Generac PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Gain a strategic advantage with our PESTLE Analysis of Generac—unpack how political shifts, economic cycles, social trends, and technological advances are shaping its outlook and risk profile; ideal for investors and strategists seeking actionable foresight. Purchase the full report to access the complete, editable breakdown and make smarter, faster decisions.

Political factors

Federal clean energy incentives

Extension of federal tax credits through 2025, including up to 30% Investment Tax Credit for residential solar and the 26%/30% battery storage incentives, is projected to increase demand for Generac’s storage and solar products; residential solar installations rose 23% in 2024 to about 380,000 systems, expanding addressable market. Government subsidies and state rebates cut upfront costs for homeowners, improving payback and supporting Generac’s battery unit growth—company reported 2024 energy revenue up ~18%. Policies drive Generac’s strategic pivot from combustion engines to integrated energy technology, with management targeting energy segment to exceed 30% of total revenue by 2026.

Trade policy and component tariffs

Generac’s global supply chain exposes it to US trade policy shifts; in 2024 imports of steel and aluminum facing average tariffs of 25% and 10% respectively and semiconductor disruptions raised component costs by an estimated 8–12% for the industry. Tariffs and Section 301 measures can compress Generac’s 2025 gross margin (currently ~28% in FY2024) if costs cannot be passed to consumers. Management must hedge suppliers, localize sourcing, and pursue pricing to protect margins amid US-China tensions and rising protectionism.

Grid modernization and infrastructure spending

Legislative focus on grid resilience has driven US federal infrastructure allocations—Bipartisan Infrastructure Law and IIJA directed over 65 billion USD toward grid upgrades through 2025—boosting public-private partnerships where Generac can supply utility-scale backup and microgrid tech.

New mandates to harden grids against cyber and physical threats (DOE funding rising to ~9.1 billion USD in 2024 for grid security programs) create demand for Generac’s industrial backup solutions and hardened control systems.

Political pressure and state-level clean-energy targets pushing utilities to integrate distributed energy resources—rooftop solar + storage penetration up ~40% in key states by 2024—favor Generac’s decentralized power offerings and services revenue growth.

Geopolitical instability and energy security

Geopolitical conflicts since 2022 have pushed wholesale natural gas and oil price volatility—U.S. Henry Hub futures rose ~45% in 2022 and European TTF spiked over 200%—boosting political calls for energy self-sufficiency that favor on-site backup power.

With U.S. residential generator market up ~12% in 2023 and Generac holding ~70% share, policymakers’ emphasis on resilience positions Generac as a strategic supplier for home standby units and commercial microgrids.

This political backdrop supports increased federal and state funding: the 2023 Bipartisan Infrastructure Law and IRA directed billions to grid resilience, expanding demand for Generac’s distributed energy solutions.

- Energy price shocks: 2022–23 spikes drove policy focus on self-reliance

- Market share: Generac ~70% U.S. residential generator share

- Growth: U.S. residential generator market ≈ +12% in 2023

- Funding tailwinds: Infrastructure/IRA billions for resilience and microgrids

State and local backup power mandates

Increasingly frequent outages—US power outages rose 23% from 2010–2020 and major storm-related outages spiked in 2022–2024—prompted states like California, New York and Massachusetts to require backup power for nursing homes and some gas stations, creating direct demand for Generac's commercial/industrial solutions.

These localized mandates drive predictable baseline revenue: Generac reported commercial & industrial sales growth of 18% in 2024, benefiting from regulatory-driven purchases.

- Regulatory drivers: state mandates in CA, NY, MA

- Market impact: predictable baseline demand in C&I segment

- Financial signal: Generac C&I sales +18% in 2024

Tax Credits & Funding Power Solar Surge; Tariffs Threaten 2025 Margins

Federal tax credits (ITC up to 30% through 2025) and IRA/IIJA funding lifted residential solar +23% in 2024 (~380k systems) and Generac energy revenue +~18% in 2024; US tariffs (steel 25%, aluminum 10%) and component cost rises (8–12%) threaten FY2025 margins (~28% in FY2024); grid resilience funding (~$65B to 2025) and state mandates boosted C&I sales +18% in 2024.

| Metric | 2024/2025 |

|---|---|

| Residential solar installs | ~380,000 (+23% 2024) |

| Generac energy rev | +~18% 2024 |

| FY2024 gross margin | ~28% |

| C&I sales | +18% 2024 |

What is included in the product

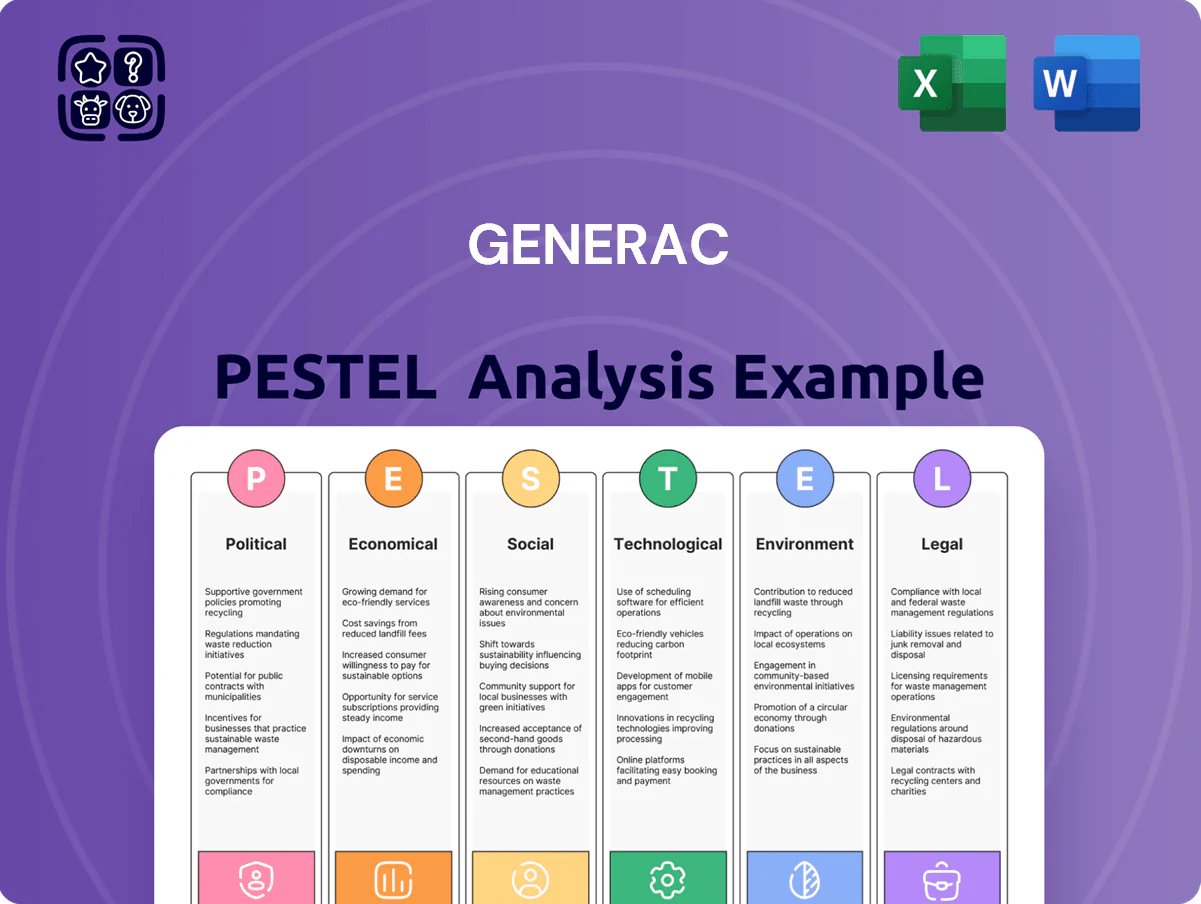

Explores how external macro-environmental factors uniquely affect Generac across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trends to highlight actionable risks and opportunities.

Concise PESTLE summary for Generac that distills regulatory, economic, social, technological, legal, and environmental factors into a single-slide-ready format for quick reference during strategy sessions or client briefings.

Economic factors

Interest rate environment and financing

Persistently high US federal funds rates—4.25–5.25% through 2025—raise borrowing costs, reducing affordability for large-scale home upgrades like Generac standby generators and battery systems; many residential purchases rely on financing, so higher APRs pressure sales volumes.

Given that consumer durable goods purchases fall as real borrowing costs rise, Generac’s revenue mix (residential ≈40% of 2024 sales) is exposed to rate-sensitive demand.

To offset this, Generac needs competitive internal financing and time-limited promotions; offering 0% APR or low-rate plans and dealer incentives can sustain conversion rates while monetary policy remains tight.

Housing market health and new construction

The US housing starts fell 6.3% year-over-year to 1.38M units in 2025, reducing near-term demand for permanent backup generators tied to new builds; existing-home turnover also slowed, with existing-home sales down 10% in 2024 vs 2023. A cooling market curbs high-end additions, whereas robust regions saw builders in 2024-25 increasingly bundle energy tech—supporting Generac, whose residential segment represented ~62% of 2024 revenue.

Raw material and commodity price volatility

Fluctuations in copper, steel and lithium — copper up ~35% and lithium carbonate up over 120% YTD in parts of 2023–2024 — materially raise Generac’s input costs for generators and energy-storage systems, pressuring margins. Economic shifts that lift commodity prices force Generac to adopt agile pricing and passed-through surcharges; product gross margin risk rose alongside commodity-driven cost inflation in FY2024. Generac’s use of hedging and multi-year supplier contracts, including disclosed supply agreements for key components, is critical to stabilize input cost exposure and protect EBITDA.

Energy price trends for consumers

- US residential electricity: 16.83 cents/kWh (2024)

- Henry Hub natural gas: ~$3.50/MMBtu (2024 average)

- Higher bills = stronger payback for solar-plus-storage; low prices = slower adoption

Labor market dynamics and installation costs

Shortages of skilled electricians and technicians create installation bottlenecks for Generac; the U.S. Bureau of Labor Statistics projects electrician employment growth of 8% through 2032 with a potential shortfall in trained installers affecting sales conversion.

Rising labor costs—average electrician wages rose ~6% year-over-year to about $31.50/hour in 2024—push total project prices higher, deterring price-sensitive buyers and compressing market demand.

Generac must increase investment in dealer training and certification; expanding programs could mitigate delays and reduce installation times, preserving revenue and customer satisfaction.

- Electrician wage ~ $31.50/hr in 2024 (≈+6% YoY)

- 8% projected job growth through 2032 (BLS)

- Dealer training investment needed to prevent sales loss

Tighter Rates, Rising Input Costs Squeeze Solar Residential Demand—Storage Gains Traction

Higher US rates (4.25–5.25% through 2025) and slowing housing (1.38M starts, -6.3% YoY) depress rate-sensitive residential demand (~40–62% of 2024 sales); commodity spikes (copper +35%, lithium carbonate +120% YTD 2023–24) and rising electrician wages (~$31.50/hr, +6% YoY) squeeze margins, while higher retail electricity (16.83¢/kWh, 2024) supports solar-plus-storage adoption.

| Metric | Value |

|---|---|

| Fed funds | 4.25–5.25% |

| Housing starts | 1.38M (-6.3% YoY) |

| Residential electricity | 16.83¢/kWh (2024) |

| Copper | +35% |

| Lithium carbonate | +120% YTD |

| Electrician wage | $31.50/hr (+6% YoY) |

Full Version Awaits

Generac PESTLE Analysis

The preview shown here is the exact Generac PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Gain a strategic advantage with our PESTLE Analysis of Generac—unpack how political shifts, economic cycles, social trends, and technological advances are shaping its outlook and risk profile; ideal for investors and strategists seeking actionable foresight. Purchase the full report to access the complete, editable breakdown and make smarter, faster decisions.

Political factors

Federal clean energy incentives

Extension of federal tax credits through 2025, including up to 30% Investment Tax Credit for residential solar and the 26%/30% battery storage incentives, is projected to increase demand for Generac’s storage and solar products; residential solar installations rose 23% in 2024 to about 380,000 systems, expanding addressable market. Government subsidies and state rebates cut upfront costs for homeowners, improving payback and supporting Generac’s battery unit growth—company reported 2024 energy revenue up ~18%. Policies drive Generac’s strategic pivot from combustion engines to integrated energy technology, with management targeting energy segment to exceed 30% of total revenue by 2026.

Trade policy and component tariffs

Generac’s global supply chain exposes it to US trade policy shifts; in 2024 imports of steel and aluminum facing average tariffs of 25% and 10% respectively and semiconductor disruptions raised component costs by an estimated 8–12% for the industry. Tariffs and Section 301 measures can compress Generac’s 2025 gross margin (currently ~28% in FY2024) if costs cannot be passed to consumers. Management must hedge suppliers, localize sourcing, and pursue pricing to protect margins amid US-China tensions and rising protectionism.

Grid modernization and infrastructure spending

Legislative focus on grid resilience has driven US federal infrastructure allocations—Bipartisan Infrastructure Law and IIJA directed over 65 billion USD toward grid upgrades through 2025—boosting public-private partnerships where Generac can supply utility-scale backup and microgrid tech.

New mandates to harden grids against cyber and physical threats (DOE funding rising to ~9.1 billion USD in 2024 for grid security programs) create demand for Generac’s industrial backup solutions and hardened control systems.

Political pressure and state-level clean-energy targets pushing utilities to integrate distributed energy resources—rooftop solar + storage penetration up ~40% in key states by 2024—favor Generac’s decentralized power offerings and services revenue growth.

Geopolitical instability and energy security

Geopolitical conflicts since 2022 have pushed wholesale natural gas and oil price volatility—U.S. Henry Hub futures rose ~45% in 2022 and European TTF spiked over 200%—boosting political calls for energy self-sufficiency that favor on-site backup power.

With U.S. residential generator market up ~12% in 2023 and Generac holding ~70% share, policymakers’ emphasis on resilience positions Generac as a strategic supplier for home standby units and commercial microgrids.

This political backdrop supports increased federal and state funding: the 2023 Bipartisan Infrastructure Law and IRA directed billions to grid resilience, expanding demand for Generac’s distributed energy solutions.

- Energy price shocks: 2022–23 spikes drove policy focus on self-reliance

- Market share: Generac ~70% U.S. residential generator share

- Growth: U.S. residential generator market ≈ +12% in 2023

- Funding tailwinds: Infrastructure/IRA billions for resilience and microgrids

State and local backup power mandates

Increasingly frequent outages—US power outages rose 23% from 2010–2020 and major storm-related outages spiked in 2022–2024—prompted states like California, New York and Massachusetts to require backup power for nursing homes and some gas stations, creating direct demand for Generac's commercial/industrial solutions.

These localized mandates drive predictable baseline revenue: Generac reported commercial & industrial sales growth of 18% in 2024, benefiting from regulatory-driven purchases.

- Regulatory drivers: state mandates in CA, NY, MA

- Market impact: predictable baseline demand in C&I segment

- Financial signal: Generac C&I sales +18% in 2024

Tax Credits & Funding Power Solar Surge; Tariffs Threaten 2025 Margins

Federal tax credits (ITC up to 30% through 2025) and IRA/IIJA funding lifted residential solar +23% in 2024 (~380k systems) and Generac energy revenue +~18% in 2024; US tariffs (steel 25%, aluminum 10%) and component cost rises (8–12%) threaten FY2025 margins (~28% in FY2024); grid resilience funding (~$65B to 2025) and state mandates boosted C&I sales +18% in 2024.

| Metric | 2024/2025 |

|---|---|

| Residential solar installs | ~380,000 (+23% 2024) |

| Generac energy rev | +~18% 2024 |

| FY2024 gross margin | ~28% |

| C&I sales | +18% 2024 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Generac across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trends to highlight actionable risks and opportunities.

Concise PESTLE summary for Generac that distills regulatory, economic, social, technological, legal, and environmental factors into a single-slide-ready format for quick reference during strategy sessions or client briefings.

Economic factors

Interest rate environment and financing

Persistently high US federal funds rates—4.25–5.25% through 2025—raise borrowing costs, reducing affordability for large-scale home upgrades like Generac standby generators and battery systems; many residential purchases rely on financing, so higher APRs pressure sales volumes.

Given that consumer durable goods purchases fall as real borrowing costs rise, Generac’s revenue mix (residential ≈40% of 2024 sales) is exposed to rate-sensitive demand.

To offset this, Generac needs competitive internal financing and time-limited promotions; offering 0% APR or low-rate plans and dealer incentives can sustain conversion rates while monetary policy remains tight.

Housing market health and new construction

The US housing starts fell 6.3% year-over-year to 1.38M units in 2025, reducing near-term demand for permanent backup generators tied to new builds; existing-home turnover also slowed, with existing-home sales down 10% in 2024 vs 2023. A cooling market curbs high-end additions, whereas robust regions saw builders in 2024-25 increasingly bundle energy tech—supporting Generac, whose residential segment represented ~62% of 2024 revenue.

Raw material and commodity price volatility

Fluctuations in copper, steel and lithium — copper up ~35% and lithium carbonate up over 120% YTD in parts of 2023–2024 — materially raise Generac’s input costs for generators and energy-storage systems, pressuring margins. Economic shifts that lift commodity prices force Generac to adopt agile pricing and passed-through surcharges; product gross margin risk rose alongside commodity-driven cost inflation in FY2024. Generac’s use of hedging and multi-year supplier contracts, including disclosed supply agreements for key components, is critical to stabilize input cost exposure and protect EBITDA.

Energy price trends for consumers

- US residential electricity: 16.83 cents/kWh (2024)

- Henry Hub natural gas: ~$3.50/MMBtu (2024 average)

- Higher bills = stronger payback for solar-plus-storage; low prices = slower adoption

Labor market dynamics and installation costs

Shortages of skilled electricians and technicians create installation bottlenecks for Generac; the U.S. Bureau of Labor Statistics projects electrician employment growth of 8% through 2032 with a potential shortfall in trained installers affecting sales conversion.

Rising labor costs—average electrician wages rose ~6% year-over-year to about $31.50/hour in 2024—push total project prices higher, deterring price-sensitive buyers and compressing market demand.

Generac must increase investment in dealer training and certification; expanding programs could mitigate delays and reduce installation times, preserving revenue and customer satisfaction.

- Electrician wage ~ $31.50/hr in 2024 (≈+6% YoY)

- 8% projected job growth through 2032 (BLS)

- Dealer training investment needed to prevent sales loss

Tighter Rates, Rising Input Costs Squeeze Solar Residential Demand—Storage Gains Traction

Higher US rates (4.25–5.25% through 2025) and slowing housing (1.38M starts, -6.3% YoY) depress rate-sensitive residential demand (~40–62% of 2024 sales); commodity spikes (copper +35%, lithium carbonate +120% YTD 2023–24) and rising electrician wages (~$31.50/hr, +6% YoY) squeeze margins, while higher retail electricity (16.83¢/kWh, 2024) supports solar-plus-storage adoption.

| Metric | Value |

|---|---|

| Fed funds | 4.25–5.25% |

| Housing starts | 1.38M (-6.3% YoY) |

| Residential electricity | 16.83¢/kWh (2024) |

| Copper | +35% |

| Lithium carbonate | +120% YTD |

| Electrician wage | $31.50/hr (+6% YoY) |

Full Version Awaits

Generac PESTLE Analysis

The preview shown here is the exact Generac PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.