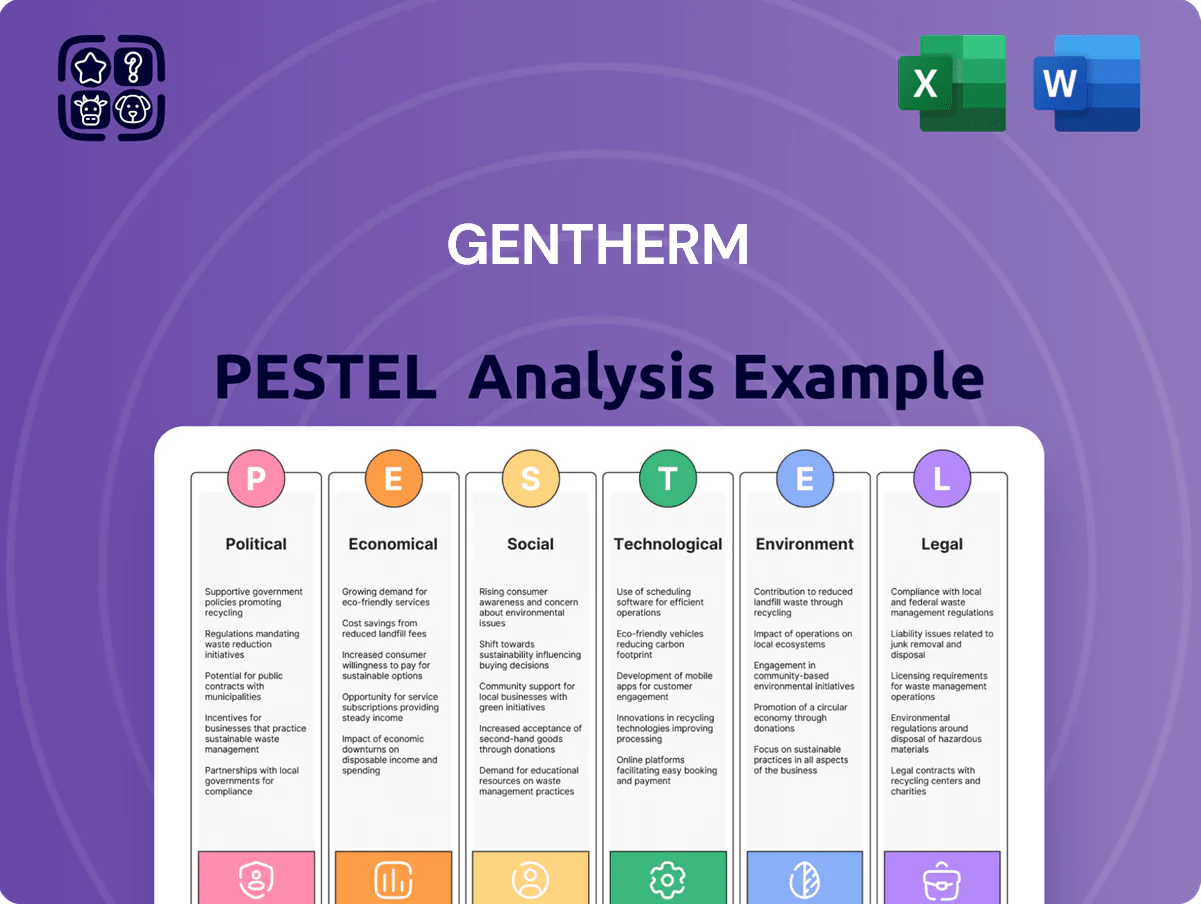

Gentherm PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a competitive edge with our targeted PESTLE Analysis of Gentherm—uncover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures will shape its strategy and valuation; download the full report now for actionable insights, editable charts, and ready-to-use recommendations tailored for investors, consultants, and strategists.

Political factors

Trade policy and tariff volatility

Ongoing trade tensions among the US, China, and EU force Gentherm to adjust its global supply chain; in 2024 US-China tariff uncertainty and EU industrial tariffs contributed to component cost volatility of roughly 3–5% for automotive electronics.

Import duties on semiconductors, copper, and polymers have shifted with protectionist measures, raising part costs and squeezing GM margins; Gentherm reported 2024 input-cost inflation near 4% in thermal systems.

To mitigate tariff shocks, Gentherm is diversifying manufacturing—expanding capacity in Mexico, Hungary, and China—reducing single-market exposure and shielding revenues from sudden tariff increases.

Government incentives for electric vehicles

Geopolitical stability in manufacturing hubs

Gentherm's manufacturing footprint in Mexico, Vietnam and Eastern Europe exposes it to regional political risks; Mexico accounted for about 22% of 2024 production capacity, Vietnam ~18% and Eastern Europe ~12%, so instability could disrupt a third-plus of output.

Political unrest or changes in labor laws—recent wage hikes of 6–8% in parts of Mexico (2024) and evolving labor rules in Vietnam—could raise COGS and push operating margins below the 2024 adjusted margin of 6.3%.

Management must continuously monitor local election cycles, regulatory shifts and geopolitical tensions to protect capital expenditures of roughly $120–140 million planned through 2025 and to mitigate supply-chain and labor-cost shocks.

National security and supply chain localization

Governments view automotive and semiconductor supply chains as national security issues, prompting localization mandates—US CHIPS Act ($280B since 2022) and EU’s 2023 Critical Raw Materials and IPCEI measures—forcing Gentherm to site production near OEMs to meet domestic content rules.

Failure to localize risks losing contracts with state-backed OEMs; automakers now demand >60% regional content in some programs, affecting Gentherm’s revenue exposure (FY2024 revenue $1.46B).

- CHIPS Act and EU measures drive onshoring

- Automakers requiring >60% regional content

- Gentherm FY2024 revenue $1.46B—localization impacts contract retention

Global energy security mandates

Political pressure to cut fossil fuel dependence is driving stricter efficiency mandates in automotive and industrial sectors; EU aims for at least 55% GHG reduction by 2030 and many countries target net-zero by 2050, raising compliance urgency.

Gentherm’s thermal management lowers vehicle battery loads and industrial energy use, aligning with these mandates and creating market upside as EV thermal tech demand grows—global EV sales hit ~14 million in 2024.

As governments tighten rules, Gentherm faces regulatory compliance costs but also a multi-billion-dollar opportunity in efficiency solutions, with vehicle thermal management market projected to exceed $10B by 2030.

- Aligns with 2030 carbon targets (EU 55% reduction)

- Supports EVs—14M global EVs sold in 2024

- Market opp: vehicle thermal management >$10B by 2030

Rising input costs, onshoring risks; EV tailwinds push thermal market toward $10B+

Trade tensions, tariffs and localization rules (CHIPS Act, EU measures) raised 2024 input costs ~3–5% and drove onshoring; Mexico/Vietnam/Eastern Europe held ~52% of capacity, exposing >33% of output to regional risks. EV incentives (IRA, EU Green Deal) lifted EV share to ~7.6% US/14% EU, expanding addressable market as vehicle thermal-management market eyes >$10B by 2030; FY2024 revenue $1.46B; capex planned $120–140M through 2025.

| Metric | 2024/2025 |

|---|---|

| FY2024 revenue | $1.46B |

| Input-cost inflation | ~3–5% |

| Manufacturing share (Mx/VN/EE) | ~52% |

| EV share (US/EU) | 7.6% / 14% |

| Capex 2024–25 | $120–140M |

| Thermal market to 2030 | >$10B |

What is included in the product

Explores how macro-environmental factors uniquely affect Gentherm across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples to identify threats and opportunities for executives, consultants, and investors.

Clean, concise Gentherm PESTLE summary tailored for quick reference in meetings and presentations, visually organized by category to speed interpretation and support risk discussions across teams.

Economic factors

Fluctuations in global automotive production

Gentherm’s revenue is closely tied to global light-vehicle production—which fell 2.6% in 2023 to about 77.5 million units and was projected around 79–80 million in 2024—so GDP slowdowns that trim vehicle demand hit its seating and thermal order book directly.

A 1% decline in global vehicle volumes can meaningfully reduce Gentherm’s sales given automotive customers account for over 85% of revenue, amplifying operating leverage during cyclical troughs.

The company must preserve a flexible cost base—adjustable labor, variable sourcing, and capacity scaling—to protect margins that compressed to mid-single digits in weaker quarters of 2023–2024.

Interest rate impacts on consumer spending

High interest rates through 2024–2025 raised average new auto loan rates to ~8.0% in 2024 (up from ~5.5% in 2021), increasing monthly payments and likely reducing demand for luxury trims that carry Gentherm thermal systems.

More expensive financing encourages buyers toward base models or purchase delays, lowering penetration of premium comfort options and pressuring OEM orders for Gentherm components.

Auto sales slowed with U.S. light-vehicle sales ~13.6M SAAR in 2024 versus ~15.0M pre-pandemic, amplifying sensitivity to optional-feature uptake.

If rates stabilize in 2025, analysts expect pent-up demand could boost adoption of advanced in-cabin technologies and restore upgrade rates for Gentherm products.

Rising costs of raw materials and electronics

The price of inputs like copper, specialty plastics and semiconductor chips is material for Gentherm; LME copper rose ~17% in 2024 while global chip spot indices climbed ~22%, lifting input costs and pressuring margins.

Inflation in commodity markets limits Gentherm’s pricing power with OEMs; 2024 gross margin compression signaled sensitivity when cost passthrough was constrained.

Gentherm uses hedging and multi‑year supply agreements—about 60% of key components under contract in 2024—to mitigate volatility, but sustained input inflation remains a significant headwind.

Currency exchange rate volatility

As a U.S.-reported multinational, Gentherm faces transactional and translational FX risk; a 10% USD appreciation vs EUR or CNY can materially compress overseas margins and lower reported international revenue—Gentherm disclosed 2024 international sales at about 55% of total, amplifying exposure.

Management uses hedging, localized sourcing and pricing adjustments; in 2024 Gentherm reported FX hedges and cost localization programs that helped protect operating income against volatility.

- ~55% of 2024 sales generated outside U.S., raising FX impact

- 10% USD strength vs EUR/CNY notably reduces competitiveness and reported earnings

- Mitigations: hedging, localized sourcing, regional pricing

Economic growth in emerging markets

Rapid urbanization and a rising middle class in India and Southeast Asia—projected to add over 400 million urban residents by 2030—expand demand for automotive comfort, benefiting Gentherm’s thermal-management systems.

Vehicle air-conditioning penetration is rising: India’s A/C fitment in new cars grew from ~38% in 2019 to ~52% in 2024, signaling market alignment with Gentherm’s strengths.

To capture share, Gentherm must offer cost-optimized variants; local sourcing and modular designs can address price sensitivity while preserving performance.

- India/Southeast Asia urbanization +400M by 2030

- India A/C fitment ~52% in 2024 (from ~38% in 2019)

- Strategy: local sourcing, modular/cost-optimized products

Gentherm: 85% auto exposure, 55% international sales, input costs rise risk

Gentherm revenue tied to ~77.5M global vehicle builds in 2023; 85% automotive exposure makes a 1% volume drop material; 2024: ~8.0% avg new auto loan rate, LME copper +17%, chip indices +22%; 2024 international sales ~55%; ~60% of key components under multi‑year contracts.

| Metric | 2024/2023 |

|---|---|

| Global light vehicles | ~77.5M (2023) |

| Auto revenue exposure | ~85% |

| New loan rate | ~8.0% (2024) |

| LME copper | +17% (2024) |

| Chip indices | +22% (2024) |

| Intl sales | ~55% (2024) |

| Contracted components | ~60% |

Same Document Delivered

Gentherm PESTLE Analysis

The preview shown here is the exact Gentherm PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a competitive edge with our targeted PESTLE Analysis of Gentherm—uncover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures will shape its strategy and valuation; download the full report now for actionable insights, editable charts, and ready-to-use recommendations tailored for investors, consultants, and strategists.

Political factors

Trade policy and tariff volatility

Ongoing trade tensions among the US, China, and EU force Gentherm to adjust its global supply chain; in 2024 US-China tariff uncertainty and EU industrial tariffs contributed to component cost volatility of roughly 3–5% for automotive electronics.

Import duties on semiconductors, copper, and polymers have shifted with protectionist measures, raising part costs and squeezing GM margins; Gentherm reported 2024 input-cost inflation near 4% in thermal systems.

To mitigate tariff shocks, Gentherm is diversifying manufacturing—expanding capacity in Mexico, Hungary, and China—reducing single-market exposure and shielding revenues from sudden tariff increases.

Government incentives for electric vehicles

Geopolitical stability in manufacturing hubs

Gentherm's manufacturing footprint in Mexico, Vietnam and Eastern Europe exposes it to regional political risks; Mexico accounted for about 22% of 2024 production capacity, Vietnam ~18% and Eastern Europe ~12%, so instability could disrupt a third-plus of output.

Political unrest or changes in labor laws—recent wage hikes of 6–8% in parts of Mexico (2024) and evolving labor rules in Vietnam—could raise COGS and push operating margins below the 2024 adjusted margin of 6.3%.

Management must continuously monitor local election cycles, regulatory shifts and geopolitical tensions to protect capital expenditures of roughly $120–140 million planned through 2025 and to mitigate supply-chain and labor-cost shocks.

National security and supply chain localization

Governments view automotive and semiconductor supply chains as national security issues, prompting localization mandates—US CHIPS Act ($280B since 2022) and EU’s 2023 Critical Raw Materials and IPCEI measures—forcing Gentherm to site production near OEMs to meet domestic content rules.

Failure to localize risks losing contracts with state-backed OEMs; automakers now demand >60% regional content in some programs, affecting Gentherm’s revenue exposure (FY2024 revenue $1.46B).

- CHIPS Act and EU measures drive onshoring

- Automakers requiring >60% regional content

- Gentherm FY2024 revenue $1.46B—localization impacts contract retention

Global energy security mandates

Political pressure to cut fossil fuel dependence is driving stricter efficiency mandates in automotive and industrial sectors; EU aims for at least 55% GHG reduction by 2030 and many countries target net-zero by 2050, raising compliance urgency.

Gentherm’s thermal management lowers vehicle battery loads and industrial energy use, aligning with these mandates and creating market upside as EV thermal tech demand grows—global EV sales hit ~14 million in 2024.

As governments tighten rules, Gentherm faces regulatory compliance costs but also a multi-billion-dollar opportunity in efficiency solutions, with vehicle thermal management market projected to exceed $10B by 2030.

- Aligns with 2030 carbon targets (EU 55% reduction)

- Supports EVs—14M global EVs sold in 2024

- Market opp: vehicle thermal management >$10B by 2030

Rising input costs, onshoring risks; EV tailwinds push thermal market toward $10B+

Trade tensions, tariffs and localization rules (CHIPS Act, EU measures) raised 2024 input costs ~3–5% and drove onshoring; Mexico/Vietnam/Eastern Europe held ~52% of capacity, exposing >33% of output to regional risks. EV incentives (IRA, EU Green Deal) lifted EV share to ~7.6% US/14% EU, expanding addressable market as vehicle thermal-management market eyes >$10B by 2030; FY2024 revenue $1.46B; capex planned $120–140M through 2025.

| Metric | 2024/2025 |

|---|---|

| FY2024 revenue | $1.46B |

| Input-cost inflation | ~3–5% |

| Manufacturing share (Mx/VN/EE) | ~52% |

| EV share (US/EU) | 7.6% / 14% |

| Capex 2024–25 | $120–140M |

| Thermal market to 2030 | >$10B |

What is included in the product

Explores how macro-environmental factors uniquely affect Gentherm across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples to identify threats and opportunities for executives, consultants, and investors.

Clean, concise Gentherm PESTLE summary tailored for quick reference in meetings and presentations, visually organized by category to speed interpretation and support risk discussions across teams.

Economic factors

Fluctuations in global automotive production

Gentherm’s revenue is closely tied to global light-vehicle production—which fell 2.6% in 2023 to about 77.5 million units and was projected around 79–80 million in 2024—so GDP slowdowns that trim vehicle demand hit its seating and thermal order book directly.

A 1% decline in global vehicle volumes can meaningfully reduce Gentherm’s sales given automotive customers account for over 85% of revenue, amplifying operating leverage during cyclical troughs.

The company must preserve a flexible cost base—adjustable labor, variable sourcing, and capacity scaling—to protect margins that compressed to mid-single digits in weaker quarters of 2023–2024.

Interest rate impacts on consumer spending

High interest rates through 2024–2025 raised average new auto loan rates to ~8.0% in 2024 (up from ~5.5% in 2021), increasing monthly payments and likely reducing demand for luxury trims that carry Gentherm thermal systems.

More expensive financing encourages buyers toward base models or purchase delays, lowering penetration of premium comfort options and pressuring OEM orders for Gentherm components.

Auto sales slowed with U.S. light-vehicle sales ~13.6M SAAR in 2024 versus ~15.0M pre-pandemic, amplifying sensitivity to optional-feature uptake.

If rates stabilize in 2025, analysts expect pent-up demand could boost adoption of advanced in-cabin technologies and restore upgrade rates for Gentherm products.

Rising costs of raw materials and electronics

The price of inputs like copper, specialty plastics and semiconductor chips is material for Gentherm; LME copper rose ~17% in 2024 while global chip spot indices climbed ~22%, lifting input costs and pressuring margins.

Inflation in commodity markets limits Gentherm’s pricing power with OEMs; 2024 gross margin compression signaled sensitivity when cost passthrough was constrained.

Gentherm uses hedging and multi‑year supply agreements—about 60% of key components under contract in 2024—to mitigate volatility, but sustained input inflation remains a significant headwind.

Currency exchange rate volatility

As a U.S.-reported multinational, Gentherm faces transactional and translational FX risk; a 10% USD appreciation vs EUR or CNY can materially compress overseas margins and lower reported international revenue—Gentherm disclosed 2024 international sales at about 55% of total, amplifying exposure.

Management uses hedging, localized sourcing and pricing adjustments; in 2024 Gentherm reported FX hedges and cost localization programs that helped protect operating income against volatility.

- ~55% of 2024 sales generated outside U.S., raising FX impact

- 10% USD strength vs EUR/CNY notably reduces competitiveness and reported earnings

- Mitigations: hedging, localized sourcing, regional pricing

Economic growth in emerging markets

Rapid urbanization and a rising middle class in India and Southeast Asia—projected to add over 400 million urban residents by 2030—expand demand for automotive comfort, benefiting Gentherm’s thermal-management systems.

Vehicle air-conditioning penetration is rising: India’s A/C fitment in new cars grew from ~38% in 2019 to ~52% in 2024, signaling market alignment with Gentherm’s strengths.

To capture share, Gentherm must offer cost-optimized variants; local sourcing and modular designs can address price sensitivity while preserving performance.

- India/Southeast Asia urbanization +400M by 2030

- India A/C fitment ~52% in 2024 (from ~38% in 2019)

- Strategy: local sourcing, modular/cost-optimized products

Gentherm: 85% auto exposure, 55% international sales, input costs rise risk

Gentherm revenue tied to ~77.5M global vehicle builds in 2023; 85% automotive exposure makes a 1% volume drop material; 2024: ~8.0% avg new auto loan rate, LME copper +17%, chip indices +22%; 2024 international sales ~55%; ~60% of key components under multi‑year contracts.

| Metric | 2024/2023 |

|---|---|

| Global light vehicles | ~77.5M (2023) |

| Auto revenue exposure | ~85% |

| New loan rate | ~8.0% (2024) |

| LME copper | +17% (2024) |

| Chip indices | +22% (2024) |

| Intl sales | ~55% (2024) |

| Contracted components | ~60% |

Same Document Delivered

Gentherm PESTLE Analysis

The preview shown here is the exact Gentherm PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and investment decisions.