Galliford Try Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

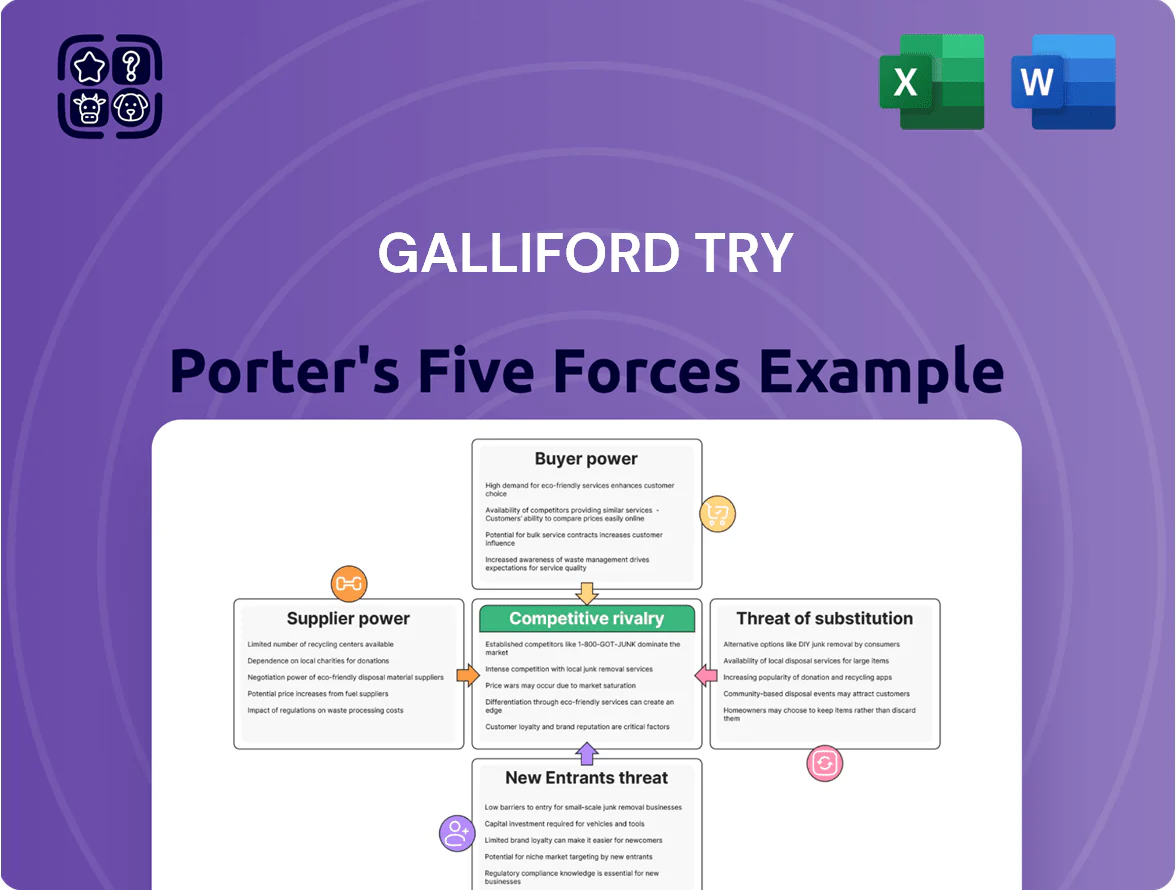

Galliford Try faces high competitive intensity from established contractors, moderate supplier power tied to materials and skilled labour, and tangible threats from new entrants and substitutes in modular construction—while regulatory and public-sector demand shape long-term opportunities and risks; this snapshot highlights where strategic focus matters most. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications tailored to Galliford Try.

Suppliers Bargaining Power

Skilled Labor Shortages and Wage Inflation

The UK construction sector faced a shortfall of about 200,000 skilled workers by late 2025, boosting bargaining power for trades and specialist agencies; that scarcity pushed average construction wages up roughly 7.5% y/y in 2024–25.

Galliford Try saw labour cost inflation squeeze margins—staff costs rose ~6% in FY2025—forcing higher bid contingencies and use of subcontractor pass-throughs to protect margins across building and infrastructure projects.

Volatility in Essential Raw Material Pricing

Suppliers of steel, cement and timber hold moderate power for Galliford Try as global steel prices rose ~12% in 2024 and UK cement costs climbed 6% year-on-year, driven by energy and freight volatility.

Supply chains are steadier than 2020–22, but demand for low-carbon concrete and FSC-certified timber commands premiums of 8–20%, tightening supplier leverage.

Galliford Try offsets swings via multi-year purchase agreements and indexed hedges; in 2024 these contracts covered roughly 40% of anticipated core-material spend.

Specialized Sub-contractor Dependency

For complex water and highways projects Galliford Try relies on a narrow pool of specialized sub-contractors whose niche skills are hard to replace quickly, raising supplier bargaining power during negotiations. These firms can command price premia; industry data shows specialist subcontract rates rose ~8% in 2024 in UK infrastructure markets. Strong, collaborative relationships and long-term frameworks are essential to de-risk schedules and hit delivery targets. Losing a key specialist could delay projects by months and add multi-million-pound costs.

ESG Compliance and Sustainable Sourcing

- 2025 rule: mandatory scope 1–3 carbon and ethical traces

- 42% suppliers invested in low-carbon by 2024

- 65% public tenders require verified sustainability

- Suppliers can command price premia and stricter terms

Digital Integration and Supply Chain Transparency

Digital integration via Building Information Modeling (BIM) and Galliford Try’s digital twins raises supplier power by rewarding those who sync logistics and inventory: integrated suppliers cut rework and delays—industry studies show BIM reduces project costs by ~20% and schedule overruns by ~18% (CPCS/EU data, 2023).

That integration creates soft switching costs: replacing a synced supplier risks losing real‑time material visibility and disrupting data workflows, raising time-to-replace and potential cost overruns.

- Integrated suppliers = higher value, lower rework

- BIM linked suppliers cut costs ~20%

- Soft switching cost: data/process disruption

- Non-integrated suppliers raise delay risk ~18%

Galliford Try faces supplier squeeze: labour shortfalls, rising materials & green mandates

Suppliers hold moderate-to-high bargaining power for Galliford Try due to skilled labour shortfalls (~200,000 UK deficit by late 2025), material price rises (steel +12% in 2024, cement +6% y/y) and niche subcontractor premia (+8% in 2024); 40% of material spend was hedged in 2024 and 65% of public tenders require verified sustainability.

| Metric | Value |

|---|---|

| Skilled labour gap (UK) | ~200,000 (late 2025) |

| Steel price change (2024) | +12% |

| Cement cost change (2024) | +6% y/y |

| Specialist subcontract rate rise (2024) | +8% |

| Core-material spend hedged (2024) | ~40% |

| Public tenders needing sustainability | 65% |

What is included in the product

Tailored Porter's Five Forces assessment of Galliford Try, revealing competitive intensity, buyer and supplier leverage, entry barriers, substitute threats, and strategic implications for profitability and market positioning.

A clear, one-sheet Porter's Five Forces summary for Galliford Try—instantly highlights competitive pressures to speed strategic decisions and investor briefings.

Customers Bargaining Power

Dominance of Public Sector Procurement

Framework Agreement Structures

Emphasis on Social Value and Qualitative Metrics

By 2025 procurement weights shifted: social value now often accounts for 20–30% of scoring on UK public contracts, with local employment and carbon reduction metrics increasingly decisive, not just price. Savvy clients use these qualitative filters to weed out low-cost bidders and demand wider corporate commitments; 68% of UK councils report prioritising community impact in 2024 tenders. Galliford Try must prove measurable benefits—jobs created, £-value local supply spend, and CO2 cuts—to win high-value projects.

Low Switching Costs in General Building

In private commercial building, switching costs between tier-one contractors are low, so price and track record drive selection; for example, private developers awarded 62% of UK office projects to the lowest-cost compliant bidder in 2024, per industry procurement reports.

This horizontal competition lets developers leverage contractors during bidding, pushing margins down—Galliford Try reported a 3.1% operating margin in 2024, reflecting sector price pressure.

- Low switching cost — many firms match capabilities

- Price and past performance are key deciders

- Developers play contractors off each other in bids

- 2024: 62% lowest-cost wins; sector margin pressure (Galliford Try 3.1%)

Sophisticated Technical Requirements

Clients in infrastructure are more technically savvy and now demand future-proof assets; 2024 UK public sector procurement showed 38% of contracts required digital twin or BIM Level 3 capabilities, pushing suppliers to raise technical standards.

This sophistication lets buyers probe engineering assumptions and insist on bespoke innovations, raising project scope and margin pressure for Galliford Try.

Galliford Try must keep investing in technical skills and tools—R&D and digital spend rose industry-wide ~12% in 2023—to meet these exacting professional clients.

- 38% of UK public contracts required BIM/digital twin (2024)

- Industry digital/R&D spend up ~12% (2023)

- Clients demand bespoke digital deliverables and future-proofing

Public sector drive squeezes margins as price competition and social value reshape bids

Public-sector clients hold strong buyer power (≈45% of 2024 revenue), driving low-margin frameworks (AMP8 cap £51bn; Galliford Try margins ~3–5%; 2024 operating margin 3.1%). Procurement weights now include 20–30% social value; 68% of councils prioritise community impact (2024). Private developers push price competition (62% lowest-cost wins, 2024), while 38% of contracts demanded BIM/digital twin (2024).

| Metric | Value |

|---|---|

| Public revenue share (2024) | ≈45% |

| AMP8 capital (2025–30) | £51bn |

| Operating margin (GT, 2024) | 3.1% |

Same Document Delivered

Galliford Try Porter's Five Forces Analysis

This preview shows the exact Galliford Try Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document displayed is fully formatted and ready for download and use the moment you buy. You're viewing the final, professionally written file; once payment is complete you'll get instant access to this same deliverable. No mockups—what you see is what you get.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Galliford Try faces high competitive intensity from established contractors, moderate supplier power tied to materials and skilled labour, and tangible threats from new entrants and substitutes in modular construction—while regulatory and public-sector demand shape long-term opportunities and risks; this snapshot highlights where strategic focus matters most. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications tailored to Galliford Try.

Suppliers Bargaining Power

Skilled Labor Shortages and Wage Inflation

The UK construction sector faced a shortfall of about 200,000 skilled workers by late 2025, boosting bargaining power for trades and specialist agencies; that scarcity pushed average construction wages up roughly 7.5% y/y in 2024–25.

Galliford Try saw labour cost inflation squeeze margins—staff costs rose ~6% in FY2025—forcing higher bid contingencies and use of subcontractor pass-throughs to protect margins across building and infrastructure projects.

Volatility in Essential Raw Material Pricing

Suppliers of steel, cement and timber hold moderate power for Galliford Try as global steel prices rose ~12% in 2024 and UK cement costs climbed 6% year-on-year, driven by energy and freight volatility.

Supply chains are steadier than 2020–22, but demand for low-carbon concrete and FSC-certified timber commands premiums of 8–20%, tightening supplier leverage.

Galliford Try offsets swings via multi-year purchase agreements and indexed hedges; in 2024 these contracts covered roughly 40% of anticipated core-material spend.

Specialized Sub-contractor Dependency

For complex water and highways projects Galliford Try relies on a narrow pool of specialized sub-contractors whose niche skills are hard to replace quickly, raising supplier bargaining power during negotiations. These firms can command price premia; industry data shows specialist subcontract rates rose ~8% in 2024 in UK infrastructure markets. Strong, collaborative relationships and long-term frameworks are essential to de-risk schedules and hit delivery targets. Losing a key specialist could delay projects by months and add multi-million-pound costs.

ESG Compliance and Sustainable Sourcing

- 2025 rule: mandatory scope 1–3 carbon and ethical traces

- 42% suppliers invested in low-carbon by 2024

- 65% public tenders require verified sustainability

- Suppliers can command price premia and stricter terms

Digital Integration and Supply Chain Transparency

Digital integration via Building Information Modeling (BIM) and Galliford Try’s digital twins raises supplier power by rewarding those who sync logistics and inventory: integrated suppliers cut rework and delays—industry studies show BIM reduces project costs by ~20% and schedule overruns by ~18% (CPCS/EU data, 2023).

That integration creates soft switching costs: replacing a synced supplier risks losing real‑time material visibility and disrupting data workflows, raising time-to-replace and potential cost overruns.

- Integrated suppliers = higher value, lower rework

- BIM linked suppliers cut costs ~20%

- Soft switching cost: data/process disruption

- Non-integrated suppliers raise delay risk ~18%

Galliford Try faces supplier squeeze: labour shortfalls, rising materials & green mandates

Suppliers hold moderate-to-high bargaining power for Galliford Try due to skilled labour shortfalls (~200,000 UK deficit by late 2025), material price rises (steel +12% in 2024, cement +6% y/y) and niche subcontractor premia (+8% in 2024); 40% of material spend was hedged in 2024 and 65% of public tenders require verified sustainability.

| Metric | Value |

|---|---|

| Skilled labour gap (UK) | ~200,000 (late 2025) |

| Steel price change (2024) | +12% |

| Cement cost change (2024) | +6% y/y |

| Specialist subcontract rate rise (2024) | +8% |

| Core-material spend hedged (2024) | ~40% |

| Public tenders needing sustainability | 65% |

What is included in the product

Tailored Porter's Five Forces assessment of Galliford Try, revealing competitive intensity, buyer and supplier leverage, entry barriers, substitute threats, and strategic implications for profitability and market positioning.

A clear, one-sheet Porter's Five Forces summary for Galliford Try—instantly highlights competitive pressures to speed strategic decisions and investor briefings.

Customers Bargaining Power

Dominance of Public Sector Procurement

Framework Agreement Structures

Emphasis on Social Value and Qualitative Metrics

By 2025 procurement weights shifted: social value now often accounts for 20–30% of scoring on UK public contracts, with local employment and carbon reduction metrics increasingly decisive, not just price. Savvy clients use these qualitative filters to weed out low-cost bidders and demand wider corporate commitments; 68% of UK councils report prioritising community impact in 2024 tenders. Galliford Try must prove measurable benefits—jobs created, £-value local supply spend, and CO2 cuts—to win high-value projects.

Low Switching Costs in General Building

In private commercial building, switching costs between tier-one contractors are low, so price and track record drive selection; for example, private developers awarded 62% of UK office projects to the lowest-cost compliant bidder in 2024, per industry procurement reports.

This horizontal competition lets developers leverage contractors during bidding, pushing margins down—Galliford Try reported a 3.1% operating margin in 2024, reflecting sector price pressure.

- Low switching cost — many firms match capabilities

- Price and past performance are key deciders

- Developers play contractors off each other in bids

- 2024: 62% lowest-cost wins; sector margin pressure (Galliford Try 3.1%)

Sophisticated Technical Requirements

Clients in infrastructure are more technically savvy and now demand future-proof assets; 2024 UK public sector procurement showed 38% of contracts required digital twin or BIM Level 3 capabilities, pushing suppliers to raise technical standards.

This sophistication lets buyers probe engineering assumptions and insist on bespoke innovations, raising project scope and margin pressure for Galliford Try.

Galliford Try must keep investing in technical skills and tools—R&D and digital spend rose industry-wide ~12% in 2023—to meet these exacting professional clients.

- 38% of UK public contracts required BIM/digital twin (2024)

- Industry digital/R&D spend up ~12% (2023)

- Clients demand bespoke digital deliverables and future-proofing

Public sector drive squeezes margins as price competition and social value reshape bids

Public-sector clients hold strong buyer power (≈45% of 2024 revenue), driving low-margin frameworks (AMP8 cap £51bn; Galliford Try margins ~3–5%; 2024 operating margin 3.1%). Procurement weights now include 20–30% social value; 68% of councils prioritise community impact (2024). Private developers push price competition (62% lowest-cost wins, 2024), while 38% of contracts demanded BIM/digital twin (2024).

| Metric | Value |

|---|---|

| Public revenue share (2024) | ≈45% |

| AMP8 capital (2025–30) | £51bn |

| Operating margin (GT, 2024) | 3.1% |

Same Document Delivered

Galliford Try Porter's Five Forces Analysis

This preview shows the exact Galliford Try Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document displayed is fully formatted and ready for download and use the moment you buy. You're viewing the final, professionally written file; once payment is complete you'll get instant access to this same deliverable. No mockups—what you see is what you get.