GATX Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

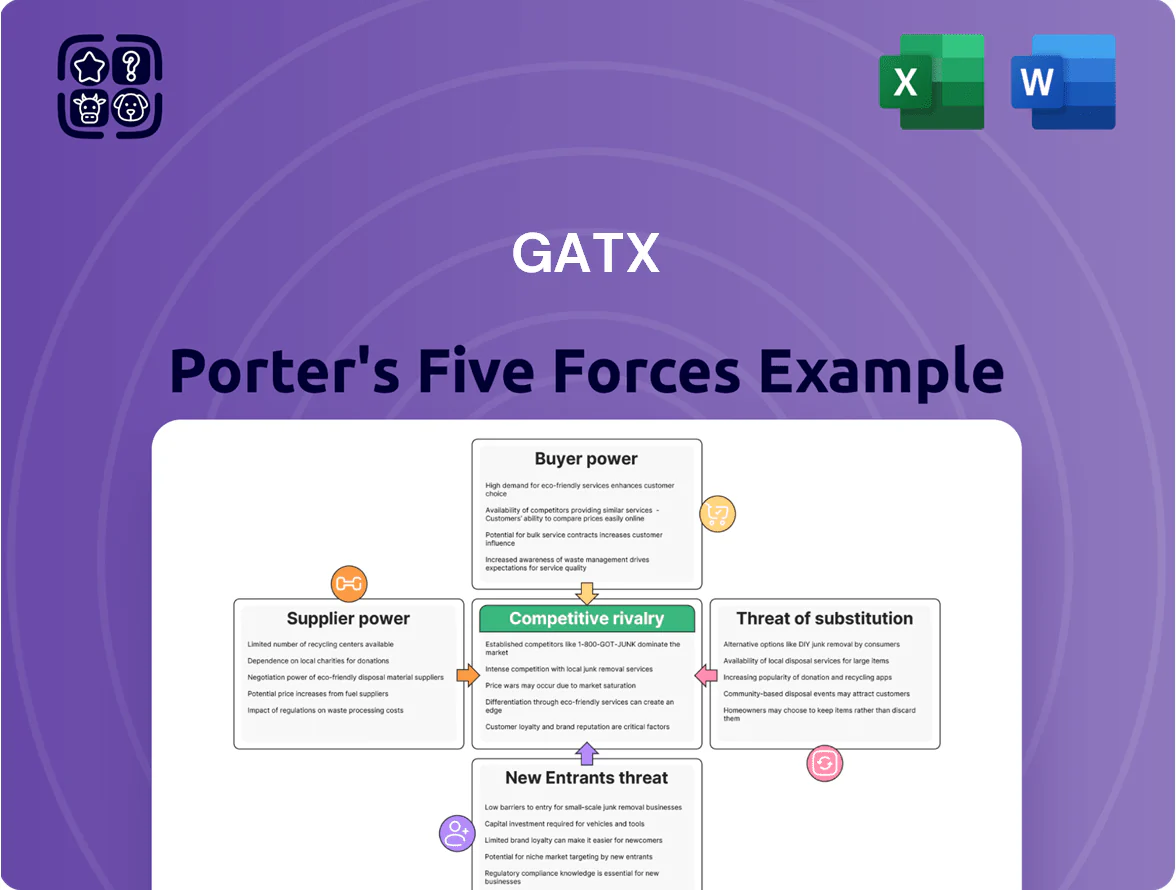

GATX operates in a capital-intensive railcar leasing market where supplier power is moderate, buyer negotiations are strong with large industrial clients, and rivalry centers on fleet scale and service differentiation; regulatory and technological shifts add external pressure. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore GATX’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Railcar Manufacturers

The new-railcar market is concentrated: Trinity Industries and The Greenbrier Company together held about 60% of North American railcar shipments in 2024, limiting GATX’s price leverage and pushing purchase premiums near 8–12% above historical averages.

These manufacturers set capacity for specialized tank and freight cars, so GATX often accepts market-driven lead times—averaging 9–14 months in 2024—and pays order premiums to secure slots.

By late 2025 consolidation (several smaller yards closed; two mid‑tier exits) strengthened supplier bargaining power, raising replacement-cycle costs for large lessors like GATX.

Raw Material Price Volatility

Suppliers of steel and precision parts face global commodity swings; benchmark hot-rolled coil rose ~18% in 2024 and remained ~12% above 2019 levels by Dec 2025, keeping supplier leverage high. GATX uses scale to negotiate discounts—fleet purchases cut unit steel cost ~5–8% in recent deals—but high-grade alloy and machined components prices are largely exogenous. Inflation in industrial materials (PPI for metals +9% y/y in 2025) sustains supplier bargaining power.

Specialized Component Dependency

Modern railcars need sophisticated braking systems, telematics, and safety valves made by a small set of niche suppliers; roughly 70–80% of AAR (Association of American Railroads)–certified components come from top 5 vendors, limiting substitution.

Because components must meet strict AAR standards, GATX faces high switching costs and long qualification cycles (often 6–18 months), so it cannot easily use lower‑cost providers.

This supplier concentration gives certified component makers significant pricing power; industry reports show specialty supplier margins near 20–30%, pressuring GATX’s maintenance and assembly costs.

Labor Market Constraints

Suppliers of maintenance, repair, and specialized railcar manufacturing labor have gained bargaining power due to skill shortages, pushing certified technician wages up ~8–12% CAGR through 2025 and increasing service costs for GATX.

GATX depends on these labor-intensive services to keep a 120,000+ railcar fleet compliant with FRA safety rules, so rising hourly rates forced GATX into longer, pricier contracts with key technical partners.

- Certified tech wage growth: 8–12% CAGR to 2025

- GATX fleet: 120,000+ railcars

- Higher long-term contracts: increased fixed servicing costs

Strategic Partnerships and Vertical Integration

GATX limits supplier power via long-term contracts and in-house maintenance; as of 2025 the company operates over 50 service centers, cutting third-party repair spend and lowering lifecycle costs by an estimated 10–15% per carload car compared with outsourced peers.

This vertical integration hedges against independent providers’ pricing swings and secures component availability, supporting higher asset utilization and predictable maintenance capex.

- 50+ service centers (2025)

- 10–15% lifecycle cost reduction

- Long-term supply agreements reduce volatility

High supplier power vs GATX scale: long lead times, rising costs, but 10–15% lifecycle cuts

Supplier power is high: two OEMs held ~60% of 2024 NA shipments, lead times 9–14 months, and steel HRC +18% in 2024 (still +12% vs 2019); certified component vendors supply ~70–80% of AAR parts, margins ~20–30%, and tech wages rose 8–12% CAGR to 2025. GATX mitigates via 50+ service centers and long-term contracts, trimming lifecycle costs ~10–15%.

| Metric | Value |

|---|---|

| OEM concentration (2024) | ~60% |

| Lead times (2024) | 9–14 months |

| HRC change (2024) | +18% |

| Component vendor share | 70–80% |

| Vendor margins | 20–30% |

| Tech wage CAGR to 2025 | 8–12% |

| GATX service centers (2025) | 50+ |

| Lifecycle cost reduction | 10–15% |

What is included in the product

Tailored Porter's Five Forces analysis for GATX that uncovers competitive drivers, supplier and buyer power, entry barriers, substitute threats, and strategic levers shaping its freight railcar leasing and asset management profitability.

Concise Porter's Five Forces summary tailored to GATX—ideal for rapid strategic decisions and slide-ready presentation.

Customers Bargaining Power

Concentration of Major Shippers

Major shippers in chemicals, petroleum, and food—each moving millions of tons annually—drive GATX fleet utilization; top 20 customers account for roughly 45% of lease revenue, giving them heavy leverage.

Because high-volume contracts directly impact GATX utilization and 2024–2025 quarterly utilization hovered near 90%, these customers extract favorable lease rates and longer terms.

By late 2025, large shippers increasingly demanded integrated digital tracking and analytics; GATX reported rising investments in telematics after customer-led pilots in 2024.

Availability of Alternative Leasing Options

Customers can lease from GATX, rival lessors, or buy fleets outright, and with U.S. railcar lease rates averaging about $1,200–$1,800 per month in 2024, price sensitivity is high.

Market transparency—online rate listings and brokers—lets customers compare offers quickly, forcing GATX to match or beat competitor pricing.

To retain business, GATX must demonstrate higher uptime and newer fleets; GATX reported a 2024 fleet utilization near 92%, a selling point versus older competitors.

Lease Term Lengths and Renewals

The bargaining power of customers is limited by multi-year railcar leases—GATX reported average lease terms around 5–7 years in 2024—so buyers are locked into rates and specs during the contract.

Customers exert leverage mainly at initial negotiation or renewal, but mid-term switching costs and asset specificity reduce practical power.

By 2025, 28% of new contracts include flexible clauses (pay-per-use, early return), reflecting growing demand for demand-linked terms.

Switching Costs and Operational Integration

GATX faces moderate customer bargaining power because switching large fleets is logistically complex; replacing 1,000+ railcars can take months and cost millions in reconfiguration and downtime. GATX embeds assets into shippers’ operations—20–40% of cycle costs can be tied to asset integration—so mid-lease price pressure is limited. Operational stickiness thus protects GATX from aggressive mid-cycle concessions.

- Large fleet swaps: months, $mn costs

- Integration share: 20–40% of cycle costs

- Mid-lease leverage: low for customers

Impact of Rail Traffic Volatility

In 2025, customer bargaining swings with rail freight health: U.S. rail carload volumes fell 3.8% year‑over‑year in 2024, so lessees gained leverage and GATX faced pricing pressure as lessors scrambled to lease idle cars.

When volumes rise—US carloadings up 2.1% in Q1 2025—GATX reclaims power because compliant, well-maintained railcars are scarce and critical to shipper uptime, allowing higher lease rates.

- Low traffic: excess capacity → lower lease rates

- High traffic: scarce compliant cars → higher rates

- 2024: −3.8% carloads; Q1 2025: +2.1%

Top shippers hold sway short-term; leases mute pressure, renewals risk leverage

Large shippers (top 20 ≈45% revenue) hold moderate bargaining power: multi‑year leases (avg 5–7 yrs in 2024) and integration costs (20–40% cycle) limit mid‑term pressure, but volume swings (US carloads −3.8% in 2024, Q1 2025 +2.1%) and online price transparency increase leverage at renewals.

| Metric | Value |

|---|---|

| Top‑20 revenue | ≈45% |

| Avg lease term (2024) | 5–7 yrs |

| Integration cost | 20–40% |

| US carloads 2024 | −3.8% |

| US carloads Q1 2025 | +2.1% |

Full Version Awaits

GATX Porter's Five Forces Analysis

This preview shows the exact GATX Porter's Five Forces analysis you'll receive after purchase—no placeholders or samples, fully formatted and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

GATX operates in a capital-intensive railcar leasing market where supplier power is moderate, buyer negotiations are strong with large industrial clients, and rivalry centers on fleet scale and service differentiation; regulatory and technological shifts add external pressure. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore GATX’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Railcar Manufacturers

The new-railcar market is concentrated: Trinity Industries and The Greenbrier Company together held about 60% of North American railcar shipments in 2024, limiting GATX’s price leverage and pushing purchase premiums near 8–12% above historical averages.

These manufacturers set capacity for specialized tank and freight cars, so GATX often accepts market-driven lead times—averaging 9–14 months in 2024—and pays order premiums to secure slots.

By late 2025 consolidation (several smaller yards closed; two mid‑tier exits) strengthened supplier bargaining power, raising replacement-cycle costs for large lessors like GATX.

Raw Material Price Volatility

Suppliers of steel and precision parts face global commodity swings; benchmark hot-rolled coil rose ~18% in 2024 and remained ~12% above 2019 levels by Dec 2025, keeping supplier leverage high. GATX uses scale to negotiate discounts—fleet purchases cut unit steel cost ~5–8% in recent deals—but high-grade alloy and machined components prices are largely exogenous. Inflation in industrial materials (PPI for metals +9% y/y in 2025) sustains supplier bargaining power.

Specialized Component Dependency

Modern railcars need sophisticated braking systems, telematics, and safety valves made by a small set of niche suppliers; roughly 70–80% of AAR (Association of American Railroads)–certified components come from top 5 vendors, limiting substitution.

Because components must meet strict AAR standards, GATX faces high switching costs and long qualification cycles (often 6–18 months), so it cannot easily use lower‑cost providers.

This supplier concentration gives certified component makers significant pricing power; industry reports show specialty supplier margins near 20–30%, pressuring GATX’s maintenance and assembly costs.

Labor Market Constraints

Suppliers of maintenance, repair, and specialized railcar manufacturing labor have gained bargaining power due to skill shortages, pushing certified technician wages up ~8–12% CAGR through 2025 and increasing service costs for GATX.

GATX depends on these labor-intensive services to keep a 120,000+ railcar fleet compliant with FRA safety rules, so rising hourly rates forced GATX into longer, pricier contracts with key technical partners.

- Certified tech wage growth: 8–12% CAGR to 2025

- GATX fleet: 120,000+ railcars

- Higher long-term contracts: increased fixed servicing costs

Strategic Partnerships and Vertical Integration

GATX limits supplier power via long-term contracts and in-house maintenance; as of 2025 the company operates over 50 service centers, cutting third-party repair spend and lowering lifecycle costs by an estimated 10–15% per carload car compared with outsourced peers.

This vertical integration hedges against independent providers’ pricing swings and secures component availability, supporting higher asset utilization and predictable maintenance capex.

- 50+ service centers (2025)

- 10–15% lifecycle cost reduction

- Long-term supply agreements reduce volatility

High supplier power vs GATX scale: long lead times, rising costs, but 10–15% lifecycle cuts

Supplier power is high: two OEMs held ~60% of 2024 NA shipments, lead times 9–14 months, and steel HRC +18% in 2024 (still +12% vs 2019); certified component vendors supply ~70–80% of AAR parts, margins ~20–30%, and tech wages rose 8–12% CAGR to 2025. GATX mitigates via 50+ service centers and long-term contracts, trimming lifecycle costs ~10–15%.

| Metric | Value |

|---|---|

| OEM concentration (2024) | ~60% |

| Lead times (2024) | 9–14 months |

| HRC change (2024) | +18% |

| Component vendor share | 70–80% |

| Vendor margins | 20–30% |

| Tech wage CAGR to 2025 | 8–12% |

| GATX service centers (2025) | 50+ |

| Lifecycle cost reduction | 10–15% |

What is included in the product

Tailored Porter's Five Forces analysis for GATX that uncovers competitive drivers, supplier and buyer power, entry barriers, substitute threats, and strategic levers shaping its freight railcar leasing and asset management profitability.

Concise Porter's Five Forces summary tailored to GATX—ideal for rapid strategic decisions and slide-ready presentation.

Customers Bargaining Power

Concentration of Major Shippers

Major shippers in chemicals, petroleum, and food—each moving millions of tons annually—drive GATX fleet utilization; top 20 customers account for roughly 45% of lease revenue, giving them heavy leverage.

Because high-volume contracts directly impact GATX utilization and 2024–2025 quarterly utilization hovered near 90%, these customers extract favorable lease rates and longer terms.

By late 2025, large shippers increasingly demanded integrated digital tracking and analytics; GATX reported rising investments in telematics after customer-led pilots in 2024.

Availability of Alternative Leasing Options

Customers can lease from GATX, rival lessors, or buy fleets outright, and with U.S. railcar lease rates averaging about $1,200–$1,800 per month in 2024, price sensitivity is high.

Market transparency—online rate listings and brokers—lets customers compare offers quickly, forcing GATX to match or beat competitor pricing.

To retain business, GATX must demonstrate higher uptime and newer fleets; GATX reported a 2024 fleet utilization near 92%, a selling point versus older competitors.

Lease Term Lengths and Renewals

The bargaining power of customers is limited by multi-year railcar leases—GATX reported average lease terms around 5–7 years in 2024—so buyers are locked into rates and specs during the contract.

Customers exert leverage mainly at initial negotiation or renewal, but mid-term switching costs and asset specificity reduce practical power.

By 2025, 28% of new contracts include flexible clauses (pay-per-use, early return), reflecting growing demand for demand-linked terms.

Switching Costs and Operational Integration

GATX faces moderate customer bargaining power because switching large fleets is logistically complex; replacing 1,000+ railcars can take months and cost millions in reconfiguration and downtime. GATX embeds assets into shippers’ operations—20–40% of cycle costs can be tied to asset integration—so mid-lease price pressure is limited. Operational stickiness thus protects GATX from aggressive mid-cycle concessions.

- Large fleet swaps: months, $mn costs

- Integration share: 20–40% of cycle costs

- Mid-lease leverage: low for customers

Impact of Rail Traffic Volatility

In 2025, customer bargaining swings with rail freight health: U.S. rail carload volumes fell 3.8% year‑over‑year in 2024, so lessees gained leverage and GATX faced pricing pressure as lessors scrambled to lease idle cars.

When volumes rise—US carloadings up 2.1% in Q1 2025—GATX reclaims power because compliant, well-maintained railcars are scarce and critical to shipper uptime, allowing higher lease rates.

- Low traffic: excess capacity → lower lease rates

- High traffic: scarce compliant cars → higher rates

- 2024: −3.8% carloads; Q1 2025: +2.1%

Top shippers hold sway short-term; leases mute pressure, renewals risk leverage

Large shippers (top 20 ≈45% revenue) hold moderate bargaining power: multi‑year leases (avg 5–7 yrs in 2024) and integration costs (20–40% cycle) limit mid‑term pressure, but volume swings (US carloads −3.8% in 2024, Q1 2025 +2.1%) and online price transparency increase leverage at renewals.

| Metric | Value |

|---|---|

| Top‑20 revenue | ≈45% |

| Avg lease term (2024) | 5–7 yrs |

| Integration cost | 20–40% |

| US carloads 2024 | −3.8% |

| US carloads Q1 2025 | +2.1% |

Full Version Awaits

GATX Porter's Five Forces Analysis

This preview shows the exact GATX Porter's Five Forces analysis you'll receive after purchase—no placeholders or samples, fully formatted and ready to use.