Garmin PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, economic trends, and rapid tech advances are reshaping Garmin’s market—our concise PESTLE snapshot highlights key risks and opportunities to inform smarter decisions; purchase the full analysis for detailed, actionable insights and editable charts ready for boardrooms and investor decks.

Political factors

Geopolitical Trade Relations and Tariffs

Global trade tensions, notably US-China relations, raised US tariffs on certain electronics to as high as 25% in recent years, increasing Garmin’s component costs and prompting higher logistics spend that contributed to supply-chain pressures seen industry-wide in 2023–2024.

With 2024 revenue outside the US comprising about 60% of Garmin’s roughly $5.8B sales, shifts in import duties force reassessments of production locations and nearshoring to protect margins.

Monitoring tariff policy and bilateral trade measures remains essential to preserve competitive pricing in consumer wearables and aviation avionics, where price sensitivity and regulatory certification cycles amplify cost pass-through risks.

Government Defense and Aviation Spending

A significant portion of Garmin’s revenue is tied to government-regulated sectors like aviation and marine navigation; in FY2024 Garmin reported approximately $1.7 billion in aviation and government-related sales, making defense and federal aviation funding material to demand for high-end flight decks and integrated cockpit systems. Changes in US defense budgets (FY2025 request $858 billion) or FAA funding shifts can directly affect procurement cycles, while political stability in the US and EU sustains multi-year institutional contracts.

Global Navigation Satellite System Sovereignty

Political decisions on the maintenance and security of GPS, GLONASS and Galileo directly impact Garmin’s device reliability; for example, 40% of consumer GPS chipset fixes rely on US GPS signals while EU funding for Galileo reached €9.3bn for 2021–2027, shaping network resilience. Rising national interests and export controls have prompted regional limits and the promotion of local systems—e.g., India’s NavIC expansion—forcing Garmin to adapt firmware and supply chains. Navigating these international dynamics is critical to ensure uninterrupted service across Garmin’s 18 million active users and $4.8bn FY2024 revenue base.

Export Control Regulations

Export controls on dual-use tech constrain Garmin’s international sales, with ITAR and EAR compliance essential for its avionics, maritime and tactical products; noncompliance risks fines—US penalties have reached up to $1.3m per violation in recent years—so legal controls add direct cost and delay to shipments.

Political shifts and sanctions (e.g., 2022–2024 US/EU measures) can close markets overnight, forcing Garmin to reroute $1.6bn+ in FY2024 global revenue streams through compliant channels and agile operational responses.

- Mandatory ITAR/EAR compliance raises legal/operational costs

- Penalties can exceed $1m per violation

- Sanctions 2022–2024 show rapid market closures

- FY2024 revenue exposure ~ $1.6bn requires agile routing

Stability in Manufacturing Hubs

Political stability in Southeast Asia, where Garmin sources components and assembles devices, underpins uninterrupted operations; ASEAN GDP grew 4.5% in 2024, supporting manufacturing resilience.

Civil unrest or abrupt policy shifts—e.g., 2023 tariff adjustments in key markets—could delay shipments, raising supply-chain costs and impacting Garmin’s FY2024 gross margin of 48.1%.

Garmin must quantify political risk in long-term site selection and capital allocation.

- Assess country risk scores, monitor tariffs/controls

Garmin margins hit by US‑China trade, export controls; ASEAN ops cushion but risks persist

Trade tensions, tariffs (US-China up to 25%), and export controls (ITAR/EAR) raised Garmin’s FY2024 component/logistics costs and compliance expenses, impacting margins on ~$5.8B revenue; ~60% sales outside US and ~$1.7B aviation/government exposure increase sensitivity to defense/Faa funding and sanctions. ASEAN manufacturing resilience (2024 GDP +4.5%) helps but political risk can disrupt supply chains and affect FY2024 gross margin 48.1%.

| Metric | Value |

|---|---|

| FY2024 Revenue | $5.8B |

| Non-US % | ~60% |

| Aviation/Govt Sales | $1.7B |

| FY2024 Gross Margin | 48.1% |

| US Defense FY2025 Request | $858B |

| ASEAN GDP 2024 | +4.5% |

What is included in the product

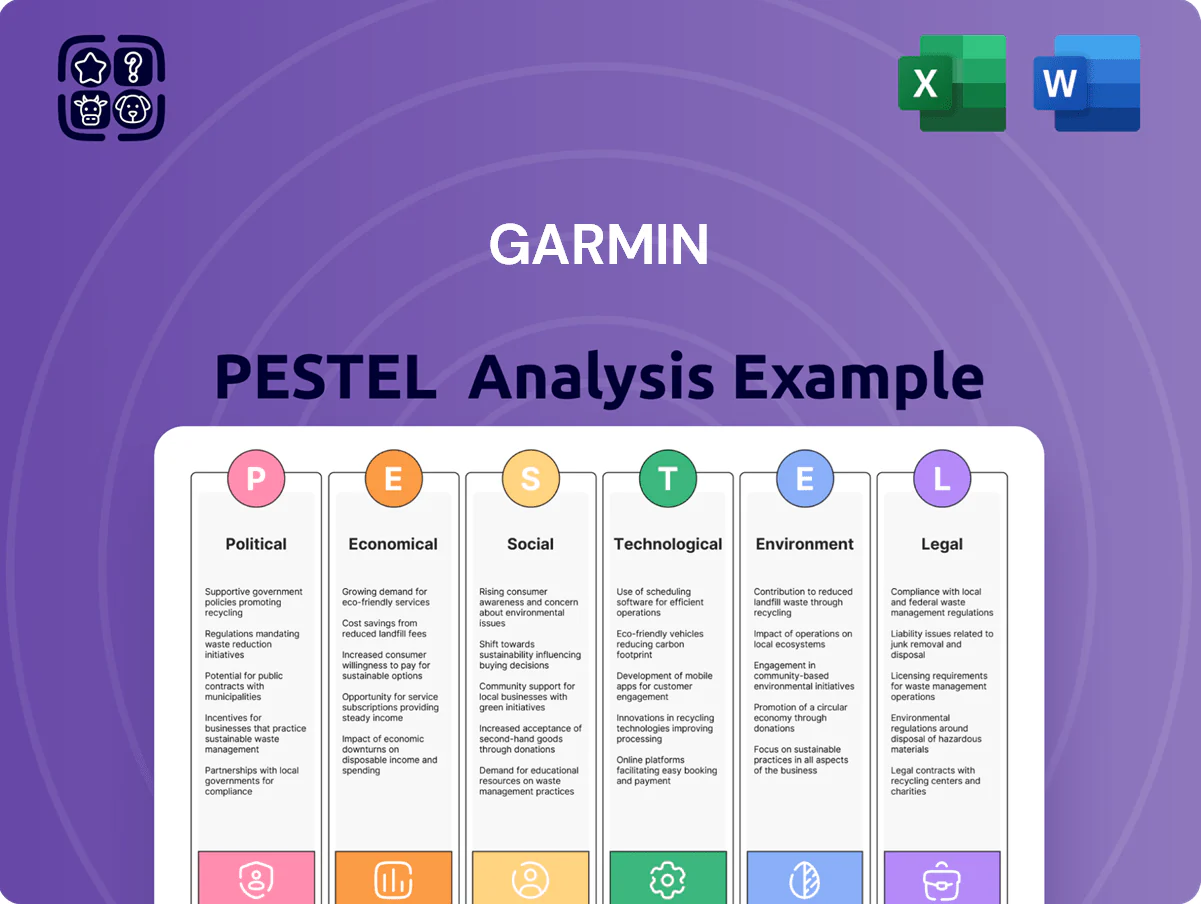

Explores how external macro-environmental factors uniquely affect Garmin across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Compact PESTLE snapshot tailored for Garmin that highlights regulatory, technological, and market risks to streamline strategic discussions and slide-ready summaries for quick team alignment.

Economic factors

Discretionary Consumer Spending Trends

Garmin’s fitness and outdoor segments depend on discretionary spending for premium smartwatches and GPS devices; US consumer spending on leisure goods fell 1.2% in 2024 amid 3.7% CPI inflation, pressuring demand for non-essential wearables. Economic downturns historically cut wearable sales—global smartwatch shipments dropped 4% in 2023—while US real GDP growth of 2.6% in 2024 supported a rebound in high-margin device sales. Rising disposable income in 2024 correlated with a 7% year-over-year increase in Garmin’s wearable revenue in Q4 2024.

Currency Exchange Rate Volatility

As a US Dollar-reporting multinational, Garmin faces FX risk across Europe, Asia and Latin America; a 10% USD appreciation vs. major currencies would have reduced FY2024 revenues by an estimated 2–3% based on geographic sales mix. Strengthening dollar raises retail prices abroad and compresses reported international earnings—Garmin noted FX headwinds of about $90–110m in 2024 adjusted operating results. Management uses forwards and options to hedge exposures, but ongoing volatility—EUR down ~6% and JPY down ~8% vs. USD in 2024—remains a material economic headwind.

Interest Rate Environments

Higher interest rates—with the US Fed funds target at 5.25–5.50% as of Dec 2025—raise borrowing costs for capital expenditures and can curb investment in aviation and marine sectors. For Garmin, this may slow commercial fleet upgrades and reduce demand for luxury marine vessels outfitted with its avionics and marine electronics. Garmin’s revenue exposure to aviation and marine (about 20% of FY2024 revenue) makes central bank policy monitoring vital for demand forecasting.

Supply Chain Inflation and Component Costs

The global inflation in 2024 raised prices for specialized semiconductors and PCB inputs by roughly 8–12% year-over-year, pressuring Garmin's hardware cost base and squeezing gross margins that were 49.6% in FY2023.

Volatility in rare earth metals and passive components—spot prices for neodymium rose ~15% in 2024—directly increases production costs and can erode Garmin's margins if not offset.

Garmin must drive internal cost efficiencies and may need modest consumer price increases; a 3–5% price pass-through could help preserve margins without harming demand.

- Semiconductor/PCB input inflation ~8–12% (2024)

- Neodymium spot +15% (2024)

- Gross margin FY2023 49.6%

- Suggested price pass-through 3–5%

Global Economic Growth Disparities

Variations in GDP growth—3.2% global forecast for 2025 by IMF, 1.4% in advanced economies vs 4.2% in emerging markets—shape Garmin’s regional expansion: mature markets drive steady replacement demand for wearables and marine electronics, while 4%+ growth in parts of APAC/Latin America fuels demand for automotive navigation and basic handheld devices.

Geographic revenue diversification (2024: North America ~62% of revenue, EMEA ~18%, APAC ~14%) stabilizes Garmin against local downturns and supports targeted investments where GDP growth outpaces developed markets.

- IMF 2025 global growth 3.2%

- Advanced economies 1.4%, emerging 4.2%

- Garmin FY2024 revenue split: NA ~62%, EMEA ~18%, APAC ~14%

Wearables grow 7% but FX & rising input costs shave margins, $90–110M headwind

Economic headwinds in 2024 (US CPI 3.7%) pressured discretionary wearable demand despite 2.6% US real GDP growth; FY2024 wearable revenue rose ~7% in Q4. USD strength (EUR -6%, JPY -8%) created ~$90–110m FY2024 FX headwind. Input costs rose: semiconductors/PCB +8–12%, neodymium +15%, pressuring margins (FY2023 gross margin 49.6%).

| Metric | 2024/2025 |

|---|---|

| US CPI | 3.7% |

| US real GDP | 2.6% |

| Wearable rev Q4 YoY | +7% |

| FX headwind | $90–110m |

| Semiconductor/PCB inflation | 8–12% |

| Neodymium | +15% |

| Gross margin FY2023 | 49.6% |

Preview Before You Purchase

Garmin PESTLE Analysis

The preview shown here is the exact Garmin PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment review.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political shifts, economic trends, and rapid tech advances are reshaping Garmin’s market—our concise PESTLE snapshot highlights key risks and opportunities to inform smarter decisions; purchase the full analysis for detailed, actionable insights and editable charts ready for boardrooms and investor decks.

Political factors

Geopolitical Trade Relations and Tariffs

Global trade tensions, notably US-China relations, raised US tariffs on certain electronics to as high as 25% in recent years, increasing Garmin’s component costs and prompting higher logistics spend that contributed to supply-chain pressures seen industry-wide in 2023–2024.

With 2024 revenue outside the US comprising about 60% of Garmin’s roughly $5.8B sales, shifts in import duties force reassessments of production locations and nearshoring to protect margins.

Monitoring tariff policy and bilateral trade measures remains essential to preserve competitive pricing in consumer wearables and aviation avionics, where price sensitivity and regulatory certification cycles amplify cost pass-through risks.

Government Defense and Aviation Spending

A significant portion of Garmin’s revenue is tied to government-regulated sectors like aviation and marine navigation; in FY2024 Garmin reported approximately $1.7 billion in aviation and government-related sales, making defense and federal aviation funding material to demand for high-end flight decks and integrated cockpit systems. Changes in US defense budgets (FY2025 request $858 billion) or FAA funding shifts can directly affect procurement cycles, while political stability in the US and EU sustains multi-year institutional contracts.

Global Navigation Satellite System Sovereignty

Political decisions on the maintenance and security of GPS, GLONASS and Galileo directly impact Garmin’s device reliability; for example, 40% of consumer GPS chipset fixes rely on US GPS signals while EU funding for Galileo reached €9.3bn for 2021–2027, shaping network resilience. Rising national interests and export controls have prompted regional limits and the promotion of local systems—e.g., India’s NavIC expansion—forcing Garmin to adapt firmware and supply chains. Navigating these international dynamics is critical to ensure uninterrupted service across Garmin’s 18 million active users and $4.8bn FY2024 revenue base.

Export Control Regulations

Export controls on dual-use tech constrain Garmin’s international sales, with ITAR and EAR compliance essential for its avionics, maritime and tactical products; noncompliance risks fines—US penalties have reached up to $1.3m per violation in recent years—so legal controls add direct cost and delay to shipments.

Political shifts and sanctions (e.g., 2022–2024 US/EU measures) can close markets overnight, forcing Garmin to reroute $1.6bn+ in FY2024 global revenue streams through compliant channels and agile operational responses.

- Mandatory ITAR/EAR compliance raises legal/operational costs

- Penalties can exceed $1m per violation

- Sanctions 2022–2024 show rapid market closures

- FY2024 revenue exposure ~ $1.6bn requires agile routing

Stability in Manufacturing Hubs

Political stability in Southeast Asia, where Garmin sources components and assembles devices, underpins uninterrupted operations; ASEAN GDP grew 4.5% in 2024, supporting manufacturing resilience.

Civil unrest or abrupt policy shifts—e.g., 2023 tariff adjustments in key markets—could delay shipments, raising supply-chain costs and impacting Garmin’s FY2024 gross margin of 48.1%.

Garmin must quantify political risk in long-term site selection and capital allocation.

- Assess country risk scores, monitor tariffs/controls

Garmin margins hit by US‑China trade, export controls; ASEAN ops cushion but risks persist

Trade tensions, tariffs (US-China up to 25%), and export controls (ITAR/EAR) raised Garmin’s FY2024 component/logistics costs and compliance expenses, impacting margins on ~$5.8B revenue; ~60% sales outside US and ~$1.7B aviation/government exposure increase sensitivity to defense/Faa funding and sanctions. ASEAN manufacturing resilience (2024 GDP +4.5%) helps but political risk can disrupt supply chains and affect FY2024 gross margin 48.1%.

| Metric | Value |

|---|---|

| FY2024 Revenue | $5.8B |

| Non-US % | ~60% |

| Aviation/Govt Sales | $1.7B |

| FY2024 Gross Margin | 48.1% |

| US Defense FY2025 Request | $858B |

| ASEAN GDP 2024 | +4.5% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Garmin across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Compact PESTLE snapshot tailored for Garmin that highlights regulatory, technological, and market risks to streamline strategic discussions and slide-ready summaries for quick team alignment.

Economic factors

Discretionary Consumer Spending Trends

Garmin’s fitness and outdoor segments depend on discretionary spending for premium smartwatches and GPS devices; US consumer spending on leisure goods fell 1.2% in 2024 amid 3.7% CPI inflation, pressuring demand for non-essential wearables. Economic downturns historically cut wearable sales—global smartwatch shipments dropped 4% in 2023—while US real GDP growth of 2.6% in 2024 supported a rebound in high-margin device sales. Rising disposable income in 2024 correlated with a 7% year-over-year increase in Garmin’s wearable revenue in Q4 2024.

Currency Exchange Rate Volatility

As a US Dollar-reporting multinational, Garmin faces FX risk across Europe, Asia and Latin America; a 10% USD appreciation vs. major currencies would have reduced FY2024 revenues by an estimated 2–3% based on geographic sales mix. Strengthening dollar raises retail prices abroad and compresses reported international earnings—Garmin noted FX headwinds of about $90–110m in 2024 adjusted operating results. Management uses forwards and options to hedge exposures, but ongoing volatility—EUR down ~6% and JPY down ~8% vs. USD in 2024—remains a material economic headwind.

Interest Rate Environments

Higher interest rates—with the US Fed funds target at 5.25–5.50% as of Dec 2025—raise borrowing costs for capital expenditures and can curb investment in aviation and marine sectors. For Garmin, this may slow commercial fleet upgrades and reduce demand for luxury marine vessels outfitted with its avionics and marine electronics. Garmin’s revenue exposure to aviation and marine (about 20% of FY2024 revenue) makes central bank policy monitoring vital for demand forecasting.

Supply Chain Inflation and Component Costs

The global inflation in 2024 raised prices for specialized semiconductors and PCB inputs by roughly 8–12% year-over-year, pressuring Garmin's hardware cost base and squeezing gross margins that were 49.6% in FY2023.

Volatility in rare earth metals and passive components—spot prices for neodymium rose ~15% in 2024—directly increases production costs and can erode Garmin's margins if not offset.

Garmin must drive internal cost efficiencies and may need modest consumer price increases; a 3–5% price pass-through could help preserve margins without harming demand.

- Semiconductor/PCB input inflation ~8–12% (2024)

- Neodymium spot +15% (2024)

- Gross margin FY2023 49.6%

- Suggested price pass-through 3–5%

Global Economic Growth Disparities

Variations in GDP growth—3.2% global forecast for 2025 by IMF, 1.4% in advanced economies vs 4.2% in emerging markets—shape Garmin’s regional expansion: mature markets drive steady replacement demand for wearables and marine electronics, while 4%+ growth in parts of APAC/Latin America fuels demand for automotive navigation and basic handheld devices.

Geographic revenue diversification (2024: North America ~62% of revenue, EMEA ~18%, APAC ~14%) stabilizes Garmin against local downturns and supports targeted investments where GDP growth outpaces developed markets.

- IMF 2025 global growth 3.2%

- Advanced economies 1.4%, emerging 4.2%

- Garmin FY2024 revenue split: NA ~62%, EMEA ~18%, APAC ~14%

Wearables grow 7% but FX & rising input costs shave margins, $90–110M headwind

Economic headwinds in 2024 (US CPI 3.7%) pressured discretionary wearable demand despite 2.6% US real GDP growth; FY2024 wearable revenue rose ~7% in Q4. USD strength (EUR -6%, JPY -8%) created ~$90–110m FY2024 FX headwind. Input costs rose: semiconductors/PCB +8–12%, neodymium +15%, pressuring margins (FY2023 gross margin 49.6%).

| Metric | 2024/2025 |

|---|---|

| US CPI | 3.7% |

| US real GDP | 2.6% |

| Wearable rev Q4 YoY | +7% |

| FX headwind | $90–110m |

| Semiconductor/PCB inflation | 8–12% |

| Neodymium | +15% |

| Gross margin FY2023 | 49.6% |

Preview Before You Purchase

Garmin PESTLE Analysis

The preview shown here is the exact Garmin PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment review.