Gartner PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

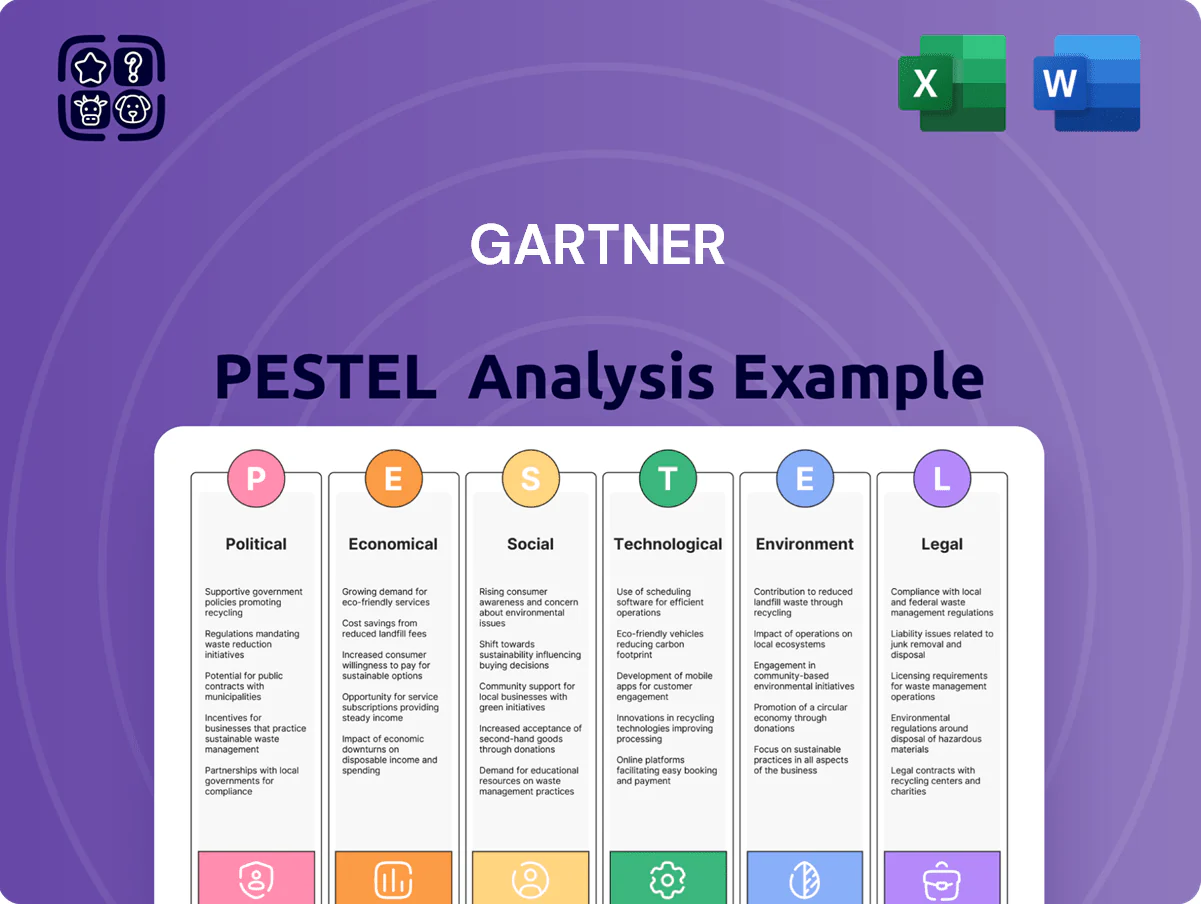

Our Gartner PESTLE Analysis reveals the key political, economic, social, technological, legal, and environmental forces shaping its strategy and market position—perfect for investors and strategists who need concise, actionable intelligence; purchase the full, editable report to access deep-dive insights, data-driven implications, and ready-to-use slides for immediate decision-making.

Political factors

Geopolitical instability and trade relations

The ongoing geopolitical tensions between the US, China, Russia and EU in late 2025 continue to disrupt supply chains, with 48% of global firms reporting increased sourcing shifts and 22% citing higher tech investment relocations; Gartner must guide clients on diversification as tariffs and export controls raise operational costs and capex risk.

Government digitization initiatives

Public sector organizations are prioritizing digital transformation, with global government IT spending projected at $1.6 trillion in 2025, driving demand for service modernization and efficiency gains.

Gartner captures this demand by delivering specialized research and consulting to agencies modernizing legacy systems, contributing to its government services revenue, which represented about 12–15% of client consulting engagements in 2024.

National policies on digital sovereignty and investments in public tech infrastructure—EU Digital Decade targets and US federal modernization funds exceeding $100 billion since 2021—create a steady advisory pipeline for Gartner.

Data sovereignty and localization laws

Governments are tightening data sovereignty rules—over 80 countries had data localization laws by 2024, impacting cross-border processing and cloud deployments.

Gartner aids multinationals by mapping these mandates; in 2024 its regulatory research served 15,000+ enterprise clients navigating compliance and vendor selection.

Providing localized legal insights across 120+ jurisdictions is a key differentiator for Gartner amid a fragmented political landscape, reducing compliance risks and potential fines.

Election cycles and policy shifts

Major elections in 2024–2025 in the US, UK, India and EU members prompted shifts in corporate tax proposals and tighter tech regulation, with 2024 US corporate tax debate affecting forecasts for 2025 M&A and capex (estimated 4–6% impact on effective tax rates in scenarios Gartner models).

Gartner tracks transitions to advise clients on policy volatility and likely regulatory oversight increases in data/privacy and AI, incorporating scenario probabilities and stress-testing revenue and compliance cost impacts.

Political stability is flagged as key for long-term planning: Gartner’s client risk dashboards weight stability metrics and show firms in unstable jurisdictions face 10–20% higher contingency reserves on average.

- Key markets: US, UK, EU, India — elections 2024–25

- Modeled tax rate swing: ~4–6% in scenarios

- Contingency reserve uplift for instability: 10–20%

- Focus areas: tech regulation, data/privacy, AI oversight

Tech export controls and sanctions

The weaponization of tech has driven stricter export controls on advanced semiconductors and AI software—US/EU restrictions and China countermeasures impacted $500B+ semiconductor trade in 2023 and tightened AI tool transfers in 2024.

Gartner helps providers and buyers map regulatory risk, compliance pathways, and partner selection across 60+ jurisdictions, reducing deal failure risk and political exposure.

Gartner’s impartial market assessments gain value as firms face higher regulatory fines and transaction delays in restricted markets.

- Export controls rose post-2022; semiconductors $500B+ trade; 60+ jurisdictions monitored

- Gartner advisory reduces regulatory and political deal risk

- Objective analysis increasingly valuable amid rising fines and delays

Geopolitics, export rules & elections rewire supply chains; $1.6T gov IT fuels advisory demand

Geopolitical tensions, export controls and elections (US/UK/EU/India 2024–25) drive supply-chain shifts, tax uncertainty (modeled 4–6% effective rate swing), and higher compliance costs; gov’t IT spend ~$1.6T (2025) and >80 countries with data localization create steady advisory demand; semiconductor export rules affected $500B+ trade (2023); Gartner serves 15k+ regulatory clients across 120+ jurisdictions.

| Metric | Value |

|---|---|

| Gov IT spend (2025) | $1.6T |

| Data localization laws (2024) | 80+ |

| Semiconductor trade hit (2023) | $500B+ |

| Gartner regulatory clients (2024) | 15,000+ |

What is included in the product

Explores how external macro-environmental factors uniquely affect Gartner across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to highlight threats and opportunities.

Condenses Gartner's full PESTLE into a concise, visually segmented brief that’s easily dropped into presentations or shared across teams for fast alignment and decision-making.

Economic factors

Corporate spending on digital transformation

Despite macro volatility, global enterprise IT spending reached an estimated 5.3 trillion USD in 2024 with digital transformation a major share; firms sustained high investment to stay competitive.

Gartner benefits as 78% of CIOs in 2024 sought third-party data to justify multi-year tech budgets, creating demand for its advisory and validation services.

Growth in SaaS and cloud — 2024 public cloud services revenue hit ~620 billion USD — fuels continual need for Gartner benchmarking, cost-optimization and migration guidance.

Interest rates and capital allocation

As of late 2025, with USFed funds around 5.25%–5.50% and global corporate borrowing spreads up ~120 bps year-over-year, higher rates push clients to deprioritize capital-intensive projects and favor operational efficiency; 62% of surveyed CIOs said cost-optimization is top priority.

Inflationary pressure on service pricing

Persistent inflation raises costs for high-quality analysts—Gartner reported FY2024 total operating expenses up 9% YoY—forcing trade-offs between higher wages and keeping subscription prices competitive; yet demand remains, with clients spending on advisory to cut costs—Gartner’s 2024 subscription revenue grew ~6% as firms seek automation and waste reduction, reinforcing Gartner’s value proposition during inflationary pressure.

Emerging market expansion opportunities

Emerging-market GDP growth—Southeast Asia projected 4.8% in 2025 and sub-Saharan Africa 3.5%—creates client acquisition paths as mid-market firms scale and seek Gartner’s research and frameworks.

Gartner’s localized economic outlooks and services can drive global revenue diversification; APAC contributed ~33% of global IT spend growth in 2024, signaling demand for region-specific advisory.

- 2024 APAC IT spend growth ~33% of global increase

- Southeast Asia GDP ~4.8% proj. 2025

- Sub-Saharan Africa GDP ~3.5% proj. 2025

- Localization of outlooks essential for revenue diversification

Currency exchange rate volatility

As a global firm, Gartner's reported 2024 revenue of $5.5bn is sensitive to FX swings; a 5% USD strengthening can reduce translated revenue by roughly $275m, pressuring margins and international pricing.

USD strength makes Gartner services pricier for non-USD clients; in 2024, currency movements lowered international organic growth by ~1.2 percentage points.

Gartner mitigates risk via financial hedges and regional pricing—hedges covered ~40% of forecasted FX exposure in 2024.

- 2024 revenue $5.5bn; 5% USD move ≈ $275m impact

- FX trimmed intl organic growth ~1.2 pp in 2024

- Hedges covered ~40% of FX exposure in 2024

Cost pressure fuels cloud migration & benchmarking as APAC drives IT spend growth

Economic pressures—2024 global IT spend $5.3T, Gartner revenue $5.5B—drive demand for cost-optimization, benchmarking and cloud migration guidance as clients prioritize efficiency amid ~5.25% US policy rates and ~120bp wider corporate spreads; APAC drove ~33% of 2024 IT spend growth while Southeast Asia and SSA GDPs are ~4.8% and ~3.5% (2025 proj.); FX (5% USD move ≈ $275M) and 9% Opex rise in 2024 constrain margin levers.

| Metric | 2024/2025 |

|---|---|

| Global IT spend | $5.3T (2024) |

| Gartner revenue | $5.5B (2024) |

| Public cloud rev | $620B (2024) |

| US policy rate | 5.25%–5.50% (late 2025) |

| APAC share of IT spend growth | ~33% (2024) |

| Southeast Asia GDP | ~4.8% (2025 proj.) |

| Sub‑Saharan Africa GDP | ~3.5% (2025 proj.) |

| Opex rise | +9% YoY (2024) |

| FX sensitivity | 5% USD ≈ $275M impact (2024) |

Same Document Delivered

Gartner PESTLE Analysis

The preview shown here is the exact Gartner PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and market assessment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Our Gartner PESTLE Analysis reveals the key political, economic, social, technological, legal, and environmental forces shaping its strategy and market position—perfect for investors and strategists who need concise, actionable intelligence; purchase the full, editable report to access deep-dive insights, data-driven implications, and ready-to-use slides for immediate decision-making.

Political factors

Geopolitical instability and trade relations

The ongoing geopolitical tensions between the US, China, Russia and EU in late 2025 continue to disrupt supply chains, with 48% of global firms reporting increased sourcing shifts and 22% citing higher tech investment relocations; Gartner must guide clients on diversification as tariffs and export controls raise operational costs and capex risk.

Government digitization initiatives

Public sector organizations are prioritizing digital transformation, with global government IT spending projected at $1.6 trillion in 2025, driving demand for service modernization and efficiency gains.

Gartner captures this demand by delivering specialized research and consulting to agencies modernizing legacy systems, contributing to its government services revenue, which represented about 12–15% of client consulting engagements in 2024.

National policies on digital sovereignty and investments in public tech infrastructure—EU Digital Decade targets and US federal modernization funds exceeding $100 billion since 2021—create a steady advisory pipeline for Gartner.

Data sovereignty and localization laws

Governments are tightening data sovereignty rules—over 80 countries had data localization laws by 2024, impacting cross-border processing and cloud deployments.

Gartner aids multinationals by mapping these mandates; in 2024 its regulatory research served 15,000+ enterprise clients navigating compliance and vendor selection.

Providing localized legal insights across 120+ jurisdictions is a key differentiator for Gartner amid a fragmented political landscape, reducing compliance risks and potential fines.

Election cycles and policy shifts

Major elections in 2024–2025 in the US, UK, India and EU members prompted shifts in corporate tax proposals and tighter tech regulation, with 2024 US corporate tax debate affecting forecasts for 2025 M&A and capex (estimated 4–6% impact on effective tax rates in scenarios Gartner models).

Gartner tracks transitions to advise clients on policy volatility and likely regulatory oversight increases in data/privacy and AI, incorporating scenario probabilities and stress-testing revenue and compliance cost impacts.

Political stability is flagged as key for long-term planning: Gartner’s client risk dashboards weight stability metrics and show firms in unstable jurisdictions face 10–20% higher contingency reserves on average.

- Key markets: US, UK, EU, India — elections 2024–25

- Modeled tax rate swing: ~4–6% in scenarios

- Contingency reserve uplift for instability: 10–20%

- Focus areas: tech regulation, data/privacy, AI oversight

Tech export controls and sanctions

The weaponization of tech has driven stricter export controls on advanced semiconductors and AI software—US/EU restrictions and China countermeasures impacted $500B+ semiconductor trade in 2023 and tightened AI tool transfers in 2024.

Gartner helps providers and buyers map regulatory risk, compliance pathways, and partner selection across 60+ jurisdictions, reducing deal failure risk and political exposure.

Gartner’s impartial market assessments gain value as firms face higher regulatory fines and transaction delays in restricted markets.

- Export controls rose post-2022; semiconductors $500B+ trade; 60+ jurisdictions monitored

- Gartner advisory reduces regulatory and political deal risk

- Objective analysis increasingly valuable amid rising fines and delays

Geopolitics, export rules & elections rewire supply chains; $1.6T gov IT fuels advisory demand

Geopolitical tensions, export controls and elections (US/UK/EU/India 2024–25) drive supply-chain shifts, tax uncertainty (modeled 4–6% effective rate swing), and higher compliance costs; gov’t IT spend ~$1.6T (2025) and >80 countries with data localization create steady advisory demand; semiconductor export rules affected $500B+ trade (2023); Gartner serves 15k+ regulatory clients across 120+ jurisdictions.

| Metric | Value |

|---|---|

| Gov IT spend (2025) | $1.6T |

| Data localization laws (2024) | 80+ |

| Semiconductor trade hit (2023) | $500B+ |

| Gartner regulatory clients (2024) | 15,000+ |

What is included in the product

Explores how external macro-environmental factors uniquely affect Gartner across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to highlight threats and opportunities.

Condenses Gartner's full PESTLE into a concise, visually segmented brief that’s easily dropped into presentations or shared across teams for fast alignment and decision-making.

Economic factors

Corporate spending on digital transformation

Despite macro volatility, global enterprise IT spending reached an estimated 5.3 trillion USD in 2024 with digital transformation a major share; firms sustained high investment to stay competitive.

Gartner benefits as 78% of CIOs in 2024 sought third-party data to justify multi-year tech budgets, creating demand for its advisory and validation services.

Growth in SaaS and cloud — 2024 public cloud services revenue hit ~620 billion USD — fuels continual need for Gartner benchmarking, cost-optimization and migration guidance.

Interest rates and capital allocation

As of late 2025, with USFed funds around 5.25%–5.50% and global corporate borrowing spreads up ~120 bps year-over-year, higher rates push clients to deprioritize capital-intensive projects and favor operational efficiency; 62% of surveyed CIOs said cost-optimization is top priority.

Inflationary pressure on service pricing

Persistent inflation raises costs for high-quality analysts—Gartner reported FY2024 total operating expenses up 9% YoY—forcing trade-offs between higher wages and keeping subscription prices competitive; yet demand remains, with clients spending on advisory to cut costs—Gartner’s 2024 subscription revenue grew ~6% as firms seek automation and waste reduction, reinforcing Gartner’s value proposition during inflationary pressure.

Emerging market expansion opportunities

Emerging-market GDP growth—Southeast Asia projected 4.8% in 2025 and sub-Saharan Africa 3.5%—creates client acquisition paths as mid-market firms scale and seek Gartner’s research and frameworks.

Gartner’s localized economic outlooks and services can drive global revenue diversification; APAC contributed ~33% of global IT spend growth in 2024, signaling demand for region-specific advisory.

- 2024 APAC IT spend growth ~33% of global increase

- Southeast Asia GDP ~4.8% proj. 2025

- Sub-Saharan Africa GDP ~3.5% proj. 2025

- Localization of outlooks essential for revenue diversification

Currency exchange rate volatility

As a global firm, Gartner's reported 2024 revenue of $5.5bn is sensitive to FX swings; a 5% USD strengthening can reduce translated revenue by roughly $275m, pressuring margins and international pricing.

USD strength makes Gartner services pricier for non-USD clients; in 2024, currency movements lowered international organic growth by ~1.2 percentage points.

Gartner mitigates risk via financial hedges and regional pricing—hedges covered ~40% of forecasted FX exposure in 2024.

- 2024 revenue $5.5bn; 5% USD move ≈ $275m impact

- FX trimmed intl organic growth ~1.2 pp in 2024

- Hedges covered ~40% of FX exposure in 2024

Cost pressure fuels cloud migration & benchmarking as APAC drives IT spend growth

Economic pressures—2024 global IT spend $5.3T, Gartner revenue $5.5B—drive demand for cost-optimization, benchmarking and cloud migration guidance as clients prioritize efficiency amid ~5.25% US policy rates and ~120bp wider corporate spreads; APAC drove ~33% of 2024 IT spend growth while Southeast Asia and SSA GDPs are ~4.8% and ~3.5% (2025 proj.); FX (5% USD move ≈ $275M) and 9% Opex rise in 2024 constrain margin levers.

| Metric | 2024/2025 |

|---|---|

| Global IT spend | $5.3T (2024) |

| Gartner revenue | $5.5B (2024) |

| Public cloud rev | $620B (2024) |

| US policy rate | 5.25%–5.50% (late 2025) |

| APAC share of IT spend growth | ~33% (2024) |

| Southeast Asia GDP | ~4.8% (2025 proj.) |

| Sub‑Saharan Africa GDP | ~3.5% (2025 proj.) |

| Opex rise | +9% YoY (2024) |

| FX sensitivity | 5% USD ≈ $275M impact (2024) |

Same Document Delivered

Gartner PESTLE Analysis

The preview shown here is the exact Gartner PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and market assessment.