Garrett Motion Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

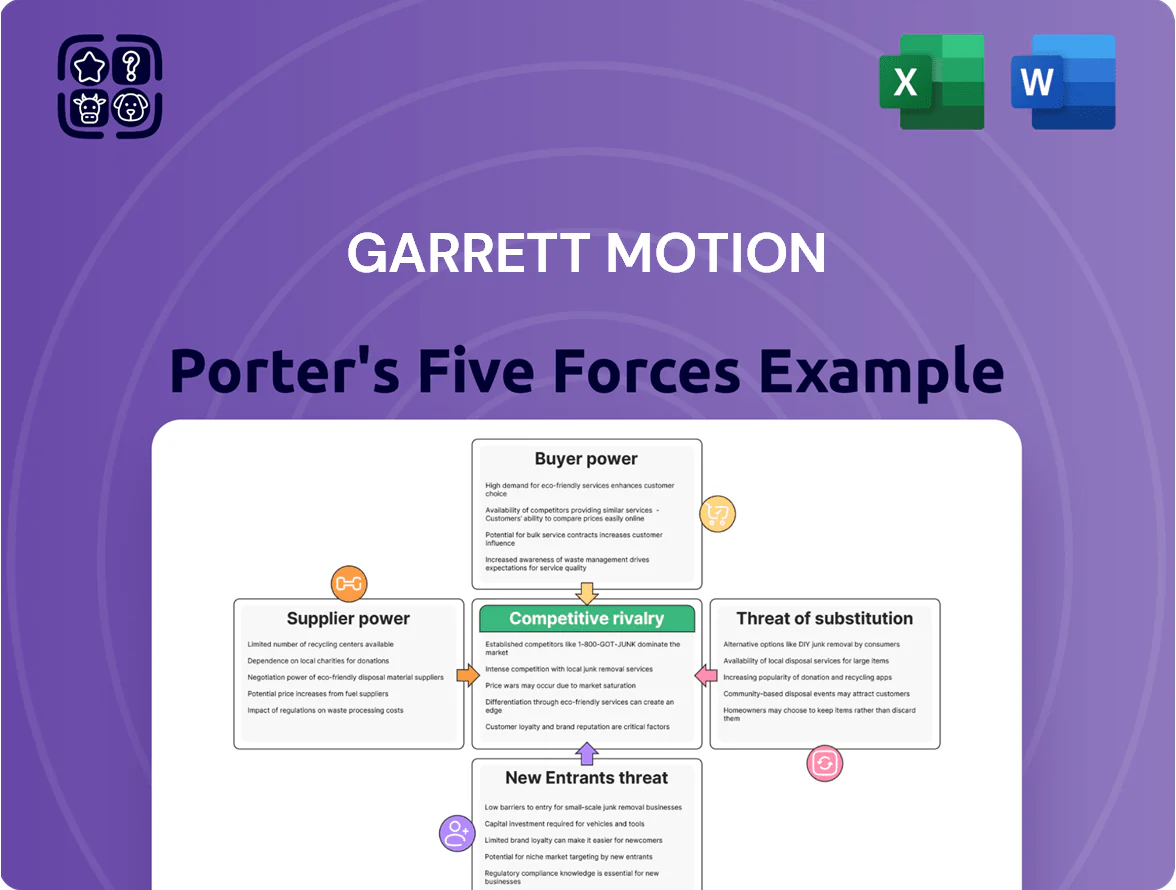

Garrett Motion faces moderate supplier power and high competitive rivalry as turbocharger tech advances and OEM consolidation intensify, while substitutes and new entrants pose variable threats depending on EV adoption timelines.

This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Garrett Motion’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material price volatility

Garrett Motion depends on high-temp alloys, aluminum, and nickel for turbochargers, and late 2025 commodity swings raised input costs about 12% year-on-year, pushing gross margins down; materials account for roughly 28% of COGS.

Semiconductor and electronics dependency

As Garrett shifts to e-boosting and software-enabled systems, its reliance on automotive-grade semiconductors rose; global chip shortages cut automotive output by 8% in 2021 and auto chip demand grew ~20% CAGR through 2024, concentrating power with a few foundries like TSMC and Infineon.

These specialized suppliers can dictate lead times and pricing; Garrett now signs multi-year supply agreements—reducing price leverage while securing priority, with semiconductor content per vehicle up to $600 in 2024 for electrified models.

Tier 2 and Tier 3 concentration

By 2025 consolidation left the automotive Tier 2–Tier 3 base concentrated: the top 10 regional casting/machining suppliers control an estimated 62% of capacity, so Garrett Motion frequently relies on a few vendors for specialized castings and machined parts.

Supplier distress is material: between 2019–2024 bankruptcies rose 28% in North American small parts makers, reducing Garrett’s switching options and raising lead-time risk.

Energy and logistics costs

Suppliers of energy‑intensive parts like turbine housings face high exposure to regional energy prices—Europe and North America saw industrial electricity prices averaging €0.12–0.18/kWh and $0.06–0.10/kWh in 2024—so suppliers pass costs via contractual surcharges to protect margins.

Those surcharge clauses mean Garrett Motion’s input costs track macro energy and logistics swings (2024 global container freight rates rose ~35% yoy at peaks), reducing Garrett’s pricing control and margin predictability.

- 2024 industrial electricity: Europe €0.12–0.18/kWh, North America $0.06–0.10/kWh

- Global container freight rates: +~35% peak 2024 yoy

- Supplier surcharge clauses commonly contracted

- Garrett input costs tied to external macro factors

Specialized technical expertise

Suppliers of complex sub-components for electric compressors and fuel-cell systems supply proprietary designs that Garrett Motion cannot easily copy, creating high technical switching costs—re-validation and testing can take 6–12+ months and cost an estimated $2–5 million per platform based on industry benchmarks in 2024.

That lengthy, costly lock-in gives suppliers strong leverage over pricing and contract terms; for Garrett, supplier concentration in select electro-mechanical parts meant top-three vendors supplied ~65% of such components in 2024, strengthening supplier bargaining power.

- 6–12+ months re-validation

- $2–5M estimated requalification cost

- Top-3 vendors ≈65% share (2024)

- High supplier-led pricing leverage

Supplier leverage surges: materials up 12%, chips $600/EV, top‑3 control 65%—high switch costs

Suppliers hold strong leverage: material costs (~28% of COGS) rose ~12% y/y in late‑2025, semiconductor content per electrified vehicle hit ~$600 in 2024, and top‑3 electro‑mechanical vendors supplied ~65% of that segment in 2024, making multi‑year contracts and surcharge clauses common and raising switching costs (revalidation 6–12+ months, $2–5M).

| Metric | Value |

|---|---|

| Materials % of COGS | ~28% |

| Late‑2025 material cost change | +~12% y/y |

| Semiconductor $/vehicle (2024) | $600 |

| Top‑3 vendor share (2024) | ~65% |

| Revalidation time | 6–12+ months |

| Requalification cost | $2–5M |

What is included in the product

Tailored Porter's Five Forces analysis for Garrett Motion that uncovers competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and strategic implications for its profitability and market positioning.

A concise Porter's Five Forces snapshot for Garrett Motion—ideal for quick strategic decisions and investor meetings.

Customers Bargaining Power

Concentration of global OEMs

Garrett Motion sells mainly to a handful of giant OEMs—Volkswagen, Ford, BMW—who account for over 40% of its 2024 OEM revenue, so buyers can demand large price cuts and extended payment terms.

These OEMs buy millions of units annually; a 1% price concession can cut Garrett’s gross margin by ~25 basis points based on 2024 margins.

By 2025 OEMs are consolidating platforms (e.g., VW’s unified platform, Ford’s EV architecture), increasing their purchasing leverage and raising supplier switching costs.

Transition to electric vehicle platforms

OEMs moving to BEV platforms cut ICE R&D budgets, forcing Garrett Motion to validate e-boosting and hybrid tech to stay in architectures; e-turbo adoption targets reached 2025–2027 will decide funding.

Buyers cite multi-year electrification roadmaps—EVs hit 14% global light-vehicle share in 2024—to push prices down on legacy turbochargers, squeezing Garrett’s ICE margins and volume forecasts.

Annual productivity price downs

In 2025 OEMs still demand annual productivity price downs—so-called give-backs—forcing Garrett Motion to cut prices roughly 1–3% yearly on core turbocharger contracts; suppliers report average cumulative margin erosion of about 5–10% over three years unless offset by internal cost savings. OEMs expect Garrett to realize efficiency gains and transfer them to customers, creating constant downward margin pressure that makes continuous product and process innovation mandatory to sustain 2024 EBITDA levels near 14%.

Stringent quality and emissions standards

Customers force Garrett to meet tougher global emissions and performance standards—EU CO2 targets tightened for 2030 (down 55% vs 1990) and China’s CAFC rules raise compliance costs—so OEMs reward technical leaders but also can impose steep penalties for defects.

Because recalls cost automakers an average $1,000–$5,000 per vehicle and Garrett supplies turbochargers to ~25% of global OEMs, buyers demand extensive warranties and indemnities, shifting liability and cash-flow risk onto suppliers.

- OEMs enforce strict compliance and penalties

- Recalls cost ~$1k–$5k/vehicle

- Garrett’s tech gives leverage but raises liability

- Buyers demand long warranties, indemnities

Open bidding and dual sourcing

OEMs use open bidding and dual sourcing on engine programs, often awarding contracts to two suppliers; in 2024 OEM dual-sourcing prevalence hit ~60% in turbocharger programs, forcing price competition.

By pitting Garrett against BorgWarner and IHI, customers squeezed bids—Garrett reported 2024 gross margin pressure with automotive margins down ~120 bps vs 2023—so Garrett must bid tightly and cut costs.

- Dual-sourcing ~60% of engine programs (2024)

Garrett under squeeze: OEM power, dual-sourcing & EVs drive ~120bps hit to 2024 EBITDA

Garrett faces high buyer power: top OEMs (VW, Ford, BMW) >40% 2024 OEM sales push 1–3% annual price give-backs, dual-sourcing ~60% of turbo programs (2024), and EV shift (14% global EV share in 2024) cuts ICE demand. Result: ~120 bps margin pressure in 2024, warranty/recall liability ~$1k–$5k/vehicle, forcing continuous cost, tech and e-boost validation to preserve ~14% 2024 EBITDA.

| Metric | 2024 |

|---|---|

| Top OEM share | 40%+ |

| Dual-sourcing | ~60% |

| EV light-vehicle share | 14% |

| Margin pressure | -120 bps |

Preview Before You Purchase

Garrett Motion Porter's Five Forces Analysis

This preview shows the exact Garrett Motion Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups, fully formatted and ready for use.

You're looking at the final, professionally written document; once you complete your purchase you'll get instant access to this same file for download and application.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Garrett Motion faces moderate supplier power and high competitive rivalry as turbocharger tech advances and OEM consolidation intensify, while substitutes and new entrants pose variable threats depending on EV adoption timelines.

This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Garrett Motion’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material price volatility

Garrett Motion depends on high-temp alloys, aluminum, and nickel for turbochargers, and late 2025 commodity swings raised input costs about 12% year-on-year, pushing gross margins down; materials account for roughly 28% of COGS.

Semiconductor and electronics dependency

As Garrett shifts to e-boosting and software-enabled systems, its reliance on automotive-grade semiconductors rose; global chip shortages cut automotive output by 8% in 2021 and auto chip demand grew ~20% CAGR through 2024, concentrating power with a few foundries like TSMC and Infineon.

These specialized suppliers can dictate lead times and pricing; Garrett now signs multi-year supply agreements—reducing price leverage while securing priority, with semiconductor content per vehicle up to $600 in 2024 for electrified models.

Tier 2 and Tier 3 concentration

By 2025 consolidation left the automotive Tier 2–Tier 3 base concentrated: the top 10 regional casting/machining suppliers control an estimated 62% of capacity, so Garrett Motion frequently relies on a few vendors for specialized castings and machined parts.

Supplier distress is material: between 2019–2024 bankruptcies rose 28% in North American small parts makers, reducing Garrett’s switching options and raising lead-time risk.

Energy and logistics costs

Suppliers of energy‑intensive parts like turbine housings face high exposure to regional energy prices—Europe and North America saw industrial electricity prices averaging €0.12–0.18/kWh and $0.06–0.10/kWh in 2024—so suppliers pass costs via contractual surcharges to protect margins.

Those surcharge clauses mean Garrett Motion’s input costs track macro energy and logistics swings (2024 global container freight rates rose ~35% yoy at peaks), reducing Garrett’s pricing control and margin predictability.

- 2024 industrial electricity: Europe €0.12–0.18/kWh, North America $0.06–0.10/kWh

- Global container freight rates: +~35% peak 2024 yoy

- Supplier surcharge clauses commonly contracted

- Garrett input costs tied to external macro factors

Specialized technical expertise

Suppliers of complex sub-components for electric compressors and fuel-cell systems supply proprietary designs that Garrett Motion cannot easily copy, creating high technical switching costs—re-validation and testing can take 6–12+ months and cost an estimated $2–5 million per platform based on industry benchmarks in 2024.

That lengthy, costly lock-in gives suppliers strong leverage over pricing and contract terms; for Garrett, supplier concentration in select electro-mechanical parts meant top-three vendors supplied ~65% of such components in 2024, strengthening supplier bargaining power.

- 6–12+ months re-validation

- $2–5M estimated requalification cost

- Top-3 vendors ≈65% share (2024)

- High supplier-led pricing leverage

Supplier leverage surges: materials up 12%, chips $600/EV, top‑3 control 65%—high switch costs

Suppliers hold strong leverage: material costs (~28% of COGS) rose ~12% y/y in late‑2025, semiconductor content per electrified vehicle hit ~$600 in 2024, and top‑3 electro‑mechanical vendors supplied ~65% of that segment in 2024, making multi‑year contracts and surcharge clauses common and raising switching costs (revalidation 6–12+ months, $2–5M).

| Metric | Value |

|---|---|

| Materials % of COGS | ~28% |

| Late‑2025 material cost change | +~12% y/y |

| Semiconductor $/vehicle (2024) | $600 |

| Top‑3 vendor share (2024) | ~65% |

| Revalidation time | 6–12+ months |

| Requalification cost | $2–5M |

What is included in the product

Tailored Porter's Five Forces analysis for Garrett Motion that uncovers competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and strategic implications for its profitability and market positioning.

A concise Porter's Five Forces snapshot for Garrett Motion—ideal for quick strategic decisions and investor meetings.

Customers Bargaining Power

Concentration of global OEMs

Garrett Motion sells mainly to a handful of giant OEMs—Volkswagen, Ford, BMW—who account for over 40% of its 2024 OEM revenue, so buyers can demand large price cuts and extended payment terms.

These OEMs buy millions of units annually; a 1% price concession can cut Garrett’s gross margin by ~25 basis points based on 2024 margins.

By 2025 OEMs are consolidating platforms (e.g., VW’s unified platform, Ford’s EV architecture), increasing their purchasing leverage and raising supplier switching costs.

Transition to electric vehicle platforms

OEMs moving to BEV platforms cut ICE R&D budgets, forcing Garrett Motion to validate e-boosting and hybrid tech to stay in architectures; e-turbo adoption targets reached 2025–2027 will decide funding.

Buyers cite multi-year electrification roadmaps—EVs hit 14% global light-vehicle share in 2024—to push prices down on legacy turbochargers, squeezing Garrett’s ICE margins and volume forecasts.

Annual productivity price downs

In 2025 OEMs still demand annual productivity price downs—so-called give-backs—forcing Garrett Motion to cut prices roughly 1–3% yearly on core turbocharger contracts; suppliers report average cumulative margin erosion of about 5–10% over three years unless offset by internal cost savings. OEMs expect Garrett to realize efficiency gains and transfer them to customers, creating constant downward margin pressure that makes continuous product and process innovation mandatory to sustain 2024 EBITDA levels near 14%.

Stringent quality and emissions standards

Customers force Garrett to meet tougher global emissions and performance standards—EU CO2 targets tightened for 2030 (down 55% vs 1990) and China’s CAFC rules raise compliance costs—so OEMs reward technical leaders but also can impose steep penalties for defects.

Because recalls cost automakers an average $1,000–$5,000 per vehicle and Garrett supplies turbochargers to ~25% of global OEMs, buyers demand extensive warranties and indemnities, shifting liability and cash-flow risk onto suppliers.

- OEMs enforce strict compliance and penalties

- Recalls cost ~$1k–$5k/vehicle

- Garrett’s tech gives leverage but raises liability

- Buyers demand long warranties, indemnities

Open bidding and dual sourcing

OEMs use open bidding and dual sourcing on engine programs, often awarding contracts to two suppliers; in 2024 OEM dual-sourcing prevalence hit ~60% in turbocharger programs, forcing price competition.

By pitting Garrett against BorgWarner and IHI, customers squeezed bids—Garrett reported 2024 gross margin pressure with automotive margins down ~120 bps vs 2023—so Garrett must bid tightly and cut costs.

- Dual-sourcing ~60% of engine programs (2024)

Garrett under squeeze: OEM power, dual-sourcing & EVs drive ~120bps hit to 2024 EBITDA

Garrett faces high buyer power: top OEMs (VW, Ford, BMW) >40% 2024 OEM sales push 1–3% annual price give-backs, dual-sourcing ~60% of turbo programs (2024), and EV shift (14% global EV share in 2024) cuts ICE demand. Result: ~120 bps margin pressure in 2024, warranty/recall liability ~$1k–$5k/vehicle, forcing continuous cost, tech and e-boost validation to preserve ~14% 2024 EBITDA.

| Metric | 2024 |

|---|---|

| Top OEM share | 40%+ |

| Dual-sourcing | ~60% |

| EV light-vehicle share | 14% |

| Margin pressure | -120 bps |

Preview Before You Purchase

Garrett Motion Porter's Five Forces Analysis

This preview shows the exact Garrett Motion Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups, fully formatted and ready for use.

You're looking at the final, professionally written document; once you complete your purchase you'll get instant access to this same file for download and application.