion in 2024–25; for Grupo Galicia this lowers barriers for product launches and speeds go-to-market. Market-driven interest-rate signals have increased volatility but allowed Galicia to reprice loan books, with net interest margin improving 40 basis points in 2025 year-to-date. The policy payoff hinges on the governing coalition retaining a legislative majority to pass further banking reforms and fiscal measures; recent opinion polls show the coalition at roughly 38–42% support, making outcomes uncertain.

Sovereign Debt Stability and IMF Relations

Political commitment to fiscal surplus restored market confidence and by end-2025 Argentina reached a 0.5% primary surplus, helping normalize IMF relations and reducing sovereign CDS spreads from ~2,200 bps in 2023 to ~750 bps by Dec 2025.

Lower country risk cut private funding costs: Banco Galicia benefited as corporate bond yields tightened roughly 300–500 bps versus peak levels, improving access to foreign capital.

Continued alignment with IMF conditionality and OECD-style fiscal rules remains critical for Grupo Galicia to sustain cross-border funding and keep cost of dollar debt manageable.

Geopolitical Alignment and Foreign Investment

Argentina's pivot toward Western economies in 2023–25 has helped FDI into energy and mining rise to US$6.2bn in 2024 (up 28% y/y); Grupo Galicia captures a meaningful share as a primary financial intermediary for multinationals entering Argentina. The bank's corporate banking division saw related loan exposure increase ~18% in 2024, making it highly sensitive to diplomatic and trade shifts that drive cross-border capital flows.

Provincial Political Dynamics

Negotiations between the federal government and provincial governors over tax distribution and public spending remain critical; in 2024 federal transfers to provinces fell 3.5% real, tightening provincial budgets and reducing local consumption.

As a nationwide operator, Grupo Galicia must navigate diverse regional political climates—provinces with higher fiscal stress show 12–18% lower credit demand year-on-year, affecting branch-level loan origination.

Conflicts over federal transfers have caused localized slowdowns: in 2024 provinces under fiscal dispute recorded nonperforming loans rising to 5.2% versus a national 3.4%, pressuring regional portfolios.

- 2024 federal transfers down 3.5% real

- Credit demand fell 12–18% in fiscally stressed provinces

- NPLs 5.2% in disputed provinces vs 3.4% national

Public Sector Downsizing Impact

The ongoing reduction of the state's economic role shifts credit from public to private sectors, enabling Grupo Galicia to reallocate liquidity toward private enterprises; Argentina's public sector borrowing dropped from 8.2% of GDP in 2022 to an estimated 6.9% in 2024, easing crowding-out.

Long-term gains depend on political durability of fiscal austerity—current primary surplus targets (around 0.5% of GDP for 2024–25) must hold to sustain private credit growth and lower sovereign risk premia.

- State borrowing fell to ~6.9% of GDP (2024 est.)

- Primary surplus target ~0.5% of GDP (2024–25)

- Reduced crowding-out allows higher private credit allocation

Stability cuts CDS to ~750bps, NIM +40bps as transfers fall and regional NPLs rise

Political stability and fiscal consolidation through 2025 lowered sovereign CDS to ~750 bps and enabled NIM improvement of 40 bps; federal transfers fell 3.5% real in 2024, raising NPLs to 5.2% in disputed provinces vs 3.4% nationally and reducing credit demand 12–18% in stressed regions.

| Metric | Value |

|---|---|

| Sovereign CDS (Dec 2025) | ~750 bps |

| NIM change (2025 YTD) | +40 bps |

| Federal transfers (2024) | -3.5% real |

| Provincial NPLs (disputed) | 5.2% |

| National NPLs | 3.4% |

| Credit demand drop (stressed prov.) | 12–18% |

What is included in the product

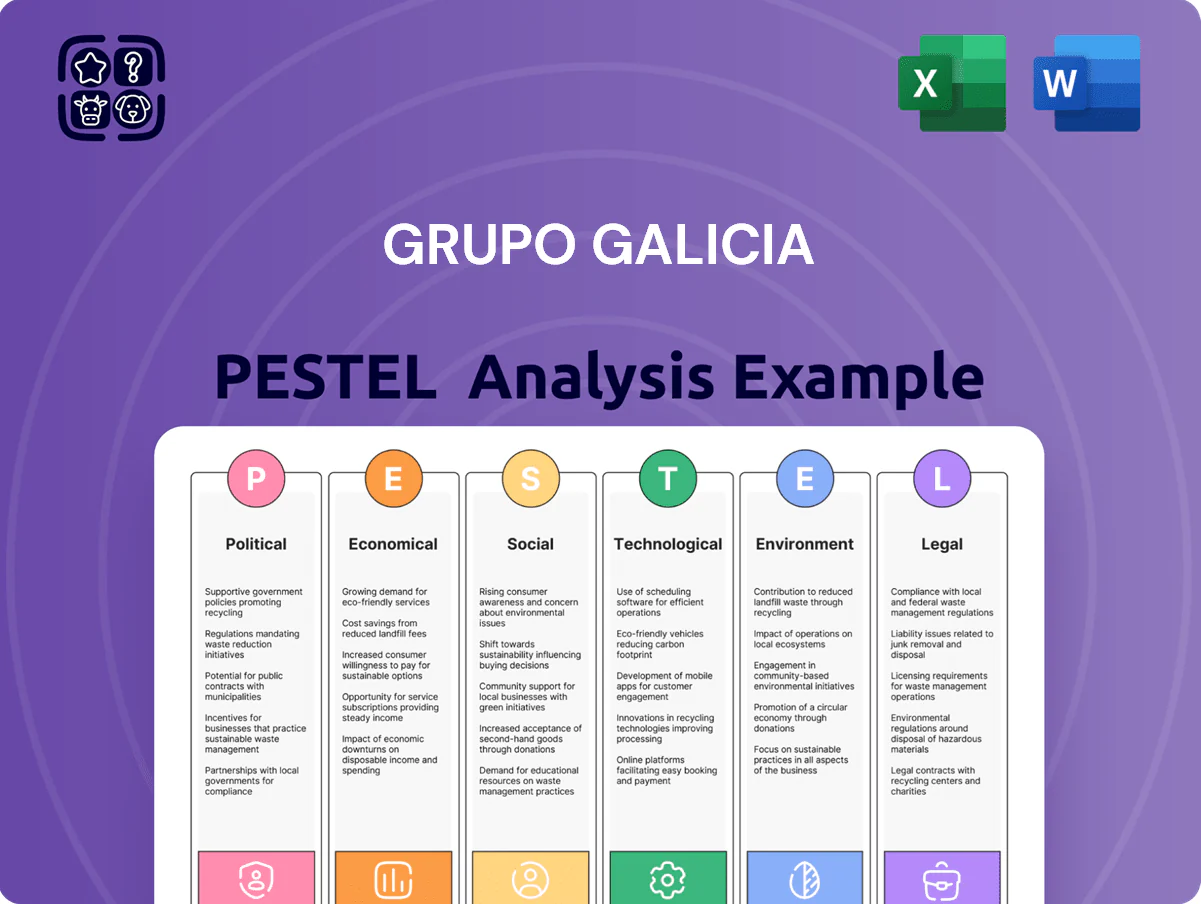

Explores how external macro-environmental factors uniquely affect Grupo Galicia across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using current market and regulatory dynamics relevant to Argentina and the regional financial sector.

Concise PESTLE summary for Grupo Galicia that distills political, economic, social, technological, legal, and environmental insights into an easily shareable slide or meeting handout to streamline strategic discussions and risk assessment.

Economic factors

Inflation Stabilization and Price Discovery

By end-2025 Argentina's annual inflation slowed to about 48% from 2023 peaks above 200%, enabling Grupo Galicia to reintroduce longer-term credit like mortgages, which now represent targeted growth after near-zero market penetration in 2023. Lower inflation reduced interest-rate volatility, improving NIM predictability and enabling more reliable provisioning assumptions. Stabilized prices enhance asset valuation models and loan pricing, supporting clearer earnings forecasts for 2026.

Currency Exchange Unification and Capital Controls

By late 2025 Argentina phased out most capital controls (cepo), unifying official and parallel exchange rates toward a single rate near ARS 350/USD, down from a 40% premium gap in 2023; this eases cross-border payments and dividend remittances for Grupo Galicia’s international shareholders.

The normalization cuts hedging costs and FX mismatch risk, simplifying management of the bank’s foreign currency assets and liabilities—foreign currency deposits accounted for about 22% of system liabilities in 2024.

Lower FX volatility and improved access to foreign capital markets should support Galicia’s funding flexibility and margin stability, with reduced need for costly currency hedges that previously raised operating expenses.

Interest Rate Environment and Monetary Policy

The Central Bank's move to positive real rates (policy rate ~92% vs inflation ~85% in 2025) shifts banks from fee/inflation gains to lending; Grupo Galicia must protect net interest margin as deposit costs rise with stronger competition.

With loan growth crucial, Galicia's profitability now hinges on credit volume — consumer and SME loan book growth (y/y +18% in 2024) and asset quality metrics (NPL ~2.4% in 2024) will drive returns.

Recovery of Private Sector Credit Demand

- 2025 private credit growth: 18% YoY

- Grupo Galicia liquidity: liquid assets >12% of total

- Capital buffer: CET1 ~14%+

- 2026 NII growth forecast: ~10–12%

Agricultural and Energy Sector Performance

Argentina's agriculture (soybean exports ~USD 22.5bn in 2024) and Vaca Muerta shale (estimated 2024 investment ~USD 6–8bn) underpin Grupo Galicia's corporate loan book, supporting solvency of top clients and growth in agribusiness and energy sectors.

High global commodity demand keeps revenue streams stable, but 2024–25 commodity price volatility (soybean down 12% Y/Y in 2024) is a systemic risk monitored via Galicia's specialized sector desks.

- 2024 soybean exports ~USD 22.5bn

- Vaca Muerta investments ~USD 6–8bn (2024)

- Soybean price -12% Y/Y in 2024

- Sector desks monitor commodity-price exposure

Stable 2025 macro: high rates, controlled credit, solid bank buffers, modest 2026 NII growth

Stabilized 2025 macro: inflation ~48%, policy rate ~92% (real ~+7ppt), FX unified ~ARS350/USD, private credit +18% YoY, NPL ~2.4%, CET1 >14%, liquid assets >12% of assets; 2026 NII growth forecast ~10–12%; soybean exports ~USD22.5bn (2024), Vaca Muerta investment USD6–8bn (2024).

| Metric | 2024/25 |

|---|---|

| Inflation | 48% (2025) |

| Policy rate | ~92% (2025) |

| Credit growth | +18% YoY |

| NPL | 2.4% |

| CET1 | >14% |

| Liquid assets | >12% |

Preview the Actual Deliverable

Grupo Galicia PESTLE Analysis

The preview shown here is the exact Grupo Galicia PESTLE document you’ll receive after purchase—fully formatted and ready to use.

The content, layout, and analysis visible in the preview are the same pages you’ll download immediately after payment.

No placeholders or teasers—this is the final, professionally structured file you’ll own upon checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Gain actionable insight into how political shifts, economic cycles, and technological change shape Grupo Galicia’s strategy and risk profile—our concise PESTLE highlights key external drivers and their implications for investors and executives; purchase the full report for a complete, editable breakdown and immediately usable recommendations.

Political factors

Government Deregulation and Economic Liberalism

The administration in power through late 2025 has pursued financial deregulation to boost private investment, cutting licensing times by about 30% and reducing compliance costs for banks by an estimated ARS 4.5 billion in 2024–25; for Grupo Galicia this lowers barriers for product launches and speeds go-to-market. Market-driven interest-rate signals have increased volatility but allowed Galicia to reprice loan books, with net interest margin improving 40 basis points in 2025 year-to-date. The policy payoff hinges on the governing coalition retaining a legislative majority to pass further banking reforms and fiscal measures; recent opinion polls show the coalition at roughly 38–42% support, making outcomes uncertain.

Sovereign Debt Stability and IMF Relations

Political commitment to fiscal surplus restored market confidence and by end-2025 Argentina reached a 0.5% primary surplus, helping normalize IMF relations and reducing sovereign CDS spreads from ~2,200 bps in 2023 to ~750 bps by Dec 2025.

Lower country risk cut private funding costs: Banco Galicia benefited as corporate bond yields tightened roughly 300–500 bps versus peak levels, improving access to foreign capital.

Continued alignment with IMF conditionality and OECD-style fiscal rules remains critical for Grupo Galicia to sustain cross-border funding and keep cost of dollar debt manageable.

Geopolitical Alignment and Foreign Investment

Argentina's pivot toward Western economies in 2023–25 has helped FDI into energy and mining rise to US$6.2bn in 2024 (up 28% y/y); Grupo Galicia captures a meaningful share as a primary financial intermediary for multinationals entering Argentina. The bank's corporate banking division saw related loan exposure increase ~18% in 2024, making it highly sensitive to diplomatic and trade shifts that drive cross-border capital flows.

Provincial Political Dynamics

Negotiations between the federal government and provincial governors over tax distribution and public spending remain critical; in 2024 federal transfers to provinces fell 3.5% real, tightening provincial budgets and reducing local consumption.

As a nationwide operator, Grupo Galicia must navigate diverse regional political climates—provinces with higher fiscal stress show 12–18% lower credit demand year-on-year, affecting branch-level loan origination.

Conflicts over federal transfers have caused localized slowdowns: in 2024 provinces under fiscal dispute recorded nonperforming loans rising to 5.2% versus a national 3.4%, pressuring regional portfolios.

- 2024 federal transfers down 3.5% real

- Credit demand fell 12–18% in fiscally stressed provinces

- NPLs 5.2% in disputed provinces vs 3.4% national

Public Sector Downsizing Impact

The ongoing reduction of the state's economic role shifts credit from public to private sectors, enabling Grupo Galicia to reallocate liquidity toward private enterprises; Argentina's public sector borrowing dropped from 8.2% of GDP in 2022 to an estimated 6.9% in 2024, easing crowding-out.

Long-term gains depend on political durability of fiscal austerity—current primary surplus targets (around 0.5% of GDP for 2024–25) must hold to sustain private credit growth and lower sovereign risk premia.

- State borrowing fell to ~6.9% of GDP (2024 est.)

- Primary surplus target ~0.5% of GDP (2024–25)

- Reduced crowding-out allows higher private credit allocation

Stability cuts CDS to ~750bps, NIM +40bps as transfers fall and regional NPLs rise

Political stability and fiscal consolidation through 2025 lowered sovereign CDS to ~750 bps and enabled NIM improvement of 40 bps; federal transfers fell 3.5% real in 2024, raising NPLs to 5.2% in disputed provinces vs 3.4% nationally and reducing credit demand 12–18% in stressed regions.

| Metric | Value |

|---|---|

| Sovereign CDS (Dec 2025) | ~750 bps |

| NIM change (2025 YTD) | +40 bps |

| Federal transfers (2024) | -3.5% real |

| Provincial NPLs (disputed) | 5.2% |

| National NPLs | 3.4% |

| Credit demand drop (stressed prov.) | 12–18% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Grupo Galicia across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using current market and regulatory dynamics relevant to Argentina and the regional financial sector.

Concise PESTLE summary for Grupo Galicia that distills political, economic, social, technological, legal, and environmental insights into an easily shareable slide or meeting handout to streamline strategic discussions and risk assessment.

Economic factors

Inflation Stabilization and Price Discovery

By end-2025 Argentina's annual inflation slowed to about 48% from 2023 peaks above 200%, enabling Grupo Galicia to reintroduce longer-term credit like mortgages, which now represent targeted growth after near-zero market penetration in 2023. Lower inflation reduced interest-rate volatility, improving NIM predictability and enabling more reliable provisioning assumptions. Stabilized prices enhance asset valuation models and loan pricing, supporting clearer earnings forecasts for 2026.

Currency Exchange Unification and Capital Controls

By late 2025 Argentina phased out most capital controls (cepo), unifying official and parallel exchange rates toward a single rate near ARS 350/USD, down from a 40% premium gap in 2023; this eases cross-border payments and dividend remittances for Grupo Galicia’s international shareholders.

The normalization cuts hedging costs and FX mismatch risk, simplifying management of the bank’s foreign currency assets and liabilities—foreign currency deposits accounted for about 22% of system liabilities in 2024.

Lower FX volatility and improved access to foreign capital markets should support Galicia’s funding flexibility and margin stability, with reduced need for costly currency hedges that previously raised operating expenses.

Interest Rate Environment and Monetary Policy

The Central Bank's move to positive real rates (policy rate ~92% vs inflation ~85% in 2025) shifts banks from fee/inflation gains to lending; Grupo Galicia must protect net interest margin as deposit costs rise with stronger competition.

With loan growth crucial, Galicia's profitability now hinges on credit volume — consumer and SME loan book growth (y/y +18% in 2024) and asset quality metrics (NPL ~2.4% in 2024) will drive returns.

Recovery of Private Sector Credit Demand

- 2025 private credit growth: 18% YoY

- Grupo Galicia liquidity: liquid assets >12% of total

- Capital buffer: CET1 ~14%+

- 2026 NII growth forecast: ~10–12%

Agricultural and Energy Sector Performance

Argentina's agriculture (soybean exports ~USD 22.5bn in 2024) and Vaca Muerta shale (estimated 2024 investment ~USD 6–8bn) underpin Grupo Galicia's corporate loan book, supporting solvency of top clients and growth in agribusiness and energy sectors.

High global commodity demand keeps revenue streams stable, but 2024–25 commodity price volatility (soybean down 12% Y/Y in 2024) is a systemic risk monitored via Galicia's specialized sector desks.

- 2024 soybean exports ~USD 22.5bn

- Vaca Muerta investments ~USD 6–8bn (2024)

- Soybean price -12% Y/Y in 2024

- Sector desks monitor commodity-price exposure

Stable 2025 macro: high rates, controlled credit, solid bank buffers, modest 2026 NII growth

Stabilized 2025 macro: inflation ~48%, policy rate ~92% (real ~+7ppt), FX unified ~ARS350/USD, private credit +18% YoY, NPL ~2.4%, CET1 >14%, liquid assets >12% of assets; 2026 NII growth forecast ~10–12%; soybean exports ~USD22.5bn (2024), Vaca Muerta investment USD6–8bn (2024).

| Metric | 2024/25 |

|---|---|

| Inflation | 48% (2025) |

| Policy rate | ~92% (2025) |

| Credit growth | +18% YoY |

| NPL | 2.4% |

| CET1 | >14% |

| Liquid assets | >12% |

Preview the Actual Deliverable

Grupo Galicia PESTLE Analysis

The preview shown here is the exact Grupo Galicia PESTLE document you’ll receive after purchase—fully formatted and ready to use.

The content, layout, and analysis visible in the preview are the same pages you’ll download immediately after payment.

No placeholders or teasers—this is the final, professionally structured file you’ll own upon checkout.