Gerresheimer Porter's Five Forces Analysis

Don't Miss the Bigger Picture

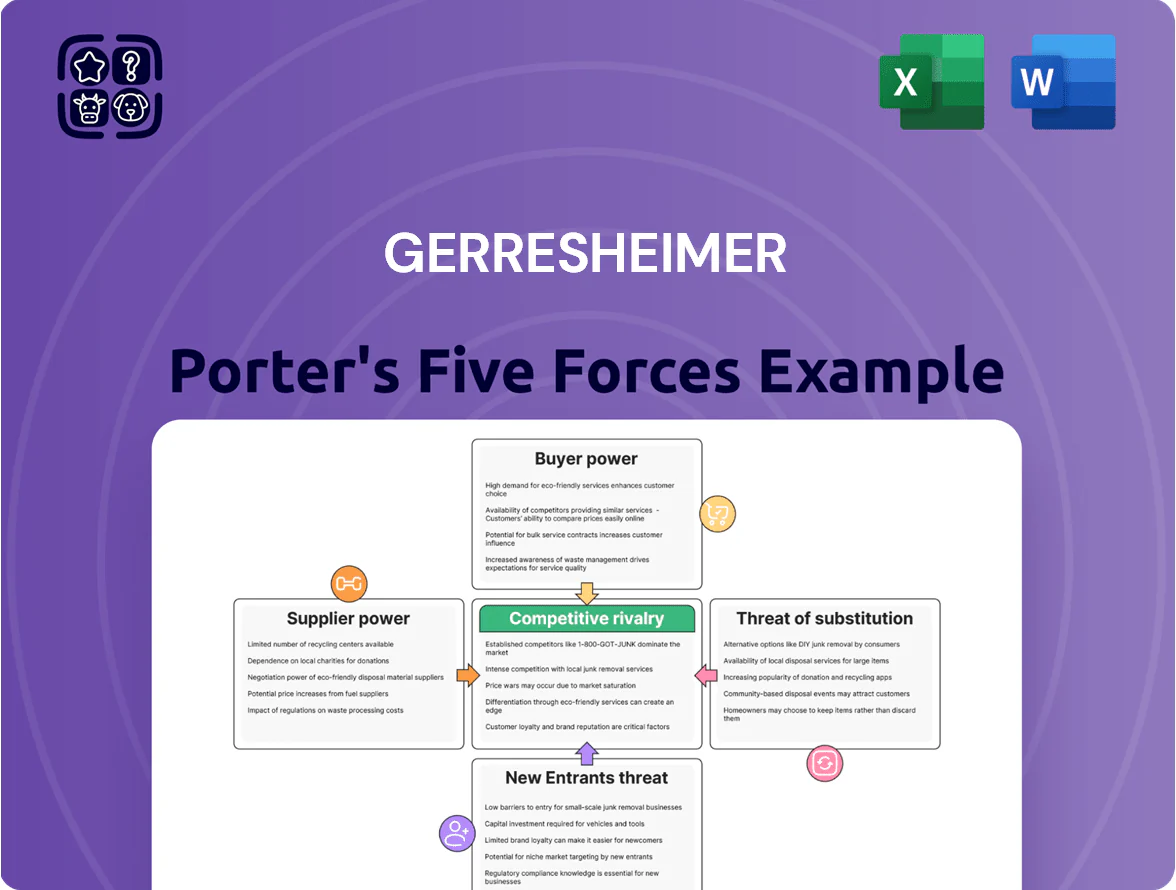

Gerresheimer faces moderate supplier power and high buyer scrutiny due to regulatory demands and quality expectations, while niche product differentiation limits substitute threats but raises R&D intensity.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Gerresheimer’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Energy Market Volatility

Gerresheimer’s specialty-glass furnaces are energy-intensive, so Europe’s 2024 average industrial gas price (about €0.09/kWh) and US industrial electricity at ~$0.07/kWh keep input costs sensitive despite hedges through 2025; energy suppliers therefore exert moderate bargaining power.

Raw Material Specialization

Gerresheimer needs high-purity quartz sand and medical-grade polymers to meet GxP standards, and roughly 70% of qualified suppliers are concentrated in three regions, giving them strong bargaining power; supplier-led price swings of 8–12% in 2024 pushed packaging input costs up 4.5% year-over-year, delaying some plants by 7–14 days when shipments were disrupted.

Specialized Manufacturing Equipment

Gerresheimer depends on specialized glass forming and cleanroom-grade injection molding equipment from a few global vendors, creating supplier concentration and reliance on proprietary tech and service contracts; about 60–70% of high-precision pharma-capital purchases worldwide come from top 3 suppliers, limiting bargaining power.

Regulatory Compliance Costs

Regulatory compliance—ISO 13485, EU MDR 2017/745, and FDA QSR—raises suppliers’ costs, with industry estimates showing supplier compliance adds 5–12% to COGS for medical-glass and pharma-component vendors as of 2024.

High regulatory burden deters entrants, so established suppliers gain leverage and often pass compliance costs to Gerresheimer, raising input prices and margin pressure.

Lengthy qualification/validation (often 6–12 months) locks Gerresheimer to current suppliers, boosting supplier stability and bargaining power.

- Compliance adds 5–12% to supplier COGS

- EU MDR/FDA rules concentrate suppliers

- Validation time 6–12 months, reducing switching

Logistics and Transport Costs

Gerresheimer’s global footprint makes freight providers critical; late-2025 container rates rose ~35% year-over-year on key lanes, letting carriers push higher surcharges and longer lead times.

Glass packaging is heavy and fragile, limiting modal switches and boosting dependence on specialized handlers; logistics firms’ pricing power raised transport cost share of COGS by an estimated 2–3 percentage points in 2025.

- Global container rate jump ~35% YoY (late-2025)

- Transport added ~2–3 ppt to COGS in 2025

- Low modal flexibility increases supplier leverage

Suppliers wield moderate–high power: concentrated, costly, slow-to-switch inputs

Suppliers hold moderate–high power: energy price sensitivity (EU gas €0.09/kWh 2024, US electricity $0.07/kWh) and supplier concentration (≈70% qualified suppliers in 3 regions; 60–70% pharma-capex from top 3 vendors) drive input-cost volatility (packaging +4.5% YoY 2024) and long qualification (6–12 months) that limits switching.

| Metric | 2024–25 |

|---|---|

| EU gas | €0.09/kWh (2024) |

| US electricity | $0.07/kWh (2024) |

| Supplier concentration | ≈70% in 3 regions |

| Packaging cost change | +4.5% YoY (2024) |

| Validation time | 6–12 months |

What is included in the product

Tailored exclusively for Gerresheimer, this Porter's Five Forces overview evaluates supplier and buyer power, competitive rivalry, threat of substitutes and new entrants, and highlights disruptive trends and market barriers shaping its pricing, profitability, and strategic defenses.

A concise, one-sheet Porter’s Five Forces snapshot for Gerresheimer—ideal for rapid strategic decisions and investor briefings.

Customers Bargaining Power

Concentration of Big Pharma

A large share of Gerresheimer’s revenue—about 25–30% in 2024—comes from a few pharma giants, including Novo Nordisk and Eli Lilly, giving these buyers strong leverage.

Their massive orders for GLP-1 delivery devices (pens, cartridges, syringes) let them demand volume discounts that compress Gerresheimer’s margins.

During contract renewals they can push price concessions; in 2024 price pressure reportedly trimmed mix-adjusted margins by ~150–200 basis points.

High Switching Costs

Once a drug delivery device or primary packaging is locked into a regulatory filing, changing suppliers can add months and costs—FDA/EMA revalidation and tech transfers often cost $1–5m and 6–18 months—so customers face high switching costs. This technical lock-in cuts customer bargaining power in commercialization, as buyers trade price pressure for supply certainty. Pharma firms prefer multi-year contracts and stability; industry surveys (2024) show 72% of firms prioritise supplier continuity over price.

Demand for Customization

Biotech and cosmetic clients now demand bespoke packaging for molecule-specific stability and delivery; 2024 industry surveys show 62% of biopharma projects require some co-development.

Co-development shifts Gerresheimer from vendor to strategic partner, reducing buyer leverage and supporting premium pricing—Gerresheimer reported 2024 packaging solutions revenue growth of ~9%.

High CapEx for customization forces Gerresheimer to seek multi-year volume commitments to protect margins; a 3–5 year contract target keeps ROI aligned with tooling costs.

Price Transparency and Tendering

Public healthcare systems and large hospital groups use competitive tendering for generic packaging, raising price transparency and forcing suppliers to undercut each other for vials and ampoules; EU tender data show average price drops of 15–30% in 2023 for standard parenteral packs.

This lets buyers play competitors off each other for standardized products, boosting customer leverage; Gerresheimer sees higher margin pressure in generic packaging versus specialized, patent-protected drug delivery devices where switching costs and design complexity keep buyer power lower.

Quality and Safety Standards

Customers in pharma set absolute quality and safety standards; a single packaging defect can trigger drug recalls—U.S. recalls rose 12% in 2024, costing firms millions—so buyers demand zero-defect supply and can withdraw preferred-supplier status or impose penalties for lapses.

That pressure forces Gerresheimer to invest in automated inspection: the company reported capital expenditure of €128 million in 2024, with ~15% allocated to quality automation, to meet clients’ non-negotiable demands.

- Zero-defect mandate: customer-controlled

- 2024 recall trend: +12% in U.S.

- Gerresheimer CapEx 2024: €128M; ~€19M to automation

- Penalty risk: loss of preferred status, financial fines

Pharma buying power trims standard prices; co‑dev and revalidation lock in suppliers

Large pharma account for ~25–30% of 2024 revenue, giving buyers strong leverage via volume discounts; tendering drove 15–30% price falls for standard packs (EU, 2023). Co-development demand (62% biopharma, 2024) and high switching costs (revalidation €1–5m, 6–18 months) reduce buyer power for specialized devices, while zero-defect demands raised Gerresheimer CapEx to €128m in 2024 (~€19m quality automation).

| Metric | Value |

|---|---|

| Pharma share | 25–30% (2024) |

| Tender price drops | 15–30% (EU, 2023) |

| Co‑dev demand | 62% (2024) |

| Revalidation cost/time | €1–5m; 6–18m |

| CapEx | €128m (2024); ~€19m quality |

Same Document Delivered

Gerresheimer Porter's Five Forces Analysis

This preview shows the exact Gerresheimer Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups.

The document displayed is the full, professionally formatted file, ready for download and use the moment you buy.

You're viewing the final deliverable: the same comprehensive analysis available instantly after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Gerresheimer faces moderate supplier power and high buyer scrutiny due to regulatory demands and quality expectations, while niche product differentiation limits substitute threats but raises R&D intensity.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Gerresheimer’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Energy Market Volatility

Gerresheimer’s specialty-glass furnaces are energy-intensive, so Europe’s 2024 average industrial gas price (about €0.09/kWh) and US industrial electricity at ~$0.07/kWh keep input costs sensitive despite hedges through 2025; energy suppliers therefore exert moderate bargaining power.

Raw Material Specialization

Gerresheimer needs high-purity quartz sand and medical-grade polymers to meet GxP standards, and roughly 70% of qualified suppliers are concentrated in three regions, giving them strong bargaining power; supplier-led price swings of 8–12% in 2024 pushed packaging input costs up 4.5% year-over-year, delaying some plants by 7–14 days when shipments were disrupted.

Specialized Manufacturing Equipment

Gerresheimer depends on specialized glass forming and cleanroom-grade injection molding equipment from a few global vendors, creating supplier concentration and reliance on proprietary tech and service contracts; about 60–70% of high-precision pharma-capital purchases worldwide come from top 3 suppliers, limiting bargaining power.

Regulatory Compliance Costs

Regulatory compliance—ISO 13485, EU MDR 2017/745, and FDA QSR—raises suppliers’ costs, with industry estimates showing supplier compliance adds 5–12% to COGS for medical-glass and pharma-component vendors as of 2024.

High regulatory burden deters entrants, so established suppliers gain leverage and often pass compliance costs to Gerresheimer, raising input prices and margin pressure.

Lengthy qualification/validation (often 6–12 months) locks Gerresheimer to current suppliers, boosting supplier stability and bargaining power.

- Compliance adds 5–12% to supplier COGS

- EU MDR/FDA rules concentrate suppliers

- Validation time 6–12 months, reducing switching

Logistics and Transport Costs

Gerresheimer’s global footprint makes freight providers critical; late-2025 container rates rose ~35% year-over-year on key lanes, letting carriers push higher surcharges and longer lead times.

Glass packaging is heavy and fragile, limiting modal switches and boosting dependence on specialized handlers; logistics firms’ pricing power raised transport cost share of COGS by an estimated 2–3 percentage points in 2025.

- Global container rate jump ~35% YoY (late-2025)

- Transport added ~2–3 ppt to COGS in 2025

- Low modal flexibility increases supplier leverage

Suppliers wield moderate–high power: concentrated, costly, slow-to-switch inputs

Suppliers hold moderate–high power: energy price sensitivity (EU gas €0.09/kWh 2024, US electricity $0.07/kWh) and supplier concentration (≈70% qualified suppliers in 3 regions; 60–70% pharma-capex from top 3 vendors) drive input-cost volatility (packaging +4.5% YoY 2024) and long qualification (6–12 months) that limits switching.

| Metric | 2024–25 |

|---|---|

| EU gas | €0.09/kWh (2024) |

| US electricity | $0.07/kWh (2024) |

| Supplier concentration | ≈70% in 3 regions |

| Packaging cost change | +4.5% YoY (2024) |

| Validation time | 6–12 months |

What is included in the product

Tailored exclusively for Gerresheimer, this Porter's Five Forces overview evaluates supplier and buyer power, competitive rivalry, threat of substitutes and new entrants, and highlights disruptive trends and market barriers shaping its pricing, profitability, and strategic defenses.

A concise, one-sheet Porter’s Five Forces snapshot for Gerresheimer—ideal for rapid strategic decisions and investor briefings.

Customers Bargaining Power

Concentration of Big Pharma

A large share of Gerresheimer’s revenue—about 25–30% in 2024—comes from a few pharma giants, including Novo Nordisk and Eli Lilly, giving these buyers strong leverage.

Their massive orders for GLP-1 delivery devices (pens, cartridges, syringes) let them demand volume discounts that compress Gerresheimer’s margins.

During contract renewals they can push price concessions; in 2024 price pressure reportedly trimmed mix-adjusted margins by ~150–200 basis points.

High Switching Costs

Once a drug delivery device or primary packaging is locked into a regulatory filing, changing suppliers can add months and costs—FDA/EMA revalidation and tech transfers often cost $1–5m and 6–18 months—so customers face high switching costs. This technical lock-in cuts customer bargaining power in commercialization, as buyers trade price pressure for supply certainty. Pharma firms prefer multi-year contracts and stability; industry surveys (2024) show 72% of firms prioritise supplier continuity over price.

Demand for Customization

Biotech and cosmetic clients now demand bespoke packaging for molecule-specific stability and delivery; 2024 industry surveys show 62% of biopharma projects require some co-development.

Co-development shifts Gerresheimer from vendor to strategic partner, reducing buyer leverage and supporting premium pricing—Gerresheimer reported 2024 packaging solutions revenue growth of ~9%.

High CapEx for customization forces Gerresheimer to seek multi-year volume commitments to protect margins; a 3–5 year contract target keeps ROI aligned with tooling costs.

Price Transparency and Tendering

Public healthcare systems and large hospital groups use competitive tendering for generic packaging, raising price transparency and forcing suppliers to undercut each other for vials and ampoules; EU tender data show average price drops of 15–30% in 2023 for standard parenteral packs.

This lets buyers play competitors off each other for standardized products, boosting customer leverage; Gerresheimer sees higher margin pressure in generic packaging versus specialized, patent-protected drug delivery devices where switching costs and design complexity keep buyer power lower.

Quality and Safety Standards

Customers in pharma set absolute quality and safety standards; a single packaging defect can trigger drug recalls—U.S. recalls rose 12% in 2024, costing firms millions—so buyers demand zero-defect supply and can withdraw preferred-supplier status or impose penalties for lapses.

That pressure forces Gerresheimer to invest in automated inspection: the company reported capital expenditure of €128 million in 2024, with ~15% allocated to quality automation, to meet clients’ non-negotiable demands.

- Zero-defect mandate: customer-controlled

- 2024 recall trend: +12% in U.S.

- Gerresheimer CapEx 2024: €128M; ~€19M to automation

- Penalty risk: loss of preferred status, financial fines

Pharma buying power trims standard prices; co‑dev and revalidation lock in suppliers

Large pharma account for ~25–30% of 2024 revenue, giving buyers strong leverage via volume discounts; tendering drove 15–30% price falls for standard packs (EU, 2023). Co-development demand (62% biopharma, 2024) and high switching costs (revalidation €1–5m, 6–18 months) reduce buyer power for specialized devices, while zero-defect demands raised Gerresheimer CapEx to €128m in 2024 (~€19m quality automation).

| Metric | Value |

|---|---|

| Pharma share | 25–30% (2024) |

| Tender price drops | 15–30% (EU, 2023) |

| Co‑dev demand | 62% (2024) |

| Revalidation cost/time | €1–5m; 6–18m |

| CapEx | €128m (2024); ~€19m quality |

Same Document Delivered

Gerresheimer Porter's Five Forces Analysis

This preview shows the exact Gerresheimer Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups.

The document displayed is the full, professionally formatted file, ready for download and use the moment you buy.

You're viewing the final deliverable: the same comprehensive analysis available instantly after payment.