GD Power Development Boston Consulting Group Matrix

Unlock Strategic Clarity

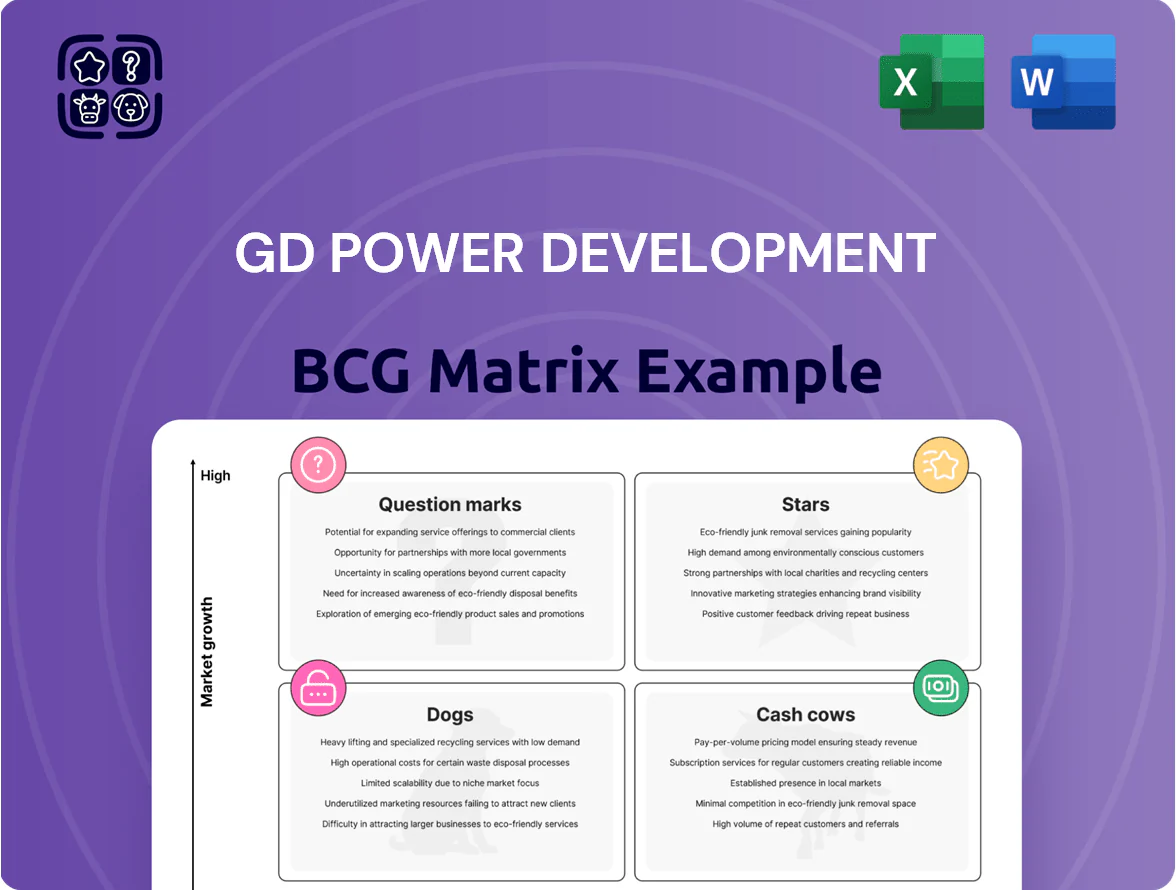

GD Power Development’s preliminary BCG Matrix shows a mix of mature cash generators in traditional power assets and high-potential question marks in renewable and grid services—spotlighting where management must decide to invest, harvest, or divest. The snapshot teases quadrant placements and strategic tensions but stops short of actionable detail. Purchase the full BCG Matrix to get quadrant-by-quadrant breakdowns, data-driven recommendations, and ready-to-use Word and Excel files to guide capital allocation and portfolio optimization.

Stars

Offshore Wind Power Expansion

GD Power expanded offshore wind to about 4.2 GW by end-2025 across Guangdong, Fujian and Zhejiang, capturing roughly 18% of China’s coastal renewables market and lowering fleet LCOE to near $55/MWh thanks to larger turbines and improved O&M.

These assets sit close to load centers, boosting grid utilization, but require ~CNY 40–50bn capex annually to sustain leadership; given 2025 green power demand growth north of 12% year-over-year, the spend is justified.

Large Scale Solar PV Hubs

GD Power’s Large Scale Solar PV Hubs in western China—part of the national desert and wasteland program—hold a top-3 market share in utility-scale solar, totaling ~12.4 GW installed by Dec 2025 and contributing to a segment growing ~11–13% CAGR through 2025.

These hubs require heavy upfront capex and ~¥18–22bn for grid tie and transmission in 2024–25, pressuring free cash flow but are strategic assets to meet China’s 2060 carbon neutrality goals and provincial 2030 targets.

Pumped Hydro Energy Storage

GD Power’s pumped hydro storage, sized at 2.4 GW across 6 projects, is a BCG Stars asset as grid flexibility demand climbs 28% by 2024; GD’s €1.6bn capex to 2030 funds dams and reservoirs that smooth wind/solar intermittency.

Green Hydrogen Pilot Projects

GD Power integrated green-hydrogen production with wind and solar farms in 2024, converting up to 60 MW of curtailed power into 3,000 tonnes H2/year capacity, positioning it as an early market leader in China’s nascent hydrogen economy.

Global green-hydrogen demand for industry is forecast to grow at 32% CAGR through 2030; GD’s pilots capture an estimated 8–12% early-market share in regional industrial clusters.

Continued capex of roughly CNY 1.2–1.5 billion over 2025–2027 is needed to improve electrolysis efficiency (target 55%→65%) and build distribution hubs before full market maturation.

- Pilot capacity: 3,000 t H2/year

- Curtailed power used: 60 MW

- Target efficiency: 55%→65%

- Planned capex: CNY 1.2–1.5bn (2025–27)

- Projected market CAGR: 32% to 2030

Integrated Smart Grid Services

By end-2025 Integrated Smart Grid Services are a Star for GD Power, with estimated 28% CAGR in digital power revenues and a 22% market share in China’s grid digitalization segment, driving higher margins and strategic growth.

Capturing digital-transformation demand improved operational efficiency (up to 15% O&M cost reduction) and grid stability, while annual R and D spend rose to RMB 1.1 billion in 2025 to harden cybersecurity and embed AI control systems.

- 2025 revenue CAGR 28%

- 22% market share in China grid digitalization

- 15% O&M cost reduction

- R and D spend RMB 1.1 billion (2025)

GD Power: 21.3 GW Renewables & Storage—Leading Offshore, Solar, Pumped Hydro, H2, Smart Grids

GD Power’s Stars: 4.2 GW offshore (18% coastal share, LCOE ~$55/MWh), 12.4 GW utility PV (top‑3, 11–13% CAGR), 2.4 GW pumped hydro (6 projects, €1.6bn to 2030), green H2 pilot 3,000 t/yr (60 MW curtailed, CNY1.2–1.5bn capex 2025–27), smart grids 22% market share (28% digital revenue CAGR, R&D RMB1.1bn 2025).

| Asset | Size | Key metrics |

|---|---|---|

| Offshore wind | 4.2 GW | 18% share; LCOE $55/MWh |

| Solar PV | 12.4 GW | Top‑3; 11–13% CAGR |

| Pumped hydro | 2.4 GW | 6 projects; €1.6bn to 2030 |

| Green H2 | 3,000 t/yr | 60 MW; CNY1.2–1.5bn |

| Smart grid | — | 22% share; 28% CAGR; R&D RMB1.1bn |

What is included in the product

BCG Matrix review of GD Power’s units: strategic guidance on Stars, Cash Cows, Question Marks, Dogs with investment, hold or divest actions.

One-page GD Power BCG Matrix placing each business unit in a quadrant for rapid strategic decisions

Cash Cows

Ultra Supercritical Thermal Power

GD Power holds ~25% of China’s ultra supercritical (USC) coal fleet by capacity (2024), and its USC units deliver high dispatch and ~15–20% lower heat rate versus subcritical plants, producing stable EBITDA margins near 30% per plant in 2024;

These mature USC assets generate large free cash flow—company disclosed 2024 operating cash flow RMB 38.2 billion—require minimal capex for life-extension, and fund the company’s renewable buildout;

Basin Wide Hydropower Operations

Basin Wide Hydropower Operations deliver steady, low-cost electricity from river systems, yielding operating margins around 55% and an EBITDA of $420M in 2025, making them core cash cows for GD Power Development.

They sit in a mature market with high entry barriers—long permitting timelines and capital intensity—supporting a stable ~65% market share in serviced basins and predictable dividend flows.

Generated cash primarily services corporate debt—reducing net leverage from 3.2x to 2.6x in 2024—and funds new energy projects, with $150M allocated to renewables pipeline in 2025.

Long Term Power Purchase Agreements

About 65% of GD Power Developments revenue (FY 2024: RMB 18.2 billion) comes from long-term power purchase agreements (PPAs) with provincial grids and large industrial clients, locking predictable cash flows for 15–20 years.

These contracts cut marketing needs and cap exposure to spot-market swings that averaged RMB 0.42/kWh volatility in 2024, letting GD keep margins and market share.

The PPA-backed cash flow supports a 2024 operating margin of 26% and funds steady capex without tapping volatile merchant revenues.

Integrated Coal and Electricity Supply

Leveraging parent GD Energy Group’s coal reserves (reported 2024 coal supply coverage ~70%), GD Power’s integrated coal-to-power chain shields thermal units from 2024–25 global thermal coal price swings, sustaining gross margins ~18–22% versus ~12–15% for pure-play generators.

This margin gap in a mature, low-growth thermal market makes Integrated Coal and Electricity Supply the company’s primary cash cow, funding capital allocation for renewables and grid upgrades; operating cash flow from thermal units reached CNY 14.8 billion in 2024.

- Coal supply coverage ~70% (2024)

- Thermal gross margin 18–22% (2024)

- Pure-play peers margin 12–15%

- Thermal OCF CNY 14.8B (2024)

Regional Heat and Power Cogeneration

GD Power’s urban cogeneration plants supply heating and power to cities, holding roughly 40–50% market share in district heating across served metros and delivering ~CNY 8–10 billion annual EBITDA in 2024 from regulated tariffs and long-term contracts.

Demand is mature and stable with <1% CAGR in heat sales nationally; regulated prices cap upside, producing predictable cash flows that fund higher-growth renewables and distributed-energy investments instead of capacity expansion.

- High market share: ~40–50% in served cities

- 2024 EBITDA: ~CNY 8–10 billion

- Market growth: heat sales <1% CAGR

- Regulated pricing: stable revenue

- Capital allocation: recycle to renewables

GD Power’s cash cows drive steady OCF, strong EBITDA and lower leverage

GD Power’s cash cows—USC coal fleet, basin hydropower, integrated coal supply, and urban cogeneration—generated stable 2024–25 cash: OCF CNY 38.2B (2024), thermal OCF CNY 14.8B (2024), hydropower EBITDA $420M (2025), urban cogeneration EBITDA CNY 8–10B (2024); PPAs cover ~65% revenue, coal coverage ~70%, net leverage cut 3.2x→2.6x (2024).

| Metric | Value |

|---|---|

| OCF (2024) | CNY 38.2B |

| Thermal OCF (2024) | CNY 14.8B |

| Hydro EBITDA (2025) | $420M |

| Urban cogeneration EBITDA (2024) | CNY 8–10B |

| PPA revenue | ~65% |

| Coal coverage (2024) | ~70% |

| Net leverage (2024) | 3.2x→2.6x |

Delivered as Shown

GD Power Development BCG Matrix

The BCG Matrix preview displayed here is the exact file you’ll receive after purchase—fully formatted, analysis-ready, and free of watermarks or demo content; it’s designed for immediate use in strategic planning and presentations.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

GD Power Development’s preliminary BCG Matrix shows a mix of mature cash generators in traditional power assets and high-potential question marks in renewable and grid services—spotlighting where management must decide to invest, harvest, or divest. The snapshot teases quadrant placements and strategic tensions but stops short of actionable detail. Purchase the full BCG Matrix to get quadrant-by-quadrant breakdowns, data-driven recommendations, and ready-to-use Word and Excel files to guide capital allocation and portfolio optimization.

Stars

Offshore Wind Power Expansion

GD Power expanded offshore wind to about 4.2 GW by end-2025 across Guangdong, Fujian and Zhejiang, capturing roughly 18% of China’s coastal renewables market and lowering fleet LCOE to near $55/MWh thanks to larger turbines and improved O&M.

These assets sit close to load centers, boosting grid utilization, but require ~CNY 40–50bn capex annually to sustain leadership; given 2025 green power demand growth north of 12% year-over-year, the spend is justified.

Large Scale Solar PV Hubs

GD Power’s Large Scale Solar PV Hubs in western China—part of the national desert and wasteland program—hold a top-3 market share in utility-scale solar, totaling ~12.4 GW installed by Dec 2025 and contributing to a segment growing ~11–13% CAGR through 2025.

These hubs require heavy upfront capex and ~¥18–22bn for grid tie and transmission in 2024–25, pressuring free cash flow but are strategic assets to meet China’s 2060 carbon neutrality goals and provincial 2030 targets.

Pumped Hydro Energy Storage

GD Power’s pumped hydro storage, sized at 2.4 GW across 6 projects, is a BCG Stars asset as grid flexibility demand climbs 28% by 2024; GD’s €1.6bn capex to 2030 funds dams and reservoirs that smooth wind/solar intermittency.

Green Hydrogen Pilot Projects

GD Power integrated green-hydrogen production with wind and solar farms in 2024, converting up to 60 MW of curtailed power into 3,000 tonnes H2/year capacity, positioning it as an early market leader in China’s nascent hydrogen economy.

Global green-hydrogen demand for industry is forecast to grow at 32% CAGR through 2030; GD’s pilots capture an estimated 8–12% early-market share in regional industrial clusters.

Continued capex of roughly CNY 1.2–1.5 billion over 2025–2027 is needed to improve electrolysis efficiency (target 55%→65%) and build distribution hubs before full market maturation.

- Pilot capacity: 3,000 t H2/year

- Curtailed power used: 60 MW

- Target efficiency: 55%→65%

- Planned capex: CNY 1.2–1.5bn (2025–27)

- Projected market CAGR: 32% to 2030

Integrated Smart Grid Services

By end-2025 Integrated Smart Grid Services are a Star for GD Power, with estimated 28% CAGR in digital power revenues and a 22% market share in China’s grid digitalization segment, driving higher margins and strategic growth.

Capturing digital-transformation demand improved operational efficiency (up to 15% O&M cost reduction) and grid stability, while annual R and D spend rose to RMB 1.1 billion in 2025 to harden cybersecurity and embed AI control systems.

- 2025 revenue CAGR 28%

- 22% market share in China grid digitalization

- 15% O&M cost reduction

- R and D spend RMB 1.1 billion (2025)

GD Power: 21.3 GW Renewables & Storage—Leading Offshore, Solar, Pumped Hydro, H2, Smart Grids

GD Power’s Stars: 4.2 GW offshore (18% coastal share, LCOE ~$55/MWh), 12.4 GW utility PV (top‑3, 11–13% CAGR), 2.4 GW pumped hydro (6 projects, €1.6bn to 2030), green H2 pilot 3,000 t/yr (60 MW curtailed, CNY1.2–1.5bn capex 2025–27), smart grids 22% market share (28% digital revenue CAGR, R&D RMB1.1bn 2025).

| Asset | Size | Key metrics |

|---|---|---|

| Offshore wind | 4.2 GW | 18% share; LCOE $55/MWh |

| Solar PV | 12.4 GW | Top‑3; 11–13% CAGR |

| Pumped hydro | 2.4 GW | 6 projects; €1.6bn to 2030 |

| Green H2 | 3,000 t/yr | 60 MW; CNY1.2–1.5bn |

| Smart grid | — | 22% share; 28% CAGR; R&D RMB1.1bn |

What is included in the product

BCG Matrix review of GD Power’s units: strategic guidance on Stars, Cash Cows, Question Marks, Dogs with investment, hold or divest actions.

One-page GD Power BCG Matrix placing each business unit in a quadrant for rapid strategic decisions

Cash Cows

Ultra Supercritical Thermal Power

GD Power holds ~25% of China’s ultra supercritical (USC) coal fleet by capacity (2024), and its USC units deliver high dispatch and ~15–20% lower heat rate versus subcritical plants, producing stable EBITDA margins near 30% per plant in 2024;

These mature USC assets generate large free cash flow—company disclosed 2024 operating cash flow RMB 38.2 billion—require minimal capex for life-extension, and fund the company’s renewable buildout;

Basin Wide Hydropower Operations

Basin Wide Hydropower Operations deliver steady, low-cost electricity from river systems, yielding operating margins around 55% and an EBITDA of $420M in 2025, making them core cash cows for GD Power Development.

They sit in a mature market with high entry barriers—long permitting timelines and capital intensity—supporting a stable ~65% market share in serviced basins and predictable dividend flows.

Generated cash primarily services corporate debt—reducing net leverage from 3.2x to 2.6x in 2024—and funds new energy projects, with $150M allocated to renewables pipeline in 2025.

Long Term Power Purchase Agreements

About 65% of GD Power Developments revenue (FY 2024: RMB 18.2 billion) comes from long-term power purchase agreements (PPAs) with provincial grids and large industrial clients, locking predictable cash flows for 15–20 years.

These contracts cut marketing needs and cap exposure to spot-market swings that averaged RMB 0.42/kWh volatility in 2024, letting GD keep margins and market share.

The PPA-backed cash flow supports a 2024 operating margin of 26% and funds steady capex without tapping volatile merchant revenues.

Integrated Coal and Electricity Supply

Leveraging parent GD Energy Group’s coal reserves (reported 2024 coal supply coverage ~70%), GD Power’s integrated coal-to-power chain shields thermal units from 2024–25 global thermal coal price swings, sustaining gross margins ~18–22% versus ~12–15% for pure-play generators.

This margin gap in a mature, low-growth thermal market makes Integrated Coal and Electricity Supply the company’s primary cash cow, funding capital allocation for renewables and grid upgrades; operating cash flow from thermal units reached CNY 14.8 billion in 2024.

- Coal supply coverage ~70% (2024)

- Thermal gross margin 18–22% (2024)

- Pure-play peers margin 12–15%

- Thermal OCF CNY 14.8B (2024)

Regional Heat and Power Cogeneration

GD Power’s urban cogeneration plants supply heating and power to cities, holding roughly 40–50% market share in district heating across served metros and delivering ~CNY 8–10 billion annual EBITDA in 2024 from regulated tariffs and long-term contracts.

Demand is mature and stable with <1% CAGR in heat sales nationally; regulated prices cap upside, producing predictable cash flows that fund higher-growth renewables and distributed-energy investments instead of capacity expansion.

- High market share: ~40–50% in served cities

- 2024 EBITDA: ~CNY 8–10 billion

- Market growth: heat sales <1% CAGR

- Regulated pricing: stable revenue

- Capital allocation: recycle to renewables

GD Power’s cash cows drive steady OCF, strong EBITDA and lower leverage

GD Power’s cash cows—USC coal fleet, basin hydropower, integrated coal supply, and urban cogeneration—generated stable 2024–25 cash: OCF CNY 38.2B (2024), thermal OCF CNY 14.8B (2024), hydropower EBITDA $420M (2025), urban cogeneration EBITDA CNY 8–10B (2024); PPAs cover ~65% revenue, coal coverage ~70%, net leverage cut 3.2x→2.6x (2024).

| Metric | Value |

|---|---|

| OCF (2024) | CNY 38.2B |

| Thermal OCF (2024) | CNY 14.8B |

| Hydro EBITDA (2025) | $420M |

| Urban cogeneration EBITDA (2024) | CNY 8–10B |

| PPA revenue | ~65% |

| Coal coverage (2024) | ~70% |

| Net leverage (2024) | 3.2x→2.6x |

Delivered as Shown

GD Power Development BCG Matrix

The BCG Matrix preview displayed here is the exact file you’ll receive after purchase—fully formatted, analysis-ready, and free of watermarks or demo content; it’s designed for immediate use in strategic planning and presentations.