Assicurazioni Generali Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

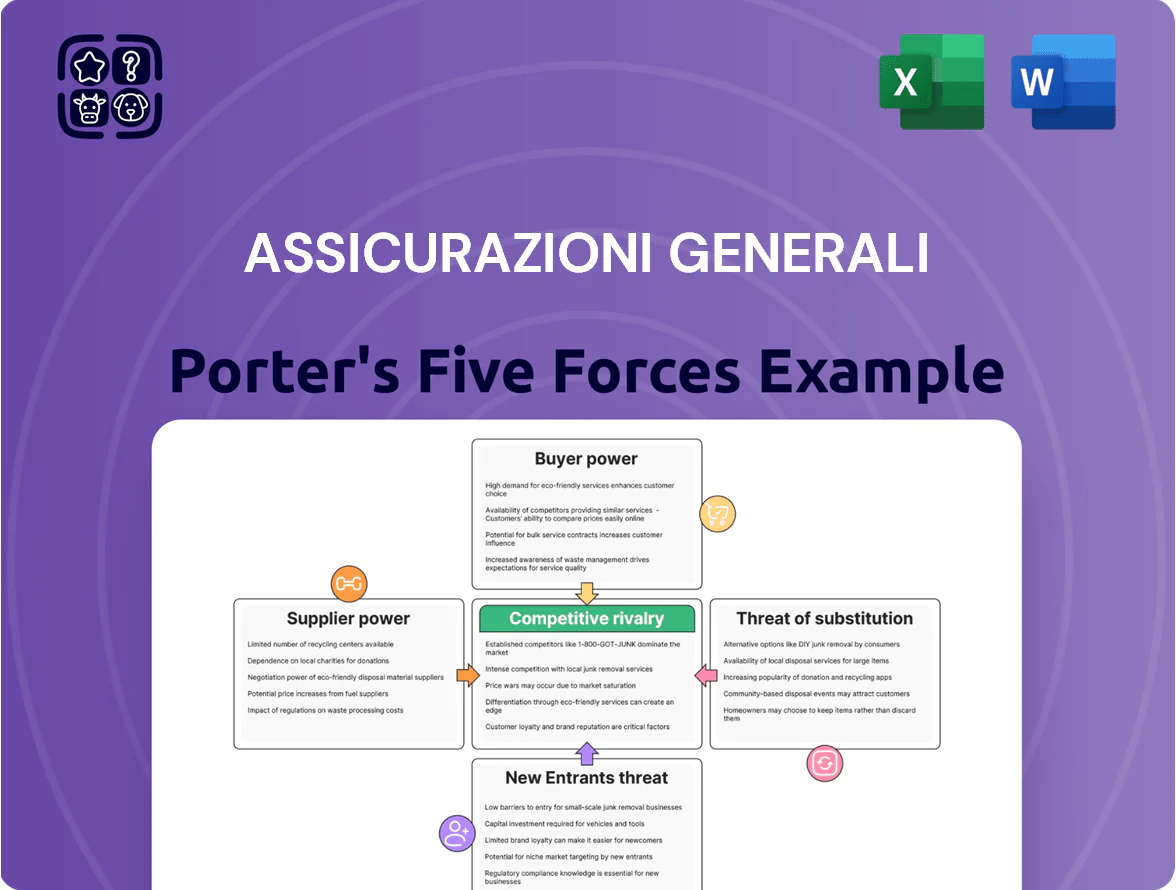

Assicurazioni Generali faces moderate buyer power, high regulatory pressure, and intense rivalry from global insurers, while digital entrants and insurtechs raise the threat of substitution; supplier power (reinsurance and capital markets) remains a key strategic variable. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Assicurazioni Generali’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration in the Reinsurance Market

Generali depends on global reinsurers such as Munich Re and Swiss Re to manage large, systemic risks; these two firms account for a large share of capacity, leaving few alternatives and raising supplier power.

By end-2025, a reinsurance hard market—reinsurance rate-on-line rises of 10–20% seen in 2023–24—would directly compress Generali’s combined ratio and margins as ceded premiums climb.

This reliance makes reinsurance pricing and availability a key supplier-driven driver of Generali’s cost of capital and risk-transfer expense, affecting solvency and earnings volatility.

Critical Dependence on Specialized IT and Cybersecurity Vendors

Generali depends on high-end software and cloud providers as insurance shifts digital; 2024 group IT spend was ~€1.2bn, raising reliance on vendors for AI underwriting and cloud ops.

Specialized firms offering AI-driven risk models and cybersecurity hold bargaining power—Gartner estimated 40% price premium for certified AI/compliance tools in 2025.

Tighter EU data rules by 2026 raise demand for compliance services, letting vendors charge premiums while Generali’s continuity hinges on these third-party tech stacks.

Scarcity of Specialized Actuarial and Data Science Talent

Human capital is central for Assicurazioni Generali; demand for actuaries and data scientists rose ~28% globally 2019–2024 while supply lagged, creating a talent gap.

Scarcity lets senior specialists and headhunters push pay premiums—median data scientist salary in Italy reached ~€60k–€85k in 2024, up ~12% year-on-year.

Generali competes with insurers, fintech and big tech for this scarce skill set, raising hiring and retention costs.

Influence of Financial Market Data Providers

Generali’s asset management and investment teams rely on real-time feeds from near-oligopoly providers such as Bloomberg, Refinitiv (Reuters), and MSCI, which in 2024 controlled ~70–80% of institutional market-data revenue, letting them charge high fees and impose restrictive licenses.

Because such data is essential for trading, risk models, and regulatory reporting (MiFID II, Solvency II), suppliers exert strong pricing power and materially affect Generali’s operational costs—vendor fees can represent low-single-digit basis points of AUM but millions of euros annually.

- ~70–80% market share among top providers (2024)

- High fixed fees and restrictive licenses

- Essential for MiFID II and Solvency II compliance

- Costs: millions EUR annually; low-single-digit bps of AUM

Impact of Regulatory Bodies as De Facto Suppliers

Regulatory authorities act as de facto suppliers by providing licenses and the legal framework essential for Generali’s operations; Solvency II rules set minimum capital and risk-margin requirements. As of late 2025, Solvency II-related capital targets push Generali to maintain Solvency II ratio near 200% (Q3 2025 reported ~198%), constraining product mix and M&A flexibility. Sudden regulatory changes can force higher capital buffers or business-model adjustments, raising cost of capital and limiting strategic moves.

- Regulatory supply: licenses, rules, oversight

- Key rule: Solvency II → capital/reserve mandates

- Q3 2025 Solvency II ratio ~198% → limited leverage

- Policy change risk → higher capital, constrained strategy

Generali squeezed by reinsurers, data oligopoly & talent costs; Solvency II caps flexibility

Generali faces high supplier power from concentrated reinsurers (Munich Re, Swiss Re), market-data oligopolies (Bloomberg, Refinitiv, MSCI ~70–80% share 2024), and scarce tech talent (Italy data-scientist median €60–85k in 2024), raising ceded-premium, vendor fees, and salary costs; Q3 2025 Solvency II ratio ~198% limits capital flexibility.

| Supplier | Key stat | Impact |

|---|---|---|

| Reinsurers | Rate-on-line +10–20% (2023–24) | Higher ceded premiums |

| Market data | 70–80% share (2024) | High fees, restrictive licenses |

| Tech talent | €60–85k median (Italy 2024) | Rising payroll |

| Regulator | SII ratio ~198% (Q3 2025) | Limits strategy |

What is included in the product

Tailored Porter’s Five Forces analysis for Assicurazioni Generali that uncovers competitive intensity, buyer and supplier power, threat of substitutes and entrants, and highlights disruptive pressures and strategic levers to protect market share and profitability.

A concise Porter's Five Forces snapshot for Assicurazioni Generali—quickly assess competitive pressure and regulatory risk to speed strategic decisions.

Customers Bargaining Power

High Price Sensitivity in Retail Insurance Segments

Individual customers in Generali’s motor and home segments are highly price-sensitive and brand-agnostic; 2024 IVASS data show price comparison usage at 62% for motor shoppers, driving churn rates above 18% annually in Italy. Digital comparison tools let consumers switch instantly to the lowest premium, with price-led online channels capturing 35% of new retail policies in 2024. This commoditization caps Generali’s pricing power—raising premiums risks immediate market-share loss given a 10–15% elasticity observed in recent studies. As a result, individual consumers wield strong bargaining power through easy comparison and migration.

Leverage of Large Corporate and Institutional Clients

Generali serves multinational corporates that supply large premium volumes—about 22% of group commercial premiums in 2024—giving them strong bargaining power.

These clients use in‑house risk managers to negotiate bespoke, low‑margin deals; Generali often concedes on pricing or terms to retain accounts tied to regional revenue targets.

The segment leverages scale to demand tailored, cost‑effective solutions, pressuring margins and pushing product customization.

Influence of Independent Brokers and Intermediaries

A large portion of Generali’s retail and SME premiums—about 45% of gross written premiums in 2024—flows through independent brokers who act as proxies for end customers, giving intermediaries directional power over insurer choice.

Brokers can steer clients via commission levels and service quality; Generali paid roughly €1.2bn in broker commissions in 2024, a lever that influences retention and new business.

Because brokers aggregate many small clients, their collective bargaining can compress margins; a 1 percentage-point cut in commission demands could reduce net combined ratio by ~0.5–1.0 pts.

Maintaining broker relationships is essential but costly—Generali’s 2024 distribution expenses rose ~3% YoY—so the group must balance commission, service, and digital tools to defend share.

Low Switching Costs in Asset Management Services

Low switching costs in Generali’s asset management mean institutional and retail clients can reallocate capital quickly if funds lag peers; global fund flows showed €250bn moved between European asset managers in 2024, highlighting liquidity of client decisions.

Underperformance versus benchmarks forces Generali to keep returns competitive and fees tight; Generali AM reported €520bn AUM at end-2024, so small net outflows can hit revenue.

By late 2025, greater performance transparency—public RTS reporting and third-party data—will let clients make rapid, data-driven exits, raising retention pressure.

- Clients can switch quickly; 2024 EU fund flows €250bn

- Generali AM AUM €520bn (end-2024)

- Performance transparency rising by late 2025

- Pressure on returns and fees to avoid outflows

Rising Expectations for Digital Integration and UX

Modern insurance customers demand seamless digital experiences from purchase to claims; 68% of European policyholders now expect mobile-first service, per a 2024 McKinsey survey, so Generali risks losing buyers if its UX or digital payouts lag.

If Generali fails to match insurtech speed—median digital claims payout times under 48 hours—customers will switch, giving buyers leverage to set the pace of tech investment.

Meeting these standards is required to prevent churn: Generali reported 2024 digital channel growth of ~22%, signaling customer preference and the cost of falling behind.

- 68% expect mobile-first service (McKinsey 2024)

- Median digital claims payout <48 hours (insurtech benchmark)

- Generali digital channel growth ~22% in 2024

Customers' pricing power squeezes insurers: retailers, brokers and corporates dominate

Customers exert strong bargaining power across retail, corporate, broker and asset‑management channels: price-sensitive retail shoppers (62% use price comparisons; motor churn >18% in Italy, IVASS 2024) and digital channels (35% new retail policies online, 2024) cap pricing; 22% of commercial premiums come from large corporates (2024) who demand bespoke low‑margin deals; brokers drive ~45% of retail/SME premiums and €1.2bn in commissions (2024); Generali AM AUM €520bn (end‑2024) risks rapid outflows on underperformance.

| Metric | 2024 |

|---|---|

| Retail price comparison use | 62% |

| Motor churn (Italy) | >18% |

| Online new retail share | 35% |

| Commercial premiums from large corporates | 22% |

| Broker share of retail/SME premiums | 45% |

| Broker commissions paid | €1.2bn |

| Generali AM AUM | €520bn |

Full Version Awaits

Assicurazioni Generali Porter's Five Forces Analysis

This preview shows the exact Assicurazioni Generali Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full, professionally formatted report you’ll be able to download and use the moment you buy.

You're looking at the actual, final deliverable; once payment is complete, you’ll get instant access to this same file, ready for use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Assicurazioni Generali faces moderate buyer power, high regulatory pressure, and intense rivalry from global insurers, while digital entrants and insurtechs raise the threat of substitution; supplier power (reinsurance and capital markets) remains a key strategic variable. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Assicurazioni Generali’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration in the Reinsurance Market

Generali depends on global reinsurers such as Munich Re and Swiss Re to manage large, systemic risks; these two firms account for a large share of capacity, leaving few alternatives and raising supplier power.

By end-2025, a reinsurance hard market—reinsurance rate-on-line rises of 10–20% seen in 2023–24—would directly compress Generali’s combined ratio and margins as ceded premiums climb.

This reliance makes reinsurance pricing and availability a key supplier-driven driver of Generali’s cost of capital and risk-transfer expense, affecting solvency and earnings volatility.

Critical Dependence on Specialized IT and Cybersecurity Vendors

Generali depends on high-end software and cloud providers as insurance shifts digital; 2024 group IT spend was ~€1.2bn, raising reliance on vendors for AI underwriting and cloud ops.

Specialized firms offering AI-driven risk models and cybersecurity hold bargaining power—Gartner estimated 40% price premium for certified AI/compliance tools in 2025.

Tighter EU data rules by 2026 raise demand for compliance services, letting vendors charge premiums while Generali’s continuity hinges on these third-party tech stacks.

Scarcity of Specialized Actuarial and Data Science Talent

Human capital is central for Assicurazioni Generali; demand for actuaries and data scientists rose ~28% globally 2019–2024 while supply lagged, creating a talent gap.

Scarcity lets senior specialists and headhunters push pay premiums—median data scientist salary in Italy reached ~€60k–€85k in 2024, up ~12% year-on-year.

Generali competes with insurers, fintech and big tech for this scarce skill set, raising hiring and retention costs.

Influence of Financial Market Data Providers

Generali’s asset management and investment teams rely on real-time feeds from near-oligopoly providers such as Bloomberg, Refinitiv (Reuters), and MSCI, which in 2024 controlled ~70–80% of institutional market-data revenue, letting them charge high fees and impose restrictive licenses.

Because such data is essential for trading, risk models, and regulatory reporting (MiFID II, Solvency II), suppliers exert strong pricing power and materially affect Generali’s operational costs—vendor fees can represent low-single-digit basis points of AUM but millions of euros annually.

- ~70–80% market share among top providers (2024)

- High fixed fees and restrictive licenses

- Essential for MiFID II and Solvency II compliance

- Costs: millions EUR annually; low-single-digit bps of AUM

Impact of Regulatory Bodies as De Facto Suppliers

Regulatory authorities act as de facto suppliers by providing licenses and the legal framework essential for Generali’s operations; Solvency II rules set minimum capital and risk-margin requirements. As of late 2025, Solvency II-related capital targets push Generali to maintain Solvency II ratio near 200% (Q3 2025 reported ~198%), constraining product mix and M&A flexibility. Sudden regulatory changes can force higher capital buffers or business-model adjustments, raising cost of capital and limiting strategic moves.

- Regulatory supply: licenses, rules, oversight

- Key rule: Solvency II → capital/reserve mandates

- Q3 2025 Solvency II ratio ~198% → limited leverage

- Policy change risk → higher capital, constrained strategy

Generali squeezed by reinsurers, data oligopoly & talent costs; Solvency II caps flexibility

Generali faces high supplier power from concentrated reinsurers (Munich Re, Swiss Re), market-data oligopolies (Bloomberg, Refinitiv, MSCI ~70–80% share 2024), and scarce tech talent (Italy data-scientist median €60–85k in 2024), raising ceded-premium, vendor fees, and salary costs; Q3 2025 Solvency II ratio ~198% limits capital flexibility.

| Supplier | Key stat | Impact |

|---|---|---|

| Reinsurers | Rate-on-line +10–20% (2023–24) | Higher ceded premiums |

| Market data | 70–80% share (2024) | High fees, restrictive licenses |

| Tech talent | €60–85k median (Italy 2024) | Rising payroll |

| Regulator | SII ratio ~198% (Q3 2025) | Limits strategy |

What is included in the product

Tailored Porter’s Five Forces analysis for Assicurazioni Generali that uncovers competitive intensity, buyer and supplier power, threat of substitutes and entrants, and highlights disruptive pressures and strategic levers to protect market share and profitability.

A concise Porter's Five Forces snapshot for Assicurazioni Generali—quickly assess competitive pressure and regulatory risk to speed strategic decisions.

Customers Bargaining Power

High Price Sensitivity in Retail Insurance Segments

Individual customers in Generali’s motor and home segments are highly price-sensitive and brand-agnostic; 2024 IVASS data show price comparison usage at 62% for motor shoppers, driving churn rates above 18% annually in Italy. Digital comparison tools let consumers switch instantly to the lowest premium, with price-led online channels capturing 35% of new retail policies in 2024. This commoditization caps Generali’s pricing power—raising premiums risks immediate market-share loss given a 10–15% elasticity observed in recent studies. As a result, individual consumers wield strong bargaining power through easy comparison and migration.

Leverage of Large Corporate and Institutional Clients

Generali serves multinational corporates that supply large premium volumes—about 22% of group commercial premiums in 2024—giving them strong bargaining power.

These clients use in‑house risk managers to negotiate bespoke, low‑margin deals; Generali often concedes on pricing or terms to retain accounts tied to regional revenue targets.

The segment leverages scale to demand tailored, cost‑effective solutions, pressuring margins and pushing product customization.

Influence of Independent Brokers and Intermediaries

A large portion of Generali’s retail and SME premiums—about 45% of gross written premiums in 2024—flows through independent brokers who act as proxies for end customers, giving intermediaries directional power over insurer choice.

Brokers can steer clients via commission levels and service quality; Generali paid roughly €1.2bn in broker commissions in 2024, a lever that influences retention and new business.

Because brokers aggregate many small clients, their collective bargaining can compress margins; a 1 percentage-point cut in commission demands could reduce net combined ratio by ~0.5–1.0 pts.

Maintaining broker relationships is essential but costly—Generali’s 2024 distribution expenses rose ~3% YoY—so the group must balance commission, service, and digital tools to defend share.

Low Switching Costs in Asset Management Services

Low switching costs in Generali’s asset management mean institutional and retail clients can reallocate capital quickly if funds lag peers; global fund flows showed €250bn moved between European asset managers in 2024, highlighting liquidity of client decisions.

Underperformance versus benchmarks forces Generali to keep returns competitive and fees tight; Generali AM reported €520bn AUM at end-2024, so small net outflows can hit revenue.

By late 2025, greater performance transparency—public RTS reporting and third-party data—will let clients make rapid, data-driven exits, raising retention pressure.

- Clients can switch quickly; 2024 EU fund flows €250bn

- Generali AM AUM €520bn (end-2024)

- Performance transparency rising by late 2025

- Pressure on returns and fees to avoid outflows

Rising Expectations for Digital Integration and UX

Modern insurance customers demand seamless digital experiences from purchase to claims; 68% of European policyholders now expect mobile-first service, per a 2024 McKinsey survey, so Generali risks losing buyers if its UX or digital payouts lag.

If Generali fails to match insurtech speed—median digital claims payout times under 48 hours—customers will switch, giving buyers leverage to set the pace of tech investment.

Meeting these standards is required to prevent churn: Generali reported 2024 digital channel growth of ~22%, signaling customer preference and the cost of falling behind.

- 68% expect mobile-first service (McKinsey 2024)

- Median digital claims payout <48 hours (insurtech benchmark)

- Generali digital channel growth ~22% in 2024

Customers' pricing power squeezes insurers: retailers, brokers and corporates dominate

Customers exert strong bargaining power across retail, corporate, broker and asset‑management channels: price-sensitive retail shoppers (62% use price comparisons; motor churn >18% in Italy, IVASS 2024) and digital channels (35% new retail policies online, 2024) cap pricing; 22% of commercial premiums come from large corporates (2024) who demand bespoke low‑margin deals; brokers drive ~45% of retail/SME premiums and €1.2bn in commissions (2024); Generali AM AUM €520bn (end‑2024) risks rapid outflows on underperformance.

| Metric | 2024 |

|---|---|

| Retail price comparison use | 62% |

| Motor churn (Italy) | >18% |

| Online new retail share | 35% |

| Commercial premiums from large corporates | 22% |

| Broker share of retail/SME premiums | 45% |

| Broker commissions paid | €1.2bn |

| Generali AM AUM | €520bn |

Full Version Awaits

Assicurazioni Generali Porter's Five Forces Analysis

This preview shows the exact Assicurazioni Generali Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full, professionally formatted report you’ll be able to download and use the moment you buy.

You're looking at the actual, final deliverable; once payment is complete, you’ll get instant access to this same file, ready for use.