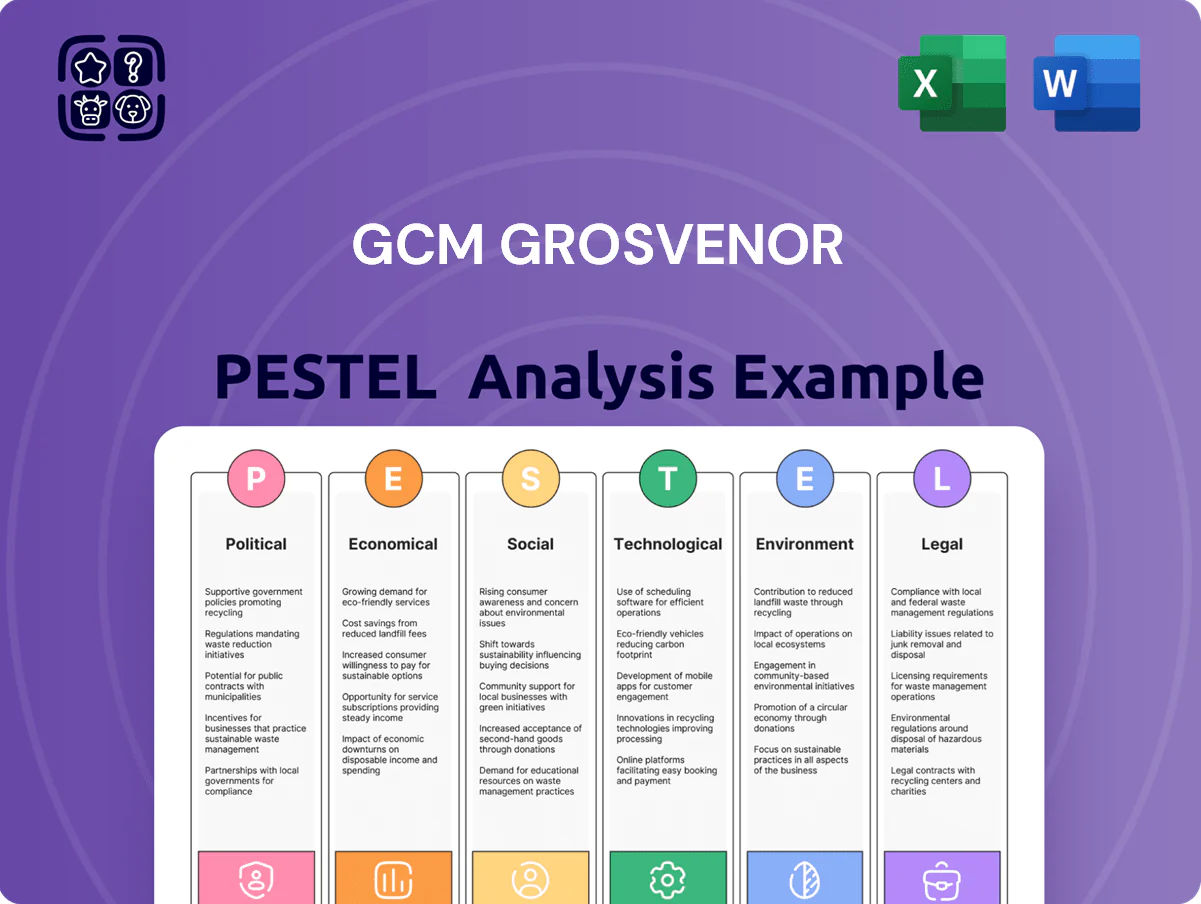

GCM Grosvenor PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how regulatory shifts, macroeconomic cycles, and technological innovation are reshaping GCM Grosvenor’s growth and risk profile—our concise PESTLE highlights the key external drivers you need to know; purchase the full analysis for an exhaustive, ready-to-use report that powers smarter investment and strategy decisions.

Political factors

Geopolitical instability and trade tensions

Ongoing geopolitical conflicts and trade tensions—such as the 2024 US-China tariff escalations and Russia-Ukraine spillovers—can divert global capital flows, with cross-border M&A activity down about 15% in 2024 and FX volatility up roughly 28%, pressuring valuations of international assets.

GCM Grosvenor, managing over $80 billion AUM (2025 figure), must recalibrate regional exposures and liquidity buffers as it spans North America, Europe and Asia.

Political instability spikes market volatility—VIX averaged ~20 in 2024 versus 14 pre-2020—necessitating enhanced hedging and scenario-based risk management to protect client capital.

U.S. tax policy and fiscal shifts

Changes in U.S. corporate tax rates or carried interest rules directly affect after-tax returns for alternatives; a 5 percentage-point rise in corporate tax could reduce fund-level distributions materially, while carried interest reform could reclassify billions in carried gains. As a public firm with $55.1bn AUM (2024), GCM Grosvenor is exposed to legislative shifts that can change private equity and real estate fund economics and investor appetite. Analysts track federal budget priorities—e.g., FY2025 proposals—to forecast sector-specific tax credits or increased burdens impacting dealflow and fee revenue.

Government infrastructure spending initiatives

Political moves to nationalize or subsidize infrastructure have expanded deployment opportunities for GCM Grosvenor’s infrastructure funds; for example, US federal infrastructure packages directed roughly 1.2 trillion USD toward physical and clean energy projects through 2026, increasing deal flow for institutional investors.

Global regulatory harmonization efforts

Political pressure for standardized financial reporting and cross-border investment rules shapes GCM Grosvenor’s operations in Europe and Asia; in 2024, EU-Asia regulatory dialogues targeted harmonization of AIFMD-like rules and investor disclosure standards impacting over $70bn in firm-controlled assets across the regions.

Divergent political agendas on transparency—evidenced by 2024 variances in beneficial ownership and tax reporting regimes—increase compliance costs for global asset managers, raising estimated annual compliance spend by 5–12% for multi-jurisdictional firms.

The firm must maintain strong relationships with international regulators to secure seamless market access, engaging in industry consultations and regulatory sandboxes to protect distribution channels responsible for a significant portion of cross-border fundraising.

- EU-Asia harmonization affects $70bn+ regional AUM exposure

- Compliance costs up 5–12% for multi-jurisdiction operations

- Active regulator engagement preserves cross-border fundraising

Pension fund reform and public mandates

Decisions by state and local governments over public pension management affect GCM Grosvenor’s client base—US public pensions held roughly $6.5 trillion in assets in 2024, making policy shifts material to mandate flows.

Political moves favoring ESG mandates vs. anti-ESG legislation (passed in 15+ US states by 2024) force GCM Grosvenor to design highly customized portfolios to retain mandates across jurisdictions.

Successfully navigating conflicting political pressures is essential to secure and maintain large-scale institutional mandates, often worth hundreds of millions per client.

- ~$6.5tn US public pension assets (2024)

- 15+ US states with anti-ESG measures (by 2024)

- Mandates often sized in hundreds of millions

GCM Grosvenor: Rising FX, M&A Drag Force Rebalance, Liquidity & Compliance Push

Geopolitical tensions (US-China tariffs, Russia-Ukraine) raised FX volatility ~28% and cut cross-border M&A ~15% in 2024, pressuring valuations; GCM Grosvenor (reported $55.1bn AUM in 2024; firm-wide >$80bn by 2025) must rebalance regional exposure, increase liquidity and hedging, monitor tax/carried interest reforms, and manage rising compliance costs (+5–12%) across jurisdictions.

| Metric | 2024/2025 |

|---|---|

| AUM | $55.1bn (2024); >$80bn (2025) |

| Cross-border M&A | -15% (2024) |

| FX volatility | +28% (2024) |

| Compliance cost rise | +5–12% |

What is included in the product

Explores how external macro-environmental factors uniquely affect GCM Grosvenor across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE summary for GCM Grosvenor that fits directly into presentations or planning decks, enabling fast alignment across teams and easy annotation for region- or business-specific notes.

Economic factors

Interest rate environment and monetary policy

The trajectory of central bank rates drives leverage costs and DCF discount rates; the US Fed funds rate moved from a peak of 5.25–5.50% in 2023–24 toward stabilization around 5.00% by late 2025, compressing spreads and lifting asset valuations.

Lower volatility in rates to late 2025 has tightened private credit yields to mid/high single digits and pushed prime real estate cap rates down ~75–150 bps versus 2022–23 peaks, altering return expectations.

GCM Grosvenor must raise or flex investment hurdle rates above prevailing 10-year UST yields (~4.0% in late 2025) and recalibrate leverage targets to stay competitive versus risk-free benchmarks and institutional peers.

Global inflationary pressures

Persistent global inflation—CPI averaging 5.8% in advanced economies and 8.3% in emerging markets in 2024—raises operating costs for GCM Grosvenor portfolio companies and compresses real investor returns.

Alternative assets like infrastructure and real estate have outpaced inflation, with global REITs delivering a 10.2% nominal return in 2023, acting as partial hedges by passing through higher costs.

GCM Grosvenor targets acquisitions with strong pricing power—evidenced by rent escalations and regulated tariff structures—preserving margins and protecting real value against rising consumer prices.

Capital market volatility and liquidity

Fluctuations in public equity markets—S&P 500 volatility index rising ~40% in 2022 and still elevated in 2024—compress valuations for private holdings and delay IPOs/secondaries, reducing exit multiples; tightening credit spreads (US IG spread widened to ~160 bps in 2023) raises financing costs and slows deal activity; GCM Grosvenor’s diversified multi-asset platform, managing ~$85 billion AUM in 2024, helps mitigate localized downturns by spreading risk across strategies and geographies.

Currency exchange rate fluctuations

As a global manager, GCM Grosvenor faces currency risk when repatriating returns to USD; a 10% USD appreciation vs EUR in 2022 cut Euro-denominated reported returns materially for many firms.

Significant dollar moves against the euro or yen—USD up ~8% vs EUR and ~15% vs JPY between 2021–2023—can swing reported performance of global portfolios.

Grosvenor employs hedging (forwards, options, cross-currency swaps) to reduce volatility and target more predictable USD cash flows; industry hedging rates vary but many managers hedge 50–100% of FX exposure.

- Exposure when repatriating to USD

- USD moves (≈+8% vs EUR, +15% vs JPY, 2021–2023) affect reported returns

- Hedging via forwards/options/swaps to stabilize cash flows

- Typical hedge ratios range 50–100%

Emerging market growth trajectories

Economic expansion in developing regions—with IMF 2025 GDP growth forecasts of 4.6% for emerging markets versus 2.9% for advanced economies—drives high-growth private equity and credit opportunities for GCM Grosvenor.

Higher volatility and sovereign risk (EM bond spreads averaged ~350 bps in 2024) require rigorous scenario stress-testing and country-specific credit analysis.

GCM Grosvenor targets allocations to high-alpha EM sectors by evaluating regional macro-trends, capital flows, and real rates to optimize risk-adjusted returns.

- IMF 2025 EM growth 4.6% vs advanced 2.9%

- EM bond spreads ~350 bps in 2024

- Allocation driven by macro, flows, real rates

Central bank tightening, mid-single-digit private credit yields and EM-driven alpha

Central bank tightening raised discount rates—US fed funds ~5.0% by late 2025—compressing private credit yields to mid/high single digits and cutting real estate cap rates ~75–150 bps vs 2022–23; CPI averaged 5.8% (adv) / 8.3% (EM) in 2024, pressuring margins; GCM Grosvenor AUM ~$85bn (2024) uses hedging (50–100%) to manage FX and targets EM growth (IMF 2025: 4.6%) for alpha.

| Metric | Value |

|---|---|

| Fed funds (late 2025) | ~5.0% |

| CPI (2024 adv/EM) | 5.8% / 8.3% |

| Grosvenor AUM (2024) | $85bn |

| EM GDP (IMF 2025) | 4.6% |

What You See Is What You Get

GCM Grosvenor PESTLE Analysis

The preview shown here is the exact GCM Grosvenor PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how regulatory shifts, macroeconomic cycles, and technological innovation are reshaping GCM Grosvenor’s growth and risk profile—our concise PESTLE highlights the key external drivers you need to know; purchase the full analysis for an exhaustive, ready-to-use report that powers smarter investment and strategy decisions.

Political factors

Geopolitical instability and trade tensions

Ongoing geopolitical conflicts and trade tensions—such as the 2024 US-China tariff escalations and Russia-Ukraine spillovers—can divert global capital flows, with cross-border M&A activity down about 15% in 2024 and FX volatility up roughly 28%, pressuring valuations of international assets.

GCM Grosvenor, managing over $80 billion AUM (2025 figure), must recalibrate regional exposures and liquidity buffers as it spans North America, Europe and Asia.

Political instability spikes market volatility—VIX averaged ~20 in 2024 versus 14 pre-2020—necessitating enhanced hedging and scenario-based risk management to protect client capital.

U.S. tax policy and fiscal shifts

Changes in U.S. corporate tax rates or carried interest rules directly affect after-tax returns for alternatives; a 5 percentage-point rise in corporate tax could reduce fund-level distributions materially, while carried interest reform could reclassify billions in carried gains. As a public firm with $55.1bn AUM (2024), GCM Grosvenor is exposed to legislative shifts that can change private equity and real estate fund economics and investor appetite. Analysts track federal budget priorities—e.g., FY2025 proposals—to forecast sector-specific tax credits or increased burdens impacting dealflow and fee revenue.

Government infrastructure spending initiatives

Political moves to nationalize or subsidize infrastructure have expanded deployment opportunities for GCM Grosvenor’s infrastructure funds; for example, US federal infrastructure packages directed roughly 1.2 trillion USD toward physical and clean energy projects through 2026, increasing deal flow for institutional investors.

Global regulatory harmonization efforts

Political pressure for standardized financial reporting and cross-border investment rules shapes GCM Grosvenor’s operations in Europe and Asia; in 2024, EU-Asia regulatory dialogues targeted harmonization of AIFMD-like rules and investor disclosure standards impacting over $70bn in firm-controlled assets across the regions.

Divergent political agendas on transparency—evidenced by 2024 variances in beneficial ownership and tax reporting regimes—increase compliance costs for global asset managers, raising estimated annual compliance spend by 5–12% for multi-jurisdictional firms.

The firm must maintain strong relationships with international regulators to secure seamless market access, engaging in industry consultations and regulatory sandboxes to protect distribution channels responsible for a significant portion of cross-border fundraising.

- EU-Asia harmonization affects $70bn+ regional AUM exposure

- Compliance costs up 5–12% for multi-jurisdiction operations

- Active regulator engagement preserves cross-border fundraising

Pension fund reform and public mandates

Decisions by state and local governments over public pension management affect GCM Grosvenor’s client base—US public pensions held roughly $6.5 trillion in assets in 2024, making policy shifts material to mandate flows.

Political moves favoring ESG mandates vs. anti-ESG legislation (passed in 15+ US states by 2024) force GCM Grosvenor to design highly customized portfolios to retain mandates across jurisdictions.

Successfully navigating conflicting political pressures is essential to secure and maintain large-scale institutional mandates, often worth hundreds of millions per client.

- ~$6.5tn US public pension assets (2024)

- 15+ US states with anti-ESG measures (by 2024)

- Mandates often sized in hundreds of millions

GCM Grosvenor: Rising FX, M&A Drag Force Rebalance, Liquidity & Compliance Push

Geopolitical tensions (US-China tariffs, Russia-Ukraine) raised FX volatility ~28% and cut cross-border M&A ~15% in 2024, pressuring valuations; GCM Grosvenor (reported $55.1bn AUM in 2024; firm-wide >$80bn by 2025) must rebalance regional exposure, increase liquidity and hedging, monitor tax/carried interest reforms, and manage rising compliance costs (+5–12%) across jurisdictions.

| Metric | 2024/2025 |

|---|---|

| AUM | $55.1bn (2024); >$80bn (2025) |

| Cross-border M&A | -15% (2024) |

| FX volatility | +28% (2024) |

| Compliance cost rise | +5–12% |

What is included in the product

Explores how external macro-environmental factors uniquely affect GCM Grosvenor across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE summary for GCM Grosvenor that fits directly into presentations or planning decks, enabling fast alignment across teams and easy annotation for region- or business-specific notes.

Economic factors

Interest rate environment and monetary policy

The trajectory of central bank rates drives leverage costs and DCF discount rates; the US Fed funds rate moved from a peak of 5.25–5.50% in 2023–24 toward stabilization around 5.00% by late 2025, compressing spreads and lifting asset valuations.

Lower volatility in rates to late 2025 has tightened private credit yields to mid/high single digits and pushed prime real estate cap rates down ~75–150 bps versus 2022–23 peaks, altering return expectations.

GCM Grosvenor must raise or flex investment hurdle rates above prevailing 10-year UST yields (~4.0% in late 2025) and recalibrate leverage targets to stay competitive versus risk-free benchmarks and institutional peers.

Global inflationary pressures

Persistent global inflation—CPI averaging 5.8% in advanced economies and 8.3% in emerging markets in 2024—raises operating costs for GCM Grosvenor portfolio companies and compresses real investor returns.

Alternative assets like infrastructure and real estate have outpaced inflation, with global REITs delivering a 10.2% nominal return in 2023, acting as partial hedges by passing through higher costs.

GCM Grosvenor targets acquisitions with strong pricing power—evidenced by rent escalations and regulated tariff structures—preserving margins and protecting real value against rising consumer prices.

Capital market volatility and liquidity

Fluctuations in public equity markets—S&P 500 volatility index rising ~40% in 2022 and still elevated in 2024—compress valuations for private holdings and delay IPOs/secondaries, reducing exit multiples; tightening credit spreads (US IG spread widened to ~160 bps in 2023) raises financing costs and slows deal activity; GCM Grosvenor’s diversified multi-asset platform, managing ~$85 billion AUM in 2024, helps mitigate localized downturns by spreading risk across strategies and geographies.

Currency exchange rate fluctuations

As a global manager, GCM Grosvenor faces currency risk when repatriating returns to USD; a 10% USD appreciation vs EUR in 2022 cut Euro-denominated reported returns materially for many firms.

Significant dollar moves against the euro or yen—USD up ~8% vs EUR and ~15% vs JPY between 2021–2023—can swing reported performance of global portfolios.

Grosvenor employs hedging (forwards, options, cross-currency swaps) to reduce volatility and target more predictable USD cash flows; industry hedging rates vary but many managers hedge 50–100% of FX exposure.

- Exposure when repatriating to USD

- USD moves (≈+8% vs EUR, +15% vs JPY, 2021–2023) affect reported returns

- Hedging via forwards/options/swaps to stabilize cash flows

- Typical hedge ratios range 50–100%

Emerging market growth trajectories

Economic expansion in developing regions—with IMF 2025 GDP growth forecasts of 4.6% for emerging markets versus 2.9% for advanced economies—drives high-growth private equity and credit opportunities for GCM Grosvenor.

Higher volatility and sovereign risk (EM bond spreads averaged ~350 bps in 2024) require rigorous scenario stress-testing and country-specific credit analysis.

GCM Grosvenor targets allocations to high-alpha EM sectors by evaluating regional macro-trends, capital flows, and real rates to optimize risk-adjusted returns.

- IMF 2025 EM growth 4.6% vs advanced 2.9%

- EM bond spreads ~350 bps in 2024

- Allocation driven by macro, flows, real rates

Central bank tightening, mid-single-digit private credit yields and EM-driven alpha

Central bank tightening raised discount rates—US fed funds ~5.0% by late 2025—compressing private credit yields to mid/high single digits and cutting real estate cap rates ~75–150 bps vs 2022–23; CPI averaged 5.8% (adv) / 8.3% (EM) in 2024, pressuring margins; GCM Grosvenor AUM ~$85bn (2024) uses hedging (50–100%) to manage FX and targets EM growth (IMF 2025: 4.6%) for alpha.

| Metric | Value |

|---|---|

| Fed funds (late 2025) | ~5.0% |

| CPI (2024 adv/EM) | 5.8% / 8.3% |

| Grosvenor AUM (2024) | $85bn |

| EM GDP (IMF 2025) | 4.6% |

What You See Is What You Get

GCM Grosvenor PESTLE Analysis

The preview shown here is the exact GCM Grosvenor PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.