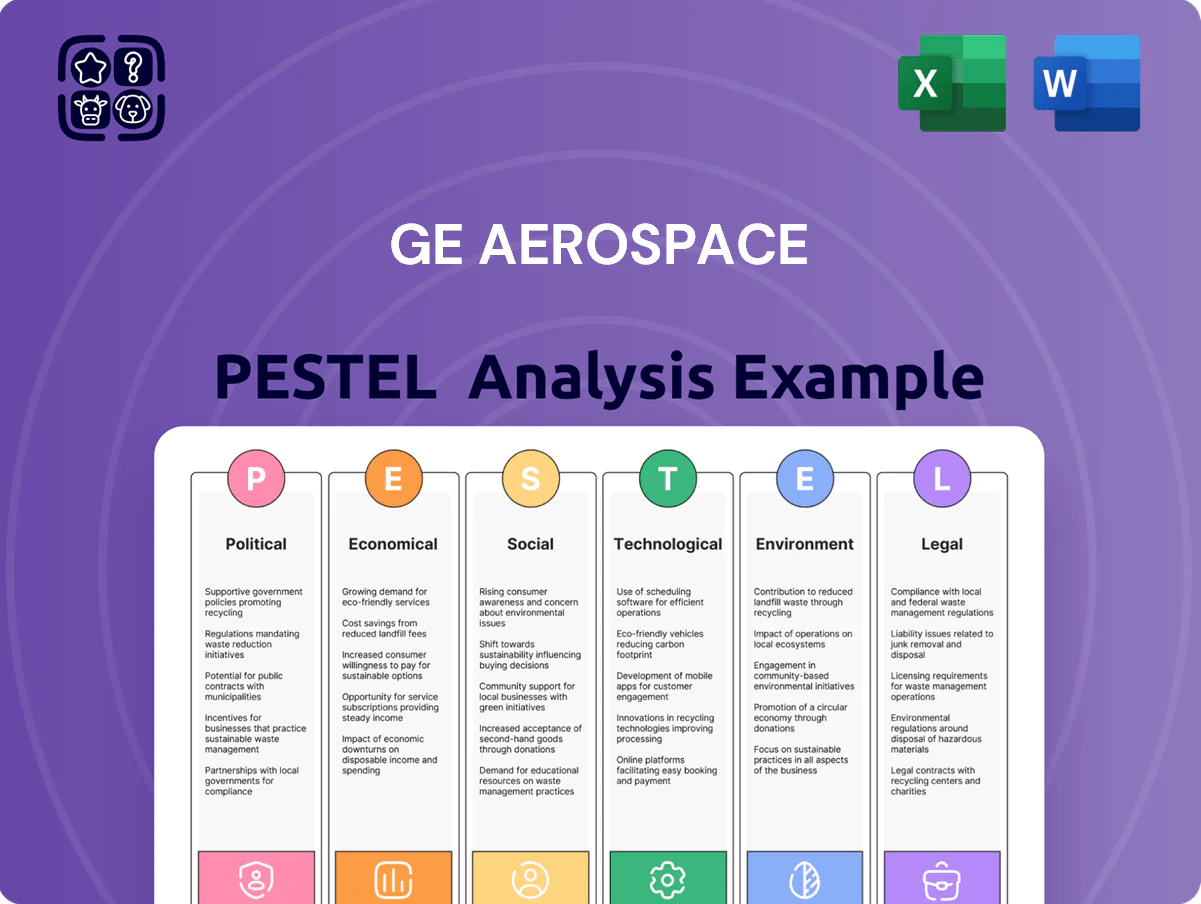

GE Aerospace PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how geopolitical shifts, supply-chain dynamics, and rapid propulsion tech advances are reshaping GE Aerospace’s competitive edge—our concise PESTLE highlights key external risks and opportunities to inform smarter decisions. Purchase the full analysis for a complete, actionable breakdown you can use in investment theses, strategy decks, or operational planning.

Political factors

Geopolitical instability and supply chain security

Ongoing regional conflicts in Europe and the Middle East as of late 2025 have increased cargo delays and raised airfreight rates by about 22% year‑over‑year, disrupting GE Aerospace’s global supply chains and logistics.

GE must navigate tightened export controls and tariffs while prioritizing resilient sourcing for specialized nickel, titanium and rare earths, which account for roughly 12% of its COGS in turbine manufacturing.

Western governments have boosted aerospace onshoring incentives—US CHIPS and Science Act follow‑ons and EU grants totaling over $30 billion in 2024–25—making domestic capacity and supplier diversification strategic imperatives for GE Aerospace.

Defense spending and national security priorities

Rising NATO and allied defense budgets—NATO members reached a combined defense spending of about $1.3 trillion in 2024—sustain demand for military propulsion and integrated systems, boosting GE Aerospace order visibility.

As a key supplier for combat aircraft and rotorcraft, GE Aerospace remains tied to U.S. DoD procurement cycles; the company reported $18.1 billion of defense-related backlog in FY2024.

Political shifts in late 2025 altering international military aid packages could materially affect long-term defense contract awards and backlog renewal rates for GE Aerospace.

Trade policies and international tariffs

Fluctuating US-China relations affect GE Aerospace exports—China accounted for about 8% of GE Aviation revenue in 2024, so tariffs or export controls could materially dent sales of LEAP and CF6 families.

Potential tariffs on aerospace parts raise input costs; a 10% tariff on engine components could erode the LEAP margin given GE Aviation’s 2024 operating margin near 9–10%.

GE must reconfigure its global footprint—over 40% of aftermarket revenues tied to international operations in 2024—shifting production and supply chains to mitigate protectionist risk.

Government subsidies for green aviation

Political pressure to reach net-zero aviation by 2050 has driven over $15 billion in global government grants for sustainable aviation since 2020, boosting GE Aerospace's access to public funding for green engine programs.

GE Aerospace leverages public-private partnerships—receiving EU Horizon and US DoE support—on hydrogen combustion and hybrid-electric tech, accelerating prototype testing and de-risking capex.

EU and North American mandates increasing SAF blend targets (EU 2% by 2025, US proposed 2025 targets under RFS/IRA incentives) push GE to scale R&D, reflected in rising sustainability R&D spend (estimated >$400m annually in 2024).

- >$15B global green aviation grants since 2020

- GE R&D >$400M/year (2024 est)

- EU SAF 2% by 2025; US incentives via IRA/RFS

- Public-private H2 and hybrid programs funded

Regulatory oversight of global aviation safety

Political scrutiny of aviation safety tightened after 2020s incidents, with FAA and EASA enforcement actions rising 18% from 2020–2024; GE Aerospace must navigate certification timelines that can shift with political appointments affecting agencies' priorities.

Strong regulator relationships are critical for RISE engines, given GE’s 2024 R&D spend of about $2.1 billion and program timelines tied to multi-year certification processes.

- FAA/EASA oversight up 18% (2020–2024)

- GE Aerospace 2024 R&D ≈ $2.1B

- Certification timelines sensitive to political appointments

- Regulatory relations crucial for RISE rollout

Supply shocks, onshoring & defense boost GE amid export risks

Geopolitical conflicts and export controls raised airfreight rates ~22% YoY and strain specialized inputs (~12% of turbine COGS), while $30B+ 2024–25 onshoring grants and $15B+ green aviation funding since 2020 shift sourcing and R&D (GE R&D ≈ $2.1B–$400M sustainability). NATO defense spend ~$1.3T (2024) and GE’s $18.1B defense backlog drive military demand; China ≈8% of revenue (2024) heightens export risk.

| Metric | Value |

|---|---|

| Airfreight ↑ | ~22% YoY |

| Specialized inputs | ~12% of COGS |

| Onshoring grants | $30B+ |

| Green grants | $15B+ |

| GE R&D | $2.1B (total); $400M (sustainability est) |

| Defense backlog | $18.1B |

| China rev | ~8% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact GE Aerospace, with each section supported by current data and sector trends to highlight risks, opportunities, and strategic implications for executives, investors, and strategists.

A concise, PESTLE-organized brief that highlights external risks and strategic opportunities for GE Aerospace, ready to drop into presentations or share across teams for fast alignment during planning and risk discussions.

Economic factors

Post-pandemic commercial aviation growth

By end-2025 global passenger traffic stabilized at or above 2019 levels, with IATA projecting 2025 RPKs roughly 3% above 2019, driving strong demand for narrow- and wide-body fleets and supporting OEM orderbacklogs. Higher flight cycles increased GE Aerospace services revenue—GE Aerospace reported services segment growth of about 10% YoY in 2024, driven by MRO and spare parts. The company leverages a massive installed base—over 70,000 commercial engines—generating recurring high-margin aftermarket sales and long-term service agreements.

Inflationary pressure on manufacturing costs

Persistent inflation in labor and specialized materials—titanium up ~18% and nickel ~22% YoY in 2024—squeezes manufacturing margins at GE Aerospace; the company reported supply-chain inflation headwinds reduced 2024 segment margins by roughly 120–150 basis points. GE offsets rising input prices via advanced lean manufacturing and digital thread adoption, targeting >5% productivity gains, and secures long-term supplier contracts to hedge commodity volatility and lock prices for key inputs.

Interest rate environment and capital expenditure

As of late 2025, global policy rates averaged near 4.5–5.0% in major markets, raising airline borrowing costs and slowing new aircraft orders; IATA reported 2025 airline net losses narrowing but with constrained capex. While GE Aerospace, post-2024 standalone spin, held net cash and improved leverage (2025 adjusted debt/EBITDA ~1.0), elevated interest rates can delay airline fleet renewals, impacting timing of GE9X and GEnx deliveries and order cyclicality.

Currency exchange rate fluctuations

As a global exporter, GE Aerospace is highly sensitive to U.S. Dollar strength; a 10% USD appreciation vs. major currencies in 2024 would have raised reported revenues by roughly $1–2 billion on constant-currency basis, squeezing competitiveness in Europe and China.

Large swings in the Euro or Yuan alter manufacturing cost relativity and aftermarket pricing; for example, EUR/USD moved ~6% in 2024 and CNY/USD about 4%, affecting margins across its global service network.

GE employs advanced hedging—FX forwards, options, and natural hedges via local sourcing—and reported hedging gains/losses neutralized an estimated $300–500 million of currency impact in 2024.

- USD sensitivity: ~10% USD move ≈ $1–2B revenue effect (2024 est.)

- Market moves: EUR ≈ 6%, CNY ≈ 4% vs USD in 2024

- Hedging offset: ~$300–500M currency impact neutralized (2024 est.)

Emerging market expansion and wealth distribution

The rising middle class in India and Southeast Asia—projected to add over 500 million people by 2030—drives sustained commercial aviation growth, boosting demand for single-aisle aircraft and engines.

Economic expansion has led to a surge in low-cost carriers (LCCs); Asia-Pacific LCC market share exceeded 55% of regional seat capacity in 2024, a key customer base for the CFM International JV.

GE Aerospace is aligning service hubs across these high-growth corridors—notably India and ASEAN—to capture aftermarket revenue growth, with regional MRO investment plans reported at over $1 billion through 2026.

- 500M new middle-class by 2030 in India/SE Asia

- Asia-Pacific LCCs >55% regional seat capacity (2024)

- CFM JV primary supplier to LCC single-aisle fleet

- GE MRO investments ~ $1B+ in region through 2026

Airline demand rebounds (+3% RPKs); input inflation, rates and USD dent margins

Economic tailwinds: 2025 RPKs ~3% above 2019 boosting narrow/wide-body demand; services +10% YoY in 2024 from higher flight cycles. Headwinds: input inflation (Ti +18%, Ni +22% in 2024) cut margins ~120–150bps; rates ~4.5–5.0% raise airline borrowing and delay orders. FX: 10% USD rise ≈ $1–2B revenue effect; hedging offset ~$300–500M (2024 est.).

| Metric | Value |

|---|---|

| 2025 RPK vs 2019 | +3% |

| Services growth 2024 | +10% |

| Titanium 2024 | +18% |

| Nickel 2024 | +22% |

| USD sensitivity | 10% ≈ $1–2B |

| Hedging 2024 | $300–500M |

Preview the Actual Deliverable

GE Aerospace PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This GE Aerospace PESTLE analysis covers political, economic, social, technological, legal, and environmental factors with actionable insights and data-driven implications. No placeholders or teasers—what you see is the final, professionally structured file available for immediate download after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how geopolitical shifts, supply-chain dynamics, and rapid propulsion tech advances are reshaping GE Aerospace’s competitive edge—our concise PESTLE highlights key external risks and opportunities to inform smarter decisions. Purchase the full analysis for a complete, actionable breakdown you can use in investment theses, strategy decks, or operational planning.

Political factors

Geopolitical instability and supply chain security

Ongoing regional conflicts in Europe and the Middle East as of late 2025 have increased cargo delays and raised airfreight rates by about 22% year‑over‑year, disrupting GE Aerospace’s global supply chains and logistics.

GE must navigate tightened export controls and tariffs while prioritizing resilient sourcing for specialized nickel, titanium and rare earths, which account for roughly 12% of its COGS in turbine manufacturing.

Western governments have boosted aerospace onshoring incentives—US CHIPS and Science Act follow‑ons and EU grants totaling over $30 billion in 2024–25—making domestic capacity and supplier diversification strategic imperatives for GE Aerospace.

Defense spending and national security priorities

Rising NATO and allied defense budgets—NATO members reached a combined defense spending of about $1.3 trillion in 2024—sustain demand for military propulsion and integrated systems, boosting GE Aerospace order visibility.

As a key supplier for combat aircraft and rotorcraft, GE Aerospace remains tied to U.S. DoD procurement cycles; the company reported $18.1 billion of defense-related backlog in FY2024.

Political shifts in late 2025 altering international military aid packages could materially affect long-term defense contract awards and backlog renewal rates for GE Aerospace.

Trade policies and international tariffs

Fluctuating US-China relations affect GE Aerospace exports—China accounted for about 8% of GE Aviation revenue in 2024, so tariffs or export controls could materially dent sales of LEAP and CF6 families.

Potential tariffs on aerospace parts raise input costs; a 10% tariff on engine components could erode the LEAP margin given GE Aviation’s 2024 operating margin near 9–10%.

GE must reconfigure its global footprint—over 40% of aftermarket revenues tied to international operations in 2024—shifting production and supply chains to mitigate protectionist risk.

Government subsidies for green aviation

Political pressure to reach net-zero aviation by 2050 has driven over $15 billion in global government grants for sustainable aviation since 2020, boosting GE Aerospace's access to public funding for green engine programs.

GE Aerospace leverages public-private partnerships—receiving EU Horizon and US DoE support—on hydrogen combustion and hybrid-electric tech, accelerating prototype testing and de-risking capex.

EU and North American mandates increasing SAF blend targets (EU 2% by 2025, US proposed 2025 targets under RFS/IRA incentives) push GE to scale R&D, reflected in rising sustainability R&D spend (estimated >$400m annually in 2024).

- >$15B global green aviation grants since 2020

- GE R&D >$400M/year (2024 est)

- EU SAF 2% by 2025; US incentives via IRA/RFS

- Public-private H2 and hybrid programs funded

Regulatory oversight of global aviation safety

Political scrutiny of aviation safety tightened after 2020s incidents, with FAA and EASA enforcement actions rising 18% from 2020–2024; GE Aerospace must navigate certification timelines that can shift with political appointments affecting agencies' priorities.

Strong regulator relationships are critical for RISE engines, given GE’s 2024 R&D spend of about $2.1 billion and program timelines tied to multi-year certification processes.

- FAA/EASA oversight up 18% (2020–2024)

- GE Aerospace 2024 R&D ≈ $2.1B

- Certification timelines sensitive to political appointments

- Regulatory relations crucial for RISE rollout

Supply shocks, onshoring & defense boost GE amid export risks

Geopolitical conflicts and export controls raised airfreight rates ~22% YoY and strain specialized inputs (~12% of turbine COGS), while $30B+ 2024–25 onshoring grants and $15B+ green aviation funding since 2020 shift sourcing and R&D (GE R&D ≈ $2.1B–$400M sustainability). NATO defense spend ~$1.3T (2024) and GE’s $18.1B defense backlog drive military demand; China ≈8% of revenue (2024) heightens export risk.

| Metric | Value |

|---|---|

| Airfreight ↑ | ~22% YoY |

| Specialized inputs | ~12% of COGS |

| Onshoring grants | $30B+ |

| Green grants | $15B+ |

| GE R&D | $2.1B (total); $400M (sustainability est) |

| Defense backlog | $18.1B |

| China rev | ~8% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact GE Aerospace, with each section supported by current data and sector trends to highlight risks, opportunities, and strategic implications for executives, investors, and strategists.

A concise, PESTLE-organized brief that highlights external risks and strategic opportunities for GE Aerospace, ready to drop into presentations or share across teams for fast alignment during planning and risk discussions.

Economic factors

Post-pandemic commercial aviation growth

By end-2025 global passenger traffic stabilized at or above 2019 levels, with IATA projecting 2025 RPKs roughly 3% above 2019, driving strong demand for narrow- and wide-body fleets and supporting OEM orderbacklogs. Higher flight cycles increased GE Aerospace services revenue—GE Aerospace reported services segment growth of about 10% YoY in 2024, driven by MRO and spare parts. The company leverages a massive installed base—over 70,000 commercial engines—generating recurring high-margin aftermarket sales and long-term service agreements.

Inflationary pressure on manufacturing costs

Persistent inflation in labor and specialized materials—titanium up ~18% and nickel ~22% YoY in 2024—squeezes manufacturing margins at GE Aerospace; the company reported supply-chain inflation headwinds reduced 2024 segment margins by roughly 120–150 basis points. GE offsets rising input prices via advanced lean manufacturing and digital thread adoption, targeting >5% productivity gains, and secures long-term supplier contracts to hedge commodity volatility and lock prices for key inputs.

Interest rate environment and capital expenditure

As of late 2025, global policy rates averaged near 4.5–5.0% in major markets, raising airline borrowing costs and slowing new aircraft orders; IATA reported 2025 airline net losses narrowing but with constrained capex. While GE Aerospace, post-2024 standalone spin, held net cash and improved leverage (2025 adjusted debt/EBITDA ~1.0), elevated interest rates can delay airline fleet renewals, impacting timing of GE9X and GEnx deliveries and order cyclicality.

Currency exchange rate fluctuations

As a global exporter, GE Aerospace is highly sensitive to U.S. Dollar strength; a 10% USD appreciation vs. major currencies in 2024 would have raised reported revenues by roughly $1–2 billion on constant-currency basis, squeezing competitiveness in Europe and China.

Large swings in the Euro or Yuan alter manufacturing cost relativity and aftermarket pricing; for example, EUR/USD moved ~6% in 2024 and CNY/USD about 4%, affecting margins across its global service network.

GE employs advanced hedging—FX forwards, options, and natural hedges via local sourcing—and reported hedging gains/losses neutralized an estimated $300–500 million of currency impact in 2024.

- USD sensitivity: ~10% USD move ≈ $1–2B revenue effect (2024 est.)

- Market moves: EUR ≈ 6%, CNY ≈ 4% vs USD in 2024

- Hedging offset: ~$300–500M currency impact neutralized (2024 est.)

Emerging market expansion and wealth distribution

The rising middle class in India and Southeast Asia—projected to add over 500 million people by 2030—drives sustained commercial aviation growth, boosting demand for single-aisle aircraft and engines.

Economic expansion has led to a surge in low-cost carriers (LCCs); Asia-Pacific LCC market share exceeded 55% of regional seat capacity in 2024, a key customer base for the CFM International JV.

GE Aerospace is aligning service hubs across these high-growth corridors—notably India and ASEAN—to capture aftermarket revenue growth, with regional MRO investment plans reported at over $1 billion through 2026.

- 500M new middle-class by 2030 in India/SE Asia

- Asia-Pacific LCCs >55% regional seat capacity (2024)

- CFM JV primary supplier to LCC single-aisle fleet

- GE MRO investments ~ $1B+ in region through 2026

Airline demand rebounds (+3% RPKs); input inflation, rates and USD dent margins

Economic tailwinds: 2025 RPKs ~3% above 2019 boosting narrow/wide-body demand; services +10% YoY in 2024 from higher flight cycles. Headwinds: input inflation (Ti +18%, Ni +22% in 2024) cut margins ~120–150bps; rates ~4.5–5.0% raise airline borrowing and delay orders. FX: 10% USD rise ≈ $1–2B revenue effect; hedging offset ~$300–500M (2024 est.).

| Metric | Value |

|---|---|

| 2025 RPK vs 2019 | +3% |

| Services growth 2024 | +10% |

| Titanium 2024 | +18% |

| Nickel 2024 | +22% |

| USD sensitivity | 10% ≈ $1–2B |

| Hedging 2024 | $300–500M |

Preview the Actual Deliverable

GE Aerospace PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This GE Aerospace PESTLE analysis covers political, economic, social, technological, legal, and environmental factors with actionable insights and data-driven implications. No placeholders or teasers—what you see is the final, professionally structured file available for immediate download after payment.