General Electric Business Model Canvas

Decode GE’s Business Model Canvas: Fast, Actionable Insights for Investors & Strategists

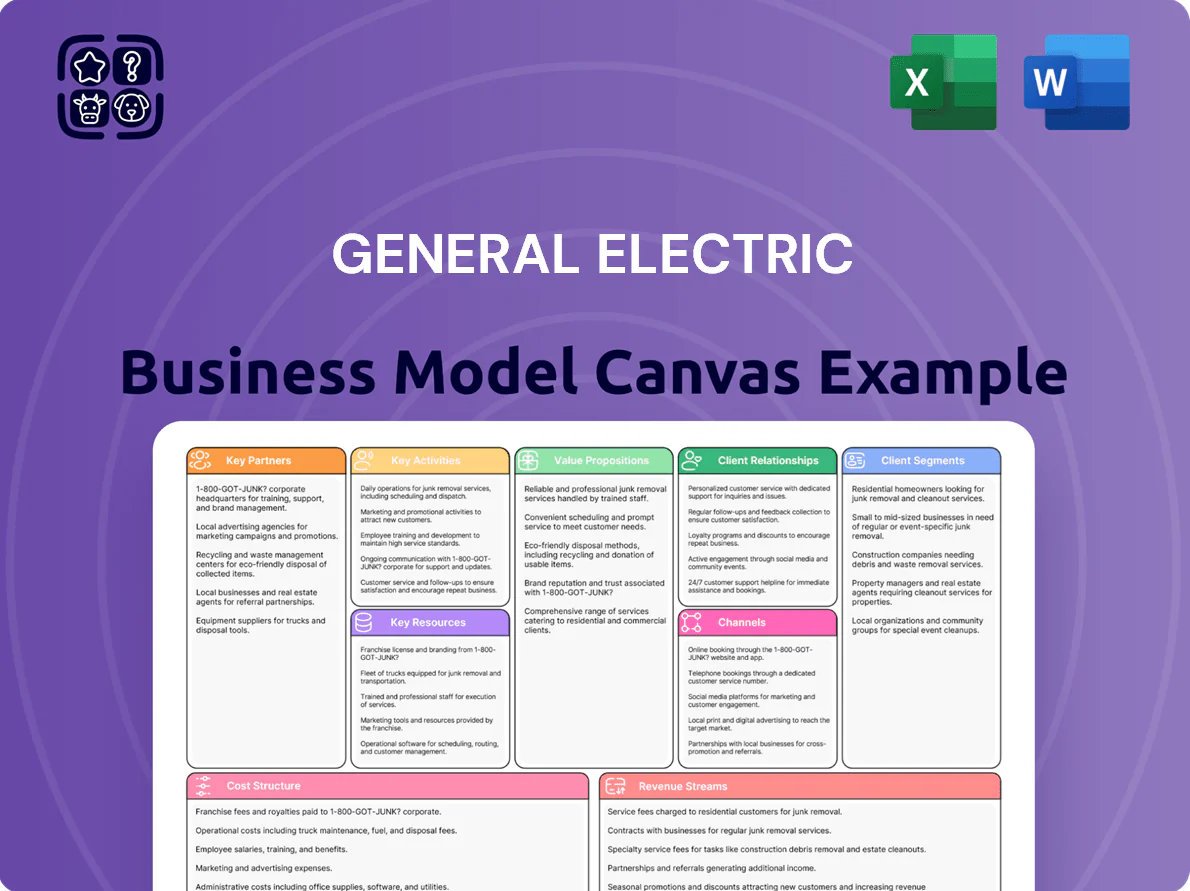

Unlock General Electric’s strategic playbook with our concise Business Model Canvas—discover how GE creates value across industrial platforms, services, and financing while managing costs and partnerships to sustain market leadership; ideal for investors, consultants, and founders seeking actionable, plug-and-play insights—download the full Word/Excel canvas to dissect each of the nine blocks and accelerate your strategic or investment analysis.

Partnerships

Strategic Joint Ventures

GE Aerospace’s Strategic Joint Ventures include CFM International, a 50-50 JV with Safran Aircraft Engines that developed the LEAP engine; LEAP engines had ~35,000 orders and backlog worth about $200 billion at end-2024, powering most narrow-body fleets and preserving GE’s market share. By sharing R&D and manufacturing risk, GE cuts development costs (LEAP program ~ $20–25B total spend estimate) and sustains dominant commercial aviation positioning.

Tier 1 Aerospace Suppliers

GE partners with dozens of Tier 1 aerospace suppliers supplying superalloys, avionics, and precision forgings; in 2024 GE Aerospace sourced ~40% of jet-engine BOM value externally, with supplier-led quality metrics cutting part defects by 22% year-over-year. These long-term contracts and dual-sourcing strategies support ramp flexibility for Boeing and Airbus programs, helping GE meet demand swings of ±25% without major lead-time breaches.

Defense and Government Agencies

GE partners with the US Department of Defense and allied militaries on propulsion R&D, including adaptive cycle engines; in 2024 GE Aerospace reported $10.8B in defense-related revenue and secured $3.2B in government contracts for advanced engines, giving multi-year procurement stability and funding that underpins national-security programs.

Maintenance and Repair Network Partners

GE partners with 120+ authorized third-party MROs in 80 countries to service ~70,000 in‑service CFM and GE engines, extending global reach and cutting AOG (aircraft on ground) response times by ~30% versus factory-only support.

- 120+ authorized MROs

- 80 countries covered

- ~70,000 in‑service engines supported

- AOG response ~30% faster with partners

Academic and Research Institutions

GE partners with top universities and national labs to co-develop materials and propulsion tech, funding over $120 million in academic research since 2020 and co-publishing 85+ papers on sustainable aviation fuel (SAF), hydrogen combustion, and carbon-fiber composites through 2024.

These ties create a talent pipeline—GE hires ~200 PhDs from partner programs annually—and accelerate net-zero aims by de‑risking technology for commercial engines and SAF scaling.

- $120M+ academic funding since 2020

- 85+ joint publications by 2024

- ~200 PhD hires/year from partners

- Focus: SAF, hydrogen combustion, carbon-fiber composites

GE Aerospace: JV scale, $200B LEAP backlog, global MRO reach, defense strength, rapid R&D

GE Aerospace leverages JVs (CFM/LEAP ~35,000 orders, $200B backlog end-2024), 120+ MROs in 80 countries (~70,000 engines serviced), ~$10.8B 2024 defense revenue with $3.2B contracts, and $120M+ academic funding since 2020 to cut R&D cost (~$20–25B LEAP) and speed SAF/hydrogen tech; hires ~200 PhDs/year.

| Partnership | Key metric |

|---|---|

| CFM/LEAP | 35,000 orders; $200B backlog |

| MRO network | 120+; 80 countries; 70,000 engines |

| Defense | $10.8B rev; $3.2B contracts |

| Academia | $120M+ funded; 200 PhDs/yr |

What is included in the product

A concise, investor-ready Business Model Canvas for General Electric covering customer segments, channels, value propositions, key activities, resources, partners, cost structure, and revenue streams with real-world alignment and SWOT-linked insights for strategic decision-making.

High-level view of General Electric’s business model with editable cells to quickly pinpoint core industrial, digital, and services value drivers for strategy, boardrooms, or investor briefings.

Activities

Advanced Propulsion R and D

GE’s Advanced propulsion R and D centers on programs like RISE (launched 2021) to cut fuel burn 20% and CO2 similarly via open-fan and hybrid-electric concepts; GE Aviation spent $5.8B on R and D in 2024 to support these architectures. Engineers target double-digit reductions in noise and 10–30% lower operating costs for airlines to meet ICAO and EU 2025–2030 emission rules.

High-Precision Manufacturing

GE manufactures jet engines and integrated propulsion systems using advanced techniques like additive manufacturing (3D printing), producing lattice and single‑piece parts that cut weight up to 20% and improve durability—GE Aviation reported 30,000 3D‑printed fuel nozzles in service by 2024 and reduced parts count by 50% on select engines.

Lifecycle Maintenance and Services

GE Aviation allocates billions yearly to lifecycle maintenance and services, managing a ~39,000-engine global fleet (2025) via health-monitoring analytics and scheduled shop visits to ensure safety; aftermarket services—over 50% gross margin on some programs—produce recurring revenue across 20–30+ year engine lifespans and drove roughly $10.5B in services revenue in 2024.

Digital Aviation Software Development

GE Aviation builds digital platforms (like FlightPulse, part of GE Digital) that analyze billions of flight-hours—GE reports 200M+ connected engine hours in 2024—to optimize routes and cut fuel burn by 1–3% per flight, saving airlines millions annually.

By fusing software with engine sensors, GE delivers predictive maintenance that reduced AOG (aircraft-on-ground) events by ~10% for customers in 2024, boosting fleet uptime and lowering maintenance costs.

- 200M+ connected engine hours (2024)

- 1–3% fuel burn reduction per flight

- ~10% fewer AOG events (2024)

- Integrates sensor data, analytics, and cockpit tools

Supply Chain and Quality Management

GE manages a global supply chain for thousands of critical engine parts, supporting ~$22B in aviation-related revenue in 2024 and ensuring production continuity across 600+ supplier sites.

Rigorous quality controls meet FAA and EASA certifications, with defect rates under 10 ppm (parts per million) in key programs, preventing bottlenecks and preserving OEM and airline trust.

- Global suppliers: 600+ sites

- 2024 aviation revenue: ~$22B

- Defect rate: <10 ppm

- Certs: FAA, EASA

GE Aerospace: $5.8B R&D, 200M+ connected hours, $10.5B services powering 39k engines

GE develops advanced propulsion R&D (RISE), manufactures 3D-printed engine parts, runs global MRO services (~39,000-engine fleet, $10.5B services revenue 2024), operates digital platforms (200M+ connected hours 2024) and manages a 600+ supplier chain to meet FAA/EASA certs and <10 ppm defect rates.

| Metric | Value |

|---|---|

| R&D spend (2024) | $5.8B |

| Services rev (2024) | $10.5B |

| Connected hours (2024) | 200M+ |

| Fleet (2025) | ~39,000 engines |

| Suppliers | 600+ sites |

| Defect rate | <10 ppm |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the exact General Electric Business Model Canvas you will receive after purchase—not a mockup or sample—and includes the same content, structure, and formatting shown here.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Decode GE’s Business Model Canvas: Fast, Actionable Insights for Investors & Strategists

Unlock General Electric’s strategic playbook with our concise Business Model Canvas—discover how GE creates value across industrial platforms, services, and financing while managing costs and partnerships to sustain market leadership; ideal for investors, consultants, and founders seeking actionable, plug-and-play insights—download the full Word/Excel canvas to dissect each of the nine blocks and accelerate your strategic or investment analysis.

Partnerships

Strategic Joint Ventures

GE Aerospace’s Strategic Joint Ventures include CFM International, a 50-50 JV with Safran Aircraft Engines that developed the LEAP engine; LEAP engines had ~35,000 orders and backlog worth about $200 billion at end-2024, powering most narrow-body fleets and preserving GE’s market share. By sharing R&D and manufacturing risk, GE cuts development costs (LEAP program ~ $20–25B total spend estimate) and sustains dominant commercial aviation positioning.

Tier 1 Aerospace Suppliers

GE partners with dozens of Tier 1 aerospace suppliers supplying superalloys, avionics, and precision forgings; in 2024 GE Aerospace sourced ~40% of jet-engine BOM value externally, with supplier-led quality metrics cutting part defects by 22% year-over-year. These long-term contracts and dual-sourcing strategies support ramp flexibility for Boeing and Airbus programs, helping GE meet demand swings of ±25% without major lead-time breaches.

Defense and Government Agencies

GE partners with the US Department of Defense and allied militaries on propulsion R&D, including adaptive cycle engines; in 2024 GE Aerospace reported $10.8B in defense-related revenue and secured $3.2B in government contracts for advanced engines, giving multi-year procurement stability and funding that underpins national-security programs.

Maintenance and Repair Network Partners

GE partners with 120+ authorized third-party MROs in 80 countries to service ~70,000 in‑service CFM and GE engines, extending global reach and cutting AOG (aircraft on ground) response times by ~30% versus factory-only support.

- 120+ authorized MROs

- 80 countries covered

- ~70,000 in‑service engines supported

- AOG response ~30% faster with partners

Academic and Research Institutions

GE partners with top universities and national labs to co-develop materials and propulsion tech, funding over $120 million in academic research since 2020 and co-publishing 85+ papers on sustainable aviation fuel (SAF), hydrogen combustion, and carbon-fiber composites through 2024.

These ties create a talent pipeline—GE hires ~200 PhDs from partner programs annually—and accelerate net-zero aims by de‑risking technology for commercial engines and SAF scaling.

- $120M+ academic funding since 2020

- 85+ joint publications by 2024

- ~200 PhD hires/year from partners

- Focus: SAF, hydrogen combustion, carbon-fiber composites

GE Aerospace: JV scale, $200B LEAP backlog, global MRO reach, defense strength, rapid R&D

GE Aerospace leverages JVs (CFM/LEAP ~35,000 orders, $200B backlog end-2024), 120+ MROs in 80 countries (~70,000 engines serviced), ~$10.8B 2024 defense revenue with $3.2B contracts, and $120M+ academic funding since 2020 to cut R&D cost (~$20–25B LEAP) and speed SAF/hydrogen tech; hires ~200 PhDs/year.

| Partnership | Key metric |

|---|---|

| CFM/LEAP | 35,000 orders; $200B backlog |

| MRO network | 120+; 80 countries; 70,000 engines |

| Defense | $10.8B rev; $3.2B contracts |

| Academia | $120M+ funded; 200 PhDs/yr |

What is included in the product

A concise, investor-ready Business Model Canvas for General Electric covering customer segments, channels, value propositions, key activities, resources, partners, cost structure, and revenue streams with real-world alignment and SWOT-linked insights for strategic decision-making.

High-level view of General Electric’s business model with editable cells to quickly pinpoint core industrial, digital, and services value drivers for strategy, boardrooms, or investor briefings.

Activities

Advanced Propulsion R and D

GE’s Advanced propulsion R and D centers on programs like RISE (launched 2021) to cut fuel burn 20% and CO2 similarly via open-fan and hybrid-electric concepts; GE Aviation spent $5.8B on R and D in 2024 to support these architectures. Engineers target double-digit reductions in noise and 10–30% lower operating costs for airlines to meet ICAO and EU 2025–2030 emission rules.

High-Precision Manufacturing

GE manufactures jet engines and integrated propulsion systems using advanced techniques like additive manufacturing (3D printing), producing lattice and single‑piece parts that cut weight up to 20% and improve durability—GE Aviation reported 30,000 3D‑printed fuel nozzles in service by 2024 and reduced parts count by 50% on select engines.

Lifecycle Maintenance and Services

GE Aviation allocates billions yearly to lifecycle maintenance and services, managing a ~39,000-engine global fleet (2025) via health-monitoring analytics and scheduled shop visits to ensure safety; aftermarket services—over 50% gross margin on some programs—produce recurring revenue across 20–30+ year engine lifespans and drove roughly $10.5B in services revenue in 2024.

Digital Aviation Software Development

GE Aviation builds digital platforms (like FlightPulse, part of GE Digital) that analyze billions of flight-hours—GE reports 200M+ connected engine hours in 2024—to optimize routes and cut fuel burn by 1–3% per flight, saving airlines millions annually.

By fusing software with engine sensors, GE delivers predictive maintenance that reduced AOG (aircraft-on-ground) events by ~10% for customers in 2024, boosting fleet uptime and lowering maintenance costs.

- 200M+ connected engine hours (2024)

- 1–3% fuel burn reduction per flight

- ~10% fewer AOG events (2024)

- Integrates sensor data, analytics, and cockpit tools

Supply Chain and Quality Management

GE manages a global supply chain for thousands of critical engine parts, supporting ~$22B in aviation-related revenue in 2024 and ensuring production continuity across 600+ supplier sites.

Rigorous quality controls meet FAA and EASA certifications, with defect rates under 10 ppm (parts per million) in key programs, preventing bottlenecks and preserving OEM and airline trust.

- Global suppliers: 600+ sites

- 2024 aviation revenue: ~$22B

- Defect rate: <10 ppm

- Certs: FAA, EASA

GE Aerospace: $5.8B R&D, 200M+ connected hours, $10.5B services powering 39k engines

GE develops advanced propulsion R&D (RISE), manufactures 3D-printed engine parts, runs global MRO services (~39,000-engine fleet, $10.5B services revenue 2024), operates digital platforms (200M+ connected hours 2024) and manages a 600+ supplier chain to meet FAA/EASA certs and <10 ppm defect rates.

| Metric | Value |

|---|---|

| R&D spend (2024) | $5.8B |

| Services rev (2024) | $10.5B |

| Connected hours (2024) | 200M+ |

| Fleet (2025) | ~39,000 engines |

| Suppliers | 600+ sites |

| Defect rate | <10 ppm |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the exact General Electric Business Model Canvas you will receive after purchase—not a mockup or sample—and includes the same content, structure, and formatting shown here.