Gartner Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Gartner’s Porter’s Five Forces snapshot highlights competitive intensity, buyer and supplier leverage, entry barriers, and substitute risks—essential context for strategic decisions and investment theses.

This brief overview only scratches the surface; unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable insights tailored to Gartner’s market dynamics.

Suppliers Bargaining Power

High Dependency on Specialized Human Capital

Gartner depends on specialized analysts and consultants who supply proprietary research; they’re the main input.

By late 2025 demand for AI and data-science talent rose ~18% year-over-year, boosting wage premiums and bargaining power.

Retention now requires top compensation and advanced tools—human-capital costs account for an estimated 40–55% of research expense.

Reliance on Advanced Technology Infrastructure

Gartner depends on cloud providers and software vendors to host its data and client platforms; by end-2025, embedding generative AI increased reliance on specialized infrastructure (GPU clusters, MLOps) raising switching costs to an estimated $50–120m for enterprise-scale migrations.

Data Acquisition from Third-Party Sources

Gartner buys secondary data from specialist vendors for raw metrics that validate its frameworks; in 2024 Gartner reported $5.9bn revenue, showing reliance on data-driven services.

Supplier power is limited: Gartner can switch among multiple providers or gather data via its 15,000+ client executive interactions and 300+ research practices.

This redundancy keeps supplier price leverage low; Gartner’s procurement likely represents a small single-digit percent of revenue, capping bargaining power.

Geographic Concentration of Expert Labor

The supply of high-level strategic advisors remains concentrated in hubs like New York, London, and San Francisco, creating localized recruitment pressure and higher pay premiums—market data shows consultant salaries in these hubs were 15–25% above national averages in 2024.

Hybrid work in 2025 eased geographic constraints, expanding Gartner’s candidate pool and reducing relocation costs by an estimated 10–12%, but sourcing experts who match Gartner’s methodologies and sector depth remains scarce.

That scarcity keeps supplier power elevated for niche roles, pushing Gartner to invest more in training and retention to avoid a 5–8% annual attrition hit among senior advisors.

- Concentration in major hubs: NY, London, SF — +15–25% pay premium

- Hybrid work 2025: broadens pool, cuts relocation costs ~10–12%

- Scarcity of Gartner-method-skilled experts: sustains higher supplier power

- Retention investment to avoid 5–8% senior attrition

Evolution of AI Training Data Rights

As Gartner shifts to LLM-driven research synthesis, suppliers of training data and model licenses became strategic chokepoints by 2025—data licensors now command higher fees and stricter use terms, raising model access costs by an estimated 12–18% for enterprises in 2024–25.

Stronger copyright rules (e.g., EU AI Act drafting, US cases clarifying training use) increased supplier leverage, making negotiation of IP training rights a core procurement task for Gartner and peers.

- Data/license fees up 12–18% (2024–25)

- IP negotiation now central to AI supply chain

- Regulatory tightening raises supplier leverage

- Suppliers form new licensing tiers and audit rights

Gartner suppliers: niche inputs push costs up, but scale keeps bargaining power moderate

Suppliers of Gartner’s core inputs—senior analysts, AI training data, cloud/GPU infrastructure, and specialist secondary datasets—wield mixed power: niche talent and data licensors push premiums (analyst wages +18% y/y; data/license fees +12–18% in 2024–25), while Gartner’s client-engagement scale (15,000+ exec interactions; 300+ practices) and multi-vendor options cap leverage, keeping overall supplier bargaining power moderate.

| Input | 2024–25 metric | Impact on bargaining power |

|---|---|---|

| Senior analysts | Wages +18% y/y; 5–8% senior attrition risk | High for niche roles |

| AI/data licenses | Fees +12–18% | Elevated; contract/legal leverage |

| Cloud/GPU infra | Switch cost $50–120m (enterprise) | Raises switching costs |

| Secondary data | Small % of revenue; replaceable | Low |

What is included in the product

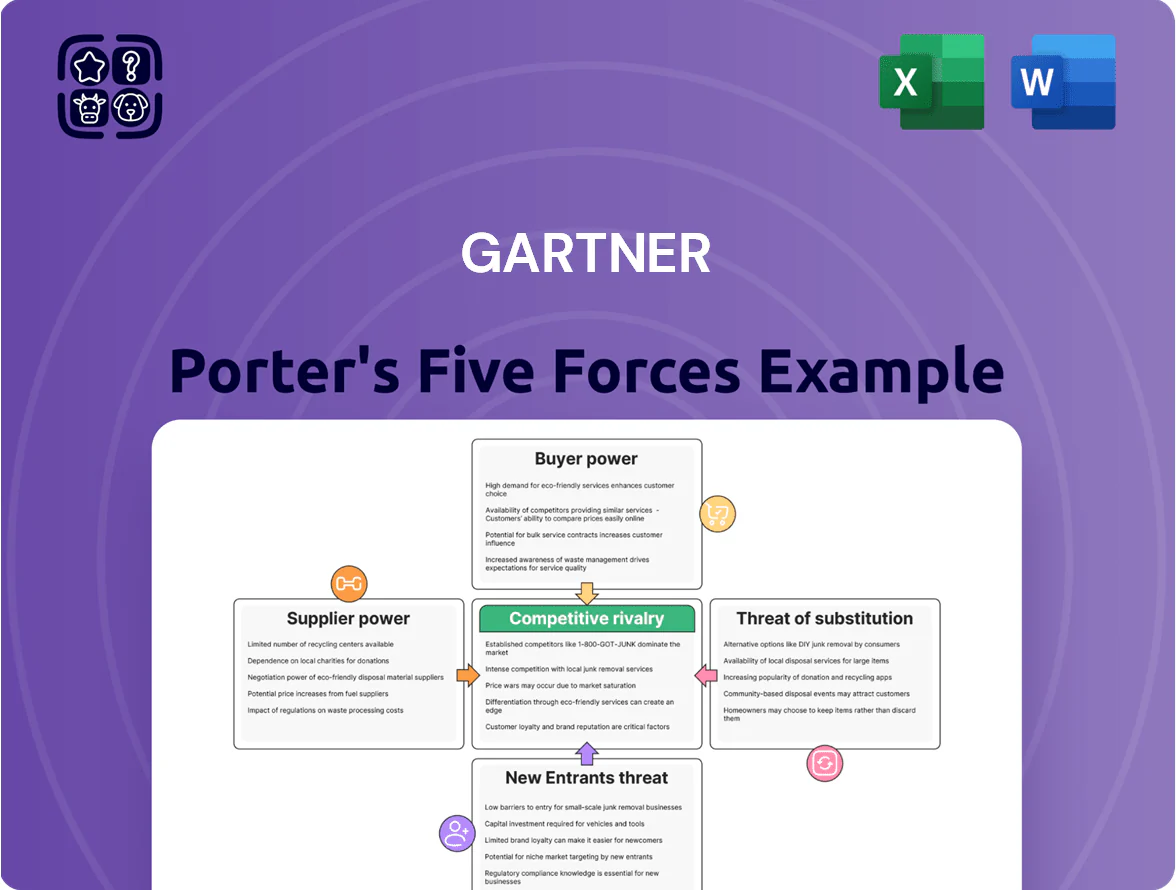

Concise Porter's Five Forces analysis tailored for Gartner, identifying competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and highlighting disruptive forces and strategic levers to protect market share and profitability.

A concise Porter's Five Forces one-pager that clarifies competitive pressures at a glance—ideal for faster strategic decisions and boardroom alignment.

Customers Bargaining Power

High Concentration of Global Enterprise Clients

Gartner serves roughly 70% of the Fortune 500, and these high-value enterprise clients hold strong negotiating leverage; in 2024 Gartner reported 75% of revenue from subscription and advisory contracts, many multi-year and multi-user, so losing a few clients would hit recurring revenue hard. Large buyers commonly demand customized SLAs, dedicated analyst access, and preferential pricing, pushing Gartner toward tailored deals and higher account management costs.

Availability of Alternative Research Providers

While Gartner remains a market leader, buyers can pick peers like Forrester Research, IDC, and ~1,200 boutique firms; by end-2025 over 350 niche providers specialized in sustainability or AI research expanded offerings, giving clients more choice. With enterprise research spend of ~$6.5B annually across major buyers, customers can shift budgets if Gartner fails to show superior ROI—contract churn rates rise when vendor ROI falls below 12% annual target.

Transparency and Information Symmetry

Modern procurement teams use benchmarking tools and vendor scorecards; 72% of enterprise buyers (Gartner 2024 client survey) compare advisory ROI before purchase, shrinking information asymmetry.

By 2025 clients run AI models to back-test Gartner forecasts—one buy-side firm reported a 15% reduction in advisory spend after AI validation—raising demand for demonstrable accuracy.

This transparency forces Gartner to keep forecast hit rates high; Gartner reported a 68% accuracy rate on major tech trend calls in 2024, critical to justify premium fees.

Switching Costs and Integration into Decision-Making

The bargaining power of customers is reduced by high switching costs: Gartner estimates clients spend $200k–$2m annually on integrating Magic Quadrant and Hype Cycle outputs into procurement and strategy, and 62% of surveyed enterprises (2024 Gartner client study) say replacing these frameworks requires 6–12+ months retraining and process changes.

- Embedded frameworks: Magic Quadrant/Hype Cycle used in RFPs

- Costed integration: $200k–$2m per year

- Retraining time: 6–12+ months (62% of firms)

- Deterrent effect: raises churn friction and reduces buyer leverage

Demand for Specialized and Actionable Insights

Customers in 2025 favor hyper-specific, actionable advice over generic reports, letting buyers push for bespoke consulting hours bundled into subscriptions; Gartner faces pressure as 62% of enterprise clients now rate personalization as a top renewal driver (Gartner client survey, 2025).

This elevates customer bargaining power: firms can demand tailored executive guidance, forcing Gartner to trade off subscription scalability for margin-heavy, low-volume consulting.

- 62% of enterprises prioritize personalization (2025)

- Bespoke consulting raises delivery costs ~15–25% per client

- Scalability hit if >20% of base requests require human hours

High buyer power: 75% subscription, 70% Fortune 500 — personalization spikes costs

Customers hold high bargaining power: 70% Fortune 500 coverage, 75% subscription revenue (2024), but large buyers can switch to Forrester/IDC/350+ niche firms; contract churn rises if ROI <12%. Switching costs remain high ($200k–$2m/year integration; 6–12+ months retrain). 62% of clients (2025) demand personalization, raising delivery costs 15–25%.

| Metric | Value |

|---|---|

| Fortune 500 coverage | ~70% |

| Subscription revenue | 75% (2024) |

| Integration cost | $200k–$2m/yr |

| Retrain time | 6–12+ months (62%) |

| Personalization demand | 62% (2025) |

Preview the Actual Deliverable

Gartner Porter's Five Forces Analysis

This preview shows the exact Gartner Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for use with no placeholders or samples.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Gartner’s Porter’s Five Forces snapshot highlights competitive intensity, buyer and supplier leverage, entry barriers, and substitute risks—essential context for strategic decisions and investment theses.

This brief overview only scratches the surface; unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable insights tailored to Gartner’s market dynamics.

Suppliers Bargaining Power

High Dependency on Specialized Human Capital

Gartner depends on specialized analysts and consultants who supply proprietary research; they’re the main input.

By late 2025 demand for AI and data-science talent rose ~18% year-over-year, boosting wage premiums and bargaining power.

Retention now requires top compensation and advanced tools—human-capital costs account for an estimated 40–55% of research expense.

Reliance on Advanced Technology Infrastructure

Gartner depends on cloud providers and software vendors to host its data and client platforms; by end-2025, embedding generative AI increased reliance on specialized infrastructure (GPU clusters, MLOps) raising switching costs to an estimated $50–120m for enterprise-scale migrations.

Data Acquisition from Third-Party Sources

Gartner buys secondary data from specialist vendors for raw metrics that validate its frameworks; in 2024 Gartner reported $5.9bn revenue, showing reliance on data-driven services.

Supplier power is limited: Gartner can switch among multiple providers or gather data via its 15,000+ client executive interactions and 300+ research practices.

This redundancy keeps supplier price leverage low; Gartner’s procurement likely represents a small single-digit percent of revenue, capping bargaining power.

Geographic Concentration of Expert Labor

The supply of high-level strategic advisors remains concentrated in hubs like New York, London, and San Francisco, creating localized recruitment pressure and higher pay premiums—market data shows consultant salaries in these hubs were 15–25% above national averages in 2024.

Hybrid work in 2025 eased geographic constraints, expanding Gartner’s candidate pool and reducing relocation costs by an estimated 10–12%, but sourcing experts who match Gartner’s methodologies and sector depth remains scarce.

That scarcity keeps supplier power elevated for niche roles, pushing Gartner to invest more in training and retention to avoid a 5–8% annual attrition hit among senior advisors.

- Concentration in major hubs: NY, London, SF — +15–25% pay premium

- Hybrid work 2025: broadens pool, cuts relocation costs ~10–12%

- Scarcity of Gartner-method-skilled experts: sustains higher supplier power

- Retention investment to avoid 5–8% senior attrition

Evolution of AI Training Data Rights

As Gartner shifts to LLM-driven research synthesis, suppliers of training data and model licenses became strategic chokepoints by 2025—data licensors now command higher fees and stricter use terms, raising model access costs by an estimated 12–18% for enterprises in 2024–25.

Stronger copyright rules (e.g., EU AI Act drafting, US cases clarifying training use) increased supplier leverage, making negotiation of IP training rights a core procurement task for Gartner and peers.

- Data/license fees up 12–18% (2024–25)

- IP negotiation now central to AI supply chain

- Regulatory tightening raises supplier leverage

- Suppliers form new licensing tiers and audit rights

Gartner suppliers: niche inputs push costs up, but scale keeps bargaining power moderate

Suppliers of Gartner’s core inputs—senior analysts, AI training data, cloud/GPU infrastructure, and specialist secondary datasets—wield mixed power: niche talent and data licensors push premiums (analyst wages +18% y/y; data/license fees +12–18% in 2024–25), while Gartner’s client-engagement scale (15,000+ exec interactions; 300+ practices) and multi-vendor options cap leverage, keeping overall supplier bargaining power moderate.

| Input | 2024–25 metric | Impact on bargaining power |

|---|---|---|

| Senior analysts | Wages +18% y/y; 5–8% senior attrition risk | High for niche roles |

| AI/data licenses | Fees +12–18% | Elevated; contract/legal leverage |

| Cloud/GPU infra | Switch cost $50–120m (enterprise) | Raises switching costs |

| Secondary data | Small % of revenue; replaceable | Low |

What is included in the product

Concise Porter's Five Forces analysis tailored for Gartner, identifying competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and highlighting disruptive forces and strategic levers to protect market share and profitability.

A concise Porter's Five Forces one-pager that clarifies competitive pressures at a glance—ideal for faster strategic decisions and boardroom alignment.

Customers Bargaining Power

High Concentration of Global Enterprise Clients

Gartner serves roughly 70% of the Fortune 500, and these high-value enterprise clients hold strong negotiating leverage; in 2024 Gartner reported 75% of revenue from subscription and advisory contracts, many multi-year and multi-user, so losing a few clients would hit recurring revenue hard. Large buyers commonly demand customized SLAs, dedicated analyst access, and preferential pricing, pushing Gartner toward tailored deals and higher account management costs.

Availability of Alternative Research Providers

While Gartner remains a market leader, buyers can pick peers like Forrester Research, IDC, and ~1,200 boutique firms; by end-2025 over 350 niche providers specialized in sustainability or AI research expanded offerings, giving clients more choice. With enterprise research spend of ~$6.5B annually across major buyers, customers can shift budgets if Gartner fails to show superior ROI—contract churn rates rise when vendor ROI falls below 12% annual target.

Transparency and Information Symmetry

Modern procurement teams use benchmarking tools and vendor scorecards; 72% of enterprise buyers (Gartner 2024 client survey) compare advisory ROI before purchase, shrinking information asymmetry.

By 2025 clients run AI models to back-test Gartner forecasts—one buy-side firm reported a 15% reduction in advisory spend after AI validation—raising demand for demonstrable accuracy.

This transparency forces Gartner to keep forecast hit rates high; Gartner reported a 68% accuracy rate on major tech trend calls in 2024, critical to justify premium fees.

Switching Costs and Integration into Decision-Making

The bargaining power of customers is reduced by high switching costs: Gartner estimates clients spend $200k–$2m annually on integrating Magic Quadrant and Hype Cycle outputs into procurement and strategy, and 62% of surveyed enterprises (2024 Gartner client study) say replacing these frameworks requires 6–12+ months retraining and process changes.

- Embedded frameworks: Magic Quadrant/Hype Cycle used in RFPs

- Costed integration: $200k–$2m per year

- Retraining time: 6–12+ months (62% of firms)

- Deterrent effect: raises churn friction and reduces buyer leverage

Demand for Specialized and Actionable Insights

Customers in 2025 favor hyper-specific, actionable advice over generic reports, letting buyers push for bespoke consulting hours bundled into subscriptions; Gartner faces pressure as 62% of enterprise clients now rate personalization as a top renewal driver (Gartner client survey, 2025).

This elevates customer bargaining power: firms can demand tailored executive guidance, forcing Gartner to trade off subscription scalability for margin-heavy, low-volume consulting.

- 62% of enterprises prioritize personalization (2025)

- Bespoke consulting raises delivery costs ~15–25% per client

- Scalability hit if >20% of base requests require human hours

High buyer power: 75% subscription, 70% Fortune 500 — personalization spikes costs

Customers hold high bargaining power: 70% Fortune 500 coverage, 75% subscription revenue (2024), but large buyers can switch to Forrester/IDC/350+ niche firms; contract churn rises if ROI <12%. Switching costs remain high ($200k–$2m/year integration; 6–12+ months retrain). 62% of clients (2025) demand personalization, raising delivery costs 15–25%.

| Metric | Value |

|---|---|

| Fortune 500 coverage | ~70% |

| Subscription revenue | 75% (2024) |

| Integration cost | $200k–$2m/yr |

| Retrain time | 6–12+ months (62%) |

| Personalization demand | 62% (2025) |

Preview the Actual Deliverable

Gartner Porter's Five Forces Analysis

This preview shows the exact Gartner Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for use with no placeholders or samples.