Gates Industrial Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

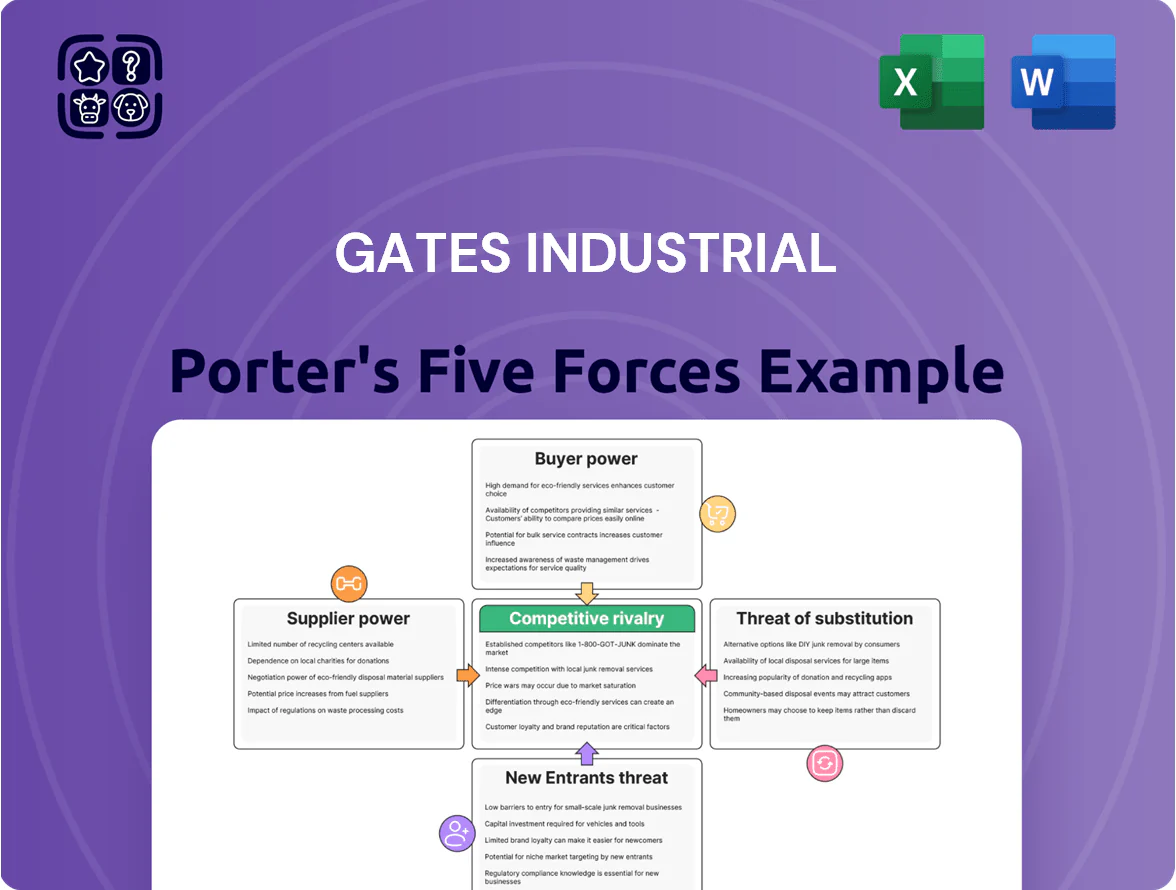

Gates Industrial faces moderate supplier power, steady buyer leverage, and growing competitive rivalry as electrification and supply-chain shifts reshape demand; substitute threats and new entrants are tempered by scale and technical know-how.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Gates Industrial’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Price Volatility

Gates Industrial depends on commodities—synthetic rubber, steel, and specialized polymers—whose prices swung 18–28% year-on-year in 2021–2023, amplifying input-cost risk. Suppliers can raise prices during tight supply; for example, global natural rubber spot prices jumped ~22% in 2021–2022, pressuring margins. This volatility lifted Gates’ cost of goods sold and forced higher inventory days—management reported inventory up 12% in FY2023—to buffer shortages and limit margin erosion.

Specialized Chemical Dependencies

Many Gates Industrial high-performance belts and hoses rely on proprietary polymer compounds and additives, and only about 6–8 global chemical firms (per 2024 ICIS supply data) meet the strict industrial specs needed for heat, oil, and abrasion resistance.

Supplier concentration raises bargaining power: when two or three suppliers control key elastomer grades, Gates faces higher input price volatility—raw-material cost swings of 15–25% in 2023–24 pushed COGS up ~3–4 percentage points for comparable manufacturers.

Energy and Utility Costs

Gates faces high supplier power on energy: its power-transmission and fluid-power lines are energy-intensive, so utility price rises hit COGS—energy was ~6–9% of manufacturing input costs for similar auto suppliers in 2024, and a 10% utility hike could raise margins by ~0.5–1.0 percentage points. Regional crises (e.g., EU 2022–24 gas spikes) and shifts to pricier renewables push global plant costs up. Localized utility monopolies limit sourcing alternatives and cap Gates’ negotiation leverage.

Global Logistics and Shipping Constraints

Suppliers of freight and logistics move Gates Industrial’s inputs and finished goods; global shipping capacity fell in 2023–24 as top 10 carriers handled ~75% of container capacity, raising supplier leverage over rates and schedules.

Port congestion and blank sailings in 2021–23 raised lead times by 10–30 days and logistics costs; a 2024 IHS Markit estimate shows container freight rates remain ~40% above 2019 averages, pressuring Gates’ margins and inventory costs.

Disruptions force higher safety stock and expediting, increasing OPEX and working capital needs, and give logistics providers bargaining power on pricing and service levels.

- Top 10 carriers ~75% capacity (2023–24)

- Lead time increases: +10–30 days (2021–23)

- Freight rates ~+40% vs 2019 (2024)

- Higher safety stock → higher OPEX/WC

Technological Integration of Components

As Gates shifts toward smart fluid-power systems, suppliers of sensors and ASICs—often protected by patents—gain leverage; in 2024 the global industrial sensor market reached $25.6B, tightening supplier concentration for niche parts.

These proprietary components raise switching costs and can extend lead times; Gates reported 12% revenue exposure in 2024 to electrified/fluid-electronics products, increasing supplier bargaining power.

What this estimate hides: dual-source strategies cut risk but add costs and CAPEX for qualification.

- Supplier patents raise switching cost and price control

- Sensors market size $25.6B (2024) increases concentration

- Gates ~12% 2024 revenue tied to electrified fluid products

- Dual-sourcing reduces risk but raises qualification cost

Supply squeeze: concentrated suppliers, +40% freight, longer lead times, electrification growth

Suppliers hold moderate–high power: concentrated elastomer/chemical suppliers (6–8 firms), energy costs ~6–9% of inputs, freight capacity top-10 ~=75%, lead times +10–30 days, freight +40% vs 2019, sensors market $25.6B (2024), Gates ~12% 2024 rev in electrified products—dual-sourcing reduces risk but raises qualification cost.

| Metric | Value |

|---|---|

| Key suppliers | 6–8 firms |

| Energy share | 6–9% |

| Top-10 carriers | ~75% |

| Lead time rise | +10–30 days |

| Freight vs 2019 | +40% |

| Sensors market | $25.6B (2024) |

| Electrified rev | ~12% (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Gates Industrial that uncovers competitive drivers, supplier and buyer power, new-entry barriers, substitute threats, and strategic implications for profitability and market positioning.

Concise Porter's Five Forces for Gates Industrial—one-sheet clarity to spot competitive pain points and prioritize strategic responses.

Customers Bargaining Power

Concentration of Large OEM Clients

A significant share of Gates Industrial revenue—about 42% of 2024 sales, per company filings—comes from large OEMs in automotive, agriculture and construction, concentrating buyer power.

These high-volume customers can demand price cuts, tailored components and extended payment terms, squeezing margins and working-capital needs.

Loss of a major OEM contract could cut utilization and revenue materially; a single top-5 OEM exit would risk double-digit percent revenue impact and raise fixed-cost absorption.

Availability of Alternative Brands

In Gates Industrial’s aftermarket, distributors and end-users can choose from multiple brands with similar specs, raising price sensitivity; industry data shows global aftermarket parts fragmentation with top five suppliers holding under 40% share as of 2024. This choice means customers often switch for short-term promos or small price gaps, pushing Gates to invest in quality assurance and delivery speed—Gates reported 98% on-time delivery in 2024 vs. 95% in 2022.

Low Switching Costs for Standard Products

For many standard belts and hoses used in general industrial maintenance, switching costs are low; industry surveys in 2024 show 62% of maintenance buyers prioritize price and availability over brand, so Gates faces frequent churn pressure. Because these products follow universal standards, customers can swap suppliers without equipment changes, forcing Gates to compete on service, delivery and warranty—areas where it reported a 2024 service NPS of 48 versus 35 for smaller peers.

Price Transparency in Digital Markets

Price transparency from B2B e-commerce means Gates Industrial faces easy cross-border price comparison; platforms showed a 28% rise in procurement tool usage in 2024, shrinking premium pricing leeway.

Procurement teams use benchmarking and TCO (total cost of ownership) analytics, so Gates must prove added value — warranty, service or supply resilience — to keep margins.

Smaller buyers now negotiate like large firms: 41% of mid-market purchasers reported using market-price dashboards in 2024, upping discount pressure.

- 28% rise in procurement tool use (2024)

- 41% mid-market buyers use price dashboards (2024)

- Must prove warranty/service value to preserve premium

Inventory Management Demands

OEM leverage and price-savvy buyers force Gates to defend margins with service

Buyers—especially large OEMs (≈42% of 2024 sales)—have strong leverage to demand price cuts, custom specs and extended terms, risking double-digit revenue loss if a top-5 OEM exits; aftermarket buyers face low switching costs (62% prioritize price) and high price transparency (procurement tool use +28% in 2024), forcing Gates to compete on service, delivery (98% on-time in 2024) and warranty to protect margins.

| Metric | 2024 |

|---|---|

| OEM revenue share | 42% |

| Procurement tool use rise | +28% |

| Maintenance buyers price-first | 62% |

| On-time delivery | 98% |

| Service churn | 2.1% |

Full Version Awaits

Gates Industrial Porter's Five Forces Analysis

This preview shows the exact Gates Industrial Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the same professionally written, fully formatted file you'll be able to download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Gates Industrial faces moderate supplier power, steady buyer leverage, and growing competitive rivalry as electrification and supply-chain shifts reshape demand; substitute threats and new entrants are tempered by scale and technical know-how.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Gates Industrial’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Price Volatility

Gates Industrial depends on commodities—synthetic rubber, steel, and specialized polymers—whose prices swung 18–28% year-on-year in 2021–2023, amplifying input-cost risk. Suppliers can raise prices during tight supply; for example, global natural rubber spot prices jumped ~22% in 2021–2022, pressuring margins. This volatility lifted Gates’ cost of goods sold and forced higher inventory days—management reported inventory up 12% in FY2023—to buffer shortages and limit margin erosion.

Specialized Chemical Dependencies

Many Gates Industrial high-performance belts and hoses rely on proprietary polymer compounds and additives, and only about 6–8 global chemical firms (per 2024 ICIS supply data) meet the strict industrial specs needed for heat, oil, and abrasion resistance.

Supplier concentration raises bargaining power: when two or three suppliers control key elastomer grades, Gates faces higher input price volatility—raw-material cost swings of 15–25% in 2023–24 pushed COGS up ~3–4 percentage points for comparable manufacturers.

Energy and Utility Costs

Gates faces high supplier power on energy: its power-transmission and fluid-power lines are energy-intensive, so utility price rises hit COGS—energy was ~6–9% of manufacturing input costs for similar auto suppliers in 2024, and a 10% utility hike could raise margins by ~0.5–1.0 percentage points. Regional crises (e.g., EU 2022–24 gas spikes) and shifts to pricier renewables push global plant costs up. Localized utility monopolies limit sourcing alternatives and cap Gates’ negotiation leverage.

Global Logistics and Shipping Constraints

Suppliers of freight and logistics move Gates Industrial’s inputs and finished goods; global shipping capacity fell in 2023–24 as top 10 carriers handled ~75% of container capacity, raising supplier leverage over rates and schedules.

Port congestion and blank sailings in 2021–23 raised lead times by 10–30 days and logistics costs; a 2024 IHS Markit estimate shows container freight rates remain ~40% above 2019 averages, pressuring Gates’ margins and inventory costs.

Disruptions force higher safety stock and expediting, increasing OPEX and working capital needs, and give logistics providers bargaining power on pricing and service levels.

- Top 10 carriers ~75% capacity (2023–24)

- Lead time increases: +10–30 days (2021–23)

- Freight rates ~+40% vs 2019 (2024)

- Higher safety stock → higher OPEX/WC

Technological Integration of Components

As Gates shifts toward smart fluid-power systems, suppliers of sensors and ASICs—often protected by patents—gain leverage; in 2024 the global industrial sensor market reached $25.6B, tightening supplier concentration for niche parts.

These proprietary components raise switching costs and can extend lead times; Gates reported 12% revenue exposure in 2024 to electrified/fluid-electronics products, increasing supplier bargaining power.

What this estimate hides: dual-source strategies cut risk but add costs and CAPEX for qualification.

- Supplier patents raise switching cost and price control

- Sensors market size $25.6B (2024) increases concentration

- Gates ~12% 2024 revenue tied to electrified fluid products

- Dual-sourcing reduces risk but raises qualification cost

Supply squeeze: concentrated suppliers, +40% freight, longer lead times, electrification growth

Suppliers hold moderate–high power: concentrated elastomer/chemical suppliers (6–8 firms), energy costs ~6–9% of inputs, freight capacity top-10 ~=75%, lead times +10–30 days, freight +40% vs 2019, sensors market $25.6B (2024), Gates ~12% 2024 rev in electrified products—dual-sourcing reduces risk but raises qualification cost.

| Metric | Value |

|---|---|

| Key suppliers | 6–8 firms |

| Energy share | 6–9% |

| Top-10 carriers | ~75% |

| Lead time rise | +10–30 days |

| Freight vs 2019 | +40% |

| Sensors market | $25.6B (2024) |

| Electrified rev | ~12% (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Gates Industrial that uncovers competitive drivers, supplier and buyer power, new-entry barriers, substitute threats, and strategic implications for profitability and market positioning.

Concise Porter's Five Forces for Gates Industrial—one-sheet clarity to spot competitive pain points and prioritize strategic responses.

Customers Bargaining Power

Concentration of Large OEM Clients

A significant share of Gates Industrial revenue—about 42% of 2024 sales, per company filings—comes from large OEMs in automotive, agriculture and construction, concentrating buyer power.

These high-volume customers can demand price cuts, tailored components and extended payment terms, squeezing margins and working-capital needs.

Loss of a major OEM contract could cut utilization and revenue materially; a single top-5 OEM exit would risk double-digit percent revenue impact and raise fixed-cost absorption.

Availability of Alternative Brands

In Gates Industrial’s aftermarket, distributors and end-users can choose from multiple brands with similar specs, raising price sensitivity; industry data shows global aftermarket parts fragmentation with top five suppliers holding under 40% share as of 2024. This choice means customers often switch for short-term promos or small price gaps, pushing Gates to invest in quality assurance and delivery speed—Gates reported 98% on-time delivery in 2024 vs. 95% in 2022.

Low Switching Costs for Standard Products

For many standard belts and hoses used in general industrial maintenance, switching costs are low; industry surveys in 2024 show 62% of maintenance buyers prioritize price and availability over brand, so Gates faces frequent churn pressure. Because these products follow universal standards, customers can swap suppliers without equipment changes, forcing Gates to compete on service, delivery and warranty—areas where it reported a 2024 service NPS of 48 versus 35 for smaller peers.

Price Transparency in Digital Markets

Price transparency from B2B e-commerce means Gates Industrial faces easy cross-border price comparison; platforms showed a 28% rise in procurement tool usage in 2024, shrinking premium pricing leeway.

Procurement teams use benchmarking and TCO (total cost of ownership) analytics, so Gates must prove added value — warranty, service or supply resilience — to keep margins.

Smaller buyers now negotiate like large firms: 41% of mid-market purchasers reported using market-price dashboards in 2024, upping discount pressure.

- 28% rise in procurement tool use (2024)

- 41% mid-market buyers use price dashboards (2024)

- Must prove warranty/service value to preserve premium

Inventory Management Demands

OEM leverage and price-savvy buyers force Gates to defend margins with service

Buyers—especially large OEMs (≈42% of 2024 sales)—have strong leverage to demand price cuts, custom specs and extended terms, risking double-digit revenue loss if a top-5 OEM exits; aftermarket buyers face low switching costs (62% prioritize price) and high price transparency (procurement tool use +28% in 2024), forcing Gates to compete on service, delivery (98% on-time in 2024) and warranty to protect margins.

| Metric | 2024 |

|---|---|

| OEM revenue share | 42% |

| Procurement tool use rise | +28% |

| Maintenance buyers price-first | 62% |

| On-time delivery | 98% |

| Service churn | 2.1% |

Full Version Awaits

Gates Industrial Porter's Five Forces Analysis

This preview shows the exact Gates Industrial Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the same professionally written, fully formatted file you'll be able to download and use the moment you buy.