Gateway PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

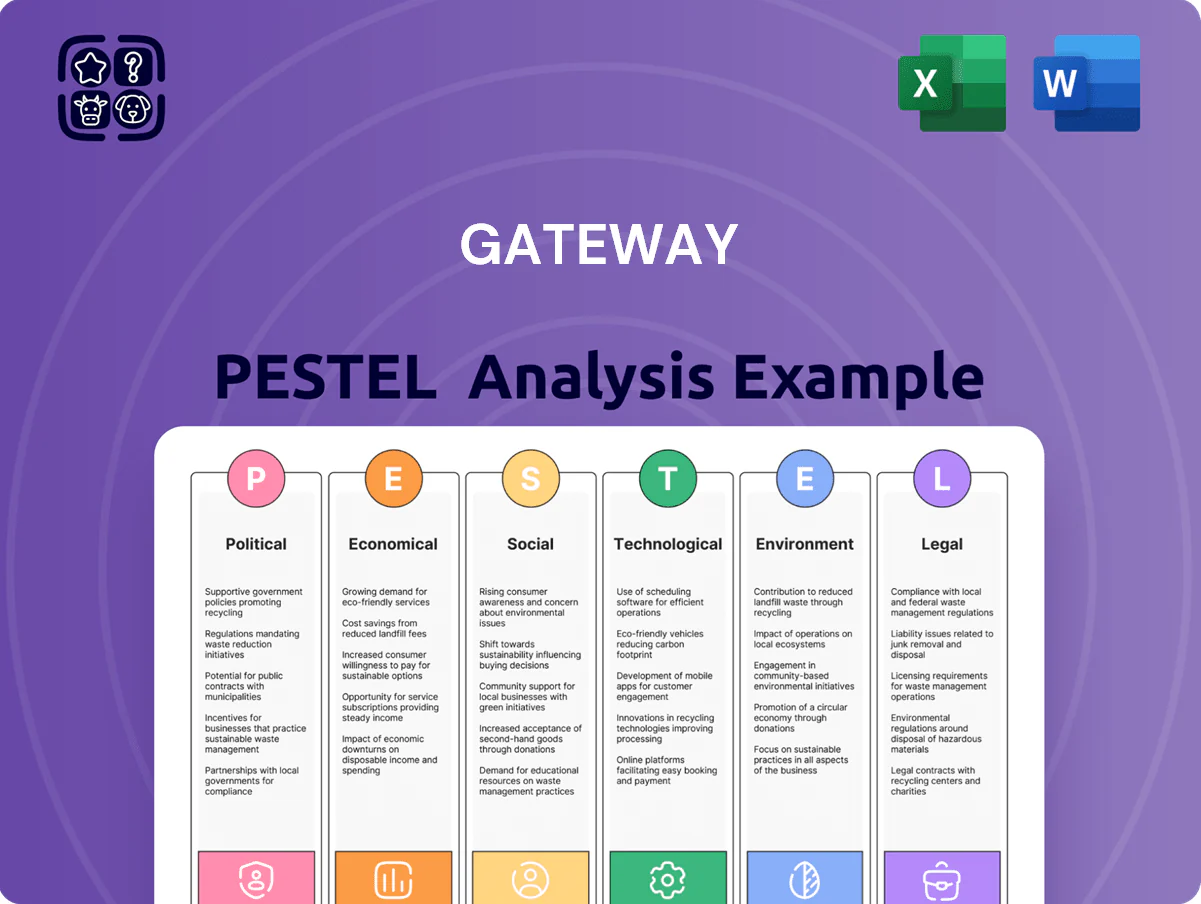

Unlock strategic advantage with our Gateway PESTLE Analysis—concise, expertly researched insight into the political, economic, social, technological, legal, and environmental forces shaping the company’s future; buy the full report to access in-depth findings, actionable risks and opportunities, and ready-to-use charts for decision-making.

Political factors

Gati-Shakti National Master Plan execution

The Gati-Shakti National Master Plan’s push for multimodal connectivity through 2025 gives integrated logistics firms a measurable tailwind, with India targeting a reduction in logistics costs from ~14% of GDP in 2023 to under 10% by 2030 per NITI Aayog estimates, aiding Gateway Distriparks’ modal integration.

Streamlined approvals and unified corridor planning cut project lead times; reports show inland container depot and rail siding expansion approvals accelerated by ~20% in 2024, easing Gateway’s capex rollout.

Better synchronization across road, rail and ports boosts asset turnover for Gateway, with industry data indicating average transit times on key corridors fell ~12% in 2024, improving utilization and freight throughput.

Government’s sustained commitment to logistics efficiency aligns with Gateway’s strategy, supporting revenue mix shift to value-added multimodal services and margin expansion as national targets lower system-wide costs.

Western Dedicated Freight Corridor completion

The full operationalization of the Western Dedicated Freight Corridor by end-2025 has cut rail transit times between the northern hinterland and western ports by up to 30%, enabling Gateway Distriparks to offer faster, more reliable container train services versus road transport.

Gateway leverages higher axle loads and double-stacking to increase throughput, supporting up to 25–30% higher container volumes per train and capturing a growing share of EXIM cargo.

Government investment—approx. $10–12 billion into DFCs through 2025—cements a policy-driven advantage for rail-linked logistics operators, improving asset utilization and margin stability for Gateway.

Trade policy and PLI scheme impact

Government Production Linked Incentive schemes have boosted domestic manufacturing, lifting containerized exports by an estimated 12-15% and increasing volumes at Gateway Distriparks’ CFSs, especially for electronics, automotive and textiles; Gateway’s FY24 revenue mix showed a 10% rise in container-related throughput tied to PLI beneficiaries. As of 2025 stable trade policies support multi-year contracts with large manufacturers, while recent bilateral trade pacts have diversified cargo mix, adding ~8% new commodity categories to handled volumes.

Port privatization and infrastructure reforms

The Sagarmala-led push to privatize major terminals has raised Indian port productivity; major ports’ container throughput grew 6.8% to 9.4 million TEUs in FY2024, aiding Gateway Distriparks by reducing CFS congestion and cutting average container dwell times by up to 12–15% at privatised terminals.

Stable maritime policy and tariff rationalisation through 2024 allow Gateway to better time capacity expansion, while increased private investment—private terminal capacity rose ~18% from 2020–2024—favours integrated providers offering end-to-end logistics.

- FY2024 container throughput: 9.4m TEUs (major ports), +6.8%

- Private terminal capacity growth 2020–2024: ~18%

- Estimated dwell time reduction at privatised terminals: 12–15%

- Enables predictable capex planning and rewards integrated service models

Geopolitical trade relations and stability

India's strategic navigation of trade tensions has strengthened its China Plus One appeal, with FDI inflows rising to USD 84.9 billion in FY2023–24 and manufacturing GVA up 8.6% in 2024, boosting Gateway Distriparks as MNCs shift production to India through 2025.

Geopolitical volatility persists, but active Indian trade diplomacy kept container throughput resilient—India handled 4.2 million TEU at major ports in 2024—supporting steady import/export volumes that align with Gateway's rail-road-port logistics model.

Gateway's asset-light, intermodal network is scaled for higher throughput: FY2024 consolidated revenue grew ~11% YoY, positioning the company to capture incremental containerized traffic from supply-chain reconfiguration.

- FDI inflows USD 84.9bn FY2023–24

- Manufacturing GVA +8.6% in 2024

- Major ports handled ~4.2m TEU in 2024

- Gateway revenue ~+11% YoY FY2024

Logistics reforms cut transit times, boost ports, FDI and Gateway revenues

Political support for logistics—Gati-Shakti, DFCs, PLI, Sagarmala—cut transit times ~12–30%, lifted container throughput (major ports 9.4m TEU FY24, +6.8%), and boosted FDI to USD84.9bn FY23–24; Gateway saw ~11% revenue growth FY24 and 10% rise in container throughput from PLI-linked cargo.

| Metric | Value |

|---|---|

| Major ports TEU FY24 | 9.4m (+6.8%) |

| FDI FY23–24 | USD84.9bn |

| Gateway rev FY24 | +11% YoY |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact the Gateway, with data-backed trends, region- and industry-specific subpoints, forward-looking insights for scenario planning, and clean formatting to support executives, investors, and entrepreneurs in identifying strategic risks and opportunities.

Gateway’s PESTLE Analysis delivers a concise, shareable summary organized by category for quick interpretation in meetings, easily drop‑in to presentations, and editable for region‑ or business‑specific notes to streamline strategic discussions and cross‑team alignment.

Economic factors

Indian GDP growth and EXIM volumes

India's GDP grew 7.2% in FY2023–24 and IMF projects ~6.5% in 2025, underpinning demand for containerized logistics as industrial production rose 5.8% YoY (2024) and retail consumption strengthened. Imports surged 9% YoY in 2024 while merchandise exports hit a record $463 billion in FY2023–24, lifting volumes through Gateway's CFS and ICDs. Gateway's revenue correlates with a resilient trade-to-GDP ratio near 45% and reported 16–18% utilization-driven margin stability in 2024. High utilization across its network supports sustained operating margins despite global headwinds.

Interest rate environment and capital expenditure

As of late 2025, India’s repo rate stood at 6.5%, a relatively stable level from 2024–25 that helps Gateway Distriparks manage debt-funded expansion and lowers average borrowing costs.

Reduced cost of capital improves feasibility of acquiring new ICD land and investing in rolling stock, directly enhancing projected ROCE on greenfield projects.

Stable/declining rates boost net profit margins via lower interest expense; analysts track leverage ratios and interest coverage to ensure sustainable funding of growth.

Fuel price volatility and operational costs

Fluctuations in global crude oil—Brent averaged about 95 USD/bbl in 2024—raise road transport and yard equipment costs, while Gateway Distriparks shifts long-haul loads to rail to reduce fuel exposure.

First/last-mile diesel sensitivity persists; diesel in India averaged ~95–110 INR/l across 2024–25, impacting short-haul margins despite fuel surcharges.

Fuel surcharge pass-through cushions costs but extreme swings (±20% oil moves) can compress quarterly EBIT margins; analysts monitor this to compare rail cost-efficiency versus road.

Container availability and global shipping rates

Stabilization of container shipping rates and availability by end-2025—global average spot rates down ~45% from 2021 peaks to about $1,200 per FEU in 2025—gave logistics predictability, lowering Gateway Distriparks’ empty repositioning costs and improving equipment balance.

Efficient ocean carrier operations increased inland depot throughput, raising rail utilization and supporting steady volume growth; Gateway’s rail load factors likely improved, cutting supply-chain bottleneck risk that hit 2021–23.

- Global spot rate ~ $1,200/FEU (2025)

- Empty repositioning costs reduced; better equipment balance

- Higher depot throughput → improved rail asset utilization

- Supports steady volume growth, lower bottleneck risk

Inflationary pressures on labor and maintenance

Persistent 2024–25 inflation (India CPI ~5.4% in 2024) has driven higher wages for skilled rail/port technicians and 8–12% increases in outsourced maintenance contracts, pressuring Gateway Distriparks’ margins.

The company balances competitive pay with productivity gains and reported FY2024 cost-control CAPEX and process optimization savings of ~₹30–50 crore to protect EBITDA.

Stakeholders should monitor inflation and wage trends to assess long-term operating-margin sustainability as input costs remain elevated.

- 2024 CPI ~5.4%; maintenance contract hikes 8–12%

- FY2024 optimization savings ~₹30–50 crore

- Wage inflation risks to EBITDA; monitoring required

Trade-led boom boosts CFS/ICD margins as costs and repo rates shape 2024–25 outlook

Robust trade-driven demand: India GDP ~7.2% (FY24), trade/GDP ~45%, merchandise exports $463bn (FY24) drove higher CFS/ICD volumes; utilization 16–18% lift to margins. Repo ~6.5% (2025) eased borrowing; FY24 optimization savings ₹30–50cr. Brent ~$95/bbl (2024) and diesel ₹95–110/liter (2024–25) raised transport costs; global spot $1,200/FEU (2025) cut repositioning costs.

| Metric | Value |

|---|---|

| GDP (FY24) | 7.2% |

| Exports (FY24) | $463bn |

| Repo (2025) | 6.5% |

| Brent (2024) | $95/bbl |

| Diesel (2024–25) | ₹95–110/l |

| Spot rate (2025) | $1,200/FEU |

| Optimization savings (FY24) | ₹30–50cr |

Preview the Actual Deliverable

Gateway PESTLE Analysis

The preview shown here is the exact Gateway PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic advantage with our Gateway PESTLE Analysis—concise, expertly researched insight into the political, economic, social, technological, legal, and environmental forces shaping the company’s future; buy the full report to access in-depth findings, actionable risks and opportunities, and ready-to-use charts for decision-making.

Political factors

Gati-Shakti National Master Plan execution

The Gati-Shakti National Master Plan’s push for multimodal connectivity through 2025 gives integrated logistics firms a measurable tailwind, with India targeting a reduction in logistics costs from ~14% of GDP in 2023 to under 10% by 2030 per NITI Aayog estimates, aiding Gateway Distriparks’ modal integration.

Streamlined approvals and unified corridor planning cut project lead times; reports show inland container depot and rail siding expansion approvals accelerated by ~20% in 2024, easing Gateway’s capex rollout.

Better synchronization across road, rail and ports boosts asset turnover for Gateway, with industry data indicating average transit times on key corridors fell ~12% in 2024, improving utilization and freight throughput.

Government’s sustained commitment to logistics efficiency aligns with Gateway’s strategy, supporting revenue mix shift to value-added multimodal services and margin expansion as national targets lower system-wide costs.

Western Dedicated Freight Corridor completion

The full operationalization of the Western Dedicated Freight Corridor by end-2025 has cut rail transit times between the northern hinterland and western ports by up to 30%, enabling Gateway Distriparks to offer faster, more reliable container train services versus road transport.

Gateway leverages higher axle loads and double-stacking to increase throughput, supporting up to 25–30% higher container volumes per train and capturing a growing share of EXIM cargo.

Government investment—approx. $10–12 billion into DFCs through 2025—cements a policy-driven advantage for rail-linked logistics operators, improving asset utilization and margin stability for Gateway.

Trade policy and PLI scheme impact

Government Production Linked Incentive schemes have boosted domestic manufacturing, lifting containerized exports by an estimated 12-15% and increasing volumes at Gateway Distriparks’ CFSs, especially for electronics, automotive and textiles; Gateway’s FY24 revenue mix showed a 10% rise in container-related throughput tied to PLI beneficiaries. As of 2025 stable trade policies support multi-year contracts with large manufacturers, while recent bilateral trade pacts have diversified cargo mix, adding ~8% new commodity categories to handled volumes.

Port privatization and infrastructure reforms

The Sagarmala-led push to privatize major terminals has raised Indian port productivity; major ports’ container throughput grew 6.8% to 9.4 million TEUs in FY2024, aiding Gateway Distriparks by reducing CFS congestion and cutting average container dwell times by up to 12–15% at privatised terminals.

Stable maritime policy and tariff rationalisation through 2024 allow Gateway to better time capacity expansion, while increased private investment—private terminal capacity rose ~18% from 2020–2024—favours integrated providers offering end-to-end logistics.

- FY2024 container throughput: 9.4m TEUs (major ports), +6.8%

- Private terminal capacity growth 2020–2024: ~18%

- Estimated dwell time reduction at privatised terminals: 12–15%

- Enables predictable capex planning and rewards integrated service models

Geopolitical trade relations and stability

India's strategic navigation of trade tensions has strengthened its China Plus One appeal, with FDI inflows rising to USD 84.9 billion in FY2023–24 and manufacturing GVA up 8.6% in 2024, boosting Gateway Distriparks as MNCs shift production to India through 2025.

Geopolitical volatility persists, but active Indian trade diplomacy kept container throughput resilient—India handled 4.2 million TEU at major ports in 2024—supporting steady import/export volumes that align with Gateway's rail-road-port logistics model.

Gateway's asset-light, intermodal network is scaled for higher throughput: FY2024 consolidated revenue grew ~11% YoY, positioning the company to capture incremental containerized traffic from supply-chain reconfiguration.

- FDI inflows USD 84.9bn FY2023–24

- Manufacturing GVA +8.6% in 2024

- Major ports handled ~4.2m TEU in 2024

- Gateway revenue ~+11% YoY FY2024

Logistics reforms cut transit times, boost ports, FDI and Gateway revenues

Political support for logistics—Gati-Shakti, DFCs, PLI, Sagarmala—cut transit times ~12–30%, lifted container throughput (major ports 9.4m TEU FY24, +6.8%), and boosted FDI to USD84.9bn FY23–24; Gateway saw ~11% revenue growth FY24 and 10% rise in container throughput from PLI-linked cargo.

| Metric | Value |

|---|---|

| Major ports TEU FY24 | 9.4m (+6.8%) |

| FDI FY23–24 | USD84.9bn |

| Gateway rev FY24 | +11% YoY |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact the Gateway, with data-backed trends, region- and industry-specific subpoints, forward-looking insights for scenario planning, and clean formatting to support executives, investors, and entrepreneurs in identifying strategic risks and opportunities.

Gateway’s PESTLE Analysis delivers a concise, shareable summary organized by category for quick interpretation in meetings, easily drop‑in to presentations, and editable for region‑ or business‑specific notes to streamline strategic discussions and cross‑team alignment.

Economic factors

Indian GDP growth and EXIM volumes

India's GDP grew 7.2% in FY2023–24 and IMF projects ~6.5% in 2025, underpinning demand for containerized logistics as industrial production rose 5.8% YoY (2024) and retail consumption strengthened. Imports surged 9% YoY in 2024 while merchandise exports hit a record $463 billion in FY2023–24, lifting volumes through Gateway's CFS and ICDs. Gateway's revenue correlates with a resilient trade-to-GDP ratio near 45% and reported 16–18% utilization-driven margin stability in 2024. High utilization across its network supports sustained operating margins despite global headwinds.

Interest rate environment and capital expenditure

As of late 2025, India’s repo rate stood at 6.5%, a relatively stable level from 2024–25 that helps Gateway Distriparks manage debt-funded expansion and lowers average borrowing costs.

Reduced cost of capital improves feasibility of acquiring new ICD land and investing in rolling stock, directly enhancing projected ROCE on greenfield projects.

Stable/declining rates boost net profit margins via lower interest expense; analysts track leverage ratios and interest coverage to ensure sustainable funding of growth.

Fuel price volatility and operational costs

Fluctuations in global crude oil—Brent averaged about 95 USD/bbl in 2024—raise road transport and yard equipment costs, while Gateway Distriparks shifts long-haul loads to rail to reduce fuel exposure.

First/last-mile diesel sensitivity persists; diesel in India averaged ~95–110 INR/l across 2024–25, impacting short-haul margins despite fuel surcharges.

Fuel surcharge pass-through cushions costs but extreme swings (±20% oil moves) can compress quarterly EBIT margins; analysts monitor this to compare rail cost-efficiency versus road.

Container availability and global shipping rates

Stabilization of container shipping rates and availability by end-2025—global average spot rates down ~45% from 2021 peaks to about $1,200 per FEU in 2025—gave logistics predictability, lowering Gateway Distriparks’ empty repositioning costs and improving equipment balance.

Efficient ocean carrier operations increased inland depot throughput, raising rail utilization and supporting steady volume growth; Gateway’s rail load factors likely improved, cutting supply-chain bottleneck risk that hit 2021–23.

- Global spot rate ~ $1,200/FEU (2025)

- Empty repositioning costs reduced; better equipment balance

- Higher depot throughput → improved rail asset utilization

- Supports steady volume growth, lower bottleneck risk

Inflationary pressures on labor and maintenance

Persistent 2024–25 inflation (India CPI ~5.4% in 2024) has driven higher wages for skilled rail/port technicians and 8–12% increases in outsourced maintenance contracts, pressuring Gateway Distriparks’ margins.

The company balances competitive pay with productivity gains and reported FY2024 cost-control CAPEX and process optimization savings of ~₹30–50 crore to protect EBITDA.

Stakeholders should monitor inflation and wage trends to assess long-term operating-margin sustainability as input costs remain elevated.

- 2024 CPI ~5.4%; maintenance contract hikes 8–12%

- FY2024 optimization savings ~₹30–50 crore

- Wage inflation risks to EBITDA; monitoring required

Trade-led boom boosts CFS/ICD margins as costs and repo rates shape 2024–25 outlook

Robust trade-driven demand: India GDP ~7.2% (FY24), trade/GDP ~45%, merchandise exports $463bn (FY24) drove higher CFS/ICD volumes; utilization 16–18% lift to margins. Repo ~6.5% (2025) eased borrowing; FY24 optimization savings ₹30–50cr. Brent ~$95/bbl (2024) and diesel ₹95–110/liter (2024–25) raised transport costs; global spot $1,200/FEU (2025) cut repositioning costs.

| Metric | Value |

|---|---|

| GDP (FY24) | 7.2% |

| Exports (FY24) | $463bn |

| Repo (2025) | 6.5% |

| Brent (2024) | $95/bbl |

| Diesel (2024–25) | ₹95–110/l |

| Spot rate (2025) | $1,200/FEU |

| Optimization savings (FY24) | ₹30–50cr |

Preview the Actual Deliverable

Gateway PESTLE Analysis

The preview shown here is the exact Gateway PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.