Galliford Try PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and environmental regulations are reshaping Galliford Try’s prospects—our concise PESTLE snapshot highlights key external risks and opportunities to inform smarter decisions; purchase the full analysis for the complete, editable report and actionable insights you can use immediately.

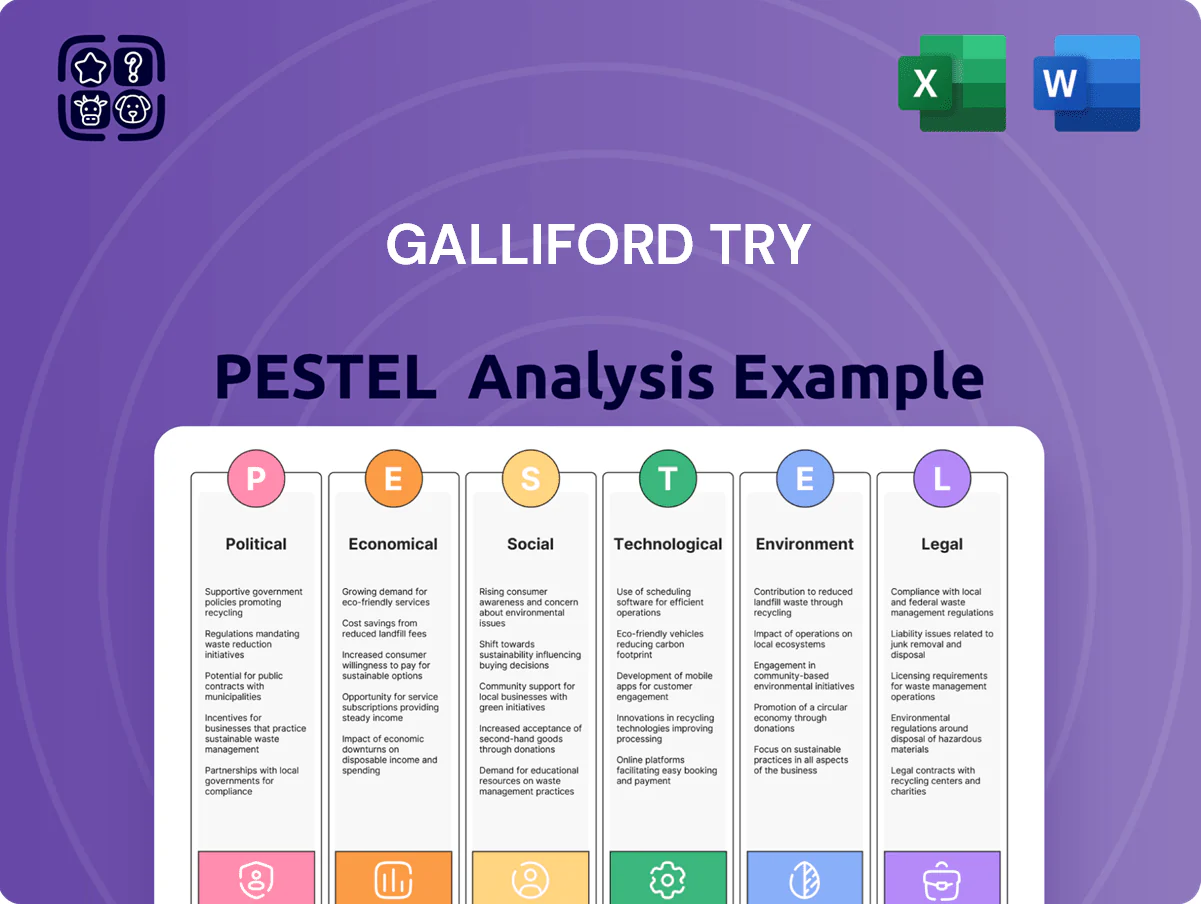

Political factors

Government Infrastructure Pipeline

The UK government remained Galliford Trys primary client in late 2025, with public-sector work representing over 60% of group revenue and a secured order book of c.£1.2bn; continued political support for multi-year programmes in water, highways and education underpins revenue resilience despite market volatility. However, ministerial reshuffles or revisions to the National Infrastructure Strategy could materially alter public contract volumes and timing, affecting near-term cashflow and margin visibility.

Regional Devolution Impact

The continued transfer of power to regional authorities and combined mayors shifts UK infrastructure allocation—local bodies now control an estimated 20–30% of regeneration budgets in key metro areas; Galliford Try must navigate varied political landscapes to win localized building and maintenance contracts. Decentralization demands targeted relationship-building with council leaders and metro mayors who oversee multi-billion pound programmes such as Greater Manchester’s £11bn pipeline and devolved transport funds.

Public Sector Procurement Reform

The UK government’s modernized procurement rules, effective end-2025, shift public contracts toward value-based scoring, altering Galliford Try’s bid strategy for projects worth over £5bn annually across infrastructure sectors.

Emphasis on social value and net-zero credentials rewards contractors with proven sustainability metrics; Galliford Try reported a 12% revenue uplift in 2024 from public-sector frameworks aligned to these criteria.

Compliance with evolving legislation and demonstrable ESG outcomes is essential to sustain win rates—public-sector contract success now correlates strongly with quantified social value scores and reduced carbon intensity.

Housing Policy and Planning Reform

Political pressure to solve the UK housing crisis—England requiring 300,000 homes p.a. target—drives planning reform that affects Galliford Try’s building division by accelerating approvals and altering project pipelines.

Galliford Try’s focus on public and regulated sectors benefits indirectly from mandates for 35% affordable housing on many schemes and urban densification policies that increase demand for mixed-use and retrofit projects.

Reforms to speed delivery, such as Planning White Paper rules and local plan updates, can shorten lead times between award and start, improving cashflow and reducing working capital needs for the group.

- England target ~300,000 homes/yr boosts demand

- Common 35% affordable housing quotas create mixed funding streams

- Faster planning reduces lead times, supporting cashflow

Geopolitical Trade Relations

Ongoing geopolitical tensions in late 2025 have pushed UK imported construction material costs up ~8–12% year-on-year, tightening availability for steel and timber and raising procurement risk for Galliford Try.

Trade decisions on tariffs and post-Brexit agreements directly affect supply-chain stability and project budgeting, with import-related inflation adding material cost pressure to margins.

Galliford Try must diversify suppliers, increase local sourcing, and embed flexible contract clauses (indexation, price caps) to mitigate sudden price shocks and preserve cash flow.

- Imported material costs +8–12% YoY (late 2025)

Public-led construction growth: £1.2bn order book, 300k homes, rising material costs

Public-sector work ~60% revenue; secured order book c.£1.2bn (late 2025). Devolution shifts 20–30% regeneration budgets to local bodies; Greater Manchester pipeline ~£11bn. England housing target ~300,000/yr; common 35% affordable quota. Imported material costs +8–12% YoY. New procurement rules (end-2025) favor value/social value/net-zero, Galliford Try saw 12% revenue uplift from aligned frameworks in 2024.

| Metric | Value |

|---|---|

| Public revenue share | ~60% |

| Order book | £1.2bn |

| Housing target | 300,000/yr |

| Imported costs YoY | +8–12% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Galliford Try across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples to identify strategic threats and opportunities for executives, investors, and consultants.

Condenses Galliford Try's full PESTLE into a neatly segmented, shareable summary that supports quick risk discussions, slide-ready copy, and editable notes for region- or division-specific planning.

Economic factors

Interest Rate Environment

The Bank of England held Bank Rate at 5.25% through late 2025, keeping borrowing costs elevated and raising Galliford Try’s weighted average cost of capital for new bids; despite a net cash position of £120m at H1 2025, sustained rates reduce private sponsors’ IRRs and slow large-scale commercial starts. Monitoring rate trajectory is critical: a 100bp move could materially cut private sector project volume and JV feasibility.

Construction Material Inflation

Although extreme volatility has eased, construction material inflation remains a priority at the end of 2025 as UK steel prices stayed about 8% above 2019 levels and UK concrete input costs rose roughly 6% year-on-year; Galliford Try uses fixed-price contracts and proactive procurement, including framework agreements and hedging, to limit margin erosion. Persistent inflationary pressures mean continuous cost-estimation updates and supply-chain monitoring to protect project profitability.

Labor Market Tightness

The UK construction sector faces a skilled labor shortfall, with CITB estimating a 200,000 worker gap by 2024, pushing average pay growth in construction to about 6.1% year-on-year in 2024; Galliford Try must increase wages yet protect margins, given 2024 operating margin pressures (net margin ~2–3% industry benchmark).

To secure talent Galliford Try is expanding direct hires and long-term subcontractor deals—strategies shown to reduce vacancy rates and stabilize labor costs—while balancing higher payroll spend against forecasted project throughput and tender margins.

Public Spending Constraints

Fiscal constraints on the UK Treasury in late 2025—net public sector borrowing projected at about £70bn for 2025/26—force stricter public project selection, favoring essential infrastructure over discretionary schemes.

Galliford Try prioritizes water and education projects, sectors historically shielded from cuts; the company derived roughly 35% of 2024 revenue from such public-sector contracts.

Galliford Try's financial outlook depends on continued government capital investment; reductions to the £600bn 10-year National Infrastructure Plan would materially risk future order books and cashflow.

- UK net borrowing ~£70bn (2025/26 forecast)

- Galliford Try ~35% revenue from essential public contracts (2024)

- National Infrastructure Plan ~£600bn over 10 years

Private Sector Investment Climate

Private developer confidence directly affects non-public contract volumes; UK construction output fell 3.1% in 2024 but showed a 0.8% m/m recovery in Q3 2025, indicating cautious pickup beneficial to Galliford Try's building pipeline.

As 2025 ends, demand for high-quality sustainable commercial space—ESG-backed assets commanding 5–10% rent premiums—drives project choices and margins for the building division.

UK GDP growth of 0.6% in 2024 and OBR forecasts of 1.2% in 2025 are critical to private investment levels that must supplement constrained public-sector spending.

- 2024 construction output -3.1%, Q3 2025 +0.8% m/m

- ESG rent premium 5–10% supporting sustainable builds

- UK GDP 2024 +0.6%, OBR 2025 forecast +1.2%

Higher rates, rising costs and skills shortfall squeeze UK construction returns

Elevated Bank Rate (5.25% late-2025) raises WACC and pressures private IRRs; material inflation (UK steel +8% vs 2019; concrete +6% y/y) and a 200k skilled-worker shortfall drive wage inflation (~6.1% 2024). Public borrowing ~£70bn (2025/26) shifts work to water/education (≈35% revenue 2024); UK GDP +0.6% (2024), OBR +1.2% (2025) still required to sustain private pipeline.

| Metric | Value |

|---|---|

| Bank Rate | 5.25% (late-2025) |

| Steel vs 2019 | +8% |

| Concrete y/y | +6% |

| Skilled gap | 200,000 (CITB) |

| Public borrowing | ~£70bn (2025/26) |

| Public revenue share | 35% (2024) |

| UK GDP | +0.6% (2024) |

Preview the Actual Deliverable

Galliford Try PESTLE Analysis

The preview shown here is the exact Galliford Try PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment review.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and environmental regulations are reshaping Galliford Try’s prospects—our concise PESTLE snapshot highlights key external risks and opportunities to inform smarter decisions; purchase the full analysis for the complete, editable report and actionable insights you can use immediately.

Political factors

Government Infrastructure Pipeline

The UK government remained Galliford Trys primary client in late 2025, with public-sector work representing over 60% of group revenue and a secured order book of c.£1.2bn; continued political support for multi-year programmes in water, highways and education underpins revenue resilience despite market volatility. However, ministerial reshuffles or revisions to the National Infrastructure Strategy could materially alter public contract volumes and timing, affecting near-term cashflow and margin visibility.

Regional Devolution Impact

The continued transfer of power to regional authorities and combined mayors shifts UK infrastructure allocation—local bodies now control an estimated 20–30% of regeneration budgets in key metro areas; Galliford Try must navigate varied political landscapes to win localized building and maintenance contracts. Decentralization demands targeted relationship-building with council leaders and metro mayors who oversee multi-billion pound programmes such as Greater Manchester’s £11bn pipeline and devolved transport funds.

Public Sector Procurement Reform

The UK government’s modernized procurement rules, effective end-2025, shift public contracts toward value-based scoring, altering Galliford Try’s bid strategy for projects worth over £5bn annually across infrastructure sectors.

Emphasis on social value and net-zero credentials rewards contractors with proven sustainability metrics; Galliford Try reported a 12% revenue uplift in 2024 from public-sector frameworks aligned to these criteria.

Compliance with evolving legislation and demonstrable ESG outcomes is essential to sustain win rates—public-sector contract success now correlates strongly with quantified social value scores and reduced carbon intensity.

Housing Policy and Planning Reform

Political pressure to solve the UK housing crisis—England requiring 300,000 homes p.a. target—drives planning reform that affects Galliford Try’s building division by accelerating approvals and altering project pipelines.

Galliford Try’s focus on public and regulated sectors benefits indirectly from mandates for 35% affordable housing on many schemes and urban densification policies that increase demand for mixed-use and retrofit projects.

Reforms to speed delivery, such as Planning White Paper rules and local plan updates, can shorten lead times between award and start, improving cashflow and reducing working capital needs for the group.

- England target ~300,000 homes/yr boosts demand

- Common 35% affordable housing quotas create mixed funding streams

- Faster planning reduces lead times, supporting cashflow

Geopolitical Trade Relations

Ongoing geopolitical tensions in late 2025 have pushed UK imported construction material costs up ~8–12% year-on-year, tightening availability for steel and timber and raising procurement risk for Galliford Try.

Trade decisions on tariffs and post-Brexit agreements directly affect supply-chain stability and project budgeting, with import-related inflation adding material cost pressure to margins.

Galliford Try must diversify suppliers, increase local sourcing, and embed flexible contract clauses (indexation, price caps) to mitigate sudden price shocks and preserve cash flow.

- Imported material costs +8–12% YoY (late 2025)

Public-led construction growth: £1.2bn order book, 300k homes, rising material costs

Public-sector work ~60% revenue; secured order book c.£1.2bn (late 2025). Devolution shifts 20–30% regeneration budgets to local bodies; Greater Manchester pipeline ~£11bn. England housing target ~300,000/yr; common 35% affordable quota. Imported material costs +8–12% YoY. New procurement rules (end-2025) favor value/social value/net-zero, Galliford Try saw 12% revenue uplift from aligned frameworks in 2024.

| Metric | Value |

|---|---|

| Public revenue share | ~60% |

| Order book | £1.2bn |

| Housing target | 300,000/yr |

| Imported costs YoY | +8–12% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Galliford Try across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples to identify strategic threats and opportunities for executives, investors, and consultants.

Condenses Galliford Try's full PESTLE into a neatly segmented, shareable summary that supports quick risk discussions, slide-ready copy, and editable notes for region- or division-specific planning.

Economic factors

Interest Rate Environment

The Bank of England held Bank Rate at 5.25% through late 2025, keeping borrowing costs elevated and raising Galliford Try’s weighted average cost of capital for new bids; despite a net cash position of £120m at H1 2025, sustained rates reduce private sponsors’ IRRs and slow large-scale commercial starts. Monitoring rate trajectory is critical: a 100bp move could materially cut private sector project volume and JV feasibility.

Construction Material Inflation

Although extreme volatility has eased, construction material inflation remains a priority at the end of 2025 as UK steel prices stayed about 8% above 2019 levels and UK concrete input costs rose roughly 6% year-on-year; Galliford Try uses fixed-price contracts and proactive procurement, including framework agreements and hedging, to limit margin erosion. Persistent inflationary pressures mean continuous cost-estimation updates and supply-chain monitoring to protect project profitability.

Labor Market Tightness

The UK construction sector faces a skilled labor shortfall, with CITB estimating a 200,000 worker gap by 2024, pushing average pay growth in construction to about 6.1% year-on-year in 2024; Galliford Try must increase wages yet protect margins, given 2024 operating margin pressures (net margin ~2–3% industry benchmark).

To secure talent Galliford Try is expanding direct hires and long-term subcontractor deals—strategies shown to reduce vacancy rates and stabilize labor costs—while balancing higher payroll spend against forecasted project throughput and tender margins.

Public Spending Constraints

Fiscal constraints on the UK Treasury in late 2025—net public sector borrowing projected at about £70bn for 2025/26—force stricter public project selection, favoring essential infrastructure over discretionary schemes.

Galliford Try prioritizes water and education projects, sectors historically shielded from cuts; the company derived roughly 35% of 2024 revenue from such public-sector contracts.

Galliford Try's financial outlook depends on continued government capital investment; reductions to the £600bn 10-year National Infrastructure Plan would materially risk future order books and cashflow.

- UK net borrowing ~£70bn (2025/26 forecast)

- Galliford Try ~35% revenue from essential public contracts (2024)

- National Infrastructure Plan ~£600bn over 10 years

Private Sector Investment Climate

Private developer confidence directly affects non-public contract volumes; UK construction output fell 3.1% in 2024 but showed a 0.8% m/m recovery in Q3 2025, indicating cautious pickup beneficial to Galliford Try's building pipeline.

As 2025 ends, demand for high-quality sustainable commercial space—ESG-backed assets commanding 5–10% rent premiums—drives project choices and margins for the building division.

UK GDP growth of 0.6% in 2024 and OBR forecasts of 1.2% in 2025 are critical to private investment levels that must supplement constrained public-sector spending.

- 2024 construction output -3.1%, Q3 2025 +0.8% m/m

- ESG rent premium 5–10% supporting sustainable builds

- UK GDP 2024 +0.6%, OBR 2025 forecast +1.2%

Higher rates, rising costs and skills shortfall squeeze UK construction returns

Elevated Bank Rate (5.25% late-2025) raises WACC and pressures private IRRs; material inflation (UK steel +8% vs 2019; concrete +6% y/y) and a 200k skilled-worker shortfall drive wage inflation (~6.1% 2024). Public borrowing ~£70bn (2025/26) shifts work to water/education (≈35% revenue 2024); UK GDP +0.6% (2024), OBR +1.2% (2025) still required to sustain private pipeline.

| Metric | Value |

|---|---|

| Bank Rate | 5.25% (late-2025) |

| Steel vs 2019 | +8% |

| Concrete y/y | +6% |

| Skilled gap | 200,000 (CITB) |

| Public borrowing | ~£70bn (2025/26) |

| Public revenue share | 35% (2024) |

| UK GDP | +0.6% (2024) |

Preview the Actual Deliverable

Galliford Try PESTLE Analysis

The preview shown here is the exact Galliford Try PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment review.