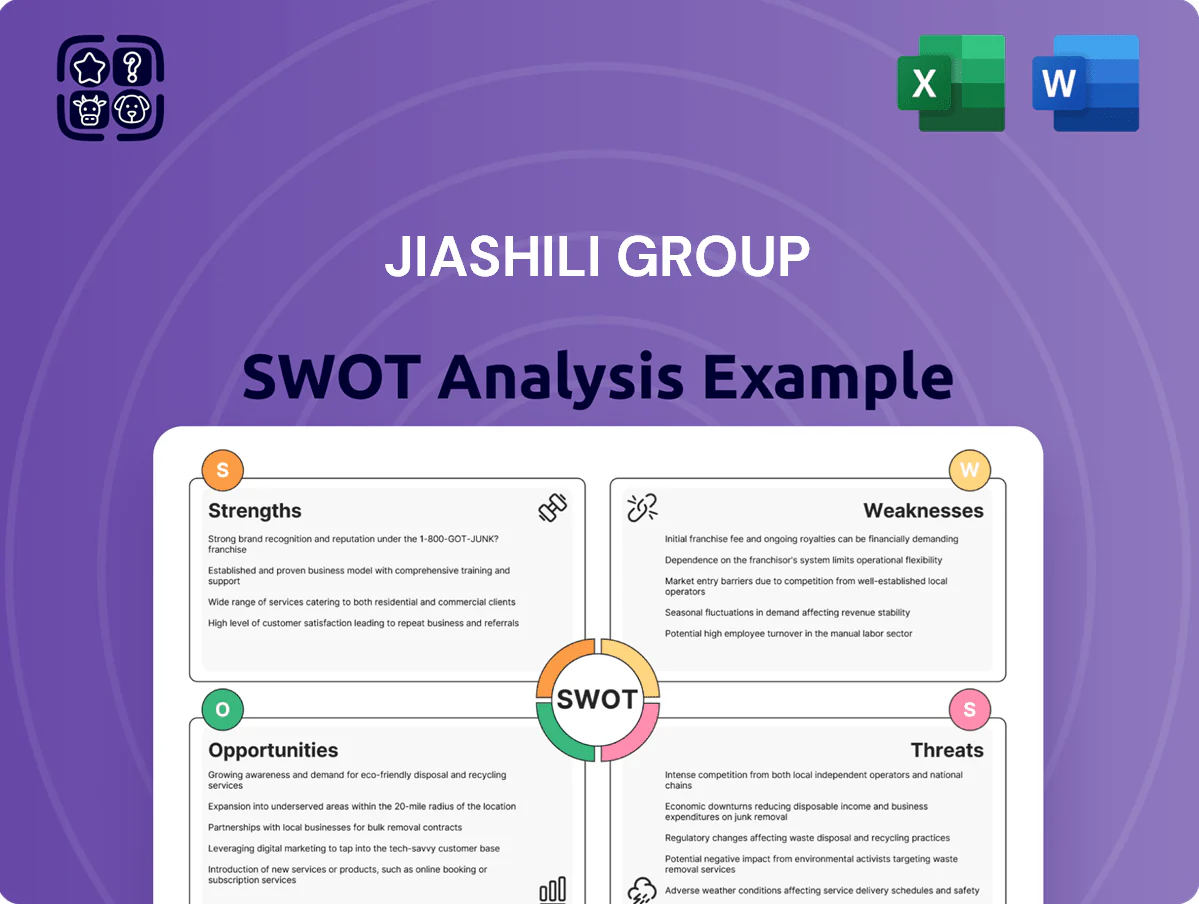

Jiashili Group SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Jiashili Group shows strong upstream integration and resilient domestic demand, but faces margin pressure from rising input costs and intensifying competition; its growth hinges on scale-driven efficiencies and geographic expansion. Discover the complete picture behind the company’s market position with our full SWOT analysis—an actionable, fully editable report with expert commentary, Word + Excel deliverables to support investment, strategy, and pitch-ready planning.

Strengths

Extensive National Distribution Network

Jiashili operates through over 450,000 sales outlets across all 31 provinces and 310 prefecture-level cities in China, giving it unmatched reach into lower-tier cities and rural areas where modern retail lags. This deep-channel penetration boosts SKU availability and repeat purchase rates among mass-market shoppers; Nielsen retail audits (2024) show rural FMCG outlets still account for ~38% of national packaged food volume. The blend of distributors and direct retail ties keeps shelf share high and logistics costs per outlet low.

Established Brand Heritage and Market Leadership

Founded in 1956, Jiashili Group is one of China’s oldest biscuit brands, with nearly 70 years of consumer trust and brand recognition that boosts repeat purchase rates (estimated 45%+ among core urban households in 2024).

As a leading manufacturer, Jiashili’s annual production capacity exceeds 100,000 tons, supporting national distribution and a market share of roughly 12–15% in the cracker and sandwich biscuit segments (2024 retail data).

This entrenched reputation and scale create a clear competitive moat versus newer entrants, underpinning its positioning as a reliable household name and aiding pricing resilience during 2023–24 inflationary pressure.

Diversified Multi-Brand Product Portfolio

Jiashili Group has expanded beyond its flagship Jiashili brand by acquiring and growing Silang, Kangli, and Jusber, creating a multi-brand portfolio that covered 28% of domestic biscuit market value in 2024 per company filings. This strategy lets the group address price tiers from low-cost crackers to premium cookies, where premium SKUs grew 14% YoY in 2024. Diversification lowers revenue concentration risk—flagship brand revenue fell to 62% of group sales in 2024 from 74% in 2019—while matching shifting tastes across age and income segments.

High-Tech Manufacturing and R&D Capabilities

Recognized as a High-New Technology Enterprise in Guangdong, Jiashili secures a reduced 15% Enterprise Income Tax rate and reinvests roughly RMB 120–150 million annually (2024) into production automation and R&D, accelerating product innovation and IP filings.

Their advanced manufacturing upgrades raised automated line throughput by about 28% year-over-year (2023–2024) while cutting defect rates to under 0.8%, preserving consistent quality at scale.

Process refinement and R&D integration lower unit costs and support rapid new-product cycles, strengthening market responsiveness and margin resilience.

- 15% preferential tax rate

- RMB 120–150M annual R&D/automation spend (2024)

- +28% automated throughput (2023–24)

- <0.8% defect rate

- Faster product cycles, lower unit costs

Resilient Revenue Growth Amid Economic Headwinds

Jiashili reported ~6.9% revenue growth in 2024, reaching RMB 1.80 billion, showing resilience despite weak retail spending.

The increase reflects the defensive demand for affordable, convenient snacks and the group’s ability to manage shifting consumer sentiment and channel mix.

The accessible price points and wide distribution keep volumes steady during cautious spending periods.

- 2024 revenue RMB 1.80 billion (+6.9%)

- Defensive product category—snacks

- Focus: accessible, convenient, affordable

Jiashili: 450k stores, RMB1.8bn revenue — rural reach & 28% automation lift

Jiashili’s 450,000+ outlets across all 31 provinces and deep rural reach drive stable volume; rural outlets still ~38% of packaged food volume (Nielsen 2024). Nearly 70-year brand history supports ~45%+ repeat purchase in core urban households (2024). 2024 revenue RMB 1.80bn (+6.9%) with 12–15% segment share and 28% automated throughput gain (2023–24) cut defect <0.8%.

| Metric | 2024 / Note |

|---|---|

| Outlets | 450,000+ |

| Rural share (packaged food) | ~38% (Nielsen 2024) |

| Revenue | RMB 1.80bn (+6.9%) |

| Segment share | 12–15% |

| Repeat rate (urban) | ~45%+ |

| R&D/automation spend | RMB 120–150M |

| Throughput gain | +28% (2023–24) |

| Defect rate | <0.8% |

What is included in the product

Provides a concise SWOT overview of Jiashili Group, highlighting its core strengths, operational weaknesses, market opportunities, and external threats shaping strategic decisions.

Provides a concise SWOT matrix for Jiashili Group, enabling quick identification of strategic priorities and pain-point relief for executives and planners.

Weaknesses

Deteriorating Liquidity and Working Capital Pressure

As of mid-2025 Jiashili Group reported net current liabilities of about RMB 92.9 million, reflecting a marked deterioration in short-term finances.

The current ratio fell below 1.0, indicating current assets are insufficient to cover current liabilities and raising default risk on near-term obligations.

This liquidity squeeze reduces financial flexibility, constrains working capital for operations, and may slow responses to sudden market shifts or urgent investment needs.

Declining Profit Margins Due to Input Costs

The group’s gross profit margin contracted from nearly 30% in 2023 to about 26.4% in early 2025, driven mainly by higher costs for flour, sugar, and palm oil that Jiashili has struggled to fully pass to price-sensitive consumers. As a result, net profit attributable to owners fell by double-digit percentages year-over-year, reflecting earnings pressure; e.g., adjusted net profit declined roughly 12–18% across fiscal 2024–2025. This exposes Jiashili to commodity price volatility and margin compression risks.

Heavy Reliance on the Traditional Biscuit Segment

Over 67% of Jiashili Group’s revenue came from biscuits in FY2024, leaving the firm exposed to a single-category shock; China’s biscuit market grew ~2% in 2023 vs. 8% for total snacks, so slower category growth risks margin pressure.

Because biscuits dominate sales, a 1–3% decline in biscuit volume would cut overall revenue by ~0.7–2.0 percentage points, hitting EBITDA more than for a diversified snack peer; diversification progress remains gradual.

Underdeveloped International Revenue Contribution

Despite launching the Kasháy brand for overseas growth, international sales were only about 9% of Jiashili Group’s RMB 18.6 billion revenue in 2024, leaving 91% tied to China.

This heavy domestic concentration raises exposure to Chinese regulatory shifts, tariff or subsidy changes, and a potential local demand slowdown without a sizable global revenue buffer.

- International sales ~9% of RMB 18.6bn (2024)

- Kasháy brand still early-stage abroad

- 91% revenue from China—high country risk

- Limited hedge vs Chinese macro or regulatory shocks

Lagging Presence in Premium Health-Conscious Segments

Jiashili’s brand remains seen as traditional mass-market despite moves into healthier SKUs, so consumer willingness to pay in tier-1 cities lags competitors.

Clean-label and functional snack brands grew 28% CAGR in China’s wellness segment 2019–2024, capturing higher gross margins (35–45% vs Jiashili’s ~22% in 2024).

Slower product reformulation and premium marketing mean Jiashili often misses early-mover pricing and distribution advantages.

- Brand perception tied to mass-market

- Wellness brands: 28% CAGR (2019–2024)

- Competitor gross margins 35–45% vs Jiashili ~22% (2024)

- Late entry → lost early-mover premium pricing

Jiashili faces liquidity strain, margin squeeze and heavy reliance on biscuits, low export mix

Jiashili shows weak short-term liquidity (net current liabilities ~RMB 92.9m; current ratio <1.0), margin pressure (gross margin ~26.4% in early 2025; adjusted net profit down ~12–18% YoY), high product concentration (biscuits 67% of FY2024 revenue) and low international diversification (Kasháy: ~9% of RMB 18.6bn 2024 revenue).

| Metric | Value |

|---|---|

| Net current liabilities | RMB 92.9m |

| Current ratio | <1.0 |

| Gross margin (early 2025) | 26.4% |

| Biscuits revenue share (FY2024) | 67% |

| International sales (2024) | 9% of RMB 18.6bn |

Preview Before You Purchase

Jiashili Group SWOT Analysis

This is the actual Jiashili Group SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth, editable version.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Jiashili Group shows strong upstream integration and resilient domestic demand, but faces margin pressure from rising input costs and intensifying competition; its growth hinges on scale-driven efficiencies and geographic expansion. Discover the complete picture behind the company’s market position with our full SWOT analysis—an actionable, fully editable report with expert commentary, Word + Excel deliverables to support investment, strategy, and pitch-ready planning.

Strengths

Extensive National Distribution Network

Jiashili operates through over 450,000 sales outlets across all 31 provinces and 310 prefecture-level cities in China, giving it unmatched reach into lower-tier cities and rural areas where modern retail lags. This deep-channel penetration boosts SKU availability and repeat purchase rates among mass-market shoppers; Nielsen retail audits (2024) show rural FMCG outlets still account for ~38% of national packaged food volume. The blend of distributors and direct retail ties keeps shelf share high and logistics costs per outlet low.

Established Brand Heritage and Market Leadership

Founded in 1956, Jiashili Group is one of China’s oldest biscuit brands, with nearly 70 years of consumer trust and brand recognition that boosts repeat purchase rates (estimated 45%+ among core urban households in 2024).

As a leading manufacturer, Jiashili’s annual production capacity exceeds 100,000 tons, supporting national distribution and a market share of roughly 12–15% in the cracker and sandwich biscuit segments (2024 retail data).

This entrenched reputation and scale create a clear competitive moat versus newer entrants, underpinning its positioning as a reliable household name and aiding pricing resilience during 2023–24 inflationary pressure.

Diversified Multi-Brand Product Portfolio

Jiashili Group has expanded beyond its flagship Jiashili brand by acquiring and growing Silang, Kangli, and Jusber, creating a multi-brand portfolio that covered 28% of domestic biscuit market value in 2024 per company filings. This strategy lets the group address price tiers from low-cost crackers to premium cookies, where premium SKUs grew 14% YoY in 2024. Diversification lowers revenue concentration risk—flagship brand revenue fell to 62% of group sales in 2024 from 74% in 2019—while matching shifting tastes across age and income segments.

High-Tech Manufacturing and R&D Capabilities

Recognized as a High-New Technology Enterprise in Guangdong, Jiashili secures a reduced 15% Enterprise Income Tax rate and reinvests roughly RMB 120–150 million annually (2024) into production automation and R&D, accelerating product innovation and IP filings.

Their advanced manufacturing upgrades raised automated line throughput by about 28% year-over-year (2023–2024) while cutting defect rates to under 0.8%, preserving consistent quality at scale.

Process refinement and R&D integration lower unit costs and support rapid new-product cycles, strengthening market responsiveness and margin resilience.

- 15% preferential tax rate

- RMB 120–150M annual R&D/automation spend (2024)

- +28% automated throughput (2023–24)

- <0.8% defect rate

- Faster product cycles, lower unit costs

Resilient Revenue Growth Amid Economic Headwinds

Jiashili reported ~6.9% revenue growth in 2024, reaching RMB 1.80 billion, showing resilience despite weak retail spending.

The increase reflects the defensive demand for affordable, convenient snacks and the group’s ability to manage shifting consumer sentiment and channel mix.

The accessible price points and wide distribution keep volumes steady during cautious spending periods.

- 2024 revenue RMB 1.80 billion (+6.9%)

- Defensive product category—snacks

- Focus: accessible, convenient, affordable

Jiashili: 450k stores, RMB1.8bn revenue — rural reach & 28% automation lift

Jiashili’s 450,000+ outlets across all 31 provinces and deep rural reach drive stable volume; rural outlets still ~38% of packaged food volume (Nielsen 2024). Nearly 70-year brand history supports ~45%+ repeat purchase in core urban households (2024). 2024 revenue RMB 1.80bn (+6.9%) with 12–15% segment share and 28% automated throughput gain (2023–24) cut defect <0.8%.

| Metric | 2024 / Note |

|---|---|

| Outlets | 450,000+ |

| Rural share (packaged food) | ~38% (Nielsen 2024) |

| Revenue | RMB 1.80bn (+6.9%) |

| Segment share | 12–15% |

| Repeat rate (urban) | ~45%+ |

| R&D/automation spend | RMB 120–150M |

| Throughput gain | +28% (2023–24) |

| Defect rate | <0.8% |

What is included in the product

Provides a concise SWOT overview of Jiashili Group, highlighting its core strengths, operational weaknesses, market opportunities, and external threats shaping strategic decisions.

Provides a concise SWOT matrix for Jiashili Group, enabling quick identification of strategic priorities and pain-point relief for executives and planners.

Weaknesses

Deteriorating Liquidity and Working Capital Pressure

As of mid-2025 Jiashili Group reported net current liabilities of about RMB 92.9 million, reflecting a marked deterioration in short-term finances.

The current ratio fell below 1.0, indicating current assets are insufficient to cover current liabilities and raising default risk on near-term obligations.

This liquidity squeeze reduces financial flexibility, constrains working capital for operations, and may slow responses to sudden market shifts or urgent investment needs.

Declining Profit Margins Due to Input Costs

The group’s gross profit margin contracted from nearly 30% in 2023 to about 26.4% in early 2025, driven mainly by higher costs for flour, sugar, and palm oil that Jiashili has struggled to fully pass to price-sensitive consumers. As a result, net profit attributable to owners fell by double-digit percentages year-over-year, reflecting earnings pressure; e.g., adjusted net profit declined roughly 12–18% across fiscal 2024–2025. This exposes Jiashili to commodity price volatility and margin compression risks.

Heavy Reliance on the Traditional Biscuit Segment

Over 67% of Jiashili Group’s revenue came from biscuits in FY2024, leaving the firm exposed to a single-category shock; China’s biscuit market grew ~2% in 2023 vs. 8% for total snacks, so slower category growth risks margin pressure.

Because biscuits dominate sales, a 1–3% decline in biscuit volume would cut overall revenue by ~0.7–2.0 percentage points, hitting EBITDA more than for a diversified snack peer; diversification progress remains gradual.

Underdeveloped International Revenue Contribution

Despite launching the Kasháy brand for overseas growth, international sales were only about 9% of Jiashili Group’s RMB 18.6 billion revenue in 2024, leaving 91% tied to China.

This heavy domestic concentration raises exposure to Chinese regulatory shifts, tariff or subsidy changes, and a potential local demand slowdown without a sizable global revenue buffer.

- International sales ~9% of RMB 18.6bn (2024)

- Kasháy brand still early-stage abroad

- 91% revenue from China—high country risk

- Limited hedge vs Chinese macro or regulatory shocks

Lagging Presence in Premium Health-Conscious Segments

Jiashili’s brand remains seen as traditional mass-market despite moves into healthier SKUs, so consumer willingness to pay in tier-1 cities lags competitors.

Clean-label and functional snack brands grew 28% CAGR in China’s wellness segment 2019–2024, capturing higher gross margins (35–45% vs Jiashili’s ~22% in 2024).

Slower product reformulation and premium marketing mean Jiashili often misses early-mover pricing and distribution advantages.

- Brand perception tied to mass-market

- Wellness brands: 28% CAGR (2019–2024)

- Competitor gross margins 35–45% vs Jiashili ~22% (2024)

- Late entry → lost early-mover premium pricing

Jiashili faces liquidity strain, margin squeeze and heavy reliance on biscuits, low export mix

Jiashili shows weak short-term liquidity (net current liabilities ~RMB 92.9m; current ratio <1.0), margin pressure (gross margin ~26.4% in early 2025; adjusted net profit down ~12–18% YoY), high product concentration (biscuits 67% of FY2024 revenue) and low international diversification (Kasháy: ~9% of RMB 18.6bn 2024 revenue).

| Metric | Value |

|---|---|

| Net current liabilities | RMB 92.9m |

| Current ratio | <1.0 |

| Gross margin (early 2025) | 26.4% |

| Biscuits revenue share (FY2024) | 67% |

| International sales (2024) | 9% of RMB 18.6bn |

Preview Before You Purchase

Jiashili Group SWOT Analysis

This is the actual Jiashili Group SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth, editable version.