Georg Fischer Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

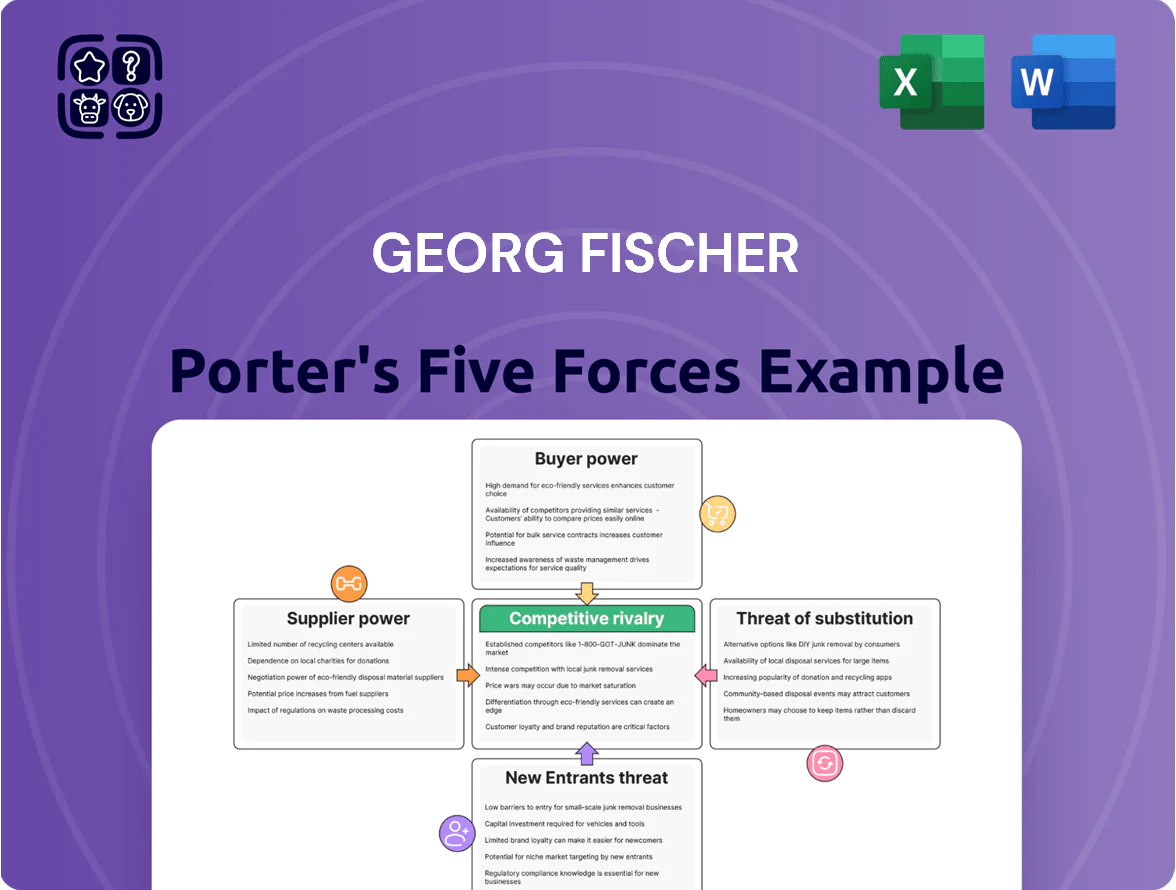

Georg Fischer faces moderate supplier power due to specialized materials, steady buyer power from industrial clients, and a moderate threat of new entrants given capital intensity; rivalry is high among precision-engineering peers while substitutes remain limited for core piping solutions. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Georg Fischer’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material price volatility

Georg Fischer depends on polyethylene, aluminum, magnesium and high-grade steel; commodity price swings cut gross margins—aluminum rose ~18% and polyethylene ~12% YTD through Q3 2025, pressuring COGS.

The firm uses long-term contracts covering ~60% of volumes and strategic sourcing hubs in Europe and China to smooth costs, trimming volatility risk.

Specialized resin and alloy suppliers retain moderate leverage because ~25–30% of inputs are single-source or qualified-spec, so passthrough is limited but real.

Energy costs and availability

The Casting Solutions and Machining Solutions divisions are energy-intensive, making Georg Fischer (GF) highly sensitive to utility pricing; in 2025 industrial electricity in Europe averaged about €0.27/kWh, up ~15% vs 2020, increasing operating cost pressure. Suppliers of green or carbon-neutral power have stronger leverage as GF pushes to meet its 2030 target of 50% CO2 reduction, with PPAs and certificates commanding premiums of 10–25%. Volatile spot markets and grid fees raise procurement complexity, so locking multi-year contracts is vital to limit margin erosion.

Specialized component suppliers

For Machining Solutions, Georg Fischer (GF) relies on niche electronic components and precision sensors made by few high-tech vendors, giving suppliers strong bargaining power due to technical complexity and scarce alternatives; in 2024 GF spent ~CHF 220m on electronics-related procurement, so supply disruption risk is material. GF reduces this by long-term contracts and joint R&D—70% of its sensor sourcing now under multi-year agreements—and dual-sourcing key parts where feasible.

Logistics and transportation providers

As a global entity, Georg Fischer depends on international shipping and logistics firms to move products across its three divisions; by 2025, ocean carrier consolidation left the top 10 container lines handling ~85% of capacity, boosting carriers’ pricing power and raising spot rates by ~40% vs 2019.

GF counters rising freight costs and decarbonization premiums by shifting production regionally—reducing average shipment distance by an estimated 12% since 2020—and by contracting longer-term logistics capacity with low-emissions surcharges capped where possible.

Sustainability and ESG compliance

Suppliers certified to high ESG standards have gained leverage as Georg Fischer (GF) prioritizes sustainable sourcing to meet investor and EU regulations; about 18% of GF’s 2024 procurement spend went to certified low-carbon suppliers, up from 11% in 2021.

Smaller supplier pools charge premiums—estimated 6–12% higher per ton for low-carbon alloys—while GF runs annual audits covering ~72% of spend to verify compliance and manage risk.

GF accepts higher input costs; in 2024 ESG-related sourcing added an estimated CHF 25–35 million to procurement costs but reduced scope 3 emissions intensity by ~7% year-over-year.

- 18% 2024 spend to certified suppliers

- 6–12% price premium for low-carbon materials

- 72% of spend audited annually

- CHF 25–35m extra procurement costs in 2024

- 7% YoY reduction in scope 3 emissions intensity

Supply squeeze: commodity-driven COGS rise vs. GF’s contract, regional & green offsets

Suppliers hold moderate-to-strong power: commodity swings (Al +18%, PE +12% YTD through Q3 2025) raise COGS, niche electronic/sensor vendors and green-power providers demand premiums, and ocean carrier consolidation (top 10 = ~85% capacity) lifts freight; GF offsets with ~60% long-term contracts, 70% sensor sourcing under multi-year deals, regional production (‑12% shipment distance) and 18% spend on certified low-carbon suppliers.

| Metric | Value |

|---|---|

| Al price change (YTD Q3 2025) | +18% |

| Polyethylene (YTD Q3 2025) | +12% |

| Volumes under long-term contracts | ~60% |

| Sensor sourcing multi-year | 70% |

| Top 10 carriers capacity (2025) | ~85% |

| Shipment distance change since 2020 | -12% |

| Spend on certified low-carbon suppliers (2024) | 18% |

What is included in the product

Tailored exclusively for Georg Fischer, this Porter's Five Forces overview uncovers competitive intensity, supplier and buyer power, entry barriers, substitute threats, and emerging disruptors, with strategic implications for its pricing, profitability, and market positioning.

Compact Porter's Five Forces for Georg Fischer—quickly spot bargaining power, rivalry, and supplier risks to streamline strategic decisions and investor briefings.

Customers Bargaining Power

Concentration of automotive and aerospace OEMs

In Casting Solutions, roughly 60% of 2024 revenue came from about 10 large automotive and aerospace OEMs, concentrating buyer power and letting customers demand lower prices and higher quality, squeezing margins during renewals.

By 2025, EV adoption increased lightweight-part sourcing: OEM requests for aluminum components rose ~18% YoY, intensifying price and specification pressure on Georg Fischer and raising supplier switching risk.

Fragmented buyer base in Piping Systems

The GF Piping Systems division serves a diverse, fragmented buyer base—utilities, construction firms, and industrial plants—so individual buyer power is low; GF reported CHF 2.9bn group sales in 2024, with piping a material share. Large infrastructure contracts can push for volume discounts, but GF’s leak‑proof, corrosion‑resistant solutions command premium pricing tied to reliability and lifecycle costs. Customers prioritize long‑term performance over lowest upfront price, lowering churn and strengthening margins.

High switching costs in Machining Solutions

Customers face high switching costs with GF Machining Solutions because proprietary software and specialist training bind users to its EDM and milling systems; studies show tech-switch projects can cost manufacturers 5–15% of annual production value and take 3–9 months of downtime. After adoption, production-cycle disruption and requalification risks make switching unlikely, creating technological lock-in that shields GF from aggressive price-driven churn and supports margin stability—GF reported 2024 aftermarket revenue resilience at ~28% of segment sales.

Total cost of ownership focus

Sophisticated buyers in 2025 focus on total cost of ownership—maintenance, energy use, and lifespan—over sticker price; industry surveys show 68% of professional purchasers cite TCO as primary buying criterion. GF uses its reputation for durable castings and piping to justify 8–15% premium pricing in EU and North America. Its service contracts and digital monitoring (reducing downtime by ~12% per GF case studies) strengthen ties with value-conscious buyers.

- 68% cite TCO as key in 2025

- GF premium pricing 8–15%

- Digital monitoring cuts downtime ~12%

- Service packages boost renewal rates

Digitalization and price transparency

The rise of digital procurement platforms and price transparency lets large buyers compare Georg Fischer (GF) products with global rivals, raising customer bargaining power; procurement platforms showed a 22% YoY increase in industrial listings in 2024, widening comparison. GF responded with ~CHF 80m invested in digital sales/CRM through 2023–24 to deliver personalized value and capture higher-margin service revenue. These tools enable tailored solutions and remote technical support, shifting competition from price to integrated service.

- 22% YoY rise in industrial procurement listings (2024)

- GF digital/CRM investment ~CHF 80m (2023–24)

- Shift: product price → tailored solutions & support

Mixed buyer power: concentrated OEM pricing vs. high switching costs and TCO focus

Customer bargaining power is mixed: Casting Solutions sees high concentration (10 OEMs = ~60% 2024 revenue) pressing prices, while Piping buyers are fragmented and less price-sensitive; Machining users face high switching costs (5–15% production value, 3–9 months downtime) that protect margins. GF charges 8–15% premium; 68% buyers cite TCO; digital procurement rose 22% (2024), GF invested ~CHF 80m (2023–24).

| Metric | Value |

|---|---|

| Top-10 OEM share (Casting, 2024) | ~60% |

| OEM demand for aluminum parts (2025 YoY) | +18% |

| Switch cost impact | 5–15% annual value; 3–9 months |

| Buyers citing TCO (2025) | 68% |

| GF premium pricing | 8–15% |

| Procurement listings growth (2024) | +22% |

| Digital/CRM investment (2023–24) | ~CHF 80m |

Full Version Awaits

Georg Fischer Porter's Five Forces Analysis

This preview shows the exact Georg Fischer Porter's Five Forces analysis you'll receive immediately after purchase—no mockups, no placeholders, fully formatted and ready for use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Georg Fischer faces moderate supplier power due to specialized materials, steady buyer power from industrial clients, and a moderate threat of new entrants given capital intensity; rivalry is high among precision-engineering peers while substitutes remain limited for core piping solutions. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Georg Fischer’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material price volatility

Georg Fischer depends on polyethylene, aluminum, magnesium and high-grade steel; commodity price swings cut gross margins—aluminum rose ~18% and polyethylene ~12% YTD through Q3 2025, pressuring COGS.

The firm uses long-term contracts covering ~60% of volumes and strategic sourcing hubs in Europe and China to smooth costs, trimming volatility risk.

Specialized resin and alloy suppliers retain moderate leverage because ~25–30% of inputs are single-source or qualified-spec, so passthrough is limited but real.

Energy costs and availability

The Casting Solutions and Machining Solutions divisions are energy-intensive, making Georg Fischer (GF) highly sensitive to utility pricing; in 2025 industrial electricity in Europe averaged about €0.27/kWh, up ~15% vs 2020, increasing operating cost pressure. Suppliers of green or carbon-neutral power have stronger leverage as GF pushes to meet its 2030 target of 50% CO2 reduction, with PPAs and certificates commanding premiums of 10–25%. Volatile spot markets and grid fees raise procurement complexity, so locking multi-year contracts is vital to limit margin erosion.

Specialized component suppliers

For Machining Solutions, Georg Fischer (GF) relies on niche electronic components and precision sensors made by few high-tech vendors, giving suppliers strong bargaining power due to technical complexity and scarce alternatives; in 2024 GF spent ~CHF 220m on electronics-related procurement, so supply disruption risk is material. GF reduces this by long-term contracts and joint R&D—70% of its sensor sourcing now under multi-year agreements—and dual-sourcing key parts where feasible.

Logistics and transportation providers

As a global entity, Georg Fischer depends on international shipping and logistics firms to move products across its three divisions; by 2025, ocean carrier consolidation left the top 10 container lines handling ~85% of capacity, boosting carriers’ pricing power and raising spot rates by ~40% vs 2019.

GF counters rising freight costs and decarbonization premiums by shifting production regionally—reducing average shipment distance by an estimated 12% since 2020—and by contracting longer-term logistics capacity with low-emissions surcharges capped where possible.

Sustainability and ESG compliance

Suppliers certified to high ESG standards have gained leverage as Georg Fischer (GF) prioritizes sustainable sourcing to meet investor and EU regulations; about 18% of GF’s 2024 procurement spend went to certified low-carbon suppliers, up from 11% in 2021.

Smaller supplier pools charge premiums—estimated 6–12% higher per ton for low-carbon alloys—while GF runs annual audits covering ~72% of spend to verify compliance and manage risk.

GF accepts higher input costs; in 2024 ESG-related sourcing added an estimated CHF 25–35 million to procurement costs but reduced scope 3 emissions intensity by ~7% year-over-year.

- 18% 2024 spend to certified suppliers

- 6–12% price premium for low-carbon materials

- 72% of spend audited annually

- CHF 25–35m extra procurement costs in 2024

- 7% YoY reduction in scope 3 emissions intensity

Supply squeeze: commodity-driven COGS rise vs. GF’s contract, regional & green offsets

Suppliers hold moderate-to-strong power: commodity swings (Al +18%, PE +12% YTD through Q3 2025) raise COGS, niche electronic/sensor vendors and green-power providers demand premiums, and ocean carrier consolidation (top 10 = ~85% capacity) lifts freight; GF offsets with ~60% long-term contracts, 70% sensor sourcing under multi-year deals, regional production (‑12% shipment distance) and 18% spend on certified low-carbon suppliers.

| Metric | Value |

|---|---|

| Al price change (YTD Q3 2025) | +18% |

| Polyethylene (YTD Q3 2025) | +12% |

| Volumes under long-term contracts | ~60% |

| Sensor sourcing multi-year | 70% |

| Top 10 carriers capacity (2025) | ~85% |

| Shipment distance change since 2020 | -12% |

| Spend on certified low-carbon suppliers (2024) | 18% |

What is included in the product

Tailored exclusively for Georg Fischer, this Porter's Five Forces overview uncovers competitive intensity, supplier and buyer power, entry barriers, substitute threats, and emerging disruptors, with strategic implications for its pricing, profitability, and market positioning.

Compact Porter's Five Forces for Georg Fischer—quickly spot bargaining power, rivalry, and supplier risks to streamline strategic decisions and investor briefings.

Customers Bargaining Power

Concentration of automotive and aerospace OEMs

In Casting Solutions, roughly 60% of 2024 revenue came from about 10 large automotive and aerospace OEMs, concentrating buyer power and letting customers demand lower prices and higher quality, squeezing margins during renewals.

By 2025, EV adoption increased lightweight-part sourcing: OEM requests for aluminum components rose ~18% YoY, intensifying price and specification pressure on Georg Fischer and raising supplier switching risk.

Fragmented buyer base in Piping Systems

The GF Piping Systems division serves a diverse, fragmented buyer base—utilities, construction firms, and industrial plants—so individual buyer power is low; GF reported CHF 2.9bn group sales in 2024, with piping a material share. Large infrastructure contracts can push for volume discounts, but GF’s leak‑proof, corrosion‑resistant solutions command premium pricing tied to reliability and lifecycle costs. Customers prioritize long‑term performance over lowest upfront price, lowering churn and strengthening margins.

High switching costs in Machining Solutions

Customers face high switching costs with GF Machining Solutions because proprietary software and specialist training bind users to its EDM and milling systems; studies show tech-switch projects can cost manufacturers 5–15% of annual production value and take 3–9 months of downtime. After adoption, production-cycle disruption and requalification risks make switching unlikely, creating technological lock-in that shields GF from aggressive price-driven churn and supports margin stability—GF reported 2024 aftermarket revenue resilience at ~28% of segment sales.

Total cost of ownership focus

Sophisticated buyers in 2025 focus on total cost of ownership—maintenance, energy use, and lifespan—over sticker price; industry surveys show 68% of professional purchasers cite TCO as primary buying criterion. GF uses its reputation for durable castings and piping to justify 8–15% premium pricing in EU and North America. Its service contracts and digital monitoring (reducing downtime by ~12% per GF case studies) strengthen ties with value-conscious buyers.

- 68% cite TCO as key in 2025

- GF premium pricing 8–15%

- Digital monitoring cuts downtime ~12%

- Service packages boost renewal rates

Digitalization and price transparency

The rise of digital procurement platforms and price transparency lets large buyers compare Georg Fischer (GF) products with global rivals, raising customer bargaining power; procurement platforms showed a 22% YoY increase in industrial listings in 2024, widening comparison. GF responded with ~CHF 80m invested in digital sales/CRM through 2023–24 to deliver personalized value and capture higher-margin service revenue. These tools enable tailored solutions and remote technical support, shifting competition from price to integrated service.

- 22% YoY rise in industrial procurement listings (2024)

- GF digital/CRM investment ~CHF 80m (2023–24)

- Shift: product price → tailored solutions & support

Mixed buyer power: concentrated OEM pricing vs. high switching costs and TCO focus

Customer bargaining power is mixed: Casting Solutions sees high concentration (10 OEMs = ~60% 2024 revenue) pressing prices, while Piping buyers are fragmented and less price-sensitive; Machining users face high switching costs (5–15% production value, 3–9 months downtime) that protect margins. GF charges 8–15% premium; 68% buyers cite TCO; digital procurement rose 22% (2024), GF invested ~CHF 80m (2023–24).

| Metric | Value |

|---|---|

| Top-10 OEM share (Casting, 2024) | ~60% |

| OEM demand for aluminum parts (2025 YoY) | +18% |

| Switch cost impact | 5–15% annual value; 3–9 months |

| Buyers citing TCO (2025) | 68% |

| GF premium pricing | 8–15% |

| Procurement listings growth (2024) | +22% |

| Digital/CRM investment (2023–24) | ~CHF 80m |

Full Version Awaits

Georg Fischer Porter's Five Forces Analysis

This preview shows the exact Georg Fischer Porter's Five Forces analysis you'll receive immediately after purchase—no mockups, no placeholders, fully formatted and ready for use.